Pan American Silver Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

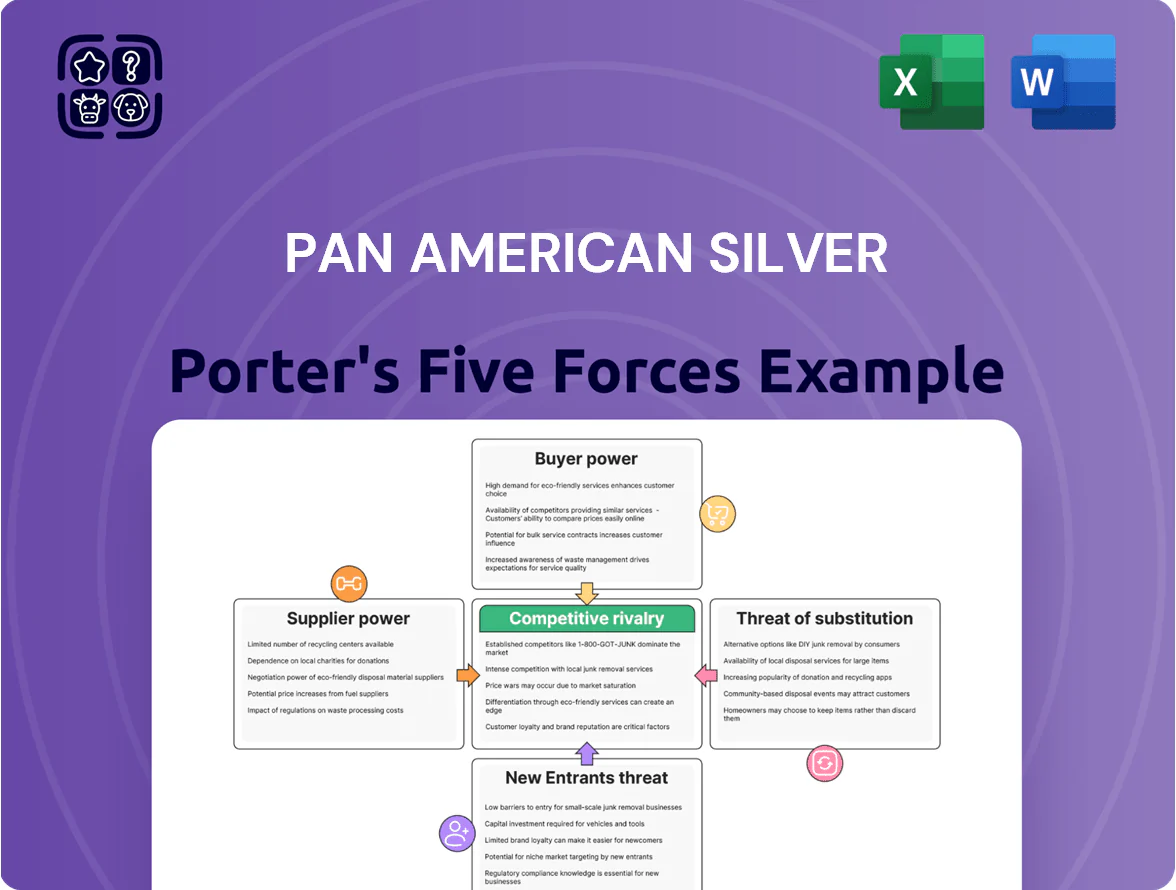

Pan American Silver faces moderate supplier power, cyclical commodity pricing, and mid-level rivalry tied to large miners and regional producers—factors that shape margins and expansion choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Pan American Silver’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Mining Equipment Providers

The heavy machinery market is concentrated: Caterpillar and Komatsu held roughly 30–40% global market share in 2024 for mining equipment, so Pan American Silver faces limited bargaining power; these suppliers also provide critical tech and aftermarket services, constraining price cuts. The specialized nature of fleets means high vendor dependence for uptime and a capital stock replacement cost exposure—Pan American reported $1.1bn in property, plant and equipment at end-2024, much of which relies on OEM support.

Energy and Fuel Costs

Mining operations need large diesel and grid power; Pan American Silver consumed about 1.1 million GJ of fuel and electricity in 2024, making energy a material input cost.

Pan American is a price taker in global oil and gas markets, so 2022–24 oil price swings raised operating costs and pushed fuel-related COGS volatility into margins.

The company is shifting to renewables—targeting 30% site renewables by 2026—to reduce supplier leverage and lower fuel spend over time.

Labor Unions and Skilled Workforce

In Latin America, where Pan American Silver operates, union density often exceeds 30% in mining regions, giving unions strong leverage over wages and benefits and raising strike risk; in 2024 Pan American reported labour costs up ~8% year-over-year. Global shortages of mining engineers—ICMM estimated a ~15% shortfall in skilled roles in 2023—intensify hiring competition, pushing wages and contractor rates higher and risking production delays if negotiations stall.

Chemical Reagents and Consumables

The extraction and processing of silver and base metals need specific reagents like cyanide and grinding media; global reagent market was valued at about $32.4B in 2024, with mining chemicals ~14% of that, concentrating supplier activity.

Multiple suppliers exist, but hazardous-material logistics to remote mines limit choices to local/regional providers, raising supplier pricing power; spot cyanide freight to Peru/Argentina added ~12–18% in 2024.

Geographic constraint gives those suppliers leverage over pricing and contract terms, increasing Pan American Silver’s input cost volatility and procurement risk.

- Mining chemicals market ~$4.5B (2024)

- Regional delivery premium 12–18% (2024)

- Local suppliers reduce sourcing alternatives

- Higher input cost volatility for Pan American Silver

Logistics and Infrastructure Services

Pan American Silver depends on third-party transport for concentrates and refined metals; in 2024 roughly 35% of outbound volume used regional rail/truck routes that lack redundancy, raising supplier leverage.

In areas with single-provider rails or trucking, that provider can extract higher rates or prioritize other shippers, and a 7–14 day disruption can defer revenue recognition and raise working-capital needs.

- ~35% outbound via limited routes (2024)

- Single-provider exposure per mine raises rates

- 7–14 day disruption delays cash inflows

Supplier concentration and logistics risk threaten Pan American’s operations and cash flow

Suppliers hold moderate-to-high power: concentrated OEMs (Caterpillar/Komatsu 30–40% share, 2024) and specialized reagents/transport raise costs and dependency; Pan American had $1.1bn PPE and used ~1.1m GJ energy in 2024, with mining chemicals market ~$4.5B and regional freight premiums 12–18%, while ~35% outbound relies on limited routes, causing 7–14 day disruption risk to cash flows.

| Metric | Value (2024) |

|---|---|

| OEM market share | 30–40% |

| PPE | $1.1bn |

| Energy use | ~1.1m GJ |

| Mining chemicals market | $4.5B |

| Freight premium | 12–18% |

| Outbound via limited routes | ~35% |

| Disruption delay | 7–14 days |

What is included in the product

Tailored Porter's Five Forces for Pan American Silver, uncovering competitive rivalry, supplier and buyer power, entry barriers, and substitutes to highlight strategic risks and opportunities shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Pan American Silver—quickly spot supplier, buyer, and substitute pressures to inform mine-level and corporate strategy.

Customers Bargaining Power

Commodity Price Taking

As a primary silver and gold producer, Pan American Silver sells into global markets where prices are set by exchanges like the London Bullion Market Association (LBMA); individual miners cannot materially influence spot prices. Customers—refiners, fabricators, and traders—effectively take prices driven by global supply/demand, making Pan American highly revenue-sensitive to metal price moves (silver fell ~12% in 2024) and FX shifts (25% of costs in USD vs. revenues in USD).

Smelter and Refinery Concentration

Standardized Product Nature

Silver and gold are fungible commodities, so Pan American Silver’s metal is indistinguishable from competitors’; in 2025 global silver mine supply was ~640 Moz and demand ~750 Moz, letting buyers shift sources easily. Customers favor lowest landed cost and can switch for small logistics or timing gains, eroding producer pricing power. In 2024 Pan American sold 24.1 Moz silver equivalent, but faces limited brand leverage versus traders and smelters.

Industrial Demand Sensitivity

- ~50% industrial share (2024)

- PV/electronics can substitute metals

- Large buyers can force long-term contracts

- 1% PV change ≈ 5–10 Moz demand swing

Low Switching Costs for Investors

In silver as a financial asset, institutional investors and ETFs can reallocate capital between mining stocks or bullion quickly; by end-2024 global silver ETF holdings were ~557.7 Moz equivalent, showing high liquidity that raises investor bargaining power over miners like Pan American Silver (PAAS).

PAAS must keep costs low (2024 AISC about $15.70/oz) and disclose transparently; poor performance or missed 2025 guidance would trigger rapid outflows and downward pressure on market valuation.

- High liquidity: 557.7 Moz ETF holdings (2024)

- PAAS 2024 AISC: $15.70/oz

- Investors can exit instantly via ETFs or stock trades

- Transparency and cost control directly affect valuation

Concentrated processors, ETFs & TRC cuts squeeze silver miners’ margins

Customers have strong bargaining power: prices set by LBMA; 60–70% of payable metals flowed through top five smelters in 2024; TRC cuts ~$4–6/oz Ag-eq (2024); global silver supply ~640 Moz vs demand ~750 Moz (2025); ETFs held ~557.7 Moz end-2024; PAAS 2024 AISC $15.70/oz—concentrated processors, fungibility, substitution risk and liquid ETF flows compress miner margins.

| Metric | Value |

|---|---|

| Top-5 processor share (2024) | 60–70% |

| TRC cuts (2024) | $4–6/oz Ag-eq |

| Silver supply (2025) | ~640 Moz |

| Silver demand (2025) | ~750 Moz |

| ETF holdings (end-2024) | ~557.7 Moz |

| PAAS AISC (2024) | $15.70/oz |

Same Document Delivered

Pan American Silver Porter's Five Forces Analysis

This preview shows the exact Pan American Silver Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Pan American Silver faces moderate supplier power, cyclical commodity pricing, and mid-level rivalry tied to large miners and regional producers—factors that shape margins and expansion choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Pan American Silver’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Mining Equipment Providers

The heavy machinery market is concentrated: Caterpillar and Komatsu held roughly 30–40% global market share in 2024 for mining equipment, so Pan American Silver faces limited bargaining power; these suppliers also provide critical tech and aftermarket services, constraining price cuts. The specialized nature of fleets means high vendor dependence for uptime and a capital stock replacement cost exposure—Pan American reported $1.1bn in property, plant and equipment at end-2024, much of which relies on OEM support.

Energy and Fuel Costs

Mining operations need large diesel and grid power; Pan American Silver consumed about 1.1 million GJ of fuel and electricity in 2024, making energy a material input cost.

Pan American is a price taker in global oil and gas markets, so 2022–24 oil price swings raised operating costs and pushed fuel-related COGS volatility into margins.

The company is shifting to renewables—targeting 30% site renewables by 2026—to reduce supplier leverage and lower fuel spend over time.

Labor Unions and Skilled Workforce

In Latin America, where Pan American Silver operates, union density often exceeds 30% in mining regions, giving unions strong leverage over wages and benefits and raising strike risk; in 2024 Pan American reported labour costs up ~8% year-over-year. Global shortages of mining engineers—ICMM estimated a ~15% shortfall in skilled roles in 2023—intensify hiring competition, pushing wages and contractor rates higher and risking production delays if negotiations stall.

Chemical Reagents and Consumables

The extraction and processing of silver and base metals need specific reagents like cyanide and grinding media; global reagent market was valued at about $32.4B in 2024, with mining chemicals ~14% of that, concentrating supplier activity.

Multiple suppliers exist, but hazardous-material logistics to remote mines limit choices to local/regional providers, raising supplier pricing power; spot cyanide freight to Peru/Argentina added ~12–18% in 2024.

Geographic constraint gives those suppliers leverage over pricing and contract terms, increasing Pan American Silver’s input cost volatility and procurement risk.

- Mining chemicals market ~$4.5B (2024)

- Regional delivery premium 12–18% (2024)

- Local suppliers reduce sourcing alternatives

- Higher input cost volatility for Pan American Silver

Logistics and Infrastructure Services

Pan American Silver depends on third-party transport for concentrates and refined metals; in 2024 roughly 35% of outbound volume used regional rail/truck routes that lack redundancy, raising supplier leverage.

In areas with single-provider rails or trucking, that provider can extract higher rates or prioritize other shippers, and a 7–14 day disruption can defer revenue recognition and raise working-capital needs.

- ~35% outbound via limited routes (2024)

- Single-provider exposure per mine raises rates

- 7–14 day disruption delays cash inflows

Supplier concentration and logistics risk threaten Pan American’s operations and cash flow

Suppliers hold moderate-to-high power: concentrated OEMs (Caterpillar/Komatsu 30–40% share, 2024) and specialized reagents/transport raise costs and dependency; Pan American had $1.1bn PPE and used ~1.1m GJ energy in 2024, with mining chemicals market ~$4.5B and regional freight premiums 12–18%, while ~35% outbound relies on limited routes, causing 7–14 day disruption risk to cash flows.

| Metric | Value (2024) |

|---|---|

| OEM market share | 30–40% |

| PPE | $1.1bn |

| Energy use | ~1.1m GJ |

| Mining chemicals market | $4.5B |

| Freight premium | 12–18% |

| Outbound via limited routes | ~35% |

| Disruption delay | 7–14 days |

What is included in the product

Tailored Porter's Five Forces for Pan American Silver, uncovering competitive rivalry, supplier and buyer power, entry barriers, and substitutes to highlight strategic risks and opportunities shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Pan American Silver—quickly spot supplier, buyer, and substitute pressures to inform mine-level and corporate strategy.

Customers Bargaining Power

Commodity Price Taking

As a primary silver and gold producer, Pan American Silver sells into global markets where prices are set by exchanges like the London Bullion Market Association (LBMA); individual miners cannot materially influence spot prices. Customers—refiners, fabricators, and traders—effectively take prices driven by global supply/demand, making Pan American highly revenue-sensitive to metal price moves (silver fell ~12% in 2024) and FX shifts (25% of costs in USD vs. revenues in USD).

Smelter and Refinery Concentration

Standardized Product Nature

Silver and gold are fungible commodities, so Pan American Silver’s metal is indistinguishable from competitors’; in 2025 global silver mine supply was ~640 Moz and demand ~750 Moz, letting buyers shift sources easily. Customers favor lowest landed cost and can switch for small logistics or timing gains, eroding producer pricing power. In 2024 Pan American sold 24.1 Moz silver equivalent, but faces limited brand leverage versus traders and smelters.

Industrial Demand Sensitivity

- ~50% industrial share (2024)

- PV/electronics can substitute metals

- Large buyers can force long-term contracts

- 1% PV change ≈ 5–10 Moz demand swing

Low Switching Costs for Investors

In silver as a financial asset, institutional investors and ETFs can reallocate capital between mining stocks or bullion quickly; by end-2024 global silver ETF holdings were ~557.7 Moz equivalent, showing high liquidity that raises investor bargaining power over miners like Pan American Silver (PAAS).

PAAS must keep costs low (2024 AISC about $15.70/oz) and disclose transparently; poor performance or missed 2025 guidance would trigger rapid outflows and downward pressure on market valuation.

- High liquidity: 557.7 Moz ETF holdings (2024)

- PAAS 2024 AISC: $15.70/oz

- Investors can exit instantly via ETFs or stock trades

- Transparency and cost control directly affect valuation

Concentrated processors, ETFs & TRC cuts squeeze silver miners’ margins

Customers have strong bargaining power: prices set by LBMA; 60–70% of payable metals flowed through top five smelters in 2024; TRC cuts ~$4–6/oz Ag-eq (2024); global silver supply ~640 Moz vs demand ~750 Moz (2025); ETFs held ~557.7 Moz end-2024; PAAS 2024 AISC $15.70/oz—concentrated processors, fungibility, substitution risk and liquid ETF flows compress miner margins.

| Metric | Value |

|---|---|

| Top-5 processor share (2024) | 60–70% |

| TRC cuts (2024) | $4–6/oz Ag-eq |

| Silver supply (2025) | ~640 Moz |

| Silver demand (2025) | ~750 Moz |

| ETF holdings (end-2024) | ~557.7 Moz |

| PAAS AISC (2024) | $15.70/oz |

Same Document Delivered

Pan American Silver Porter's Five Forces Analysis

This preview shows the exact Pan American Silver Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.