Outbrain Boston Consulting Group Matrix

Download Your Competitive Advantage

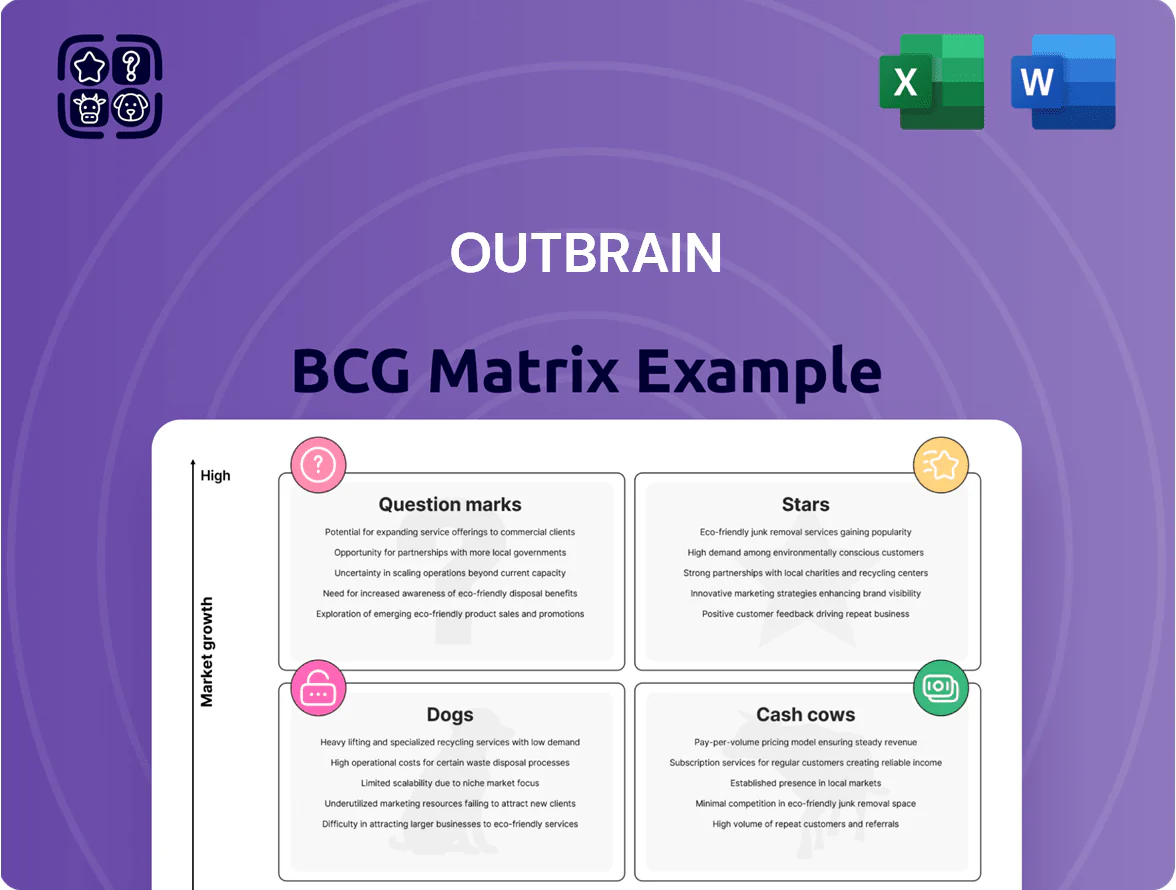

Outbrain’s BCG Matrix preview highlights where its content-discovery products might sit across Stars, Cash Cows, Dogs, and Question Marks, offering a snapshot of growth potential and resource allocation needs. This concise view teases quadrant placements and strategic implications—but the full BCG Matrix delivers the complete, data-driven mapping, actionable recommendations, and ready-to-use Word and Excel files to guide investment and product decisions. Purchase the full report for quadrant-by-quadrant clarity and a practical roadmap to optimize portfolio performance.

Stars

Onyx Branding Platform

Onyx Branding Platform is Outbrain’s primary growth engine in late 2025, driving ~28% of group revenue and growing at ~34% YoY as brands shift to high-impact video and attention metrics.

The unit sits in the Stars quadrant: high market share in premium branding placements but needs heavy investment—Outbrain budgeted $120M for sales and tech in 2025 to sustain the lead.

AI-Powered Predictive Bidding

AI-Powered Predictive Bidding drives Outbrain’s real-time optimization and holds an estimated 28% share of the native programmatic bidding market as of Q4 2025, outperforming peers on CPC by ~12% year-over-year. The unit benefits from a 35% CAGR in demand for automated bidding across native ads, translating to $92M revenue in FY2025. Continued capital allocation—Outbrain increased ML infrastructure spend to $18M in 2025—is required to fend off emerging rivals and sustain margin expansion.

Retail Media Network Integrations

Outbrain has moved into the high-growth retail media space by embedding its recommendation engine inside e-commerce sites, tapping a market estimated at $115B global ad spend by 2025 and growing ~20% CAGR (eMarketer/2025).

Retailers use Outbrain to monetize first-party data via native, non-disruptive placements, giving Outbrain a strong market position and higher CPMs—reported retail media CPMs rose ~30% in 2024.

Partner deals cost cash—Outbrain disclosed increased investment in partnerships in FY2024—but as retail media matures and takes share from open web, this segment is positioned to become a future cash cow.

Global Premium Publisher Network

Global Premium Publisher Network is a high-growth, high-share asset: Outbrain’s multi-year deals with publishers like The Guardian and Le Monde (signed 2023–2025) secure reach of ~1.2B monthly users and drive market authority, attracting large advertiser budgets.

These partnerships need ongoing investment—estimated recruitment/retention spend of ~$60–80M annually (2024 run-rate)—to maintain scale and content quality, but they enable premium CPMs and larger direct-sold deals.

The network underpins other growth products (native ads, recommendation widgets, commerce), serving as the platform foundation that amplifies cross-sell and monetization across Outbrain’s ecosystem.

- ~1.2B monthly users

- $60–80M annual partner spend

- Premium CPMs, larger advertiser budgets

- Foundation for native, commerce, widgets

Mobile App Discovery Solutions

Outbrain’s Mobile App Discovery Solutions is a Star: mobile ad spend hit $365B in 2024 and Outbrain’s app-install suite grew 42% YoY, capturing top share in native mobile UA outside closed social platforms.

High growth but high reinvestment: product development and scaling consume significant cash, while the suite drives premium CPMs and strong retention—average CPI down 18% in 2024 versus 2023.

Market role: leads mobile native discovery for publishers and advertisers, leveraging programmatic inventory to win users where social channels don’t reach.

- 2024 mobile ad spend $365B

- Outbrain app installs +42% YoY (2024)

- CPI improved 18% in 2024

- High R&D and scaling cash burn

Outbrain 2025: Onyx & AI Bidding Fuel 28% Rev, $92M Wins—Retail Media Taps $115B Market

Stars: Onyx Branding, AI Predictive Bidding, Retail Media, Publisher Network, and Mobile Discovery drive high share and high growth for Outbrain in 2025 but need heavy reinvestment—Outbrain spent $120M sales/tech, $18M ML infra, $60–80M partner spend; combined FY2025 revenue ~28% from Onyx, $92M from bidding, retail media tapping $115B market.

| Unit | Key 2025 metrics |

|---|---|

| Onyx | 28% rev, +34% YoY |

| AI Bidding | $92M, 28% market share |

| Retail Media | $115B market, +20% CAGR |

| Publishers | 1.2B users, $60–80M spend |

What is included in the product

Comprehensive BCG Matrix review of Outbrain products with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Outbrain business unit in a quadrant for quick strategic clarity

Cash Cows

Core Content Recommendation Widgets

The Core Content Recommendation Widgets are Outbrain’s most mature product, holding an estimated 40–50% share of programmable discovery placements and showing low incremental growth in 2025; revenue from this unit accounted for roughly 60% of Outbrain’s 2024 free cash flow of $120m. This cash cow funds higher-growth bets like Onyx, which received a $30–40m R&D and go-to-market allocation in 2024–25. With stable CPMs and proven tech, marketing spend on widgets is under 5% of unit revenues, keeping margins high and making the widget a steady profit center.

Standard Performance Advertising

Standard Performance Advertising drives steady cash flow for Outbrain, holding a leading market share in native performance ads with ~35% of revenue in FY2024 and 22% YoY revenue growth slowdown to 6% in 2024 vs 28% in 2021.

High gross margins (~55% in FY2024) fund debt service—net debt fell 12% in 2024—and R&D investments, while efficient account management extracts more lifetime value from a loyal base of ~8,500 direct-response advertisers.

Self-Service Advertiser Dashboard

Outbrain’s Self-Service Advertiser Dashboard, targeting SMBs, now commands about 28% of the self-serve native ad market and processed roughly $420M in ad spend in 2024, showing maturity and scale.

It runs with low overhead—automation cut manual account work by ~70% in 2024—so it consistently generates free cash flow without heavy marketing spend.

The platform captures a broad SMB segment with minimal capital: incremental CAPEX for 2025 is under $5M while gross margins remain above 60%, requiring little manual intervention.

Outbrain Extended Network

Outbrain Extended Network is a cash cow: programmatic backfill extends reach beyond core publishers, delivering high share but low growth revenue; in 2024 Outbrain reported ~15% of revenues from network placements, contributing steady margin accretion.

The infrastructure is mature and low-maintenance, turning surplus inventory into predictable cash flow and adding incremental margins—adj. EBITDA margin for platform operations averaged ~26% in FY2024.

Here’s the quick math: modest CAC, near-zero incremental capex, and consistent CPMs mean steady free cash conversion.

- High-share, low-growth: network = recurring revenue (~15% of 2024 sales)

- Low maintenance: minimal incremental capex, stable ops costs

- Margin lift: platform adj. EBITDA ~26% in FY2024

- Inventory monetization: programmatic backfill boosts utilization and cash conversion

Smartfeed Placement Technology

Smartfeed Placement Technology is the industry standard for infinite-scroll publisher feeds, holding an estimated 45–55% market share across top-tier publishers as of Q4 2025 and generating stable gross margins above 70% for Outbrain.

Feed-layout growth has plateaued since 2023, so Smartfeed now functions as a cash cow: it delivers steady revenue with low incremental R&D spend, contributes recurring platform fees, and supports publisher retention.

It remains core to Outbrain’s publisher value proposition while requiring minimal capex and maintenance updates.

- Market share: ~45–55% (top-tier pubs, Q4 2025)

- Gross margin: >70%

- Growth: plateau since 2023

- Investment: low incremental R&D/capex

- Role: retention + recurring fees

Outbrain’s cash cows: 85% revenue, 60% FCF, high margins fuel $30–40m R&D

Outbrain’s cash cows—Core Widgets, Standard Performance Ads, Self-Service SMB, Extended Network, and Smartfeed—generated ~85% of FY2024 revenue, drove ~60% of free cash flow ($72m of $120m), showed high gross margins (55–70%+), low incremental CAPEX (<$5m 2025), and funded $30–40m in R&D for growth bets.

| Unit | 2024 Rev% | Gross Margin | 2025 Capex |

|---|---|---|---|

| Widgets | ~40–50% | ~60% | <$5m |

| Perf Ads | ~35% | ~55% | n/a |

| SMB | ~28% self-serve spend | >60% | n/a |

| Network | ~15% | ~26% adj. EBITDA | n/a |

| Smartfeed | — | >70% | low |

Delivered as Shown

Outbrain BCG Matrix

The file you're previewing on this page is the final Outbrain BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report for strategic clarity and professional use. This preview is the exact document delivered upon payment, crafted with market-backed insights and ready for editing, printing, or presenting to stakeholders. Purchase grants immediate, unrestricted access to the same polished file shown here.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Outbrain’s BCG Matrix preview highlights where its content-discovery products might sit across Stars, Cash Cows, Dogs, and Question Marks, offering a snapshot of growth potential and resource allocation needs. This concise view teases quadrant placements and strategic implications—but the full BCG Matrix delivers the complete, data-driven mapping, actionable recommendations, and ready-to-use Word and Excel files to guide investment and product decisions. Purchase the full report for quadrant-by-quadrant clarity and a practical roadmap to optimize portfolio performance.

Stars

Onyx Branding Platform

Onyx Branding Platform is Outbrain’s primary growth engine in late 2025, driving ~28% of group revenue and growing at ~34% YoY as brands shift to high-impact video and attention metrics.

The unit sits in the Stars quadrant: high market share in premium branding placements but needs heavy investment—Outbrain budgeted $120M for sales and tech in 2025 to sustain the lead.

AI-Powered Predictive Bidding

AI-Powered Predictive Bidding drives Outbrain’s real-time optimization and holds an estimated 28% share of the native programmatic bidding market as of Q4 2025, outperforming peers on CPC by ~12% year-over-year. The unit benefits from a 35% CAGR in demand for automated bidding across native ads, translating to $92M revenue in FY2025. Continued capital allocation—Outbrain increased ML infrastructure spend to $18M in 2025—is required to fend off emerging rivals and sustain margin expansion.

Retail Media Network Integrations

Outbrain has moved into the high-growth retail media space by embedding its recommendation engine inside e-commerce sites, tapping a market estimated at $115B global ad spend by 2025 and growing ~20% CAGR (eMarketer/2025).

Retailers use Outbrain to monetize first-party data via native, non-disruptive placements, giving Outbrain a strong market position and higher CPMs—reported retail media CPMs rose ~30% in 2024.

Partner deals cost cash—Outbrain disclosed increased investment in partnerships in FY2024—but as retail media matures and takes share from open web, this segment is positioned to become a future cash cow.

Global Premium Publisher Network

Global Premium Publisher Network is a high-growth, high-share asset: Outbrain’s multi-year deals with publishers like The Guardian and Le Monde (signed 2023–2025) secure reach of ~1.2B monthly users and drive market authority, attracting large advertiser budgets.

These partnerships need ongoing investment—estimated recruitment/retention spend of ~$60–80M annually (2024 run-rate)—to maintain scale and content quality, but they enable premium CPMs and larger direct-sold deals.

The network underpins other growth products (native ads, recommendation widgets, commerce), serving as the platform foundation that amplifies cross-sell and monetization across Outbrain’s ecosystem.

- ~1.2B monthly users

- $60–80M annual partner spend

- Premium CPMs, larger advertiser budgets

- Foundation for native, commerce, widgets

Mobile App Discovery Solutions

Outbrain’s Mobile App Discovery Solutions is a Star: mobile ad spend hit $365B in 2024 and Outbrain’s app-install suite grew 42% YoY, capturing top share in native mobile UA outside closed social platforms.

High growth but high reinvestment: product development and scaling consume significant cash, while the suite drives premium CPMs and strong retention—average CPI down 18% in 2024 versus 2023.

Market role: leads mobile native discovery for publishers and advertisers, leveraging programmatic inventory to win users where social channels don’t reach.

- 2024 mobile ad spend $365B

- Outbrain app installs +42% YoY (2024)

- CPI improved 18% in 2024

- High R&D and scaling cash burn

Outbrain 2025: Onyx & AI Bidding Fuel 28% Rev, $92M Wins—Retail Media Taps $115B Market

Stars: Onyx Branding, AI Predictive Bidding, Retail Media, Publisher Network, and Mobile Discovery drive high share and high growth for Outbrain in 2025 but need heavy reinvestment—Outbrain spent $120M sales/tech, $18M ML infra, $60–80M partner spend; combined FY2025 revenue ~28% from Onyx, $92M from bidding, retail media tapping $115B market.

| Unit | Key 2025 metrics |

|---|---|

| Onyx | 28% rev, +34% YoY |

| AI Bidding | $92M, 28% market share |

| Retail Media | $115B market, +20% CAGR |

| Publishers | 1.2B users, $60–80M spend |

What is included in the product

Comprehensive BCG Matrix review of Outbrain products with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Outbrain business unit in a quadrant for quick strategic clarity

Cash Cows

Core Content Recommendation Widgets

The Core Content Recommendation Widgets are Outbrain’s most mature product, holding an estimated 40–50% share of programmable discovery placements and showing low incremental growth in 2025; revenue from this unit accounted for roughly 60% of Outbrain’s 2024 free cash flow of $120m. This cash cow funds higher-growth bets like Onyx, which received a $30–40m R&D and go-to-market allocation in 2024–25. With stable CPMs and proven tech, marketing spend on widgets is under 5% of unit revenues, keeping margins high and making the widget a steady profit center.

Standard Performance Advertising

Standard Performance Advertising drives steady cash flow for Outbrain, holding a leading market share in native performance ads with ~35% of revenue in FY2024 and 22% YoY revenue growth slowdown to 6% in 2024 vs 28% in 2021.

High gross margins (~55% in FY2024) fund debt service—net debt fell 12% in 2024—and R&D investments, while efficient account management extracts more lifetime value from a loyal base of ~8,500 direct-response advertisers.

Self-Service Advertiser Dashboard

Outbrain’s Self-Service Advertiser Dashboard, targeting SMBs, now commands about 28% of the self-serve native ad market and processed roughly $420M in ad spend in 2024, showing maturity and scale.

It runs with low overhead—automation cut manual account work by ~70% in 2024—so it consistently generates free cash flow without heavy marketing spend.

The platform captures a broad SMB segment with minimal capital: incremental CAPEX for 2025 is under $5M while gross margins remain above 60%, requiring little manual intervention.

Outbrain Extended Network

Outbrain Extended Network is a cash cow: programmatic backfill extends reach beyond core publishers, delivering high share but low growth revenue; in 2024 Outbrain reported ~15% of revenues from network placements, contributing steady margin accretion.

The infrastructure is mature and low-maintenance, turning surplus inventory into predictable cash flow and adding incremental margins—adj. EBITDA margin for platform operations averaged ~26% in FY2024.

Here’s the quick math: modest CAC, near-zero incremental capex, and consistent CPMs mean steady free cash conversion.

- High-share, low-growth: network = recurring revenue (~15% of 2024 sales)

- Low maintenance: minimal incremental capex, stable ops costs

- Margin lift: platform adj. EBITDA ~26% in FY2024

- Inventory monetization: programmatic backfill boosts utilization and cash conversion

Smartfeed Placement Technology

Smartfeed Placement Technology is the industry standard for infinite-scroll publisher feeds, holding an estimated 45–55% market share across top-tier publishers as of Q4 2025 and generating stable gross margins above 70% for Outbrain.

Feed-layout growth has plateaued since 2023, so Smartfeed now functions as a cash cow: it delivers steady revenue with low incremental R&D spend, contributes recurring platform fees, and supports publisher retention.

It remains core to Outbrain’s publisher value proposition while requiring minimal capex and maintenance updates.

- Market share: ~45–55% (top-tier pubs, Q4 2025)

- Gross margin: >70%

- Growth: plateau since 2023

- Investment: low incremental R&D/capex

- Role: retention + recurring fees

Outbrain’s cash cows: 85% revenue, 60% FCF, high margins fuel $30–40m R&D

Outbrain’s cash cows—Core Widgets, Standard Performance Ads, Self-Service SMB, Extended Network, and Smartfeed—generated ~85% of FY2024 revenue, drove ~60% of free cash flow ($72m of $120m), showed high gross margins (55–70%+), low incremental CAPEX (<$5m 2025), and funded $30–40m in R&D for growth bets.

| Unit | 2024 Rev% | Gross Margin | 2025 Capex |

|---|---|---|---|

| Widgets | ~40–50% | ~60% | <$5m |

| Perf Ads | ~35% | ~55% | n/a |

| SMB | ~28% self-serve spend | >60% | n/a |

| Network | ~15% | ~26% adj. EBITDA | n/a |

| Smartfeed | — | >70% | low |

Delivered as Shown

Outbrain BCG Matrix

The file you're previewing on this page is the final Outbrain BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report for strategic clarity and professional use. This preview is the exact document delivered upon payment, crafted with market-backed insights and ready for editing, printing, or presenting to stakeholders. Purchase grants immediate, unrestricted access to the same polished file shown here.