Parkland PESTLE Analysis

Skip the Research. Get the Strategy.

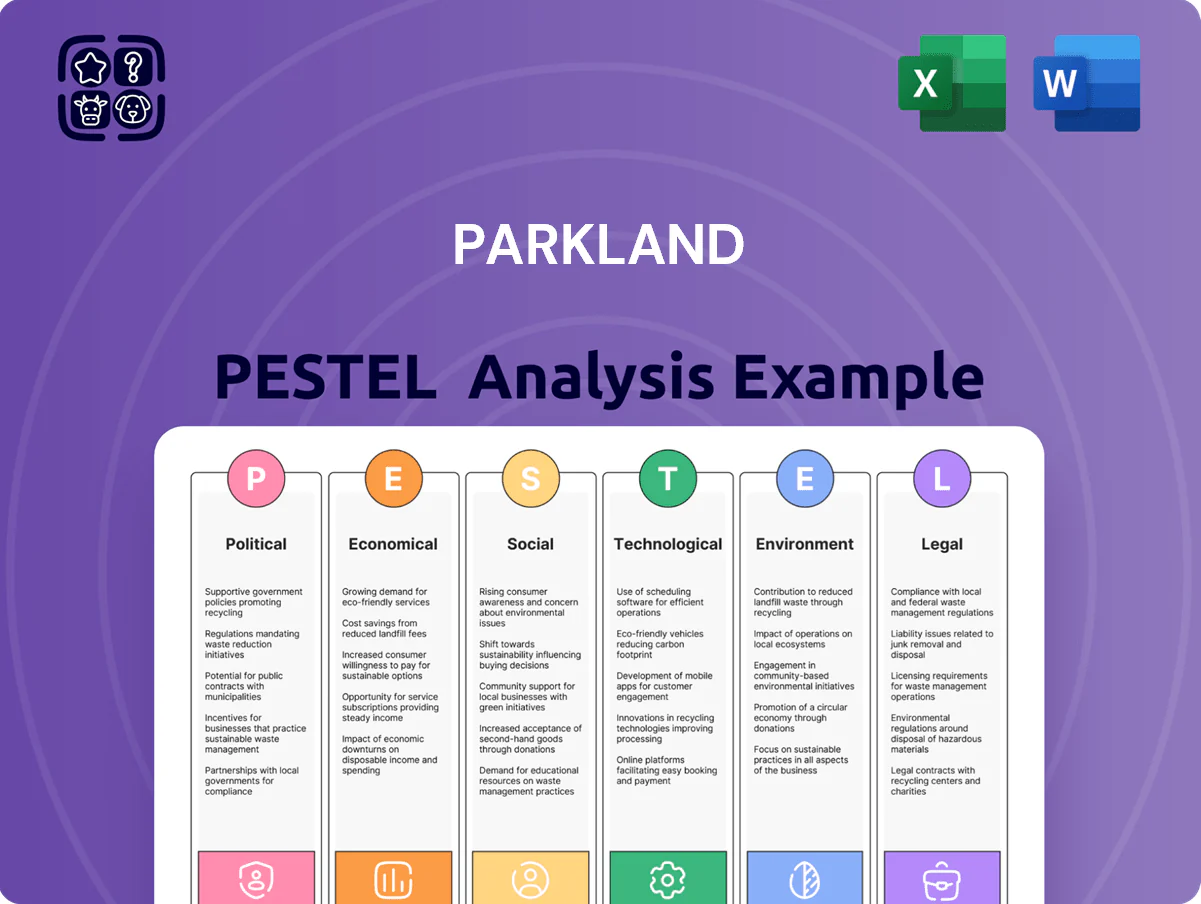

Gain a strategic advantage with our Parkland PESTLE Analysis—concise, evidence-based insights into the political, economic, social, technological, legal, and environmental forces shaping the company’s outlook; buy the full report to access actionable intelligence, ready-made charts, and editable formats that save time and sharpen investment or strategic decisions.

Political factors

Carbon Pricing and Federal Mandates

As of late 2025 the federal carbon tax in Canada reached CAD 80/tonne, adding roughly CAD 0.09–0.15/L to gasoline costs and materially affecting Parkland’s gross margins and retail pricing strategies.

Escalating carbon pricing compels Parkland to accelerate investment in lower‑carbon fuels and renewables to protect market share as fuel cost pass‑through becomes constrained.

Parkland must reconcile Canadian mandates with varied US state programs and Caribbean jurisdictions, where carbon pricing and compliance costs differ significantly and affect cross‑border pricing and supply decisions.

Geopolitical Trade Relations

Fluctuating trade ties between North America and oil-exporters have altered Parkland’s supply stability; Canada-US-Mexico policy shifts and 2024 LNG/condensate flows meant imported refined product volumes swung ~6% YoY, pressuring margins. Ongoing Middle East and Eastern Europe tensions kept Brent volatile—2024 average ~US$85/bbl vs US$79/bbl in 2023—raising import costs. Parkland actively monitors routes and holds strategic inventories to limit customer price shocks.

Caribbean Energy Regulatory Shifts

In the Caribbean and South America, governments are prioritizing energy security and fuel-infrastructure upgrades, with regional energy investment pledges reaching about US 2.1 billion in 2024; Parkland faces varying state intervention and tariff rules that can compress regional fuel margins of 3–7% reported in FY2024.

Strong diplomatic relations and local partnerships are essential for Parkland to manage regulatory shifts, secure long-term supply contracts, and protect revenues across over 20 island and coastal markets where regulatory changes accelerated in 2023–2025.

Government Subsidies for Green Energy

Government subsidies for EV infrastructure and renewable fuels create both risk and opportunity for Parkland as public policy shifts; Canada invested C$1.5B in EV charging and hydrogen supports in 2024–25, enabling grants that lower payback on capital-heavy projects.

Parkland uses federal and provincial grants to speed deployment of its ultra-fast charging across major corridors, targeting 200+ sites by 2026 and reducing capex per site by an estimated 25%.

These political incentives de-risk Parkland’s move from petroleum to a multi-energy retail model, improving project IRRs and supporting blended fuel margins during transition.

- Canada C$1.5B EV/hydrogen funding (2024–25)

- Parkland target: 200+ ultra-fast chargers by 2026

- Estimated 25% capex reduction per site via grants

- Improves IRR and lowers transition risk

Labor and Minimum Wage Legislation

Political pushes for higher minimum wages in Canada and the US have raised labor costs for Parkland, which operates over 2,000 retail/convenience sites; a 2024 average provincial minimum-wage rise of 6–8% increased regional payroll burdens by an estimated mid-single-digit percentage of operating expenses.

Rising employment standards compel Parkland to optimize staffing and invest in automation—retail tech investment climbed toward 3–5% of capex in recent company disclosures—to preserve margins and service levels.

Active policy engagement enables Parkland to forecast wage trajectories, mitigating shocks from expected further increases (several provinces signaling $15+ targets) and smoothing human-capital cost pass-throughs.

- ~2,000 retail sites exposed to regional wage hikes

- 2024 provincial wage increases averaged 6–8%

- Retail automation capex ~3–5% of total capex

- Policy outreach used to anticipate $15+ minimum-wage targets

Rising costs, EV push and automation: C$80 carbon tax, higher wages, $1.5B EV/H2 fund

Federal carbon tax C$80/t (late 2025) adds ~C$0.09–0.15/L; 2024 Brent avg US$85/bbl vs US$79 (2023); Canada C$1.5B EV/hydrogen (2024–25); Parkland target 200+ chargers by 2026; ~2,000 sites exposed to 2024 wage rises (6–8%); retail automation capex ~3–5%.

| Metric | Value |

|---|---|

| Carbon tax | C$80/t (late 2025) |

| Brent 2024 | US$85/bbl |

| EV/hydrogen funding | C$1.5B (2024–25) |

| Charger target | 200+ by 2026 |

| Retail sites | ~2,000 |

| Wage rise 2024 | 6–8% |

| Automation capex | 3–5% of capex |

What is included in the product

Explores how external macro-environmental factors uniquely affect Parkland across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise Parkland PESTLE summary formatted for quick reference in meetings or slide decks, visually segmented by category and editable for region- or business-specific notes to streamline team alignment and strategic planning.

Economic factors

Global Crude Oil Price Volatility

Global crude volatility is Parkland’s primary economic driver, with Brent swinging 35% in 2024–2025 and average wholesale inventory cost up 18% YoY, directly compressing margins.

Late-2025 market swings prompted expanded hedging; management reports hedges covering ~60% of refined product exposure, reducing EBITDA volatility by an estimated 25%.

Parkland’s integrated supply model—retail, wholesale and terminals—helped capture downstream spreads, contributing to a 2025 adjusted cash flow improvement of roughly CAD 120 million versus 2024.

Inflation and Consumer Spending Power

Interest Rate Environment

At end-2025, with global policy rates averaging near 4.5% and Canada’s overnight rate at 5.0%, Parkland faces higher cost of debt that raises annual interest expense on CAD-denominated borrowings by several percentage points, tightening free cash flow and requiring disciplined capital allocation to service ~US$1.5bn net debt; a stabilizing rate trajectory could allow renewed acquisition activity after pausing large deals in 2024–25.

Foreign Exchange Fluctuations

With major operations in Canada, the US and the Caribbean, Parkland faces FX risk—CAD/USD swings altered 2024 reported adjusted EBITDA by an estimated CAD 45–60 million, per management sensitivity disclosures.

Stronger CAD reduces translated USD revenues and lowers USD-denominated fuel import costs; a 5% CAD appreciation in 2024 cut reported US segment earnings by roughly CAD 30 million.

Parkland uses forwards, swaps and natural hedges; as of Q3 2025 management reported about USD 600 million of hedges to stabilize cash flows and earnings.

- Exposure: CAD/USD driven by US operations and Caribbean imports

- Impact: ~CAD 45–60m EBITDA sensitivity in 2024

- Mitigation: ~USD 600m hedged via forwards/swaps (Q3 2025)

Labor Market Tightness

- Low sector unemployment: retail ~4.0%, logistics ~3.5% (2025)

- Wage inflation: ~6–8% YoY for frontline roles

- Focus: automation, route optimization, digital retail tools

Hedging cushions crude swings; retail margins and CAD cashflow offset rising costs

Crude volatility and higher inventory costs compressed margins (Brent ±35% 2024–25; wholesale cost +18% YoY); hedges (~60% coverage; ~USD600m) trimmed EBITDA volatility ~25%. Retail convenience (20% margins) aided cash flow (+CAD120m in 2025) despite CPI 3–4% and wage inflation 6–8%; net debt ~US$1.5bn; FX moved EBITDA ~CAD45–60m (2024).

| Metric | Value (2024–25) |

|---|---|

| Brent swing | ±35% |

| Wholesale cost change | +18% YoY |

| Hedge coverage | ~60% / USD600m |

| Retail margin | ~20% |

| Adj. CF improvement | +CAD120m |

| Net debt | ~US$1.5bn |

| FX EBITDA impact | CAD45–60m |

| Wage inflation | 6–8% |

Full Version Awaits

Parkland PESTLE Analysis

The preview shown here is the exact Parkland PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic advantage with our Parkland PESTLE Analysis—concise, evidence-based insights into the political, economic, social, technological, legal, and environmental forces shaping the company’s outlook; buy the full report to access actionable intelligence, ready-made charts, and editable formats that save time and sharpen investment or strategic decisions.

Political factors

Carbon Pricing and Federal Mandates

As of late 2025 the federal carbon tax in Canada reached CAD 80/tonne, adding roughly CAD 0.09–0.15/L to gasoline costs and materially affecting Parkland’s gross margins and retail pricing strategies.

Escalating carbon pricing compels Parkland to accelerate investment in lower‑carbon fuels and renewables to protect market share as fuel cost pass‑through becomes constrained.

Parkland must reconcile Canadian mandates with varied US state programs and Caribbean jurisdictions, where carbon pricing and compliance costs differ significantly and affect cross‑border pricing and supply decisions.

Geopolitical Trade Relations

Fluctuating trade ties between North America and oil-exporters have altered Parkland’s supply stability; Canada-US-Mexico policy shifts and 2024 LNG/condensate flows meant imported refined product volumes swung ~6% YoY, pressuring margins. Ongoing Middle East and Eastern Europe tensions kept Brent volatile—2024 average ~US$85/bbl vs US$79/bbl in 2023—raising import costs. Parkland actively monitors routes and holds strategic inventories to limit customer price shocks.

Caribbean Energy Regulatory Shifts

In the Caribbean and South America, governments are prioritizing energy security and fuel-infrastructure upgrades, with regional energy investment pledges reaching about US 2.1 billion in 2024; Parkland faces varying state intervention and tariff rules that can compress regional fuel margins of 3–7% reported in FY2024.

Strong diplomatic relations and local partnerships are essential for Parkland to manage regulatory shifts, secure long-term supply contracts, and protect revenues across over 20 island and coastal markets where regulatory changes accelerated in 2023–2025.

Government Subsidies for Green Energy

Government subsidies for EV infrastructure and renewable fuels create both risk and opportunity for Parkland as public policy shifts; Canada invested C$1.5B in EV charging and hydrogen supports in 2024–25, enabling grants that lower payback on capital-heavy projects.

Parkland uses federal and provincial grants to speed deployment of its ultra-fast charging across major corridors, targeting 200+ sites by 2026 and reducing capex per site by an estimated 25%.

These political incentives de-risk Parkland’s move from petroleum to a multi-energy retail model, improving project IRRs and supporting blended fuel margins during transition.

- Canada C$1.5B EV/hydrogen funding (2024–25)

- Parkland target: 200+ ultra-fast chargers by 2026

- Estimated 25% capex reduction per site via grants

- Improves IRR and lowers transition risk

Labor and Minimum Wage Legislation

Political pushes for higher minimum wages in Canada and the US have raised labor costs for Parkland, which operates over 2,000 retail/convenience sites; a 2024 average provincial minimum-wage rise of 6–8% increased regional payroll burdens by an estimated mid-single-digit percentage of operating expenses.

Rising employment standards compel Parkland to optimize staffing and invest in automation—retail tech investment climbed toward 3–5% of capex in recent company disclosures—to preserve margins and service levels.

Active policy engagement enables Parkland to forecast wage trajectories, mitigating shocks from expected further increases (several provinces signaling $15+ targets) and smoothing human-capital cost pass-throughs.

- ~2,000 retail sites exposed to regional wage hikes

- 2024 provincial wage increases averaged 6–8%

- Retail automation capex ~3–5% of total capex

- Policy outreach used to anticipate $15+ minimum-wage targets

Rising costs, EV push and automation: C$80 carbon tax, higher wages, $1.5B EV/H2 fund

Federal carbon tax C$80/t (late 2025) adds ~C$0.09–0.15/L; 2024 Brent avg US$85/bbl vs US$79 (2023); Canada C$1.5B EV/hydrogen (2024–25); Parkland target 200+ chargers by 2026; ~2,000 sites exposed to 2024 wage rises (6–8%); retail automation capex ~3–5%.

| Metric | Value |

|---|---|

| Carbon tax | C$80/t (late 2025) |

| Brent 2024 | US$85/bbl |

| EV/hydrogen funding | C$1.5B (2024–25) |

| Charger target | 200+ by 2026 |

| Retail sites | ~2,000 |

| Wage rise 2024 | 6–8% |

| Automation capex | 3–5% of capex |

What is included in the product

Explores how external macro-environmental factors uniquely affect Parkland across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise Parkland PESTLE summary formatted for quick reference in meetings or slide decks, visually segmented by category and editable for region- or business-specific notes to streamline team alignment and strategic planning.

Economic factors

Global Crude Oil Price Volatility

Global crude volatility is Parkland’s primary economic driver, with Brent swinging 35% in 2024–2025 and average wholesale inventory cost up 18% YoY, directly compressing margins.

Late-2025 market swings prompted expanded hedging; management reports hedges covering ~60% of refined product exposure, reducing EBITDA volatility by an estimated 25%.

Parkland’s integrated supply model—retail, wholesale and terminals—helped capture downstream spreads, contributing to a 2025 adjusted cash flow improvement of roughly CAD 120 million versus 2024.

Inflation and Consumer Spending Power

Interest Rate Environment

At end-2025, with global policy rates averaging near 4.5% and Canada’s overnight rate at 5.0%, Parkland faces higher cost of debt that raises annual interest expense on CAD-denominated borrowings by several percentage points, tightening free cash flow and requiring disciplined capital allocation to service ~US$1.5bn net debt; a stabilizing rate trajectory could allow renewed acquisition activity after pausing large deals in 2024–25.

Foreign Exchange Fluctuations

With major operations in Canada, the US and the Caribbean, Parkland faces FX risk—CAD/USD swings altered 2024 reported adjusted EBITDA by an estimated CAD 45–60 million, per management sensitivity disclosures.

Stronger CAD reduces translated USD revenues and lowers USD-denominated fuel import costs; a 5% CAD appreciation in 2024 cut reported US segment earnings by roughly CAD 30 million.

Parkland uses forwards, swaps and natural hedges; as of Q3 2025 management reported about USD 600 million of hedges to stabilize cash flows and earnings.

- Exposure: CAD/USD driven by US operations and Caribbean imports

- Impact: ~CAD 45–60m EBITDA sensitivity in 2024

- Mitigation: ~USD 600m hedged via forwards/swaps (Q3 2025)

Labor Market Tightness

- Low sector unemployment: retail ~4.0%, logistics ~3.5% (2025)

- Wage inflation: ~6–8% YoY for frontline roles

- Focus: automation, route optimization, digital retail tools

Hedging cushions crude swings; retail margins and CAD cashflow offset rising costs

Crude volatility and higher inventory costs compressed margins (Brent ±35% 2024–25; wholesale cost +18% YoY); hedges (~60% coverage; ~USD600m) trimmed EBITDA volatility ~25%. Retail convenience (20% margins) aided cash flow (+CAD120m in 2025) despite CPI 3–4% and wage inflation 6–8%; net debt ~US$1.5bn; FX moved EBITDA ~CAD45–60m (2024).

| Metric | Value (2024–25) |

|---|---|

| Brent swing | ±35% |

| Wholesale cost change | +18% YoY |

| Hedge coverage | ~60% / USD600m |

| Retail margin | ~20% |

| Adj. CF improvement | +CAD120m |

| Net debt | ~US$1.5bn |

| FX EBITDA impact | CAD45–60m |

| Wage inflation | 6–8% |

Full Version Awaits

Parkland PESTLE Analysis

The preview shown here is the exact Parkland PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.