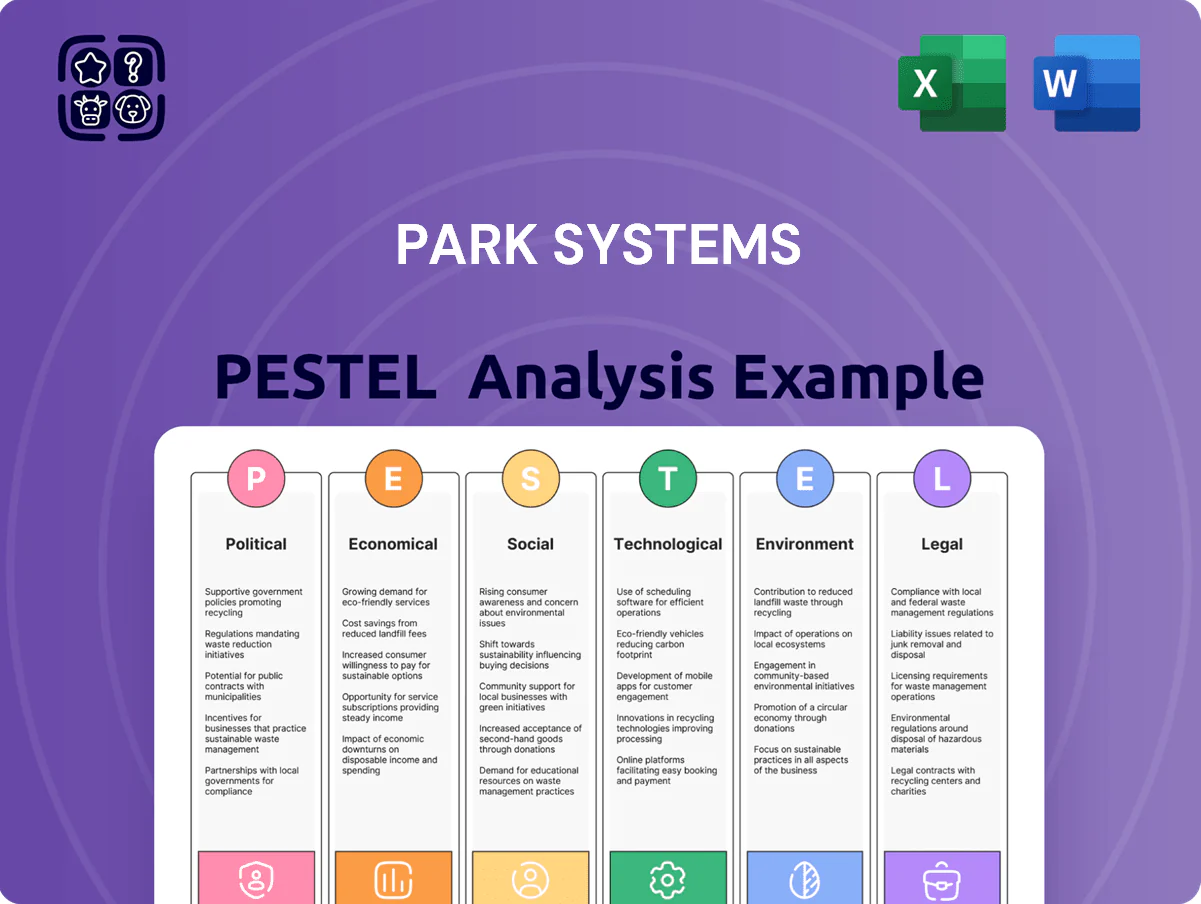

Park Systems PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our targeted PESTLE Analysis for Park Systems—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s prospects; ideal for investors, consultants, and executives. Buy the full report to access a complete, editable breakdown that powers smarter decisions and competitive advantage—download instantly.

Political factors

Geopolitical Trade Restrictions and Export Controls

The US-China tech rivalry is reshaping export controls for high-end semiconductor equipment through 2025, with US restrictions targeting over 300 Chinese entities and contributing to a 15% decline in cross-border equipment shipments to China in 2023–24; Park Systems must manage complex licensing to serve Asian hubs like Taiwan and South Korea, which accounted for roughly 60% of global fab equipment demand in 2024. Changes in trade alliances and export lists could open emerging markets—Southeast Asia capex grew ~22% in 2024—or constrain access to critical components, risking supply-chain cost increases and margin pressure for Park Systems.

Government Subsidies for Semiconductor Independence

National initiatives like the U.S. CHIPS and Science Act (US$280B total package including US$52B for semiconductor incentives), EU Chips Act (€43B mobilized) and South Korea’s KRW 510T plan have directed billions into domestic fabs, boosting demand for Park Systems’ metrology tools as new fabs and R&D centers are built.

Inter-Korean Relations and Regional Stability

As a South Korea–headquartered firm, Park Systems is highly sensitive to Korean Peninsula tensions; in 2025 foreign direct investment into South Korea fell 8.1% year-over-year to $13.4bn amid regional uncertainty, which can depress investor confidence for tech exporters.

Escalation risks threaten supply-chain logistics—South Korea handled $1.1tn in goods in 2024—so disruptions could materially raise component lead times and costs for Park Systems’ wafer-probe and AFM production.

Physical security of primary manufacturing hubs in Gyeonggi and Ulsan could force contingency spending; defense and risk insurance premiums for Korean manufacturers rose ~12% in 2024.

Ongoing government diplomatic efforts, including 2024–25 trilateral dialogues with the US and Japan, are critical inputs to Park Systems’ long-term operational planning and risk-management models.

Global Research and Development Funding Policies

Public investment in nanotech and materials science—estimated at $9.6 billion globally in 2024—boosts purchasing by universities and national labs, directly lifting demand for Park Systems’ AFM instruments.

When governments shift budgets toward quantum computing or personalized medicine (global R&D in quantum reached $3.2B in 2024), specialized AFM needs rise, creating cyclical procurement opportunities.

Park Systems depends on these policy-driven funding cycles—public grant awards to research institutions grew ~6% YoY in 2024—to maintain market leadership in scientific AFMs.

- Global nanotech R&D public funding: $9.6B (2024)

- Quantum R&D public spend: $3.2B (2024)

- Research grant growth to institutions: +6% YoY (2024)

Bilateral Trade Agreements and Tariff Structures

The 2023 RCEP and 2022 India-EU negotiations lowering average tariffs by 1–3% improve Park Systems’ export competitiveness and reduce input costs for components, potentially boosting gross margins by 0.5–1.5 percentage points in target markets.

Preferential tariff treatment entering India or ASEAN could increase net revenue per unit; conversely, 2024 US-China tariff retaliations (up to 25% on some components) may force price hikes or shift assembly to Vietnam or Korea to preserve margins.

- RCEP/India-EU tariff cuts: −1–3% average

- Potential margin lift: +0.5–1.5 pp

- Retaliatory tariffs: up to 25% on components (2024)

- Mitigation: relocate assembly to Vietnam/Korea

Export Controls Cut China Shipments 15% as CHIPS Subsidies Boost Metrology Demand

Geopolitical export controls and US-China tech rivalry (15% drop in equipment shipments to China 2023–24) force Park Systems to manage complex licensing while benefiting from domestic fab incentives (US$52B CHIPS, €43B EU, KRW510T SK) that lift metrology demand; regional tensions cut FDI (South Korea FDI −8.1% to $13.4B in 2025) and raise insurance costs (+12% 2024), while RCEP/India‑EU tariff cuts (−1–3%) may improve margins (+0.5–1.5 pp).

| Metric | Value (2024–25) |

|---|---|

| Equip shipments to China | −15% |

| US CHIPS incentives | US$52B |

| EU Chips Act | €43B |

| SK fab plan | KRW 510T |

| SK FDI | $13.4B (−8.1%) |

| Insurance costs | +12% |

| Tariff cuts (RCEP/India‑EU) | −1–3% |

| Potential margin lift | +0.5–1.5 pp |

What is included in the product

Explores how macro-environmental factors uniquely affect Park Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking analysis to identify risks and opportunities for executives, investors, and strategists.

Condenses Park Systems’ PESTLE into a concise, shareable brief that highlights regulatory, technological, and market risks for quick alignment in meetings or slide decks.

Economic factors

Semiconductor Industry Capital Expenditure Cycles

The financial health of Park Systems is tightly linked to capex plans of major logic and memory fabs; TSMC, Samsung and SK Hynix collectively forecast fab equipment spending of about $120–140 billion for 2024–2025, shaping demand for Park’s AFM metrology tools.

As the industry shifts to sub-2nm nodes and advanced packaging by late 2025, high-precision metrology becomes non-discretionary for yield control, increasing addressable market value for Park’s tools by an estimated mid-teens CAGR.

However, cyclical downturns in consumer electronics—global smartphone shipments fell ~6% in 2024—can trigger temporary capex delays, causing short-term revenue variability for Park Systems.

Global Inflationary Pressures and Operational Costs

Persistent mid-2020s inflation—global CPI averaging about 4–5% in 2024–25—has pushed prices for piezoelectric scanners, lasers and RF components up 8–12% and raised skilled labor costs, pressuring AFM gross margins. Park Systems must offset these input cost increases while keeping competitive pricing to sustain ~25–30% operating margins reported in recent years. Rigorous supply-chain management, dual sourcing and procurement hedges for key inputs and freight helped peer firms cut cost volatility by ~30% in 2024. These measures are essential to protect EBITDA against commodity and logistics swings.

Currency Exchange Rate Fluctuations

With roughly 60% of 2024 revenue from overseas markets, Park Systems faces material FX exposure as the KRW strengthened about 4.8% vs USD and 2.3% vs EUR in 2024, which can raise local-currency prices and erode price competitiveness abroad.

A stronger won risks shifting orders to competitors operating in weaker-currency jurisdictions, particularly for price-sensitive semiconductor and materials clients.

Park Systems uses forward contracts, FX options and natural hedges; disclosed hedging reduced 2024 FX-related earnings volatility, limiting translation losses to under 1.5% of revenue.

Growth of the Nanotechnology Market

Growth of the global nanotechnology market to USD 154.7 billion by 2026 (CAGR ~16% from 2021–26) and expanded use in energy storage and biotech diversify Park Systems revenue beyond semiconductors, supporting sales of both high-end and routine AFMs.

Rising venture capital—over USD 8.5 billion invested in nanotech startups in 2024—feeds demand for entry and mid-range AFM systems as new firms commercialize molecular engineering solutions.

Structural shift to molecular-level engineering ensures sustained long-term demand for high-resolution surface characterization tools, underpinning recurring service and upgrade revenue streams for Park Systems.

- Market size 2026: USD 154.7B; CAGR ~16%

- VC funding 2024: >USD 8.5B into nanotech startups

- Demand drivers: energy storage, biotech, molecular engineering

- Revenue impact: diversification, recurring service/upgrades

Interest Rate Environments and Financing Costs

The current high-rate environment—US Fed funds ~5.25–5.50% in 2024 and average corporate loan spreads up ~150–200 bps—raises financing costs, constraining startups and smaller R&D labs from purchasing expensive AFM equipment, prolonging sales cycles.

Higher borrowing costs push customers toward leasing, pay-per-use, or service-led models; Park Systems should expand flexible financing, subscription pricing, and vendor leasing partnerships to capture constrained demand.

- Fed funds ~5.25–5.50% (2024)

- Loan spreads +150–200 bps, slowing CAPEX

- Shift to leasing/service models increases recurring revenue

- Flexible financing and subscription offerings critical for sales

Park Systems rides $120–140B fab capex into booming $154.7B nanotech market

Park Systems’ 2024–25 demand tied to $120–140B fab capex; nanotech market to $154.7B by 2026 (CAGR ~16%); 60% revenue offshore with KRW +4.8% vs USD in 2024; input cost inflation +8–12% pressured ~25–30% OPM; Fed funds ~5.25–5.50% (2024) raised borrowing costs, shifting customers to leasing/subscription.

| Metric | Value |

|---|---|

| Fab capex (2024–25) | $120–140B |

| Nanotech market (2026) | $154.7B |

| Revenue offshore (2024) | ~60% |

| KRW vs USD (2024) | +4.8% |

| Input cost rise | +8–12% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

Park Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Park Systems PESTLE Analysis delivers comprehensive political, economic, social, technological, legal, and environmental insights in the same structured layout you see now. No placeholders or teasers—this is the final, professionally formatted file available for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our targeted PESTLE Analysis for Park Systems—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s prospects; ideal for investors, consultants, and executives. Buy the full report to access a complete, editable breakdown that powers smarter decisions and competitive advantage—download instantly.

Political factors

Geopolitical Trade Restrictions and Export Controls

The US-China tech rivalry is reshaping export controls for high-end semiconductor equipment through 2025, with US restrictions targeting over 300 Chinese entities and contributing to a 15% decline in cross-border equipment shipments to China in 2023–24; Park Systems must manage complex licensing to serve Asian hubs like Taiwan and South Korea, which accounted for roughly 60% of global fab equipment demand in 2024. Changes in trade alliances and export lists could open emerging markets—Southeast Asia capex grew ~22% in 2024—or constrain access to critical components, risking supply-chain cost increases and margin pressure for Park Systems.

Government Subsidies for Semiconductor Independence

National initiatives like the U.S. CHIPS and Science Act (US$280B total package including US$52B for semiconductor incentives), EU Chips Act (€43B mobilized) and South Korea’s KRW 510T plan have directed billions into domestic fabs, boosting demand for Park Systems’ metrology tools as new fabs and R&D centers are built.

Inter-Korean Relations and Regional Stability

As a South Korea–headquartered firm, Park Systems is highly sensitive to Korean Peninsula tensions; in 2025 foreign direct investment into South Korea fell 8.1% year-over-year to $13.4bn amid regional uncertainty, which can depress investor confidence for tech exporters.

Escalation risks threaten supply-chain logistics—South Korea handled $1.1tn in goods in 2024—so disruptions could materially raise component lead times and costs for Park Systems’ wafer-probe and AFM production.

Physical security of primary manufacturing hubs in Gyeonggi and Ulsan could force contingency spending; defense and risk insurance premiums for Korean manufacturers rose ~12% in 2024.

Ongoing government diplomatic efforts, including 2024–25 trilateral dialogues with the US and Japan, are critical inputs to Park Systems’ long-term operational planning and risk-management models.

Global Research and Development Funding Policies

Public investment in nanotech and materials science—estimated at $9.6 billion globally in 2024—boosts purchasing by universities and national labs, directly lifting demand for Park Systems’ AFM instruments.

When governments shift budgets toward quantum computing or personalized medicine (global R&D in quantum reached $3.2B in 2024), specialized AFM needs rise, creating cyclical procurement opportunities.

Park Systems depends on these policy-driven funding cycles—public grant awards to research institutions grew ~6% YoY in 2024—to maintain market leadership in scientific AFMs.

- Global nanotech R&D public funding: $9.6B (2024)

- Quantum R&D public spend: $3.2B (2024)

- Research grant growth to institutions: +6% YoY (2024)

Bilateral Trade Agreements and Tariff Structures

The 2023 RCEP and 2022 India-EU negotiations lowering average tariffs by 1–3% improve Park Systems’ export competitiveness and reduce input costs for components, potentially boosting gross margins by 0.5–1.5 percentage points in target markets.

Preferential tariff treatment entering India or ASEAN could increase net revenue per unit; conversely, 2024 US-China tariff retaliations (up to 25% on some components) may force price hikes or shift assembly to Vietnam or Korea to preserve margins.

- RCEP/India-EU tariff cuts: −1–3% average

- Potential margin lift: +0.5–1.5 pp

- Retaliatory tariffs: up to 25% on components (2024)

- Mitigation: relocate assembly to Vietnam/Korea

Export Controls Cut China Shipments 15% as CHIPS Subsidies Boost Metrology Demand

Geopolitical export controls and US-China tech rivalry (15% drop in equipment shipments to China 2023–24) force Park Systems to manage complex licensing while benefiting from domestic fab incentives (US$52B CHIPS, €43B EU, KRW510T SK) that lift metrology demand; regional tensions cut FDI (South Korea FDI −8.1% to $13.4B in 2025) and raise insurance costs (+12% 2024), while RCEP/India‑EU tariff cuts (−1–3%) may improve margins (+0.5–1.5 pp).

| Metric | Value (2024–25) |

|---|---|

| Equip shipments to China | −15% |

| US CHIPS incentives | US$52B |

| EU Chips Act | €43B |

| SK fab plan | KRW 510T |

| SK FDI | $13.4B (−8.1%) |

| Insurance costs | +12% |

| Tariff cuts (RCEP/India‑EU) | −1–3% |

| Potential margin lift | +0.5–1.5 pp |

What is included in the product

Explores how macro-environmental factors uniquely affect Park Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking analysis to identify risks and opportunities for executives, investors, and strategists.

Condenses Park Systems’ PESTLE into a concise, shareable brief that highlights regulatory, technological, and market risks for quick alignment in meetings or slide decks.

Economic factors

Semiconductor Industry Capital Expenditure Cycles

The financial health of Park Systems is tightly linked to capex plans of major logic and memory fabs; TSMC, Samsung and SK Hynix collectively forecast fab equipment spending of about $120–140 billion for 2024–2025, shaping demand for Park’s AFM metrology tools.

As the industry shifts to sub-2nm nodes and advanced packaging by late 2025, high-precision metrology becomes non-discretionary for yield control, increasing addressable market value for Park’s tools by an estimated mid-teens CAGR.

However, cyclical downturns in consumer electronics—global smartphone shipments fell ~6% in 2024—can trigger temporary capex delays, causing short-term revenue variability for Park Systems.

Global Inflationary Pressures and Operational Costs

Persistent mid-2020s inflation—global CPI averaging about 4–5% in 2024–25—has pushed prices for piezoelectric scanners, lasers and RF components up 8–12% and raised skilled labor costs, pressuring AFM gross margins. Park Systems must offset these input cost increases while keeping competitive pricing to sustain ~25–30% operating margins reported in recent years. Rigorous supply-chain management, dual sourcing and procurement hedges for key inputs and freight helped peer firms cut cost volatility by ~30% in 2024. These measures are essential to protect EBITDA against commodity and logistics swings.

Currency Exchange Rate Fluctuations

With roughly 60% of 2024 revenue from overseas markets, Park Systems faces material FX exposure as the KRW strengthened about 4.8% vs USD and 2.3% vs EUR in 2024, which can raise local-currency prices and erode price competitiveness abroad.

A stronger won risks shifting orders to competitors operating in weaker-currency jurisdictions, particularly for price-sensitive semiconductor and materials clients.

Park Systems uses forward contracts, FX options and natural hedges; disclosed hedging reduced 2024 FX-related earnings volatility, limiting translation losses to under 1.5% of revenue.

Growth of the Nanotechnology Market

Growth of the global nanotechnology market to USD 154.7 billion by 2026 (CAGR ~16% from 2021–26) and expanded use in energy storage and biotech diversify Park Systems revenue beyond semiconductors, supporting sales of both high-end and routine AFMs.

Rising venture capital—over USD 8.5 billion invested in nanotech startups in 2024—feeds demand for entry and mid-range AFM systems as new firms commercialize molecular engineering solutions.

Structural shift to molecular-level engineering ensures sustained long-term demand for high-resolution surface characterization tools, underpinning recurring service and upgrade revenue streams for Park Systems.

- Market size 2026: USD 154.7B; CAGR ~16%

- VC funding 2024: >USD 8.5B into nanotech startups

- Demand drivers: energy storage, biotech, molecular engineering

- Revenue impact: diversification, recurring service/upgrades

Interest Rate Environments and Financing Costs

The current high-rate environment—US Fed funds ~5.25–5.50% in 2024 and average corporate loan spreads up ~150–200 bps—raises financing costs, constraining startups and smaller R&D labs from purchasing expensive AFM equipment, prolonging sales cycles.

Higher borrowing costs push customers toward leasing, pay-per-use, or service-led models; Park Systems should expand flexible financing, subscription pricing, and vendor leasing partnerships to capture constrained demand.

- Fed funds ~5.25–5.50% (2024)

- Loan spreads +150–200 bps, slowing CAPEX

- Shift to leasing/service models increases recurring revenue

- Flexible financing and subscription offerings critical for sales

Park Systems rides $120–140B fab capex into booming $154.7B nanotech market

Park Systems’ 2024–25 demand tied to $120–140B fab capex; nanotech market to $154.7B by 2026 (CAGR ~16%); 60% revenue offshore with KRW +4.8% vs USD in 2024; input cost inflation +8–12% pressured ~25–30% OPM; Fed funds ~5.25–5.50% (2024) raised borrowing costs, shifting customers to leasing/subscription.

| Metric | Value |

|---|---|

| Fab capex (2024–25) | $120–140B |

| Nanotech market (2026) | $154.7B |

| Revenue offshore (2024) | ~60% |

| KRW vs USD (2024) | +4.8% |

| Input cost rise | +8–12% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

Park Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Park Systems PESTLE Analysis delivers comprehensive political, economic, social, technological, legal, and environmental insights in the same structured layout you see now. No placeholders or teasers—this is the final, professionally formatted file available for immediate download after payment.