Panda Restaurant Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

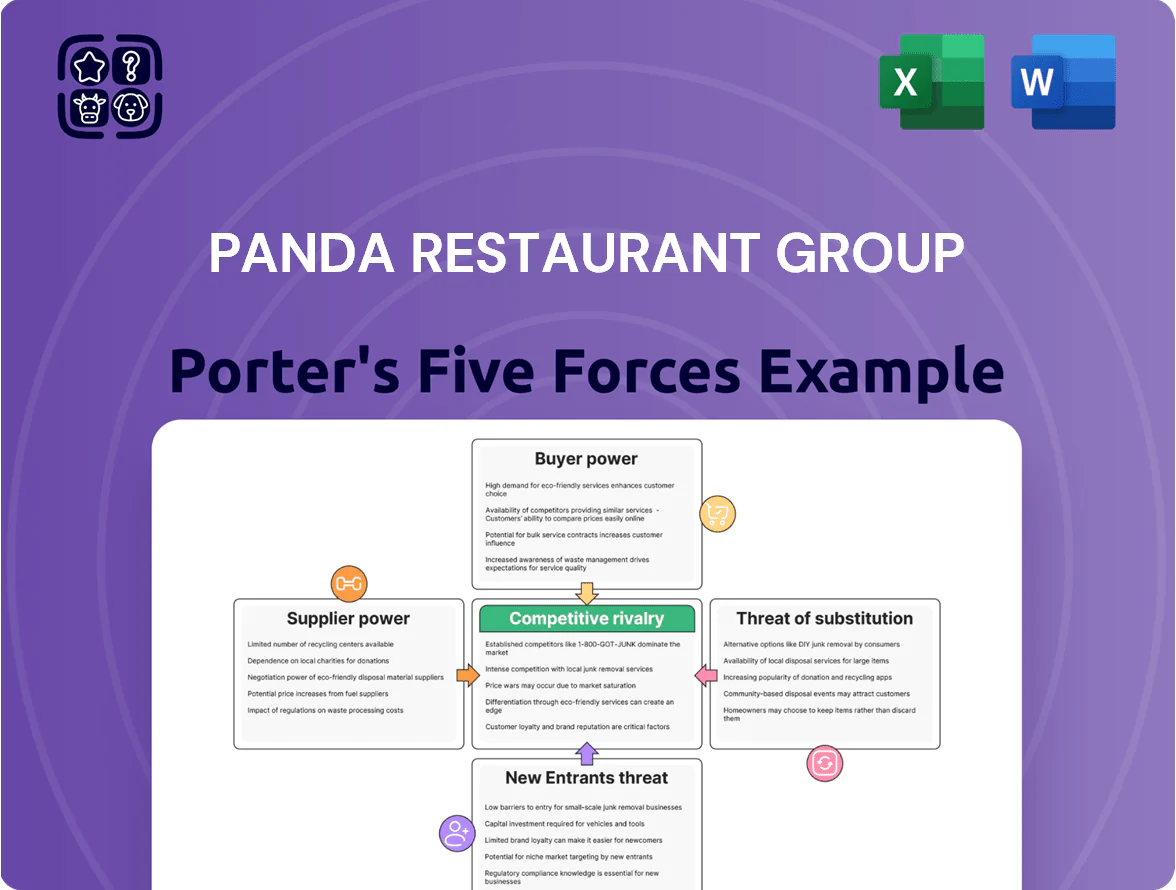

Panda Restaurant Group faces intense competitive rivalry and moderate supplier leverage, while brand loyalty and scale reduce buyer power and the threat of substitutes varies by segment; new entrants face high barriers from real estate and operational expertise. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Panda’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale-Driven Procurement Leverage

Panda Restaurant Group uses its scale—over 2,200 U.S. locations as of 2025—to negotiate lower input costs, securing protein and vegetable contracts (notably chicken and broccoli) at prices roughly 5–12% below market rates for smaller chains, per industry sourcing reports.

Buying volume lets Panda demand consistent quality and shorter lead times, shifting supply risks onto distributors who depend on Panda’s frequent orders that represent an estimated 3–7% of some suppliers’ revenue.

That volume-driven leverage compresses individual suppliers’ bargaining power, keeping input-cost inflation more contained for Panda than for regional competitors.

Commodity Price Vulnerability

Despite Panda Restaurant Group’s scale, it faces commodity risk: poultry, beef, and soybean oil account for ~18–22% of food cost; global pork and soybean price spikes in 2021–2022 raised input costs 10–25% industry-wide. When weather or trade limits supply, suppliers gain leverage, forcing Panda to absorb margins or lift menu prices. Panda therefore runs hedging programs and diversifies suppliers across US, Brazil, and China to limit single-supplier exposure.

Logistics and Distribution Dependencies

Panda Restaurant Group depends on third-party cold-chain logistics to deliver fresh ingredients to ~2,300 US locations daily; this scale gives Panda bargaining leverage but few specialized carriers can match its throughput.

In 2024 the US refrigerated trucking vacancy rate hit ~12%, and diesel averaged $3.80/gal—cost swings like these can raise carrier negotiating power and push short-term price or service concessions from Panda.

Ingredient Specialization and Quality Standards

Ingredient specialization for Panda Restaurant Group requires proprietary sauces and USDA-grade produce that meet strict safety and consistency specs, narrowing the supplier pool and raising supplier bargaining power—suppliers that qualify often secure steadier contracts and pricing leverage.

Panda offsets this by signing multi-year strategic partnerships and volume commitments; through 2024 Panda Supply Chain Investments reportedly increased supplier contract durations by ~25%, aligning supplier growth with its 2023–25 expansion.

- Proprietary sauces + USDA-grade produce limit suppliers

- Qualified suppliers gain pricing leverage

- Multi-year contracts reduce disruption

- Supplier contracts up ~25% in duration (2024)

Labor Market Dynamics as a Service Input

Skilled and entry-level labor has increased bargaining power for Panda Restaurant Group, as nationwide restaurant wages rose; by Q4 2025 average hourly pay for food service workers reached about $17.50, up ~12% year-over-year, pushing Panda to raise base pay and expand benefits, which lifted labor cost per store by an estimated 4–6% in 2025.

Higher minimum wages in key states (California, New York) and tight hiring markets forced more signing bonuses and scheduling flexibility, reducing turnover but compressing margins and adding pressure to menu pricing and automation investments.

- Avg food-service pay Q4 2025: ~$17.50/hr

- Estimated per-store labor cost increase 2025: 4–6%

- Turnover reduction vs 2024 after raises: ~8–10%

Panda’s scale cuts input costs 5–12% despite commodity spikes; contracts boost resilience

Panda’s scale (≈2,300 US stores, 2025) gives strong buying leverage—ingredient contracts 5–12% below peers—yet commodity spikes (poultry/soy 2021–22 +10–25%) and specialized suppliers/carriers raise supplier power; multi-year contracts (+25% duration, 2024) and geographic supplier mix (US/Brazil/China) mitigate risk.

| Metric | Value |

|---|---|

| Stores (2025) | ≈2,300 |

| Contract discount | 5–12% |

| Food cost exposure | 18–22% |

| Contract duration ↑ (2024) | +25% |

What is included in the product

Tailored Porter's Five Forces assessment of Panda Restaurant Group, uncovering competitive pressures, supplier and buyer influence, substitution risks, and barriers deterring new entrants to evaluate its strategic positioning and profitability.

A concise Porter's Five Forces snapshot for Panda Restaurant Group—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to guide menu, sourcing, and expansion strategy.

Customers Bargaining Power

Low Switching Costs for Diners

Low switching costs mean diners can choose a different fast-casual brand for their next meal with no penalty, so Panda Express must keep prices competitive and quality steady; NielsenIQ found 2024 U.S. fast-casual repeat visit rates fell 4% year-over-year, raising stakes for retention.

Heightened Price Sensitivity

Consumers in 2025 remain price-conscious after cumulative U.S. inflation rose ~18% from 2020–2024, so Panda faces customers quick to trade down to $5–7 fast-food value meals or cook at home as grocery prices stabilize.

This gives buyers leverage: same-day delivery and third-party apps magnify menu-price comparisons and switching.

Panda must weigh menu price rises against potential traffic loss—Q4 2024 quick-service volume fell ~2–4% industrywide when average check rose 3–5%.

Digital Empowerment and Information Access

Modern diners use apps and social media to see nutrition, ingredient lists, and realtime reviews—72% of US consumers consulted online reviews before dining in 2024, per Pew Research—so Panda Restaurant Group faces instant accountability for consistency across ~2,000 US locations; one viral food-safety or service failure can reach millions and dent same-store sales (SSS) by 1–3% in a quarter, giving customers strong indirect leverage over brand reputation.

Demand for Customization and Variety

Influence of Loyalty Programs

Digital rewards collect customer data in exchange for perks, letting Panda track visits and tailor offers; Panda Restaurant Group reported about 10 million loyalty members in 2024, driving repeat visits and higher AOV (average order value).

That data gives customers leverage to demand personalized deals and exclusives; if offers lag, customers shift—industry churn for weak loyalty apps can exceed 20% annually.

Tech-savvy guests defect to brands with better engagement, so a poor digital experience risks revenue loss and lower lifetime value.

- ~10M loyalty members (2024)

- Higher AOV from targeted offers

- >20% churn risk for weak apps

Buyers Gain Leverage: Inflation, Apps & Loyalty Threaten 20%+ Churn at Panda

Buyers have moderate-to-high leverage: low switching costs, price sensitivity after ~18% cumulative US inflation (2020–24), and real-time price/review comparison via delivery apps; Panda’s ~10M loyalty members (2024) help retention but weak digital offers risk >20% churn. Q4 2024 industry data: +3–5% check → −2–4% volume; niche fast-casual growing 8–12% annually.

| Metric | Value (2024) |

|---|---|

| Cumulative US inflation (2020–24) | ~18% |

| Panda loyalty members | ~10M |

| Check ↑ vs volume ↓ (Q4 2024) | +3–5% → −2–4% |

| App churn risk if poor | >20% annual |

| Niche fast-casual growth | 8–12% yr |

Preview the Actual Deliverable

Panda Restaurant Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Panda Restaurant Group you'll receive immediately after purchase—no placeholders or mockups; the full document is professionally formatted, comprehensive, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Panda Restaurant Group faces intense competitive rivalry and moderate supplier leverage, while brand loyalty and scale reduce buyer power and the threat of substitutes varies by segment; new entrants face high barriers from real estate and operational expertise. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Panda’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale-Driven Procurement Leverage

Panda Restaurant Group uses its scale—over 2,200 U.S. locations as of 2025—to negotiate lower input costs, securing protein and vegetable contracts (notably chicken and broccoli) at prices roughly 5–12% below market rates for smaller chains, per industry sourcing reports.

Buying volume lets Panda demand consistent quality and shorter lead times, shifting supply risks onto distributors who depend on Panda’s frequent orders that represent an estimated 3–7% of some suppliers’ revenue.

That volume-driven leverage compresses individual suppliers’ bargaining power, keeping input-cost inflation more contained for Panda than for regional competitors.

Commodity Price Vulnerability

Despite Panda Restaurant Group’s scale, it faces commodity risk: poultry, beef, and soybean oil account for ~18–22% of food cost; global pork and soybean price spikes in 2021–2022 raised input costs 10–25% industry-wide. When weather or trade limits supply, suppliers gain leverage, forcing Panda to absorb margins or lift menu prices. Panda therefore runs hedging programs and diversifies suppliers across US, Brazil, and China to limit single-supplier exposure.

Logistics and Distribution Dependencies

Panda Restaurant Group depends on third-party cold-chain logistics to deliver fresh ingredients to ~2,300 US locations daily; this scale gives Panda bargaining leverage but few specialized carriers can match its throughput.

In 2024 the US refrigerated trucking vacancy rate hit ~12%, and diesel averaged $3.80/gal—cost swings like these can raise carrier negotiating power and push short-term price or service concessions from Panda.

Ingredient Specialization and Quality Standards

Ingredient specialization for Panda Restaurant Group requires proprietary sauces and USDA-grade produce that meet strict safety and consistency specs, narrowing the supplier pool and raising supplier bargaining power—suppliers that qualify often secure steadier contracts and pricing leverage.

Panda offsets this by signing multi-year strategic partnerships and volume commitments; through 2024 Panda Supply Chain Investments reportedly increased supplier contract durations by ~25%, aligning supplier growth with its 2023–25 expansion.

- Proprietary sauces + USDA-grade produce limit suppliers

- Qualified suppliers gain pricing leverage

- Multi-year contracts reduce disruption

- Supplier contracts up ~25% in duration (2024)

Labor Market Dynamics as a Service Input

Skilled and entry-level labor has increased bargaining power for Panda Restaurant Group, as nationwide restaurant wages rose; by Q4 2025 average hourly pay for food service workers reached about $17.50, up ~12% year-over-year, pushing Panda to raise base pay and expand benefits, which lifted labor cost per store by an estimated 4–6% in 2025.

Higher minimum wages in key states (California, New York) and tight hiring markets forced more signing bonuses and scheduling flexibility, reducing turnover but compressing margins and adding pressure to menu pricing and automation investments.

- Avg food-service pay Q4 2025: ~$17.50/hr

- Estimated per-store labor cost increase 2025: 4–6%

- Turnover reduction vs 2024 after raises: ~8–10%

Panda’s scale cuts input costs 5–12% despite commodity spikes; contracts boost resilience

Panda’s scale (≈2,300 US stores, 2025) gives strong buying leverage—ingredient contracts 5–12% below peers—yet commodity spikes (poultry/soy 2021–22 +10–25%) and specialized suppliers/carriers raise supplier power; multi-year contracts (+25% duration, 2024) and geographic supplier mix (US/Brazil/China) mitigate risk.

| Metric | Value |

|---|---|

| Stores (2025) | ≈2,300 |

| Contract discount | 5–12% |

| Food cost exposure | 18–22% |

| Contract duration ↑ (2024) | +25% |

What is included in the product

Tailored Porter's Five Forces assessment of Panda Restaurant Group, uncovering competitive pressures, supplier and buyer influence, substitution risks, and barriers deterring new entrants to evaluate its strategic positioning and profitability.

A concise Porter's Five Forces snapshot for Panda Restaurant Group—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to guide menu, sourcing, and expansion strategy.

Customers Bargaining Power

Low Switching Costs for Diners

Low switching costs mean diners can choose a different fast-casual brand for their next meal with no penalty, so Panda Express must keep prices competitive and quality steady; NielsenIQ found 2024 U.S. fast-casual repeat visit rates fell 4% year-over-year, raising stakes for retention.

Heightened Price Sensitivity

Consumers in 2025 remain price-conscious after cumulative U.S. inflation rose ~18% from 2020–2024, so Panda faces customers quick to trade down to $5–7 fast-food value meals or cook at home as grocery prices stabilize.

This gives buyers leverage: same-day delivery and third-party apps magnify menu-price comparisons and switching.

Panda must weigh menu price rises against potential traffic loss—Q4 2024 quick-service volume fell ~2–4% industrywide when average check rose 3–5%.

Digital Empowerment and Information Access

Modern diners use apps and social media to see nutrition, ingredient lists, and realtime reviews—72% of US consumers consulted online reviews before dining in 2024, per Pew Research—so Panda Restaurant Group faces instant accountability for consistency across ~2,000 US locations; one viral food-safety or service failure can reach millions and dent same-store sales (SSS) by 1–3% in a quarter, giving customers strong indirect leverage over brand reputation.

Demand for Customization and Variety

Influence of Loyalty Programs

Digital rewards collect customer data in exchange for perks, letting Panda track visits and tailor offers; Panda Restaurant Group reported about 10 million loyalty members in 2024, driving repeat visits and higher AOV (average order value).

That data gives customers leverage to demand personalized deals and exclusives; if offers lag, customers shift—industry churn for weak loyalty apps can exceed 20% annually.

Tech-savvy guests defect to brands with better engagement, so a poor digital experience risks revenue loss and lower lifetime value.

- ~10M loyalty members (2024)

- Higher AOV from targeted offers

- >20% churn risk for weak apps

Buyers Gain Leverage: Inflation, Apps & Loyalty Threaten 20%+ Churn at Panda

Buyers have moderate-to-high leverage: low switching costs, price sensitivity after ~18% cumulative US inflation (2020–24), and real-time price/review comparison via delivery apps; Panda’s ~10M loyalty members (2024) help retention but weak digital offers risk >20% churn. Q4 2024 industry data: +3–5% check → −2–4% volume; niche fast-casual growing 8–12% annually.

| Metric | Value (2024) |

|---|---|

| Cumulative US inflation (2020–24) | ~18% |

| Panda loyalty members | ~10M |

| Check ↑ vs volume ↓ (Q4 2024) | +3–5% → −2–4% |

| App churn risk if poor | >20% annual |

| Niche fast-casual growth | 8–12% yr |

Preview the Actual Deliverable

Panda Restaurant Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Panda Restaurant Group you'll receive immediately after purchase—no placeholders or mockups; the full document is professionally formatted, comprehensive, and ready for download and use the moment you buy.