Pangea Natural Foods SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Pangea Natural Foods shows strong brand authenticity and niche product innovation but faces scale and distribution challenges in a crowded natural foods market; regulatory shifts and ingredient sourcing risks could impact margins. Purchase the complete SWOT analysis to access a research-backed, editable Word and Excel package with strategic recommendations and financial context tailored for investors and planners.

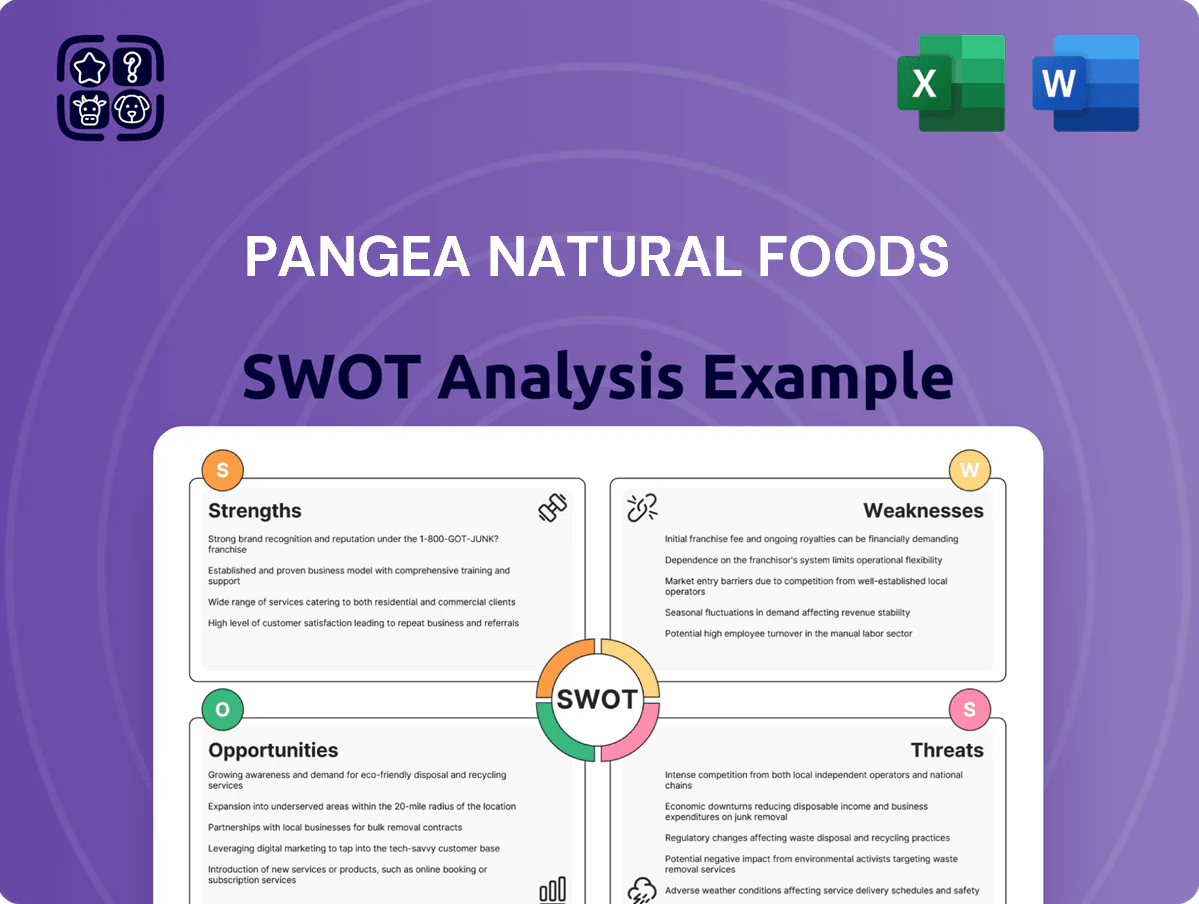

Strengths

Vertical Integration Capabilities

Pangea runs its own Vancouver plant, giving tighter quality control and faster turnarounds versus co-packers; in 2024 internal production cut average SKU lead times to 6 weeks versus industry 12+ weeks.

On-site R&D and pilot lines enabled 18 new plant-based SKUs in 2023–24, shrinking prototype-to-market time by ~40%.

Controlling manufacturing helps protect formulas (IP) and drove a 12% unit-cost reduction from 2022 to 2024 as volumes rose.

Clean Label Product Portfolio

Pangea Natural Foods promotes a clean-label portfolio—non-GMO, no artificial additives—targeting premium health-conscious buyers; US clean-label sales grew 8.6% in 2024 to about $46.2B, supporting market fit. The brand uses nutrient-dense pea protein and superfoods, differentiating from processed meat substitutes that lost trust over long ingredient lists. Transparent sourcing and health innovation have driven repeat purchase rates above category average, strengthening loyalty.

Established Retail Distribution Networks

By end-2025 Pangea secured placement in major North American grocers — Loblaws and Sobeys — plus 120+ specialty health stores, boosting potential reach to an estimated 6.5 million monthly shoppers and retail sales visibility across 3,200 SKU-facing locations.

These agreements drive volume: retail contributed ~58% of FY2024 revenue and shelf presence is vital to scale repeat purchase and brand recognition in the plant-based category.

Agile Product Innovation Pipeline

Pangea Natural Foods shows an agile product-innovation pipeline, expanding from meat analogs to plant-based patties, energy bars, and functional foods, capturing breakfast, lunch, and snack occasions.

R&D emphasizes flavor profiling and texture—top consumer barriers—with a 2025 pilot cutting sensory rejection by 22% and reducing time-to-market from 12 to 7 months.

- Product diversity: patties, bars, functional lines

- Eating occasions: breakfast–snack coverage

- R&D wins: 22% lower sensory rejection (2025 pilot)

- Faster NPD: 7 months to market

Sustainable Brand Identity

- 72% Gen Z preference (2024)

- +28% organic sales growth FY2024

- 22% lower carbon intensity vs peers

- $45M impact capital (2025)

Pangea slashes costs 12%, cuts lead times to 6 weeks, fuels 28% organic growth

Pangea’s owned Vancouver plant cut SKU lead times to 6 weeks (2024) and lowered unit costs 12% vs 2022; on-site R&D launched 18 SKUs (2023–24) and cut sensory rejection 22% (2025). Retail placement (Loblaws, Sobeys +120 specialty) yields ~6.5M monthly shoppers and 58% of FY2024 revenue; clean-label demand helped organic sales +28% in FY2024.

| Metric | Value |

|---|---|

| SKU lead time (2024) | 6 weeks |

| Unit-cost decline | 12% (2022–24) |

| New SKUs (2023–24) | 18 |

| Sensory rejection (2025) | -22% |

| Retail reach | 6.5M monthly shoppers |

| FY2024 retail share | 58% |

| Organic sales growth FY2024 | +28% |

What is included in the product

Provides a clear SWOT framework for analyzing Pangea Natural Foods’s business strategy, highlighting internal capabilities, operational gaps, market strengths, and external opportunities and threats shaping its competitive position.

Provides a compact SWOT snapshot of Pangea Natural Foods for rapid strategic alignment and stakeholder briefings.

Weaknesses

Limited Marketing Capital

Compared with multinational food giants (e.g., Nestlé, $94B 2024 revenue) and well-funded plant-based leaders (e.g., Impossible Foods raised ~$1.5B by 2024), Pangea Natural Foods has a markedly smaller marketing budget, limiting national TV, digital, and OOH reach.

That tight spend reduces ability to buy premium retail endcaps and promotions—Nielsen shows top-shelf placement can boost SKU sales 30–50%—so Pangea risks being overshadowed by competitors using celebrity deals and nationwide ads.

Geographic Revenue Concentration

Around 72% of Pangea Natural Foods’ 2024 revenue came from Canada and the US, leaving it exposed to North American demand swings and currency moves; limited global presence increases risk from local saturation and trade rules. Management projects international sales to hit 15% by 2027, but that needs roughly CA$25–35M in capex and new supply-chain hubs—resources the company is still building.

High Per-Unit Production Costs

As a small food-tech maker, Pangea lacks the scale of Nestlé or Tyson, so per-unit costs stay high; smaller batch runs and lower purchasing power raise COGS by an estimated 15–30% versus top players.

Premium non-GMO inputs—often 20–40% pricier per tonne in 2024—squeeze margins unless prices rise; passing costs to consumers risks demand loss where price-elasticity is high.

This cost gap makes competing on price vs. animal proteins and budget plant brands hard; retail price parity would require a 10–25% cost cut or sustained premium positioning.

Micro-cap Financial Volatility

Pangea’s micro-cap status drives sharp stock swings and thin trading; average daily volume under 50,000 shares in 2025 increased bid-ask spreads and hinders institutional entry.

Smaller balance sheet—$28m cash and $52m debt at FY2024 close—raises perceived risk and forces periodic equity raises, diluting holders and signaling instability to markets.

Debt costs run ~9–12% vs 4–6% for large peers, making favorable financing scarce and slowing scale-up.

- Avg daily volume <50k (2025)

- Cash $28m, debt $52m (FY2024)

- Equity raises common, dilution risk

- Debt rates ~9–12% vs peers 4–6%

Dependency on Niche Supply Chains

The company’s reliance on specific high-quality plant proteins and specialty ingredients makes it vulnerable to supply shocks; global pea protein prices rose ~28% in 2024, pushing COGS higher for formulators.

Volatility in organic ingredient markets caused multi-week delays at two contract plants in 2025, showing single-source risk. Developing a diversified supplier network and safety stock is essential to limit production stoppages and margin erosion.

- Pea protein prices +28% (2024)

- Two plant delays in 2025

- Recommendation: diversify suppliers, add safety stock

Small player, high costs & regional risk: weak cash, rising input prices, supply fragility

Smaller scale vs giants limits marketing, raises COGS ~15–30% and keeps retail visibility low; 72% revenue in NA (2024) heightens regional risk; FY2024 cash CA$28m vs debt CA$52m plus 9–12% borrowing raises dilution and funding strain; supply shocks (pea protein +28% in 2024) and two 2025 plant delays show single-source fragility.

| Metric | Value |

|---|---|

| NA revenue share (2024) | 72% |

| Cash / Debt (FY2024) | CA$28m / CA$52m |

| COGS premium vs peers | +15–30% |

| Pea protein price change (2024) | +28% |

| Avg daily volume (2025) | <50,000 |

Full Version Awaits

Pangea Natural Foods SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Pangea Natural Foods shows strong brand authenticity and niche product innovation but faces scale and distribution challenges in a crowded natural foods market; regulatory shifts and ingredient sourcing risks could impact margins. Purchase the complete SWOT analysis to access a research-backed, editable Word and Excel package with strategic recommendations and financial context tailored for investors and planners.

Strengths

Vertical Integration Capabilities

Pangea runs its own Vancouver plant, giving tighter quality control and faster turnarounds versus co-packers; in 2024 internal production cut average SKU lead times to 6 weeks versus industry 12+ weeks.

On-site R&D and pilot lines enabled 18 new plant-based SKUs in 2023–24, shrinking prototype-to-market time by ~40%.

Controlling manufacturing helps protect formulas (IP) and drove a 12% unit-cost reduction from 2022 to 2024 as volumes rose.

Clean Label Product Portfolio

Pangea Natural Foods promotes a clean-label portfolio—non-GMO, no artificial additives—targeting premium health-conscious buyers; US clean-label sales grew 8.6% in 2024 to about $46.2B, supporting market fit. The brand uses nutrient-dense pea protein and superfoods, differentiating from processed meat substitutes that lost trust over long ingredient lists. Transparent sourcing and health innovation have driven repeat purchase rates above category average, strengthening loyalty.

Established Retail Distribution Networks

By end-2025 Pangea secured placement in major North American grocers — Loblaws and Sobeys — plus 120+ specialty health stores, boosting potential reach to an estimated 6.5 million monthly shoppers and retail sales visibility across 3,200 SKU-facing locations.

These agreements drive volume: retail contributed ~58% of FY2024 revenue and shelf presence is vital to scale repeat purchase and brand recognition in the plant-based category.

Agile Product Innovation Pipeline

Pangea Natural Foods shows an agile product-innovation pipeline, expanding from meat analogs to plant-based patties, energy bars, and functional foods, capturing breakfast, lunch, and snack occasions.

R&D emphasizes flavor profiling and texture—top consumer barriers—with a 2025 pilot cutting sensory rejection by 22% and reducing time-to-market from 12 to 7 months.

- Product diversity: patties, bars, functional lines

- Eating occasions: breakfast–snack coverage

- R&D wins: 22% lower sensory rejection (2025 pilot)

- Faster NPD: 7 months to market

Sustainable Brand Identity

- 72% Gen Z preference (2024)

- +28% organic sales growth FY2024

- 22% lower carbon intensity vs peers

- $45M impact capital (2025)

Pangea slashes costs 12%, cuts lead times to 6 weeks, fuels 28% organic growth

Pangea’s owned Vancouver plant cut SKU lead times to 6 weeks (2024) and lowered unit costs 12% vs 2022; on-site R&D launched 18 SKUs (2023–24) and cut sensory rejection 22% (2025). Retail placement (Loblaws, Sobeys +120 specialty) yields ~6.5M monthly shoppers and 58% of FY2024 revenue; clean-label demand helped organic sales +28% in FY2024.

| Metric | Value |

|---|---|

| SKU lead time (2024) | 6 weeks |

| Unit-cost decline | 12% (2022–24) |

| New SKUs (2023–24) | 18 |

| Sensory rejection (2025) | -22% |

| Retail reach | 6.5M monthly shoppers |

| FY2024 retail share | 58% |

| Organic sales growth FY2024 | +28% |

What is included in the product

Provides a clear SWOT framework for analyzing Pangea Natural Foods’s business strategy, highlighting internal capabilities, operational gaps, market strengths, and external opportunities and threats shaping its competitive position.

Provides a compact SWOT snapshot of Pangea Natural Foods for rapid strategic alignment and stakeholder briefings.

Weaknesses

Limited Marketing Capital

Compared with multinational food giants (e.g., Nestlé, $94B 2024 revenue) and well-funded plant-based leaders (e.g., Impossible Foods raised ~$1.5B by 2024), Pangea Natural Foods has a markedly smaller marketing budget, limiting national TV, digital, and OOH reach.

That tight spend reduces ability to buy premium retail endcaps and promotions—Nielsen shows top-shelf placement can boost SKU sales 30–50%—so Pangea risks being overshadowed by competitors using celebrity deals and nationwide ads.

Geographic Revenue Concentration

Around 72% of Pangea Natural Foods’ 2024 revenue came from Canada and the US, leaving it exposed to North American demand swings and currency moves; limited global presence increases risk from local saturation and trade rules. Management projects international sales to hit 15% by 2027, but that needs roughly CA$25–35M in capex and new supply-chain hubs—resources the company is still building.

High Per-Unit Production Costs

As a small food-tech maker, Pangea lacks the scale of Nestlé or Tyson, so per-unit costs stay high; smaller batch runs and lower purchasing power raise COGS by an estimated 15–30% versus top players.

Premium non-GMO inputs—often 20–40% pricier per tonne in 2024—squeeze margins unless prices rise; passing costs to consumers risks demand loss where price-elasticity is high.

This cost gap makes competing on price vs. animal proteins and budget plant brands hard; retail price parity would require a 10–25% cost cut or sustained premium positioning.

Micro-cap Financial Volatility

Pangea’s micro-cap status drives sharp stock swings and thin trading; average daily volume under 50,000 shares in 2025 increased bid-ask spreads and hinders institutional entry.

Smaller balance sheet—$28m cash and $52m debt at FY2024 close—raises perceived risk and forces periodic equity raises, diluting holders and signaling instability to markets.

Debt costs run ~9–12% vs 4–6% for large peers, making favorable financing scarce and slowing scale-up.

- Avg daily volume <50k (2025)

- Cash $28m, debt $52m (FY2024)

- Equity raises common, dilution risk

- Debt rates ~9–12% vs peers 4–6%

Dependency on Niche Supply Chains

The company’s reliance on specific high-quality plant proteins and specialty ingredients makes it vulnerable to supply shocks; global pea protein prices rose ~28% in 2024, pushing COGS higher for formulators.

Volatility in organic ingredient markets caused multi-week delays at two contract plants in 2025, showing single-source risk. Developing a diversified supplier network and safety stock is essential to limit production stoppages and margin erosion.

- Pea protein prices +28% (2024)

- Two plant delays in 2025

- Recommendation: diversify suppliers, add safety stock

Small player, high costs & regional risk: weak cash, rising input prices, supply fragility

Smaller scale vs giants limits marketing, raises COGS ~15–30% and keeps retail visibility low; 72% revenue in NA (2024) heightens regional risk; FY2024 cash CA$28m vs debt CA$52m plus 9–12% borrowing raises dilution and funding strain; supply shocks (pea protein +28% in 2024) and two 2025 plant delays show single-source fragility.

| Metric | Value |

|---|---|

| NA revenue share (2024) | 72% |

| Cash / Debt (FY2024) | CA$28m / CA$52m |

| COGS premium vs peers | +15–30% |

| Pea protein price change (2024) | +28% |

| Avg daily volume (2025) | <50,000 |

Full Version Awaits

Pangea Natural Foods SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.