Paccar PESTLE Analysis

Your Shortcut to Market Insight Starts Here

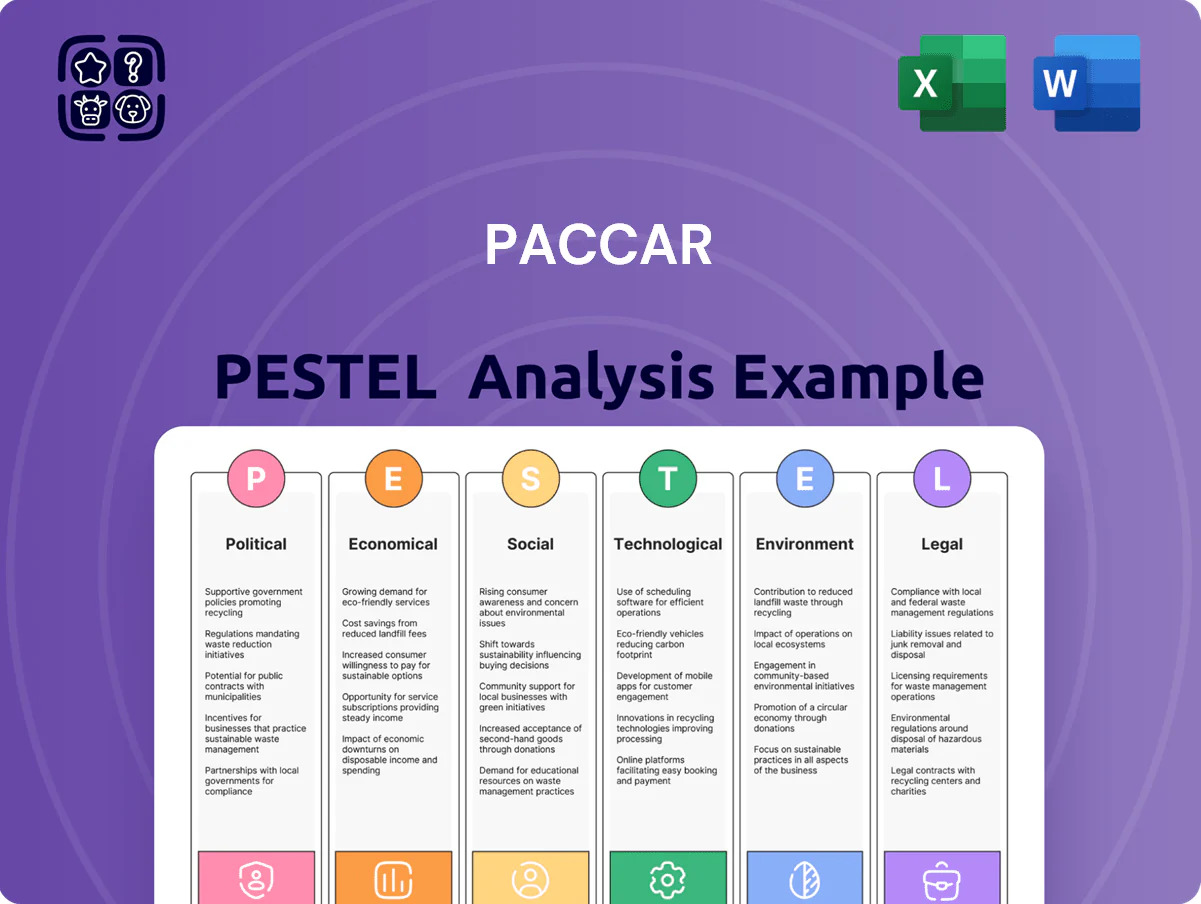

Discover how political shifts, supply-chain economics, and evolving green technologies are reshaping Paccar’s competitive edge and risk profile; our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full PESTLE Analysis to unlock detailed insights, data-driven scenarios, and actionable recommendations—ready for boardrooms, investment memos, or strategy plans.

Political factors

Trade Tariffs and Protectionism

As of late 2025, shifting trade policies between the United States, Europe, and Asia materially affect Paccar’s global footprint; US tariffs on steel and aluminum, ranging up to 25% since 2018 and intermittently applied through 2024–25, raised input costs for Kenworth and Peterbilt. Changes to EU and Chinese import duties have added regional cost volatility, contributing to an estimated 4–6% increase in truck production costs in 2024–25. Paccar must manage protectionist trends to preserve competitive pricing and secure component sourcing across assembly plants, where parts import exposure exceeds 30% of bill of materials in key facilities.

Government Subsidies for Green Tech

Political support for zero-emission vehicles provides strong tailwinds for Paccar’s electric and hydrogen truck programs through 2025, with US federal grants under the Inflation Reduction Act and DOE funding allocating over $10bn to clean truck initiatives since 2021 aiding commercialization.

State incentives (California HVIP payments up to $200,000 per truck) and EU Green Deal measures, including €3bn in heavy-vehicle decarbonization funding, lower total cost of ownership for Paccar customers.

These subsidies are crucial to accelerating DAF’s electric market penetration and Peterbilt’s zero-emission models, supporting fleet purchase economics and reducing payback periods by an estimated 20–35% versus diesel.

Infrastructure Investment Legislation

Paccar gains from major infrastructure bills—US Bipartisan Infrastructure Law and EU Recovery Fund—fueling demand for heavy-duty construction trucks; US federal infrastructure outlays of ~US$550bn (2021–2026) and EU multi-year investments of €300bn+ in green transition bolster orders for Kenworth and DAF. Public road, bridge and grid projects and logistics modernization programs support a steady pipeline, contributing to Paccar’s 2024 commercial vehicle backlog and parts revenue growth.

Geopolitical Supply Chain Risks

Persistent geopolitical tensions in key manufacturing hubs and shipping lanes force Paccar to keep a highly flexible, resilient supply chain; in 2024 Paccar reported supply-chain related downtime that trimmed net income by an estimated 2-3% vs. plan.

Political instability in regions supplying battery raw materials risks sudden price spikes or shortages—cobalt and nickel spot prices rose ~40% and ~30% respectively in 2024, increasing component cost pressure.

Paccar maintains diplomatic and strategic monitoring, sourcing diversification and safety stock policies; by 2025 it targeted supplier dual-sourcing and inventory buffers equal to roughly 6–8 weeks of production to mitigate trade disruption risks.

- 2024 supply disruptions cut earnings ~2–3%

- Cobalt +40%, nickel +30% YoY (2024)

- Targeted 6–8 weeks inventory buffer by 2025

- Active supplier diversification and diplomatic monitoring

Transatlantic Regulatory Alignment

Paccar navigates divergent US and EU political agendas on safety and CO2 rules; EU 2024 HDV CO2 targets push DAF toward zero-emission tech while Kenworth/Peterbilt follow EPA/NHTSA rulemakings (US HDV emissions standards revised 2024–25). Harmonizing standards improves ROI on global R&D — Paccar spent $1.2bn R&D in 2024, enabling cross-nameplate tech deployment.

- Manage EU vs US regulatory divergence on safety/emissions

- DAF aligns with strict EU mandates; Kenworth/Peterbilt follow evolving North American rules

- 2024 R&D spend $1.2bn supports harmonized tech across nameplates

- Alignment boosts global R&D efficiency and reduces per-unit compliance cost

Tariffs, metals surge and $10B+ clean-truck funding lift costs but fuel EV demand

Political shifts—US tariffs, EU import rules and infrastructure spending—raised 2024–25 production costs ~4–6% while boosting demand; IRA/DOE clean-truck funding >$10bn and US infrastructure ~$550bn (2021–26) aided electrification and orders. 2024 R&D $1.2bn; supply disruptions cut 2024 earnings ~2–3%; cobalt +40%, nickel +30% YoY (2024); 2025 target 6–8 week inventory buffer.

| Metric | 2024–25 |

|---|---|

| Prod cost impact | +4–6% |

| R&D | $1.2bn (2024) |

| Clean-truck funding | $10bn+ |

| Infra spend (US) | $550bn (2021–26) |

| Supply earnings hit | −2–3% |

| Cobalt/Nickel | +40% / +30% (2024) |

| Inventory buffer | 6–8 weeks (target 2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect Paccar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights that identify threats and opportunities to inform strategy, investor communications, and scenario planning.

A concise PESTLE summary for Paccar that’s visually segmented for quick interpretation, easily dropped into presentations, shared across teams, and editable for region- or business-specific notes to streamline planning and risk discussions.

Economic factors

Interest Rate Volatility

Interest rate volatility through 2025 directly affects Paccar Financial Services; the US Fed funds rate rise to 5.25-5.50% in 2023-24 pressured loan spreads and contributed to a 2024 YOY decline in North American truck retail sales of about 17% per ACT Research.

Global Freight Tonnage Trends

Paccar revenue closely tracks global freight tonnage; world seaborne and road freight fell 1.5% in 2023 but recovered with global merchandise trade up 3.4% in 2024, supporting truck demand as Class 8 orders in North America rose ~18% Y/Y in 2024 to ~330,000 units.

Raw Material Cost Inflation

The 2025 surge in high-grade steel (up ~18% YoY) and aluminum (+12% YoY) plus rising demand for rare earths elevates input-cost risk for Paccar, threatening manufacturing margins if not passed to buyers.

Paccar’s long-term supply contracts and hedging reduced commodity cost volatility, helping limit raw-material cost impact to roughly 1.5–2.0 percentage points on gross margin in FY2024–25.

Currency Exchange Fluctuations

As a global manufacturer, Paccar faces US dollar volatility versus the euro, pound and Australian dollar; in 2024 FX movements reduced reported international revenues by about 3–5% year-over-year, impacting DAF competitiveness and consolidated EPS.

A stronger dollar can lower DAF truck export prices abroad but shrink translated overseas earnings; Paccar’s treasury uses hedging and natural offsets to limit translation and transaction risk.

- 2024 FX headwind ≈ 3–5% on reported revenues

- Key exposures: EUR, GBP, AUD

- Hedging + natural offsets used to protect balance sheet

Credit Availability for Fleet Buyers

The ability of customers to secure affordable credit is critical for truck market growth; in 2024 U.S. commercial truck installment originations fell ~12% amid tighter lending standards, pressuring fleet renewals.

Smaller carriers face higher rejection rates and costlier spreads, constraining upgrades to efficient Paccar models during downturns.

Paccar Financial Services, which accounted for about $8.5 billion in receivables at end-2024, cushions sales when external credit tightens.

- Customer access to affordable credit drives unit replacement and fleet expansion

- Smaller fleets hit hardest by tighter lending, reducing demand for new trucks

- Paccar Financial Services receivables ~$8.5B (end-2024) sustain sales amid restrictive external credit

Truck finance cushions demand as orders rise but costs and FX squeeze margins

Interest-rate volatility and tighter lending reduced US truck originations ~12% in 2024, pressuring retail sales; Paccar Financial Services receivables ~$8.5B at end-2024 cushion demand. Global freight recovery (+3.4% merch. trade in 2024) lifted Class 8 orders ~18% Y/Y (~330k units), while FX (2024 headwind ≈3–5%) and raw-material inflation (steel +18%, aluminum +12% YoY in 2025) squeezed margins despite hedges.

| Metric | Value |

|---|---|

| US truck originations change (2024) | -12% |

| Paccar Financial Services receivables (end-2024) | $8.5B |

| Global merchandise trade (2024) | +3.4% |

| Class 8 orders NA (2024) | ~330,000 (+18% Y/Y) |

| FX revenue headwind (2024) | ≈3–5% |

| Steel price change (2025) | +18% YoY |

| Aluminum price change (2025) | +12% YoY |

Preview the Actual Deliverable

Paccar PESTLE Analysis

The preview shown here is the exact Paccar PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

This is the real, finished file—professionally structured and delivered instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and evolving green technologies are reshaping Paccar’s competitive edge and risk profile; our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full PESTLE Analysis to unlock detailed insights, data-driven scenarios, and actionable recommendations—ready for boardrooms, investment memos, or strategy plans.

Political factors

Trade Tariffs and Protectionism

As of late 2025, shifting trade policies between the United States, Europe, and Asia materially affect Paccar’s global footprint; US tariffs on steel and aluminum, ranging up to 25% since 2018 and intermittently applied through 2024–25, raised input costs for Kenworth and Peterbilt. Changes to EU and Chinese import duties have added regional cost volatility, contributing to an estimated 4–6% increase in truck production costs in 2024–25. Paccar must manage protectionist trends to preserve competitive pricing and secure component sourcing across assembly plants, where parts import exposure exceeds 30% of bill of materials in key facilities.

Government Subsidies for Green Tech

Political support for zero-emission vehicles provides strong tailwinds for Paccar’s electric and hydrogen truck programs through 2025, with US federal grants under the Inflation Reduction Act and DOE funding allocating over $10bn to clean truck initiatives since 2021 aiding commercialization.

State incentives (California HVIP payments up to $200,000 per truck) and EU Green Deal measures, including €3bn in heavy-vehicle decarbonization funding, lower total cost of ownership for Paccar customers.

These subsidies are crucial to accelerating DAF’s electric market penetration and Peterbilt’s zero-emission models, supporting fleet purchase economics and reducing payback periods by an estimated 20–35% versus diesel.

Infrastructure Investment Legislation

Paccar gains from major infrastructure bills—US Bipartisan Infrastructure Law and EU Recovery Fund—fueling demand for heavy-duty construction trucks; US federal infrastructure outlays of ~US$550bn (2021–2026) and EU multi-year investments of €300bn+ in green transition bolster orders for Kenworth and DAF. Public road, bridge and grid projects and logistics modernization programs support a steady pipeline, contributing to Paccar’s 2024 commercial vehicle backlog and parts revenue growth.

Geopolitical Supply Chain Risks

Persistent geopolitical tensions in key manufacturing hubs and shipping lanes force Paccar to keep a highly flexible, resilient supply chain; in 2024 Paccar reported supply-chain related downtime that trimmed net income by an estimated 2-3% vs. plan.

Political instability in regions supplying battery raw materials risks sudden price spikes or shortages—cobalt and nickel spot prices rose ~40% and ~30% respectively in 2024, increasing component cost pressure.

Paccar maintains diplomatic and strategic monitoring, sourcing diversification and safety stock policies; by 2025 it targeted supplier dual-sourcing and inventory buffers equal to roughly 6–8 weeks of production to mitigate trade disruption risks.

- 2024 supply disruptions cut earnings ~2–3%

- Cobalt +40%, nickel +30% YoY (2024)

- Targeted 6–8 weeks inventory buffer by 2025

- Active supplier diversification and diplomatic monitoring

Transatlantic Regulatory Alignment

Paccar navigates divergent US and EU political agendas on safety and CO2 rules; EU 2024 HDV CO2 targets push DAF toward zero-emission tech while Kenworth/Peterbilt follow EPA/NHTSA rulemakings (US HDV emissions standards revised 2024–25). Harmonizing standards improves ROI on global R&D — Paccar spent $1.2bn R&D in 2024, enabling cross-nameplate tech deployment.

- Manage EU vs US regulatory divergence on safety/emissions

- DAF aligns with strict EU mandates; Kenworth/Peterbilt follow evolving North American rules

- 2024 R&D spend $1.2bn supports harmonized tech across nameplates

- Alignment boosts global R&D efficiency and reduces per-unit compliance cost

Tariffs, metals surge and $10B+ clean-truck funding lift costs but fuel EV demand

Political shifts—US tariffs, EU import rules and infrastructure spending—raised 2024–25 production costs ~4–6% while boosting demand; IRA/DOE clean-truck funding >$10bn and US infrastructure ~$550bn (2021–26) aided electrification and orders. 2024 R&D $1.2bn; supply disruptions cut 2024 earnings ~2–3%; cobalt +40%, nickel +30% YoY (2024); 2025 target 6–8 week inventory buffer.

| Metric | 2024–25 |

|---|---|

| Prod cost impact | +4–6% |

| R&D | $1.2bn (2024) |

| Clean-truck funding | $10bn+ |

| Infra spend (US) | $550bn (2021–26) |

| Supply earnings hit | −2–3% |

| Cobalt/Nickel | +40% / +30% (2024) |

| Inventory buffer | 6–8 weeks (target 2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect Paccar across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights that identify threats and opportunities to inform strategy, investor communications, and scenario planning.

A concise PESTLE summary for Paccar that’s visually segmented for quick interpretation, easily dropped into presentations, shared across teams, and editable for region- or business-specific notes to streamline planning and risk discussions.

Economic factors

Interest Rate Volatility

Interest rate volatility through 2025 directly affects Paccar Financial Services; the US Fed funds rate rise to 5.25-5.50% in 2023-24 pressured loan spreads and contributed to a 2024 YOY decline in North American truck retail sales of about 17% per ACT Research.

Global Freight Tonnage Trends

Paccar revenue closely tracks global freight tonnage; world seaborne and road freight fell 1.5% in 2023 but recovered with global merchandise trade up 3.4% in 2024, supporting truck demand as Class 8 orders in North America rose ~18% Y/Y in 2024 to ~330,000 units.

Raw Material Cost Inflation

The 2025 surge in high-grade steel (up ~18% YoY) and aluminum (+12% YoY) plus rising demand for rare earths elevates input-cost risk for Paccar, threatening manufacturing margins if not passed to buyers.

Paccar’s long-term supply contracts and hedging reduced commodity cost volatility, helping limit raw-material cost impact to roughly 1.5–2.0 percentage points on gross margin in FY2024–25.

Currency Exchange Fluctuations

As a global manufacturer, Paccar faces US dollar volatility versus the euro, pound and Australian dollar; in 2024 FX movements reduced reported international revenues by about 3–5% year-over-year, impacting DAF competitiveness and consolidated EPS.

A stronger dollar can lower DAF truck export prices abroad but shrink translated overseas earnings; Paccar’s treasury uses hedging and natural offsets to limit translation and transaction risk.

- 2024 FX headwind ≈ 3–5% on reported revenues

- Key exposures: EUR, GBP, AUD

- Hedging + natural offsets used to protect balance sheet

Credit Availability for Fleet Buyers

The ability of customers to secure affordable credit is critical for truck market growth; in 2024 U.S. commercial truck installment originations fell ~12% amid tighter lending standards, pressuring fleet renewals.

Smaller carriers face higher rejection rates and costlier spreads, constraining upgrades to efficient Paccar models during downturns.

Paccar Financial Services, which accounted for about $8.5 billion in receivables at end-2024, cushions sales when external credit tightens.

- Customer access to affordable credit drives unit replacement and fleet expansion

- Smaller fleets hit hardest by tighter lending, reducing demand for new trucks

- Paccar Financial Services receivables ~$8.5B (end-2024) sustain sales amid restrictive external credit

Truck finance cushions demand as orders rise but costs and FX squeeze margins

Interest-rate volatility and tighter lending reduced US truck originations ~12% in 2024, pressuring retail sales; Paccar Financial Services receivables ~$8.5B at end-2024 cushion demand. Global freight recovery (+3.4% merch. trade in 2024) lifted Class 8 orders ~18% Y/Y (~330k units), while FX (2024 headwind ≈3–5%) and raw-material inflation (steel +18%, aluminum +12% YoY in 2025) squeezed margins despite hedges.

| Metric | Value |

|---|---|

| US truck originations change (2024) | -12% |

| Paccar Financial Services receivables (end-2024) | $8.5B |

| Global merchandise trade (2024) | +3.4% |

| Class 8 orders NA (2024) | ~330,000 (+18% Y/Y) |

| FX revenue headwind (2024) | ≈3–5% |

| Steel price change (2025) | +18% YoY |

| Aluminum price change (2025) | +12% YoY |

Preview the Actual Deliverable

Paccar PESTLE Analysis

The preview shown here is the exact Paccar PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

This is the real, finished file—professionally structured and delivered instantly upon payment.