Pacira Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

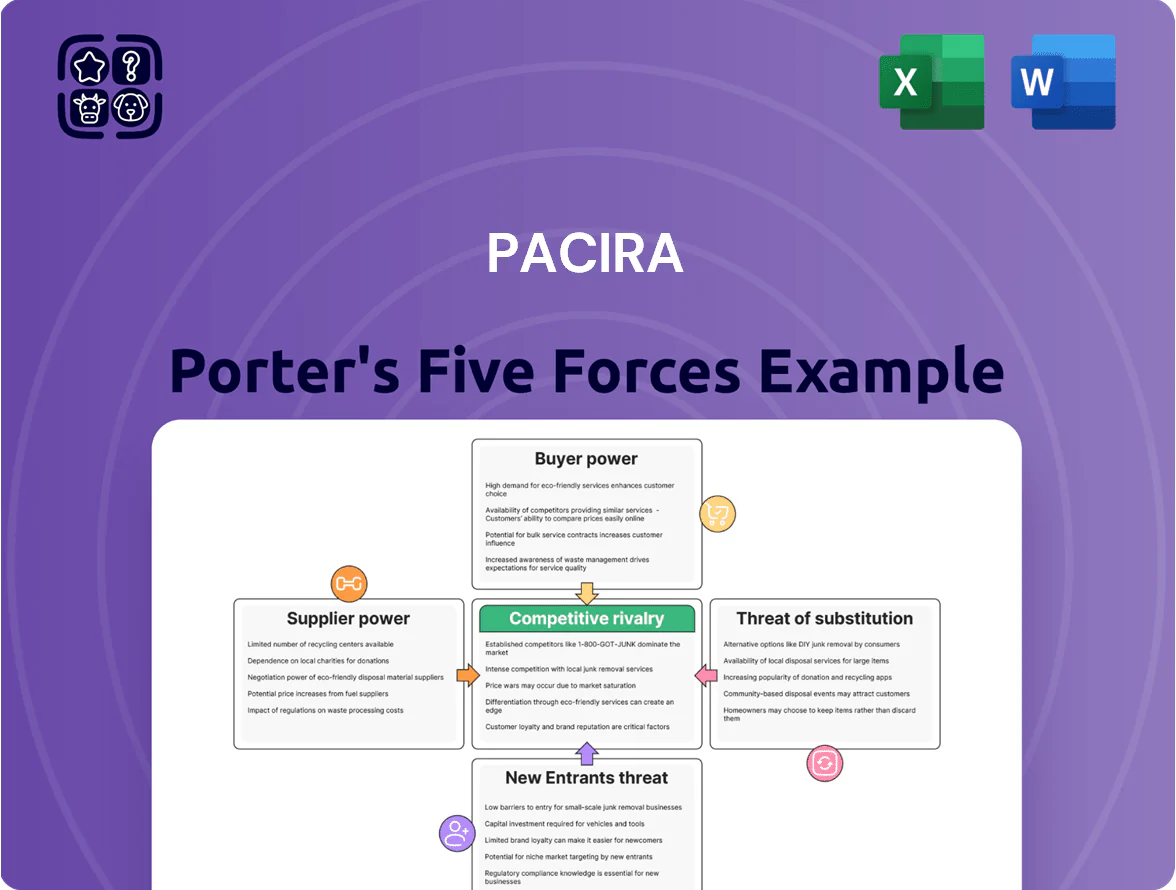

Pacira faces moderate supplier power, niche product differentiation, regulatory hurdles, and growing substitute pressure from multimodal pain therapies, creating a dynamic but navigable competitive landscape; this snapshot highlights key risks and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Pacira’s market position.

Suppliers Bargaining Power

Specialized Raw Material Sourcing

EXPAREL production depends on high-grade bupivacaine and specific lipids that meet FDA and EMA standards; Pacira sources these from a small set of qualified suppliers, giving vendors pricing and lead-time leverage.

In 2024 Pacira reported 14% of COGS tied to raw materials, and a single-supplier exposure for key lipids risked >10% revenue disruption if interrupted.

Any supply-chain disruption—regulatory hold, capacity constraint, or quality failure—could materially limit shipments to the acute care market and pressure margins.

Proprietary Manufacturing Technology Components

Pacira’s DepoFoam proprietary platform forces reliance on specialized engineering suppliers for specific mixers, sterile-fill lines, and maintenance; these niche vendors command bargaining power because off-the-shelf equipment fails to match multivesicular liposome tolerances, and replacement would risk batch failures. In 2024 Pacira reported 2023 manufacturing spend of $78M, and any supplier disruption that increases downtime beyond 5% could cut quarterly revenue by an estimated $15–25M given $600M annual revenue run-rate.

Regulatory Compliance and Quality Standards

Suppliers must follow FDA Current Good Manufacturing Practices (cGMP), which narrows Pacira’s supplier pool and concentrates spend: in 2024 Pacira reported $232m in cost of goods sold, increasing dependence on validated vendors. This high entry barrier raises existing suppliers’ bargaining power, since FDA re-validation can take 6–12 months and cost millions, limiting Pacira’s ability to switch quickly.

Energy and Specialized Utility Costs

Energy-intensive liposomal injectable manufacture needs strict cleanroom controls and industrial gases; suppliers can push costs when energy prices spike—US industrial electricity rose 6.2% y/y in 2024, and natural gas volatility lifted input costs for pharma plants.

As Pacira expands capacity for 2026 demand, higher utility and specialty-gas costs will pressure COGS and margins unless long-term supply contracts or on-site generation are used.

- 2024 US industrial electricity +6.2% y/y

- Natural gas price swings raise gas-fed sterilization costs

- Scaling to 2026 increases absolute utility spend

- Mitigation: long-term contracts, on-site power

Logistics and Cold Chain Requirements

Distribution of Pacira’s injectable products needs strict cold-chain logistics to keep sterility and potency; 2024 recalls in pharma cold-chain failures rose 18%, underscoring risk. Third-party cold-chain specialists command leverage because only a few providers meet medical-grade reliability and compliance, often charging 10–20% premiums for validated cold storage. A single cold-chain failure can cause immediate product loss and multi-million-dollar liability for Pacira.

- Medical cold-chain failure risk up 18% in 2024

- 3–5 high-reliability providers dominate market

- Logistics premium typically 10–20%

- Failure leads to immediate product loss, multi‑million liability

High supplier power lifts COGS risk—single lipid supplier >10% revenue; energy & cold‑chain pressure

Supplier power is high: narrow pool for FDA/EMA-grade bupivacaine, specialty lipids, and DepoFoam equipment raises switching costs and price/lead-time leverage; 2024 COGS $232M, raw materials ~14%, single-supplier lipid exposure >10% revenue risk. Energy and cold-chain suppliers add pricing pressure (US industrial electricity +6.2% y/y 2024; cold-chain recalls +18% 2024), so long-term contracts or on‑site options are critical.

| Metric | 2024 value |

|---|---|

| COGS | $232M |

| Raw materials share | 14% |

| Single-supplier lipid risk | >10% revenue |

| US industrial electricity y/y | +6.2% |

| Cold-chain recall rise | +18% |

What is included in the product

Tailored exclusively for Pacira, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers that impact Pacira’s pricing, market share, and profitability.

Concise Porter's Five Forces summary for Pacira—quickly gauge competitive threats, supplier/buyer leverage, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

Consolidation of Hospital Systems

Large integrated delivery networks (IDNs) and hospital systems account for roughly 60% of Pacira's US hospital sales and wield strong bargaining power via volume purchasing.

These systems used scale to secure discounts and rebates, pressuring EXPAREL list-price concessions of 20–40% in recent contracts.

Consolidation rose to 72% market share among top 100 health systems by 2024, so through 2025 their formulary leverage and ability to dictate terms increases.

Influence of Group Purchasing Organizations

GPOs (group purchasing organizations) negotiate contracts for over 90% of US hospitals and can secure price cuts of 10–30%; Pacira must keep favorable GPO ties to keep EXPAREL and other products stocked across thousands of facilities. If a top GPO shifts to a rival or generics, Pacira could lose access to networks representing tens of millions in annual hospital spend almost overnight. Maintaining contract terms and rebate structures is therefore critical.

Impact of the NOPAIN Act Reimbursement

The NOPAIN Act, effective Jan 1, 2025, gives separate Medicare reimbursement for non‑opioid outpatient analgesia, cutting hospital/ASC out‑of‑pocket costs and lowering their price sensitivity to Pacira’s EXPAREL (bupivacaine liposome), whose 2024 U.S. net price averaged about $300–$400 per vial.

Still, buyers retain power: hospitals and ASCs can select alternatives—generic bupivacaine (~$5/vial), regional blocks, or infiltration—so uptake depends on comparative efficacy, OR time saved, and hospital formularies; a 2024 survey found 38% of centers consider reimbursement changes a top adoption factor.

Surgeon Preference and Clinical Autonomy

Surgeons and anesthesiologists are the primary influencers of hospital purchasing for pain-management products; their preference drives utilization even though hospitals pay the bill.

Pacira must supply rigorous clinical evidence showing better recovery and lower opioid use—studies through 2024 report a 30–40% reduction in opioid consumption with liposomal bupivacaine in select procedures.

Maintaining clinician trust affects sales: in 2024 US hospital adoption rates for multimodal analgesia rose ~12%, raising the bar for demonstrated outcomes and real-world evidence.

- Clinicians, not procurement, dictate use

- 2024 studies: 30–40% lower opioid use

- Hospital multimodal adoption +12% (2024)

- Pacira needs ongoing RWE and RCTs

Payer Formulary Restrictions

Insurance firms and government payers set formularies and tiering, giving them indirect but strong customer power over Pacira by deciding coverage and patient cost-sharing.

Restrictive prior authorization or high co-pays for non-opioid injectables cuts effective end-user demand; a 2024 IQVIA report showed payer exclusions reduced utilization by ~18% in similar classes.

Pacira must prove cost-effectiveness—e.g., lower length-of-stay or reduced opioid-related costs—to secure preferred formulary placement and limit patient out-of-pocket barriers.

- Payer formulary = access gatekeeper

- Prior auth/high co-pay → ~18% lower use (IQVIA 2024)

- Cost-effectiveness data crucial for preferred tiering

Buyers’ leverage slashes EXPAREL prices 20–40% despite RWE showing 30–40% opioid cuts

Buyers (IDNs/health systems, GPOs, payers) hold strong leverage—IDNs = ~60% of US hospital sales, top 100 systems = 72% share (2024)—driving 20–40% contract discounts on EXPAREL and 10–30% GPO cuts; payer exclusions cut use ~18% (IQVIA 2024). Clinical preference (surgeons/anesth.) and RWE (30–40% opioid reduction in select studies) moderate but do not eliminate buyer power.

| Metric | Value (source, year) |

|---|---|

| IDN share of hospital sales | ~60% (Pacira US data, 2024) |

| Top 100 systems share | 72% (2024) |

| EXPAREL contract discounts | 20–40% (recent contracts) |

| GPO negotiated cuts | 10–30% (industry) |

| Payer exclusion impact | ~18% lower use (IQVIA 2024) |

| Net price per vial (2024) | $300–$400 (US net) |

| Clinical opioid reduction | 30–40% (select RCTs/real-world, through 2024) |

Same Document Delivered

Pacira Porter's Five Forces Analysis

This preview shows the exact Pacira Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no excerpts.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Pacira faces moderate supplier power, niche product differentiation, regulatory hurdles, and growing substitute pressure from multimodal pain therapies, creating a dynamic but navigable competitive landscape; this snapshot highlights key risks and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Pacira’s market position.

Suppliers Bargaining Power

Specialized Raw Material Sourcing

EXPAREL production depends on high-grade bupivacaine and specific lipids that meet FDA and EMA standards; Pacira sources these from a small set of qualified suppliers, giving vendors pricing and lead-time leverage.

In 2024 Pacira reported 14% of COGS tied to raw materials, and a single-supplier exposure for key lipids risked >10% revenue disruption if interrupted.

Any supply-chain disruption—regulatory hold, capacity constraint, or quality failure—could materially limit shipments to the acute care market and pressure margins.

Proprietary Manufacturing Technology Components

Pacira’s DepoFoam proprietary platform forces reliance on specialized engineering suppliers for specific mixers, sterile-fill lines, and maintenance; these niche vendors command bargaining power because off-the-shelf equipment fails to match multivesicular liposome tolerances, and replacement would risk batch failures. In 2024 Pacira reported 2023 manufacturing spend of $78M, and any supplier disruption that increases downtime beyond 5% could cut quarterly revenue by an estimated $15–25M given $600M annual revenue run-rate.

Regulatory Compliance and Quality Standards

Suppliers must follow FDA Current Good Manufacturing Practices (cGMP), which narrows Pacira’s supplier pool and concentrates spend: in 2024 Pacira reported $232m in cost of goods sold, increasing dependence on validated vendors. This high entry barrier raises existing suppliers’ bargaining power, since FDA re-validation can take 6–12 months and cost millions, limiting Pacira’s ability to switch quickly.

Energy and Specialized Utility Costs

Energy-intensive liposomal injectable manufacture needs strict cleanroom controls and industrial gases; suppliers can push costs when energy prices spike—US industrial electricity rose 6.2% y/y in 2024, and natural gas volatility lifted input costs for pharma plants.

As Pacira expands capacity for 2026 demand, higher utility and specialty-gas costs will pressure COGS and margins unless long-term supply contracts or on-site generation are used.

- 2024 US industrial electricity +6.2% y/y

- Natural gas price swings raise gas-fed sterilization costs

- Scaling to 2026 increases absolute utility spend

- Mitigation: long-term contracts, on-site power

Logistics and Cold Chain Requirements

Distribution of Pacira’s injectable products needs strict cold-chain logistics to keep sterility and potency; 2024 recalls in pharma cold-chain failures rose 18%, underscoring risk. Third-party cold-chain specialists command leverage because only a few providers meet medical-grade reliability and compliance, often charging 10–20% premiums for validated cold storage. A single cold-chain failure can cause immediate product loss and multi-million-dollar liability for Pacira.

- Medical cold-chain failure risk up 18% in 2024

- 3–5 high-reliability providers dominate market

- Logistics premium typically 10–20%

- Failure leads to immediate product loss, multi‑million liability

High supplier power lifts COGS risk—single lipid supplier >10% revenue; energy & cold‑chain pressure

Supplier power is high: narrow pool for FDA/EMA-grade bupivacaine, specialty lipids, and DepoFoam equipment raises switching costs and price/lead-time leverage; 2024 COGS $232M, raw materials ~14%, single-supplier lipid exposure >10% revenue risk. Energy and cold-chain suppliers add pricing pressure (US industrial electricity +6.2% y/y 2024; cold-chain recalls +18% 2024), so long-term contracts or on‑site options are critical.

| Metric | 2024 value |

|---|---|

| COGS | $232M |

| Raw materials share | 14% |

| Single-supplier lipid risk | >10% revenue |

| US industrial electricity y/y | +6.2% |

| Cold-chain recall rise | +18% |

What is included in the product

Tailored exclusively for Pacira, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers that impact Pacira’s pricing, market share, and profitability.

Concise Porter's Five Forces summary for Pacira—quickly gauge competitive threats, supplier/buyer leverage, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

Consolidation of Hospital Systems

Large integrated delivery networks (IDNs) and hospital systems account for roughly 60% of Pacira's US hospital sales and wield strong bargaining power via volume purchasing.

These systems used scale to secure discounts and rebates, pressuring EXPAREL list-price concessions of 20–40% in recent contracts.

Consolidation rose to 72% market share among top 100 health systems by 2024, so through 2025 their formulary leverage and ability to dictate terms increases.

Influence of Group Purchasing Organizations

GPOs (group purchasing organizations) negotiate contracts for over 90% of US hospitals and can secure price cuts of 10–30%; Pacira must keep favorable GPO ties to keep EXPAREL and other products stocked across thousands of facilities. If a top GPO shifts to a rival or generics, Pacira could lose access to networks representing tens of millions in annual hospital spend almost overnight. Maintaining contract terms and rebate structures is therefore critical.

Impact of the NOPAIN Act Reimbursement

The NOPAIN Act, effective Jan 1, 2025, gives separate Medicare reimbursement for non‑opioid outpatient analgesia, cutting hospital/ASC out‑of‑pocket costs and lowering their price sensitivity to Pacira’s EXPAREL (bupivacaine liposome), whose 2024 U.S. net price averaged about $300–$400 per vial.

Still, buyers retain power: hospitals and ASCs can select alternatives—generic bupivacaine (~$5/vial), regional blocks, or infiltration—so uptake depends on comparative efficacy, OR time saved, and hospital formularies; a 2024 survey found 38% of centers consider reimbursement changes a top adoption factor.

Surgeon Preference and Clinical Autonomy

Surgeons and anesthesiologists are the primary influencers of hospital purchasing for pain-management products; their preference drives utilization even though hospitals pay the bill.

Pacira must supply rigorous clinical evidence showing better recovery and lower opioid use—studies through 2024 report a 30–40% reduction in opioid consumption with liposomal bupivacaine in select procedures.

Maintaining clinician trust affects sales: in 2024 US hospital adoption rates for multimodal analgesia rose ~12%, raising the bar for demonstrated outcomes and real-world evidence.

- Clinicians, not procurement, dictate use

- 2024 studies: 30–40% lower opioid use

- Hospital multimodal adoption +12% (2024)

- Pacira needs ongoing RWE and RCTs

Payer Formulary Restrictions

Insurance firms and government payers set formularies and tiering, giving them indirect but strong customer power over Pacira by deciding coverage and patient cost-sharing.

Restrictive prior authorization or high co-pays for non-opioid injectables cuts effective end-user demand; a 2024 IQVIA report showed payer exclusions reduced utilization by ~18% in similar classes.

Pacira must prove cost-effectiveness—e.g., lower length-of-stay or reduced opioid-related costs—to secure preferred formulary placement and limit patient out-of-pocket barriers.

- Payer formulary = access gatekeeper

- Prior auth/high co-pay → ~18% lower use (IQVIA 2024)

- Cost-effectiveness data crucial for preferred tiering

Buyers’ leverage slashes EXPAREL prices 20–40% despite RWE showing 30–40% opioid cuts

Buyers (IDNs/health systems, GPOs, payers) hold strong leverage—IDNs = ~60% of US hospital sales, top 100 systems = 72% share (2024)—driving 20–40% contract discounts on EXPAREL and 10–30% GPO cuts; payer exclusions cut use ~18% (IQVIA 2024). Clinical preference (surgeons/anesth.) and RWE (30–40% opioid reduction in select studies) moderate but do not eliminate buyer power.

| Metric | Value (source, year) |

|---|---|

| IDN share of hospital sales | ~60% (Pacira US data, 2024) |

| Top 100 systems share | 72% (2024) |

| EXPAREL contract discounts | 20–40% (recent contracts) |

| GPO negotiated cuts | 10–30% (industry) |

| Payer exclusion impact | ~18% lower use (IQVIA 2024) |

| Net price per vial (2024) | $300–$400 (US net) |

| Clinical opioid reduction | 30–40% (select RCTs/real-world, through 2024) |

Same Document Delivered

Pacira Porter's Five Forces Analysis

This preview shows the exact Pacira Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no excerpts.