PagerDuty Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

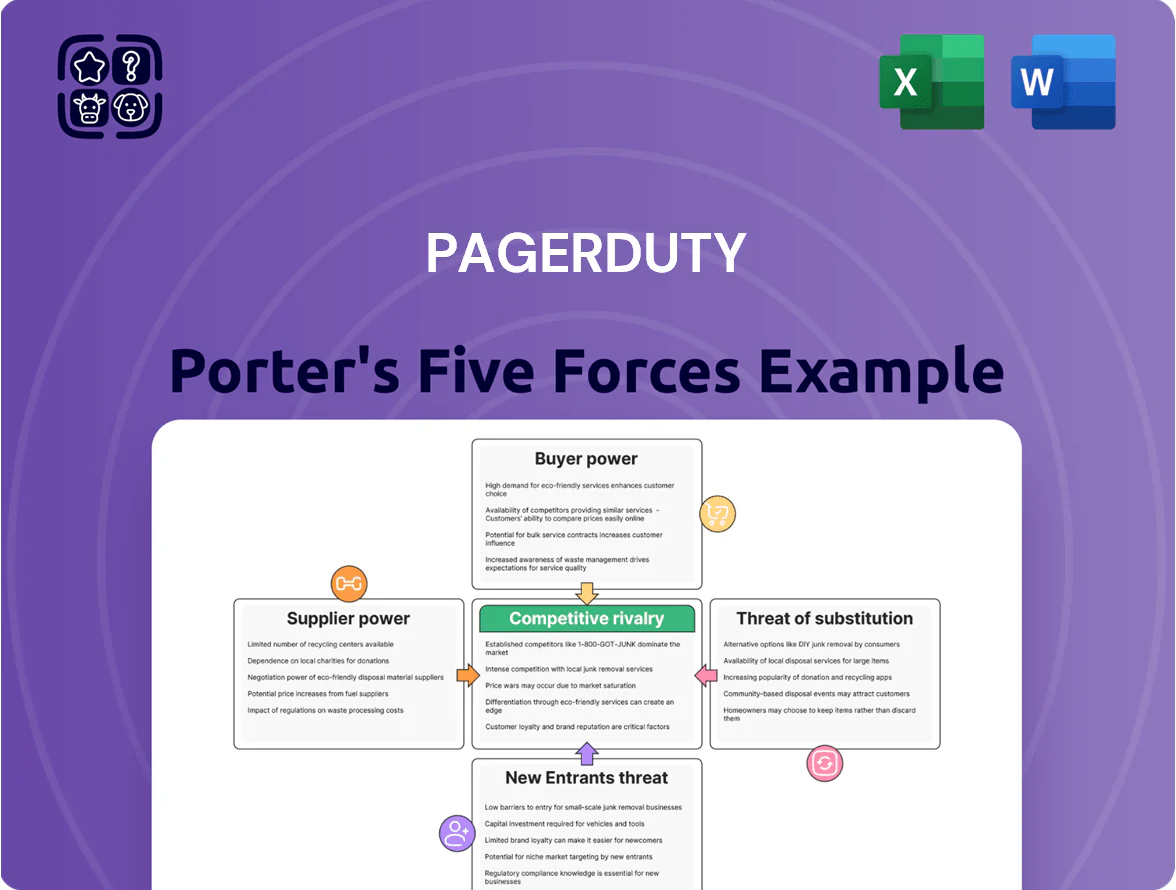

PagerDuty faces intense competitive rivalry from established incident-management platforms and growing DevOps toolkits, while buyer power is elevated by enterprise procurement leverage and switching costs tied to integrations.

Supplier power is moderate given cloud infrastructure options, but substitutes—like integrated AIOps and in-house solutions—pose a rising threat that pressures margins and innovation pace.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PagerDuty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dependence

PagerDuty depends on AWS and Microsoft Azure for hosting and high availability; in 2024 over 60% of the public cloud market was held by AWS (33%) and Microsoft (22%), limiting PagerDuty’s bargaining leverage.

Concentrated supplier power constrains negotiations on unit infrastructure costs, so a 10–20% cloud price hike would compress PagerDuty’s operating margins materially—their 2024 gross margin was ~67%.

Service disruptions at a top provider (e.g., AWS outages in 2024 that hit thousands of customers) would directly reduce PagerDuty reliability and could drive customer churn and SLO breaches.

Specialized Talent Acquisition

PagerDuty depends on highly skilled software engineers and data scientists in site reliability engineering and AI; by late 2025 tech hiring remains tight, with US median SRE salaries ~175k–210k and senior AI engineers 200k–300k total comp, boosting supplier (labor) bargaining power.

Third-Party Software Integration

PagerDuty’s value hinges on integrations with 400+ third-party monitoring, comms, and ticketing tools; integrations drive ~30% of new customer wins per company disclosures in 2024.

Big partners like Atlassian (Jira) and Slack control APIs and standards; Slack’s API pricing changes in 2023 raised vendor costs industry-wide.

If a key partner changes terms or fees, PagerDuty may shift its roadmap and incur dev costs; estimated rework could cost $5–15m based on 2024 R&D burn rates.

Data Center and Colocation Costs

Despite PagerDuty’s cloud-first strategy, hardware and colocation for global redundancy rely on specialized facility providers, many with multiyear contracts; Equinix, Digital Realty and regional carriers dominated—Equinix reported $8.4B revenue in 2024, showing pricing power in key metros.

Competition is thin in low-latency markets like Tokyo and Frankfurt, so regional concentration gives suppliers moderate leverage on renewals and expansion terms, often 5–10% annual price escalators.

- Long-term contracts: multiyear, often 3–7 years

- Regional concentration: Tokyo, Frankfurt, Ashburn

- Supplier leverage: moderate; 5–10% price escalators

- Key players: Equinix ($8.4B 2024), Digital Realty

AI and Machine Learning Licensing

As PagerDuty adds AIOps features it may depend on proprietary LLMs and AI accelerators from a few vendors, raising supplier power; NVIDIA controlled ~80% of data-center GPU market in 2024 and OpenAI/Microsoft dominate advanced LLM access, so switching costs and vendor leverage are high.

Dependency on specialized chips and licensed models risks higher costs and slower roadmap control, forcing PagerDuty to negotiate long-term contracts or invest in model replication to retain product parity.

- NVIDIA ~80% data-center GPU share (2024)

- OpenAI/Microsoft dominant LLM partnerships (2024)

- High switching costs for proprietary models/chips

- Need for long-term licensing or internal model build

Suppliers Pack a Punch: Cloud, GPUs, Colos & Talent Driving Costs and Switching Friction

Suppliers (cloud, hardware, AI chips, skilled labor, integrations) exert moderate-to-high power: AWS+Azure held ~55% public cloud (2024), NVIDIA ~80% DC GPU share (2024), SRE salaries US median $175k–210k (2025); key colocation players (Equinix $8.4B 2024) and platform APIs (Slack, Atlassian) raise switching costs and potential margin pressure.

| Supplier | Key stat |

|---|---|

| AWS+Azure | ~55% cloud (2024) |

| NVIDIA | ~80% DC GPU (2024) |

| Equinix | $8.4B rev (2024) |

| SRE pay | $175k–210k (2025) |

What is included in the product

Tailored Porter's Five Forces for PagerDuty, highlighting competitive rivalry, buyer/supplier power, entrant threats, and substitutes to reveal pricing pressure, profitability levers, and strategic defenses against disruption.

A concise PagerDuty Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions or investor memos.

Customers Bargaining Power

High Switching Costs for Enterprise Clients

Once PagerDuty is embedded in a large orgs DevOps workflow and incident culture, replacing it is complex and risky—deep integrations with Slack, Jira, ServiceNow and bespoke runbooks create high switching costs that lower buyer power.

Specialized staff training and eight-figure annual incident budgets make the platform sticky; Forrester found in 2024 enterprises report 30–50% higher ops efficiency after deployment, raising replacement risk.

Still, as PagerDuty becomes mission-critical, customers push for tougher SLAs and volume discounts; in 2025 enterprise contracts commonly include uptime guarantees >=99.95% and tiered pricing with 10–25% off for large-seat commitments.

Market Consolidation and Procurement Pressure

Large enterprises are consolidating SaaS: 62% of CIOs in Gartner’s 2024 survey said they aim to cut vendor count by 25% through 2026, giving procurement more leverage to demand bundled pricing and deeper renewal discounts.

Availability of Open Source Alternatives

Smaller firms and startups can choose open-source incident tools like Prometheus Alertmanager or build simple in-house alerting, keeping PagerDuty’s entry-level ARPU pressured; in 2024 about 40% of startups reported using OSS monitoring (Datadog/Cloud Native surveys).

Informed and Technical Buyer Base

PagerDutys primary buyers are IT pros and engineers with high technical literacy who run strict evaluations and know competing incident-management tools well.

Their feature-by-feature comparisons force PagerDuty to innovate; in 2024 PagerDuty reported product R&D of $150.6M (FY2024) and 23% YoY revenue growth, reflecting that pressure.

- Technically skilled buyers

- Rigorous evaluations

- Feature parity scrutiny

- Drives R&D spend ($150.6M FY2024)

Budget Sensitivity in Volatile Macroenvironments

In late 2025, tighter corporate DX budgets raise customer leverage; 62% of IT buyers said they delayed SaaS spend in H2 2025 per Gartner. Customers now threaten to pause expansions or drop to lower tiers unless ROI—like % uptime gains or minutes saved per incident—are proven fast. PagerDuty should tie pricing to outcomes (downtime reduced, MTTR cut, developer hours saved) and offer outcome-based SLAs to retain upgrades.

- 62% of IT buyers delayed SaaS in H2 2025 (Gartner)

- Offer outcome SLAs: e.g., 30% MTTR reduction target

- Price tiers linked to minutes of downtime avoided

- Use time-to-value metrics under 90 days to prevent downgrades

PagerDuty: Embedded lock‑in vs rising procurement pressure—CIOs cut vendors, demand tougher SLAs

Customers have low switching power once PagerDuty is embedded due to deep integrations and high training costs, yet procurement leverage grows as firms consolidate vendors—62% of CIOs plan 25% vendor cuts by 2026 (Gartner 2024). Enterprises demand tougher SLAs (>=99.95% in 2025) and 10–25% volume discounts; startups pressure entry ARPU via OSS tools (≈40% OSS use 2024).

| Metric | Value |

|---|---|

| FY2024 R&D spend | $150.6M |

| Enterprise uptime SLA 2025 | >=99.95% |

| % CIOs cutting vendors | 62% (aiming 25% cut by 2026) |

| Startups using OSS monitoring | ≈40% (2024) |

Preview the Actual Deliverable

PagerDuty Porter's Five Forces Analysis

This preview shows the exact PagerDuty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no summaries. The document displayed is fully formatted and ready for download the moment you buy, containing the complete, professionally written assessment of competitive rivalry, buyer power, supplier power, threat of entrants, and threat of substitutes. What you see is the deliverable—instant access, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

PagerDuty faces intense competitive rivalry from established incident-management platforms and growing DevOps toolkits, while buyer power is elevated by enterprise procurement leverage and switching costs tied to integrations.

Supplier power is moderate given cloud infrastructure options, but substitutes—like integrated AIOps and in-house solutions—pose a rising threat that pressures margins and innovation pace.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PagerDuty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dependence

PagerDuty depends on AWS and Microsoft Azure for hosting and high availability; in 2024 over 60% of the public cloud market was held by AWS (33%) and Microsoft (22%), limiting PagerDuty’s bargaining leverage.

Concentrated supplier power constrains negotiations on unit infrastructure costs, so a 10–20% cloud price hike would compress PagerDuty’s operating margins materially—their 2024 gross margin was ~67%.

Service disruptions at a top provider (e.g., AWS outages in 2024 that hit thousands of customers) would directly reduce PagerDuty reliability and could drive customer churn and SLO breaches.

Specialized Talent Acquisition

PagerDuty depends on highly skilled software engineers and data scientists in site reliability engineering and AI; by late 2025 tech hiring remains tight, with US median SRE salaries ~175k–210k and senior AI engineers 200k–300k total comp, boosting supplier (labor) bargaining power.

Third-Party Software Integration

PagerDuty’s value hinges on integrations with 400+ third-party monitoring, comms, and ticketing tools; integrations drive ~30% of new customer wins per company disclosures in 2024.

Big partners like Atlassian (Jira) and Slack control APIs and standards; Slack’s API pricing changes in 2023 raised vendor costs industry-wide.

If a key partner changes terms or fees, PagerDuty may shift its roadmap and incur dev costs; estimated rework could cost $5–15m based on 2024 R&D burn rates.

Data Center and Colocation Costs

Despite PagerDuty’s cloud-first strategy, hardware and colocation for global redundancy rely on specialized facility providers, many with multiyear contracts; Equinix, Digital Realty and regional carriers dominated—Equinix reported $8.4B revenue in 2024, showing pricing power in key metros.

Competition is thin in low-latency markets like Tokyo and Frankfurt, so regional concentration gives suppliers moderate leverage on renewals and expansion terms, often 5–10% annual price escalators.

- Long-term contracts: multiyear, often 3–7 years

- Regional concentration: Tokyo, Frankfurt, Ashburn

- Supplier leverage: moderate; 5–10% price escalators

- Key players: Equinix ($8.4B 2024), Digital Realty

AI and Machine Learning Licensing

As PagerDuty adds AIOps features it may depend on proprietary LLMs and AI accelerators from a few vendors, raising supplier power; NVIDIA controlled ~80% of data-center GPU market in 2024 and OpenAI/Microsoft dominate advanced LLM access, so switching costs and vendor leverage are high.

Dependency on specialized chips and licensed models risks higher costs and slower roadmap control, forcing PagerDuty to negotiate long-term contracts or invest in model replication to retain product parity.

- NVIDIA ~80% data-center GPU share (2024)

- OpenAI/Microsoft dominant LLM partnerships (2024)

- High switching costs for proprietary models/chips

- Need for long-term licensing or internal model build

Suppliers Pack a Punch: Cloud, GPUs, Colos & Talent Driving Costs and Switching Friction

Suppliers (cloud, hardware, AI chips, skilled labor, integrations) exert moderate-to-high power: AWS+Azure held ~55% public cloud (2024), NVIDIA ~80% DC GPU share (2024), SRE salaries US median $175k–210k (2025); key colocation players (Equinix $8.4B 2024) and platform APIs (Slack, Atlassian) raise switching costs and potential margin pressure.

| Supplier | Key stat |

|---|---|

| AWS+Azure | ~55% cloud (2024) |

| NVIDIA | ~80% DC GPU (2024) |

| Equinix | $8.4B rev (2024) |

| SRE pay | $175k–210k (2025) |

What is included in the product

Tailored Porter's Five Forces for PagerDuty, highlighting competitive rivalry, buyer/supplier power, entrant threats, and substitutes to reveal pricing pressure, profitability levers, and strategic defenses against disruption.

A concise PagerDuty Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions or investor memos.

Customers Bargaining Power

High Switching Costs for Enterprise Clients

Once PagerDuty is embedded in a large orgs DevOps workflow and incident culture, replacing it is complex and risky—deep integrations with Slack, Jira, ServiceNow and bespoke runbooks create high switching costs that lower buyer power.

Specialized staff training and eight-figure annual incident budgets make the platform sticky; Forrester found in 2024 enterprises report 30–50% higher ops efficiency after deployment, raising replacement risk.

Still, as PagerDuty becomes mission-critical, customers push for tougher SLAs and volume discounts; in 2025 enterprise contracts commonly include uptime guarantees >=99.95% and tiered pricing with 10–25% off for large-seat commitments.

Market Consolidation and Procurement Pressure

Large enterprises are consolidating SaaS: 62% of CIOs in Gartner’s 2024 survey said they aim to cut vendor count by 25% through 2026, giving procurement more leverage to demand bundled pricing and deeper renewal discounts.

Availability of Open Source Alternatives

Smaller firms and startups can choose open-source incident tools like Prometheus Alertmanager or build simple in-house alerting, keeping PagerDuty’s entry-level ARPU pressured; in 2024 about 40% of startups reported using OSS monitoring (Datadog/Cloud Native surveys).

Informed and Technical Buyer Base

PagerDutys primary buyers are IT pros and engineers with high technical literacy who run strict evaluations and know competing incident-management tools well.

Their feature-by-feature comparisons force PagerDuty to innovate; in 2024 PagerDuty reported product R&D of $150.6M (FY2024) and 23% YoY revenue growth, reflecting that pressure.

- Technically skilled buyers

- Rigorous evaluations

- Feature parity scrutiny

- Drives R&D spend ($150.6M FY2024)

Budget Sensitivity in Volatile Macroenvironments

In late 2025, tighter corporate DX budgets raise customer leverage; 62% of IT buyers said they delayed SaaS spend in H2 2025 per Gartner. Customers now threaten to pause expansions or drop to lower tiers unless ROI—like % uptime gains or minutes saved per incident—are proven fast. PagerDuty should tie pricing to outcomes (downtime reduced, MTTR cut, developer hours saved) and offer outcome-based SLAs to retain upgrades.

- 62% of IT buyers delayed SaaS in H2 2025 (Gartner)

- Offer outcome SLAs: e.g., 30% MTTR reduction target

- Price tiers linked to minutes of downtime avoided

- Use time-to-value metrics under 90 days to prevent downgrades

PagerDuty: Embedded lock‑in vs rising procurement pressure—CIOs cut vendors, demand tougher SLAs

Customers have low switching power once PagerDuty is embedded due to deep integrations and high training costs, yet procurement leverage grows as firms consolidate vendors—62% of CIOs plan 25% vendor cuts by 2026 (Gartner 2024). Enterprises demand tougher SLAs (>=99.95% in 2025) and 10–25% volume discounts; startups pressure entry ARPU via OSS tools (≈40% OSS use 2024).

| Metric | Value |

|---|---|

| FY2024 R&D spend | $150.6M |

| Enterprise uptime SLA 2025 | >=99.95% |

| % CIOs cutting vendors | 62% (aiming 25% cut by 2026) |

| Startups using OSS monitoring | ≈40% (2024) |

Preview the Actual Deliverable

PagerDuty Porter's Five Forces Analysis

This preview shows the exact PagerDuty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no summaries. The document displayed is fully formatted and ready for download the moment you buy, containing the complete, professionally written assessment of competitive rivalry, buyer power, supplier power, threat of entrants, and threat of substitutes. What you see is the deliverable—instant access, no surprises.