Occidental Petroleum Business Model Canvas

Occidental Petroleum Business Model Canvas: Key Insights, Risks & Downloadable Toolkit

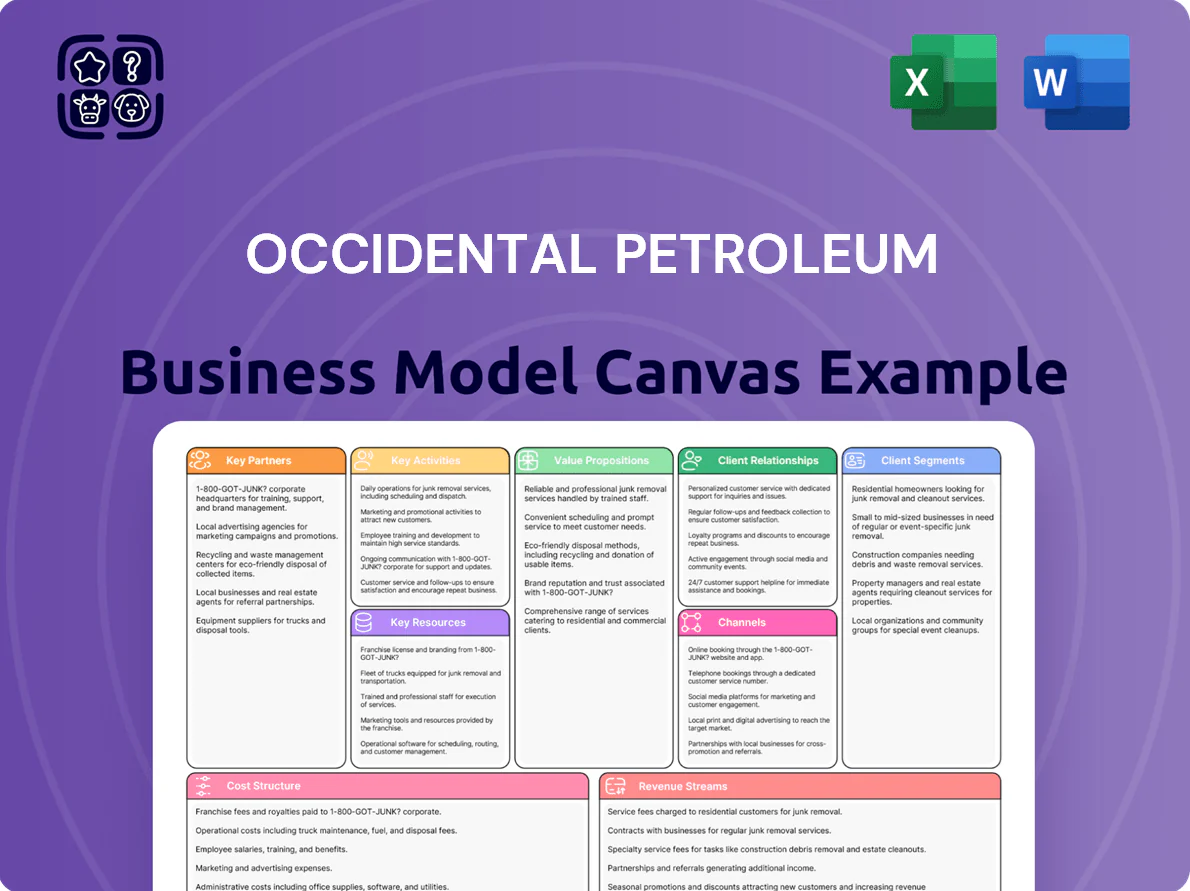

Explore a concise snapshot of Occidental Petroleum’s Business Model Canvas—covering its value propositions, key activities, partnerships, and revenue drivers to reveal how the company captures energy market value.

This preview highlights strategic strengths and risks; download the full, editable Canvas in Word and Excel for a section-by-section breakdown, financial implications, and benchmarking tools.

Perfect for investors, consultants, and strategists seeking actionable insights—get the complete document to accelerate analysis and decision-making.

Partnerships

Strategic Investment from Berkshire Hathaway

Berkshire Hathaway, via $10bn preferred equity agreed in 2019 and roughly 19% common equity stake as of 2025, supplies capital stability that enabled the $38bn Anadarko buyout and underwrote CrownRock integration financing in 2023–24.

Joint Ventures with National Oil Companies

Occidental holds long-term joint ventures with ADNOC (UAE) and state agencies in Oman and Qatar, sharing capital and operational risk on large E&P projects and securing multi-decade concessions; ADNOC JV projects contributed to Oxy’s international production, helping sustain its 2024 Permian-adjusted output after the 2022 acquisition of Anadarko.

Carbon Capture Technology Alliances

Through 1PointFive, Occidental partners with tech providers and EPC firms to scale Direct Air Capture (DAC) and CO2 sequestration hubs—targeting 70+ Mtpa project pipeline by 2035 and building cost curves toward ~$100–200/t CO2; these alliances underpin carbon management as a standalone line and joint deals with industrial emitters (chemicals, power, cement) secure offtake and a developing customer network for future carbon removal services.

Midstream and Infrastructure Partners

Academic and Research Collaborations

Occidental partners with top universities and labs to advance enhanced oil recovery (EOR) and subsurface modeling, improving CO2 injection efficiency and extending mature-field life; R&D collaborations helped raise Oxy’s CO2 storage efficiency by an estimated 8–12% in pilot projects through 2024.

- Reduced CO2 per barrel by ~0.1–0.2 tonnes in pilots (2023–24)

- 8–12% uplift in recovery in mature fields

- Partnerships include geophysics and chemical engineering programs

Berkshire-Backed Anadarko Deal Spurs Global E&P, DAC Scale & Permian Capacity

Berkshire Hathaway (2019 $10bn preferred; ~19% common, 2025) provides capital stability for the $38bn Anadarko deal and CrownRock financing; ADNOC and Gulf state JVs supply multi-decade concessions and international production support; 1PointFive partnerships target 70+ Mtpa DAC pipeline by 2035 with cost goal ~$100–200/t CO2; Western Midstream secures Permian takeaway capacity (~1.9 MMboe/d target, 2025).

| Partner | Role | Key 2024–25 Data |

|---|---|---|

| Berkshire Hathaway | Capital backer | $10bn pref; ~19% stake (2025) |

| ADNOC & Gulf JVs | E&P, concessions | Supports international production post-Anadarko |

| 1PointFive | DAC & CCS scale-up | 70+ Mtpa pipeline by 2035; $100–200/t target |

| Western Midstream | Takeaway/logistics | Aligns with ~1.9 MMboe/d Permian target (2025) |

| Universities/Labs | R&D (EOR) | 8–12% recovery uplift in pilots (2023–24) |

What is included in the product

A concise Business Model Canvas for Occidental Petroleum detailing customer segments, value propositions, channels, key activities, resources, partners, cost structure and revenue streams, aligned with its upstream oil & gas, midstream, and carbon management strategies to inform investors and analysts.

High-level view of Occidental Petroleum’s business model with editable cells to quickly pinpoint value drivers, cost centers, and carbon-management initiatives.

Activities

Upstream Exploration and Production

Occidental’s upstream focuses on identifying, drilling, and extracting crude oil, natural gas, and NGLs across domestic and international basins, with late-2025 portfolio tilt to high-margin Permian Basin and Gulf of Mexico acreage; Permian production averaged ~730,000 boe/d in 2025 and helped lower company-wide breakeven toward ~$35–40/boe. Continuous well-design and extended-lateral drilling raised average recovery and cut per-well costs ~12% year-over-year.

Chemical Manufacturing through OxyChem

Occidental’s OxyChem makes chlorine, caustic soda and PVC resins, supplying industries from construction to water treatment and generating about $2.1 billion in 2024 segment sales, giving Occidental vertical integration and a hedge when oil prices swing.

Primary focus: optimize complex supply chains, maintain 23 North American plants (2025 count) and control feedstock logistics to protect margins and cash flow during upstream volatility.

Low Carbon Venture Development

Occidental directs a large share of its capital and staff to carbon capture, utilization, and storage (CCUS), spending about $1.5–2.0 billion annually in 2024–2025 on projects and R&D; this includes building the 70,000 tCO2/yr pilot Stratos direct air capture (DAC) facility in Texas as part of a planned scale-up to >1 MtCO2/yr by 2030. These activities shift Occidental toward a carbon-managed energy model aligned with net-zero targets and expected to generate new revenue from carbon credits and enhanced oil recovery CO2 sales.

Enhanced Oil Recovery Operations

Capital Allocation and Debt Management

Occidental’s management targets shareholder returns, debt paydown, and reinvestment in high-return projects—after the 2019 Anadarko deal and later bolt-ons they prioritized de‑leveraging to regain and keep investment‑grade ratings, cutting net debt from about $40bn (2020) toward ~$25bn by Q4 2025 while funding Permian high-return drilling.

They use rigorous financial models and portfolio high‑grading to steer capital to accretive projects, targeting returns above WACC and maintaining free cash flow cover for buybacks and capex.

- Net debt reduction: ~$40bn (2020) → ~25bn (Q4 2025)

- Focus: Permian oil projects with >15% IRR target

- Priority: investment‑grade rating maintenance

- Tools: scenario models, portfolio high‑grading, FCF cover metrics

Integrated Permian growth: 730k boe/d, $2.1B OxyChem, CCUS scale & $15B debt cut

Upstream exploration, drilling, and production (Permian ~730,000 boe/d in 2025); OxyChem chemicals manufacturing (~$2.1bn sales in 2024) and 23 North American plants; CCUS/DAC and CO2 EOR (spent ~$1.5–2.0bn annually; Stratos 70,000 tCO2/yr pilot; ~300,000 t/day CO2 injected) plus capital allocation for debt cut (~$40bn→~$25bn net debt by Q4 2025) and >15% IRR Permian projects.

| Metric | Value |

|---|---|

| Permian prod (2025) | ~730,000 boe/d |

| OxyChem sales (2024) | $2.1bn |

| CCUS spend (2024–25) | $1.5–2.0bn/yr |

| Stratos DAC | 70,000 tCO2/yr |

| CO2 injected (EOR) | ~300,000 t/day |

| Net debt | $40bn→$25bn (Q4 2025) |

| Permian IRR target | >15% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Occidental Petroleum Business Model Canvas you will receive after purchase — not a mockup or sample — and it contains the same structured, editable content shown in this snapshot. Upon completing your order, you’ll instantly download the full file, formatted and ready for analysis, presentation, or customization in Word and Excel. What you see is what you’ll own, with all sections included and no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Occidental Petroleum Business Model Canvas: Key Insights, Risks & Downloadable Toolkit

Explore a concise snapshot of Occidental Petroleum’s Business Model Canvas—covering its value propositions, key activities, partnerships, and revenue drivers to reveal how the company captures energy market value.

This preview highlights strategic strengths and risks; download the full, editable Canvas in Word and Excel for a section-by-section breakdown, financial implications, and benchmarking tools.

Perfect for investors, consultants, and strategists seeking actionable insights—get the complete document to accelerate analysis and decision-making.

Partnerships

Strategic Investment from Berkshire Hathaway

Berkshire Hathaway, via $10bn preferred equity agreed in 2019 and roughly 19% common equity stake as of 2025, supplies capital stability that enabled the $38bn Anadarko buyout and underwrote CrownRock integration financing in 2023–24.

Joint Ventures with National Oil Companies

Occidental holds long-term joint ventures with ADNOC (UAE) and state agencies in Oman and Qatar, sharing capital and operational risk on large E&P projects and securing multi-decade concessions; ADNOC JV projects contributed to Oxy’s international production, helping sustain its 2024 Permian-adjusted output after the 2022 acquisition of Anadarko.

Carbon Capture Technology Alliances

Through 1PointFive, Occidental partners with tech providers and EPC firms to scale Direct Air Capture (DAC) and CO2 sequestration hubs—targeting 70+ Mtpa project pipeline by 2035 and building cost curves toward ~$100–200/t CO2; these alliances underpin carbon management as a standalone line and joint deals with industrial emitters (chemicals, power, cement) secure offtake and a developing customer network for future carbon removal services.

Midstream and Infrastructure Partners

Academic and Research Collaborations

Occidental partners with top universities and labs to advance enhanced oil recovery (EOR) and subsurface modeling, improving CO2 injection efficiency and extending mature-field life; R&D collaborations helped raise Oxy’s CO2 storage efficiency by an estimated 8–12% in pilot projects through 2024.

- Reduced CO2 per barrel by ~0.1–0.2 tonnes in pilots (2023–24)

- 8–12% uplift in recovery in mature fields

- Partnerships include geophysics and chemical engineering programs

Berkshire-Backed Anadarko Deal Spurs Global E&P, DAC Scale & Permian Capacity

Berkshire Hathaway (2019 $10bn preferred; ~19% common, 2025) provides capital stability for the $38bn Anadarko deal and CrownRock financing; ADNOC and Gulf state JVs supply multi-decade concessions and international production support; 1PointFive partnerships target 70+ Mtpa DAC pipeline by 2035 with cost goal ~$100–200/t CO2; Western Midstream secures Permian takeaway capacity (~1.9 MMboe/d target, 2025).

| Partner | Role | Key 2024–25 Data |

|---|---|---|

| Berkshire Hathaway | Capital backer | $10bn pref; ~19% stake (2025) |

| ADNOC & Gulf JVs | E&P, concessions | Supports international production post-Anadarko |

| 1PointFive | DAC & CCS scale-up | 70+ Mtpa pipeline by 2035; $100–200/t target |

| Western Midstream | Takeaway/logistics | Aligns with ~1.9 MMboe/d Permian target (2025) |

| Universities/Labs | R&D (EOR) | 8–12% recovery uplift in pilots (2023–24) |

What is included in the product

A concise Business Model Canvas for Occidental Petroleum detailing customer segments, value propositions, channels, key activities, resources, partners, cost structure and revenue streams, aligned with its upstream oil & gas, midstream, and carbon management strategies to inform investors and analysts.

High-level view of Occidental Petroleum’s business model with editable cells to quickly pinpoint value drivers, cost centers, and carbon-management initiatives.

Activities

Upstream Exploration and Production

Occidental’s upstream focuses on identifying, drilling, and extracting crude oil, natural gas, and NGLs across domestic and international basins, with late-2025 portfolio tilt to high-margin Permian Basin and Gulf of Mexico acreage; Permian production averaged ~730,000 boe/d in 2025 and helped lower company-wide breakeven toward ~$35–40/boe. Continuous well-design and extended-lateral drilling raised average recovery and cut per-well costs ~12% year-over-year.

Chemical Manufacturing through OxyChem

Occidental’s OxyChem makes chlorine, caustic soda and PVC resins, supplying industries from construction to water treatment and generating about $2.1 billion in 2024 segment sales, giving Occidental vertical integration and a hedge when oil prices swing.

Primary focus: optimize complex supply chains, maintain 23 North American plants (2025 count) and control feedstock logistics to protect margins and cash flow during upstream volatility.

Low Carbon Venture Development

Occidental directs a large share of its capital and staff to carbon capture, utilization, and storage (CCUS), spending about $1.5–2.0 billion annually in 2024–2025 on projects and R&D; this includes building the 70,000 tCO2/yr pilot Stratos direct air capture (DAC) facility in Texas as part of a planned scale-up to >1 MtCO2/yr by 2030. These activities shift Occidental toward a carbon-managed energy model aligned with net-zero targets and expected to generate new revenue from carbon credits and enhanced oil recovery CO2 sales.

Enhanced Oil Recovery Operations

Capital Allocation and Debt Management

Occidental’s management targets shareholder returns, debt paydown, and reinvestment in high-return projects—after the 2019 Anadarko deal and later bolt-ons they prioritized de‑leveraging to regain and keep investment‑grade ratings, cutting net debt from about $40bn (2020) toward ~$25bn by Q4 2025 while funding Permian high-return drilling.

They use rigorous financial models and portfolio high‑grading to steer capital to accretive projects, targeting returns above WACC and maintaining free cash flow cover for buybacks and capex.

- Net debt reduction: ~$40bn (2020) → ~25bn (Q4 2025)

- Focus: Permian oil projects with >15% IRR target

- Priority: investment‑grade rating maintenance

- Tools: scenario models, portfolio high‑grading, FCF cover metrics

Integrated Permian growth: 730k boe/d, $2.1B OxyChem, CCUS scale & $15B debt cut

Upstream exploration, drilling, and production (Permian ~730,000 boe/d in 2025); OxyChem chemicals manufacturing (~$2.1bn sales in 2024) and 23 North American plants; CCUS/DAC and CO2 EOR (spent ~$1.5–2.0bn annually; Stratos 70,000 tCO2/yr pilot; ~300,000 t/day CO2 injected) plus capital allocation for debt cut (~$40bn→~$25bn net debt by Q4 2025) and >15% IRR Permian projects.

| Metric | Value |

|---|---|

| Permian prod (2025) | ~730,000 boe/d |

| OxyChem sales (2024) | $2.1bn |

| CCUS spend (2024–25) | $1.5–2.0bn/yr |

| Stratos DAC | 70,000 tCO2/yr |

| CO2 injected (EOR) | ~300,000 t/day |

| Net debt | $40bn→$25bn (Q4 2025) |

| Permian IRR target | >15% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Occidental Petroleum Business Model Canvas you will receive after purchase — not a mockup or sample — and it contains the same structured, editable content shown in this snapshot. Upon completing your order, you’ll instantly download the full file, formatted and ready for analysis, presentation, or customization in Word and Excel. What you see is what you’ll own, with all sections included and no surprises.