Packaging Corp of America PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis of Packaging Corp of America—unpack how political shifts, economic cycles, environmental rules, and tech innovations will influence margins and growth; ideal for investors and strategists seeking an edge. Purchase the full report to get actionable, editable insights and detailed scenarios you can use immediately.

Political factors

Domestic Trade Policy and Tariffs

The company’s US-focused operations make it sensitive to federal trade policy and tariffs on imported paper; in 2024 the US imposed duties averaging 15–25% on certain foreign containerboard imports, measures that can protect PCA’s market share and support pricing power after PCA reported $7.9B revenue in 2024. Anti-dumping protections helped stabilize domestic boxboard prices, but retaliatory tariffs on US exports and 2024 machinery import costs rising ~6% could raise supply-chain and capital-equipment expenses for PCA.

Government Procurement Standards

Federal and state governments are increasingly mandating sustainable procurement; by 2024 over 30 states had recycled-content requirements and the federal Buy Clean/Buy America expansions pushed preference for fiber-based packaging in millions of dollars of contracts. PCA can capture share by marketing fiber as a plastic alternative for government RFPs, potentially growing public-sector revenue given the US federal procurement budget exceeded $700 billion in FY2024. Ongoing engagement with legislators and compliance teams is needed to track evolving standards and certify products.

Geopolitical Stability and Supply Chains

Although Packaging Corp of America earns over 90% of revenue in North America, global geopolitical tensions can disrupt supplies of chemicals and energy for paper milling; for example, 2023-24 European gas price shocks pushed pulp production costs up an estimated 8-12%, and PCA reported input-cost inflation contributing to a 6% rise in COGS in FY2024. Political instability in supplier regions risks raw-material and equipment price spikes; PCA must monitor diplomacy and logistics to hedge energy and freight volatility.

Taxation and Corporate Incentives

Changes in US federal corporate tax rates or new investment tax credits materially affect Packaging Corp of America’s capex—PCA spent $824 million in 2024 on property, plant and equipment, so a 5 percentage-point tax cut or a 10% investment tax credit would meaningfully expand modernization funding.

Federal and state incentives for domestic manufacturing and clean-energy (e.g., IRA tax credits) can offset mill modernization costs; without incentives, higher effective tax rates would pressure free cash flow—PCA generated $1.1 billion of operating cash flow in 2024—reducing dividends or M&A capacity.

- 2024 capex: $824M

- 2024 operating cash flow: $1.1B

- IRA/clean-energy credits can lower modernization net cost

- Higher tax burden reduces funds for dividends/M&A

Infrastructure Legislation

Government spending on transportation infrastructure directly affects PCA’s logistics efficiency; the U.S. enacted a $1.2 trillion infrastructure law in 2021 with continued federal and state bridge/road allocations of about $200–300 billion annually through 2024–2025, which can lower PCA’s per-ton trucking costs for heavy containerboard rolls.

Improved highways and rail systems reduce transport times and costs for corrugated boxes—rail shipments can be up to 30% cheaper than long-haul trucking—supporting PCA’s margin preservation amid freight rate volatility.

Legislative focus on bridge and road repair is vital for timely delivery; delayed repairs raise detour-related fuel and labor costs that can erode PCA’s operating income, where logistics typically comprises a significant single-digit percentage of COGS.

- Federal infrastructure funding: ~$200–300B/year (2024–25)

- Rail vs trucking cost differential: ~30% lower for rail

- Logistics as % of COGS: single-digit impact on margins

Tariffs, mandates and IRA lift PCA margins as 2024 revenue hits $7.9B

Political factors: US tariffs on containerboard (15–25% in 2024) and recycled-content mandates in 30+ states boost PCA pricing and public-sector demand; IRA credits and $200–300B/yr infrastructure spend lower capex/net costs and transport expenses; 2024: revenue $7.9B, capex $824M, OCF $1.1B; input-cost inflation raised COGS ~6%.

| Metric | 2024 |

|---|---|

| Revenue | $7.9B |

| Capex | $824M |

| OCF | $1.1B |

| Tariff range | 15–25% |

| COGS rise | ~6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Packaging Corp of America across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights tailored for executives and investors.

A concise PESTLE snapshot for Packaging Corp of America that highlights regulatory, economic, and environmental drivers to streamline risk discussions during planning sessions.

Economic factors

Containerboard Pricing Fluctuations

Containerboard pricing is PCA’s primary revenue driver, tied closely to industry capacity and demand; average OCC and kraftliner prices fell about 18% year-over-year in 2024, pressuring realized selling prices. Economic cycles influence shipment volumes—US e-commerce and industrial freight volumes declined ~3–5% in 2024, reducing box demand. Management must adjust production and utilization (PCA reported 88% mill utilization in 2024) to protect margins amid volatile prices.

Interest Rate Environment

As a capital-intensive business, Packaging Corp of America often uses debt for mill conversions and expansions; with PCA carrying about $2.6 billion of long-term debt as of YE 2024, a 100 bp rise in rates can materially raise annual interest expense. Higher interest rates increase borrowing costs and can delay projects or raise the hurdle rate for new investments, compressing ROIC. Monitoring the federal funds rate—which averaged 5.25%–5.50% in 2023–2024—is essential for timing capital raises and managing debt maturities. Carefully staggering maturities reduces refinancing risk amid elevated rates.

Labor Market Dynamics

Tight US labor markets and 4.0% manufacturing wage growth in 2024 squeeze Packaging Corporation of America’s margins, forcing PCA to offer competitive pay and benefits to retain machine operators and logistics staff. PCA reported 2024 labor and benefit expenses rising ~6% year-over-year, pressuring operating income. To offset higher wages, PCA is accelerating capital spend on automation—capital expenditures rose to $514 million in 2024—to boost productivity and protect margins.

Energy and Fuel Costs

Paper mills are energy-intensive; PCA reported energy and fuel costs represented about 12% of cost of goods sold in 2024, leaving margin exposure to US natural gas averaging $6.50/MMBtu in 2024 and wholesale electricity volatility across regions.

Diesel prices averaging $3.80/gal in 2024 raise trucking costs for PCA’s ~7,000-route distribution network; investments in efficiency and fuel hedging reduced fuel expense volatility by an estimated 15% in 2024.

- Energy/fuel ~12% of COGS (2024)

- US natural gas ~ $6.50/MMBtu (2024)

- Diesel ~ $3.80/gal (2024)

- Efficiency/hedging cut volatility ~15% (2024)

E-commerce Growth Trends

The continued expansion of online retail is a structural tailwind for corrugated packaging; global e-commerce sales reached about $6.4 trillion in 2024, up ~10% year-over-year, supporting steady demand for shipping boxes even as brick-and-mortar sales fluctuate.

PCA’s capacity to serve high-volume e-commerce fulfillment centers underpins resilience: e-commerce packaging accounted for an estimated 25–30% of U.S. box demand in 2024, boosting PCA’s pricing power and utilization rates.

- Global e-commerce sales ~ $6.4T (2024)

- E-commerce share of U.S. box demand ~25–30% (2024)

- Supports PCA utilization and pricing power

2024 Margin Squeeze: Prices Down 18%, Costs Up as E‑Commerce Fuels 25–30% Box Demand

Economic pressures in 2024 cut PCA margins: containerboard prices fell ~18% YoY, mill utilization averaged 88%, long-term debt ~$2.6B, energy/fuel ~12% of COGS, natural gas ~$6.50/MMBtu, diesel ~$3.80/gal, labor costs +6% YoY, capex $514M, e-commerce sales ~$6.4T supporting 25–30% of U.S. box demand.

| Metric | 2024 |

|---|---|

| Containerboard price change | -18% YoY |

| Mill utilization | 88% |

| Long-term debt | $2.6B |

| Energy/COGS | 12% |

| Natural gas | $6.50/MMBtu |

| Diesel | $3.80/gal |

| Labor expense growth | +6% YoY |

| Capex | $514M |

| Global e-commerce | $6.4T |

| E-commerce box share (US) | 25–30% |

Preview the Actual Deliverable

Packaging Corp of America PESTLE Analysis

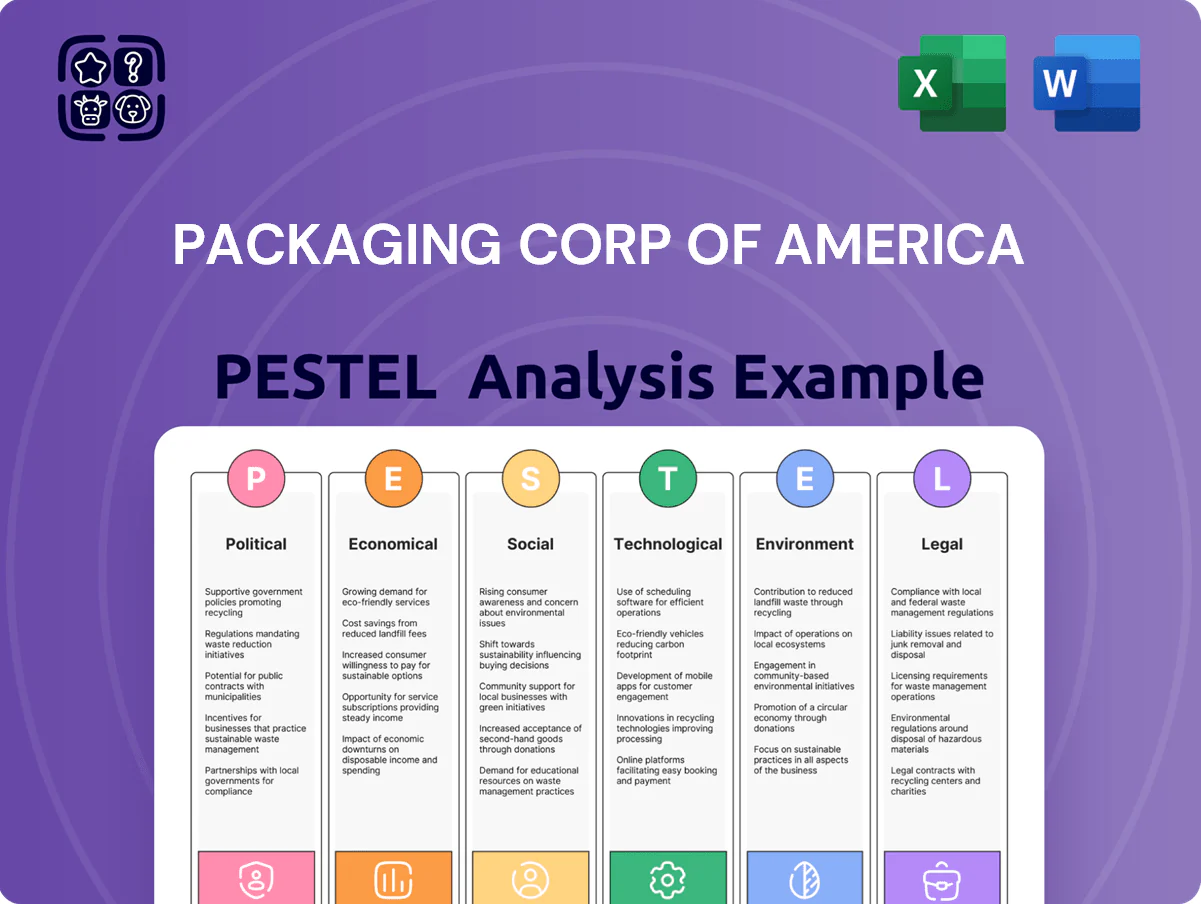

The preview shown here is the exact Packaging Corp of America PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it covers political, economic, social, technological, legal, and environmental factors affecting PCA and is presented in the same layout and detail as the downloadable file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis of Packaging Corp of America—unpack how political shifts, economic cycles, environmental rules, and tech innovations will influence margins and growth; ideal for investors and strategists seeking an edge. Purchase the full report to get actionable, editable insights and detailed scenarios you can use immediately.

Political factors

Domestic Trade Policy and Tariffs

The company’s US-focused operations make it sensitive to federal trade policy and tariffs on imported paper; in 2024 the US imposed duties averaging 15–25% on certain foreign containerboard imports, measures that can protect PCA’s market share and support pricing power after PCA reported $7.9B revenue in 2024. Anti-dumping protections helped stabilize domestic boxboard prices, but retaliatory tariffs on US exports and 2024 machinery import costs rising ~6% could raise supply-chain and capital-equipment expenses for PCA.

Government Procurement Standards

Federal and state governments are increasingly mandating sustainable procurement; by 2024 over 30 states had recycled-content requirements and the federal Buy Clean/Buy America expansions pushed preference for fiber-based packaging in millions of dollars of contracts. PCA can capture share by marketing fiber as a plastic alternative for government RFPs, potentially growing public-sector revenue given the US federal procurement budget exceeded $700 billion in FY2024. Ongoing engagement with legislators and compliance teams is needed to track evolving standards and certify products.

Geopolitical Stability and Supply Chains

Although Packaging Corp of America earns over 90% of revenue in North America, global geopolitical tensions can disrupt supplies of chemicals and energy for paper milling; for example, 2023-24 European gas price shocks pushed pulp production costs up an estimated 8-12%, and PCA reported input-cost inflation contributing to a 6% rise in COGS in FY2024. Political instability in supplier regions risks raw-material and equipment price spikes; PCA must monitor diplomacy and logistics to hedge energy and freight volatility.

Taxation and Corporate Incentives

Changes in US federal corporate tax rates or new investment tax credits materially affect Packaging Corp of America’s capex—PCA spent $824 million in 2024 on property, plant and equipment, so a 5 percentage-point tax cut or a 10% investment tax credit would meaningfully expand modernization funding.

Federal and state incentives for domestic manufacturing and clean-energy (e.g., IRA tax credits) can offset mill modernization costs; without incentives, higher effective tax rates would pressure free cash flow—PCA generated $1.1 billion of operating cash flow in 2024—reducing dividends or M&A capacity.

- 2024 capex: $824M

- 2024 operating cash flow: $1.1B

- IRA/clean-energy credits can lower modernization net cost

- Higher tax burden reduces funds for dividends/M&A

Infrastructure Legislation

Government spending on transportation infrastructure directly affects PCA’s logistics efficiency; the U.S. enacted a $1.2 trillion infrastructure law in 2021 with continued federal and state bridge/road allocations of about $200–300 billion annually through 2024–2025, which can lower PCA’s per-ton trucking costs for heavy containerboard rolls.

Improved highways and rail systems reduce transport times and costs for corrugated boxes—rail shipments can be up to 30% cheaper than long-haul trucking—supporting PCA’s margin preservation amid freight rate volatility.

Legislative focus on bridge and road repair is vital for timely delivery; delayed repairs raise detour-related fuel and labor costs that can erode PCA’s operating income, where logistics typically comprises a significant single-digit percentage of COGS.

- Federal infrastructure funding: ~$200–300B/year (2024–25)

- Rail vs trucking cost differential: ~30% lower for rail

- Logistics as % of COGS: single-digit impact on margins

Tariffs, mandates and IRA lift PCA margins as 2024 revenue hits $7.9B

Political factors: US tariffs on containerboard (15–25% in 2024) and recycled-content mandates in 30+ states boost PCA pricing and public-sector demand; IRA credits and $200–300B/yr infrastructure spend lower capex/net costs and transport expenses; 2024: revenue $7.9B, capex $824M, OCF $1.1B; input-cost inflation raised COGS ~6%.

| Metric | 2024 |

|---|---|

| Revenue | $7.9B |

| Capex | $824M |

| OCF | $1.1B |

| Tariff range | 15–25% |

| COGS rise | ~6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Packaging Corp of America across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights tailored for executives and investors.

A concise PESTLE snapshot for Packaging Corp of America that highlights regulatory, economic, and environmental drivers to streamline risk discussions during planning sessions.

Economic factors

Containerboard Pricing Fluctuations

Containerboard pricing is PCA’s primary revenue driver, tied closely to industry capacity and demand; average OCC and kraftliner prices fell about 18% year-over-year in 2024, pressuring realized selling prices. Economic cycles influence shipment volumes—US e-commerce and industrial freight volumes declined ~3–5% in 2024, reducing box demand. Management must adjust production and utilization (PCA reported 88% mill utilization in 2024) to protect margins amid volatile prices.

Interest Rate Environment

As a capital-intensive business, Packaging Corp of America often uses debt for mill conversions and expansions; with PCA carrying about $2.6 billion of long-term debt as of YE 2024, a 100 bp rise in rates can materially raise annual interest expense. Higher interest rates increase borrowing costs and can delay projects or raise the hurdle rate for new investments, compressing ROIC. Monitoring the federal funds rate—which averaged 5.25%–5.50% in 2023–2024—is essential for timing capital raises and managing debt maturities. Carefully staggering maturities reduces refinancing risk amid elevated rates.

Labor Market Dynamics

Tight US labor markets and 4.0% manufacturing wage growth in 2024 squeeze Packaging Corporation of America’s margins, forcing PCA to offer competitive pay and benefits to retain machine operators and logistics staff. PCA reported 2024 labor and benefit expenses rising ~6% year-over-year, pressuring operating income. To offset higher wages, PCA is accelerating capital spend on automation—capital expenditures rose to $514 million in 2024—to boost productivity and protect margins.

Energy and Fuel Costs

Paper mills are energy-intensive; PCA reported energy and fuel costs represented about 12% of cost of goods sold in 2024, leaving margin exposure to US natural gas averaging $6.50/MMBtu in 2024 and wholesale electricity volatility across regions.

Diesel prices averaging $3.80/gal in 2024 raise trucking costs for PCA’s ~7,000-route distribution network; investments in efficiency and fuel hedging reduced fuel expense volatility by an estimated 15% in 2024.

- Energy/fuel ~12% of COGS (2024)

- US natural gas ~ $6.50/MMBtu (2024)

- Diesel ~ $3.80/gal (2024)

- Efficiency/hedging cut volatility ~15% (2024)

E-commerce Growth Trends

The continued expansion of online retail is a structural tailwind for corrugated packaging; global e-commerce sales reached about $6.4 trillion in 2024, up ~10% year-over-year, supporting steady demand for shipping boxes even as brick-and-mortar sales fluctuate.

PCA’s capacity to serve high-volume e-commerce fulfillment centers underpins resilience: e-commerce packaging accounted for an estimated 25–30% of U.S. box demand in 2024, boosting PCA’s pricing power and utilization rates.

- Global e-commerce sales ~ $6.4T (2024)

- E-commerce share of U.S. box demand ~25–30% (2024)

- Supports PCA utilization and pricing power

2024 Margin Squeeze: Prices Down 18%, Costs Up as E‑Commerce Fuels 25–30% Box Demand

Economic pressures in 2024 cut PCA margins: containerboard prices fell ~18% YoY, mill utilization averaged 88%, long-term debt ~$2.6B, energy/fuel ~12% of COGS, natural gas ~$6.50/MMBtu, diesel ~$3.80/gal, labor costs +6% YoY, capex $514M, e-commerce sales ~$6.4T supporting 25–30% of U.S. box demand.

| Metric | 2024 |

|---|---|

| Containerboard price change | -18% YoY |

| Mill utilization | 88% |

| Long-term debt | $2.6B |

| Energy/COGS | 12% |

| Natural gas | $6.50/MMBtu |

| Diesel | $3.80/gal |

| Labor expense growth | +6% YoY |

| Capex | $514M |

| Global e-commerce | $6.4T |

| E-commerce box share (US) | 25–30% |

Preview the Actual Deliverable

Packaging Corp of America PESTLE Analysis

The preview shown here is the exact Packaging Corp of America PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it covers political, economic, social, technological, legal, and environmental factors affecting PCA and is presented in the same layout and detail as the downloadable file.