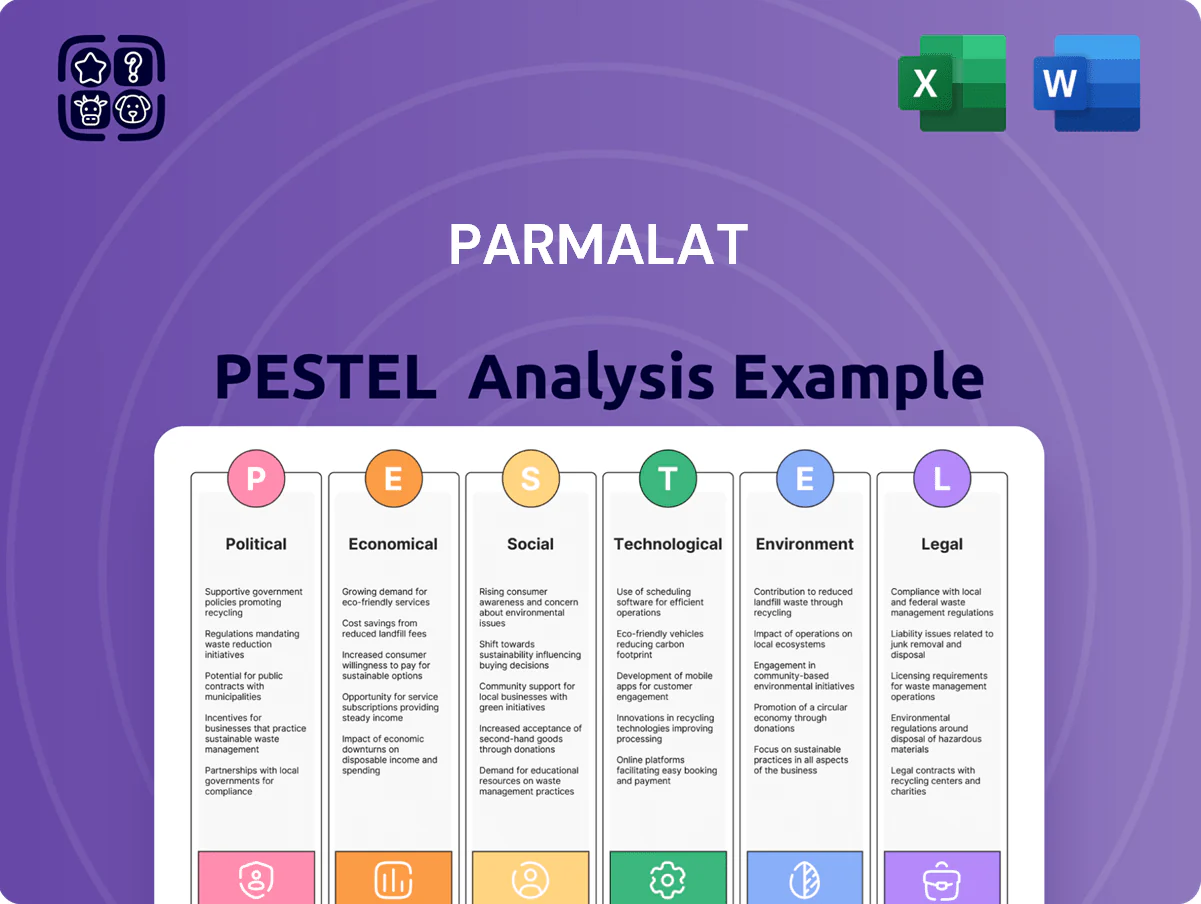

Parmalat PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures are shaping Parmalat’s strategic trajectory—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Purchase the full, editable analysis for a complete breakdown, data-driven insights, and ready-to-use slides to accelerate your investment thesis or strategic plan.

Political factors

EU Common Agricultural Policy reforms

The ongoing evolution of the EU Common Agricultural Policy (CAP) is reshaping milk production quotas and subsidy structures, with 2024–25 CAP disbursements totaling about €54 billion affecting dairy support and green payments. These reforms alter financial incentives for farmers in Italy, France and Germany, influencing Parmalat’s raw milk costs as EU milk prices averaged €0.41/kg in 2024. Management must monitor CAP adjustments to anticipate supply fluctuations and price volatility through 2026.

International trade agreements and tariffs

As a global entity, Parmalat is sensitive to shifts in EU trade relations with the UK and MERCOSUR; UK-EU trade in 2024 saw non-tariff barriers raise food sector costs by an estimated 3–5%, affecting supply chains for dairy imports and exports.

Tariffs on dairy exports can materially change competitiveness: a 10% tariff on milk powder or cheese would lift export prices and could cut Parmalat’s gross margins in affected markets by roughly 2–4 percentage points, based on 2023 product mix.

Strategic planning requires monitoring evolving trade barriers—EU-MERCOSUR negotiations stalled in 2024—with increased logistics costs (container rates up 12% year-on-year in 2024) threatening market access and cross-border delivery economics.

Geopolitical instability in emerging markets

Operations in politically volatile markets compel Parmalat to maintain robust risk management and contingency plans to protect €2.1bn 2024 revenues from EM exposures and ensure supply-chain continuity amid disruptions.

Political unrest or abrupt government shifts can trigger nationalization or sudden changes to foreign investment rules, risking asset seizure or repatriation limits that would hit margins and cash flow.

Investors should assess Parmalat’s geographical diversification—operations across 25 countries with c.45% revenue from developing economies—as a partial hedge against localized political shocks.

Public health and nutrition policies

Governments are tightening regulations on sugar and labeling to fight obesity; EU proposals aim to reduce added sugars by up to 20% in certain products and 2024 Nutri-Score adoption spans 10+ European countries, forcing Parmalat to adapt.

Meeting diverse front-of-pack rules requires reformulation—reducing sugar can raise R&D costs and impact margins; global dairy reformulation spend averages 0.5–1.5% of revenue, a potential multi-million-euro burden for Parmalat (2024 revenue €4.23bn).

Noncompliance risks fines and lost shelf space; reassessing marketing and SKUs is essential to protect brand and retain market share amid stricter public health mandates.

- EU Nutri-Score used in 10+ countries (2024)

- Parmalat 2024 revenue €4.23bn—reformulation could cost 0.5–1.5% of revenue

- Proposed sugar reduction targets up to 20% in some categories

- Noncompliance risks fines, delistings, reputational loss

Agricultural sustainability mandates

Political pressure to cut dairy’s environmental footprint has driven new EU rules targeting methane and nitrogen; EU’s methane strategy and the 2024 Farm-to-Fork updates push for up to 30% reductions in emissions intensity by 2030, raising upstream farming costs for suppliers.

These mandates force adoption of precision feeding, manure management and nitrification inhibitors, increasing supplier costs 5–12% per ton of milk in 2024–25, which feeds into Parmalat’s procurement and margin planning.

Aligning Parmalat’s strategy with government climate agendas—through supplier support, contract adjustments and capex for sustainable sourcing—is essential to preserve supply continuity and avoid regulatory fines and market access risks.

- EU targets: ~30% emissions-intensity cut by 2030

- Supplier cost rise: 5–12%/ton milk (2024–25)

- Actions: precision feeding, manure tech, contract changes

Parmalat faces EU CAP, Nutri‑Score and trade shocks — €2.1bn EM exposure, margins at risk

EU CAP reforms (2024–25 CAP €54bn) and Nutri-Score adoption (10+ countries) affect subsidies, milk costs (€0.41/kg 2024) and reformulation spend (0.5–1.5% of €4.23bn revenue). Trade frictions (UK non‑tariff +3–5%) and stalled MERCOSUR talks raise logistics (container +12% y/y) and tariff risk (10% tariff → –2–4pp gross margin). EM exposure: 45% revenues, €2.1bn at risk.

| Metric | Value |

|---|---|

| 2024 milk price | €0.41/kg |

| Parmalat revenue | €4.23bn |

| EM revenue share | 45% (€2.1bn) |

| Container costs | +12% y/y 2024 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Parmalat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities.

A concise Parmalat PESTLE summary that’s visually segmented by category for quick interpretation, editable for local context, and easily dropped into presentations to align teams on external risks and market positioning.

Economic factors

Raw material price volatility

The cost of raw milk fluctuates sharply—global milk prices rose 18% in 2024 amid stronger demand and higher feed costs—making Parmalat’s margins highly sensitive where pricing power is weak; in 2024 gross margin compressed by ~1.2ppt in Latin America. Analysts track Parmalat’s hedging (use of futures covering ~30% of milk needs in 2024) and multi-year supplier contracts that aim to stabilize input cost exposure against sudden spikes.

Currency exchange rate fluctuations

With operations across Europe, Latin America, Oceania and North America, Parmalat faces translation and transaction risk; a 10% EUR/BRL move in 2024 altered reported Brazilian revenue by roughly €40–60m for peers in the sector, illustrating scale sensitivity.

In 2024 the EUR weakened ~6% vs BRL and gained ~3% vs AUD year‑on‑year, pressuring consolidated euros results and EBITDA margin translation for multinational dairy firms.

Parmalat mitigates volatility via FX derivatives—forward contracts and options—and increased local sourcing; targeted hedges covering 50–80% of near‑term cash flows are common industry practice.

Consumer purchasing power and inflation

Global inflation averaged around 6% in 2023–2024, squeezing household budgets and driving a documented shift: private-label dairy grew 4–7% faster than branded lines in key EU markets in 2024, pressuring Parmalat to weigh price hikes against volume losses.

Parmalat must calibrate increases—2025 input-cost rises of ~8–12% (milk, energy) suggest limited scope for margin expansion without eroding share.

Segmented price-elasticity analysis is critical: low-income cohorts show elasticity estimates near −1.2 while high-income consumers are closer to −0.3, guiding 2026 revenue-management strategies.

Interest rate environment and capital cost

The 2024 ECB rates and global tightening pushed Parmalat’s average borrowing cost higher, raising interest expense—net debt rose to about €1.1bn in FY2023, increasing sensitivity to rate hikes and capital expenditure plans.

Higher rates lower DCF valuations of Parmalat’s projected cash flows, while investors track its FY2023 debt-to-equity (~1.2x) and credit metrics to gauge resilience under shifting monetary policy.

- Net debt ~€1.1bn (FY2023)

- Debt-to-equity ~1.2x (FY2023)

- ECB rate-driven borrowing costs increased in 2024

Logistics and energy cost trends

The dairy sector is energy-intensive; UHT processing and refrigerated logistics account for ~20–30% of Parmalat’s manufacturing and distribution costs, with global oil prices and European wholesale gas averaging €30–€60/MWh in 2024–25 directly impacting margins.

Efficient logistics and €40–€80m annual investments in energy-saving tech and refrigeration upgrades are crucial to shield operating margin from fuel and utility volatility.

- Energy & logistics ≈20–30% of costs

- European gas €30–€60/MWh (2024–25)

- Capex on efficiency €40–€80m/year

- Cold chain exposure drives margin risk

Parmalat under margin pressure: milk +18%, €1.1bn debt, €40–80m efficiency capex

Parmalat faces input-cost volatility—global milk +18% in 2024; hedges covered ~30% of milk needs and multi‑year contracts reduced shock; FY2023 net debt ~€1.1bn and debt/equity ~1.2x heighten rate sensitivity after ECB tightening; energy/logistics ≈20–30% of costs with EU gas €30–€60/MWh (2024–25), driving €40–€80m/yr capex for efficiency.

| Metric | Value (2024/2025) |

|---|---|

| Milk price change | +18% |

| Hedge coverage | ~30% |

| Net debt | ~€1.1bn (FY2023) |

| Debt/Equity | ~1.2x (FY2023) |

| Energy cost share | 20–30% |

| EU gas price | €30–€60/MWh |

| Efficiency capex | €40–€80m/yr |

Preview Before You Purchase

Parmalat PESTLE Analysis

The preview shown here is the exact Parmalat PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. The content, layout, and insights visible in this preview are the same file you’ll download immediately after checkout, delivering a complete, actionable PESTLE review for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures are shaping Parmalat’s strategic trajectory—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions. Purchase the full, editable analysis for a complete breakdown, data-driven insights, and ready-to-use slides to accelerate your investment thesis or strategic plan.

Political factors

EU Common Agricultural Policy reforms

The ongoing evolution of the EU Common Agricultural Policy (CAP) is reshaping milk production quotas and subsidy structures, with 2024–25 CAP disbursements totaling about €54 billion affecting dairy support and green payments. These reforms alter financial incentives for farmers in Italy, France and Germany, influencing Parmalat’s raw milk costs as EU milk prices averaged €0.41/kg in 2024. Management must monitor CAP adjustments to anticipate supply fluctuations and price volatility through 2026.

International trade agreements and tariffs

As a global entity, Parmalat is sensitive to shifts in EU trade relations with the UK and MERCOSUR; UK-EU trade in 2024 saw non-tariff barriers raise food sector costs by an estimated 3–5%, affecting supply chains for dairy imports and exports.

Tariffs on dairy exports can materially change competitiveness: a 10% tariff on milk powder or cheese would lift export prices and could cut Parmalat’s gross margins in affected markets by roughly 2–4 percentage points, based on 2023 product mix.

Strategic planning requires monitoring evolving trade barriers—EU-MERCOSUR negotiations stalled in 2024—with increased logistics costs (container rates up 12% year-on-year in 2024) threatening market access and cross-border delivery economics.

Geopolitical instability in emerging markets

Operations in politically volatile markets compel Parmalat to maintain robust risk management and contingency plans to protect €2.1bn 2024 revenues from EM exposures and ensure supply-chain continuity amid disruptions.

Political unrest or abrupt government shifts can trigger nationalization or sudden changes to foreign investment rules, risking asset seizure or repatriation limits that would hit margins and cash flow.

Investors should assess Parmalat’s geographical diversification—operations across 25 countries with c.45% revenue from developing economies—as a partial hedge against localized political shocks.

Public health and nutrition policies

Governments are tightening regulations on sugar and labeling to fight obesity; EU proposals aim to reduce added sugars by up to 20% in certain products and 2024 Nutri-Score adoption spans 10+ European countries, forcing Parmalat to adapt.

Meeting diverse front-of-pack rules requires reformulation—reducing sugar can raise R&D costs and impact margins; global dairy reformulation spend averages 0.5–1.5% of revenue, a potential multi-million-euro burden for Parmalat (2024 revenue €4.23bn).

Noncompliance risks fines and lost shelf space; reassessing marketing and SKUs is essential to protect brand and retain market share amid stricter public health mandates.

- EU Nutri-Score used in 10+ countries (2024)

- Parmalat 2024 revenue €4.23bn—reformulation could cost 0.5–1.5% of revenue

- Proposed sugar reduction targets up to 20% in some categories

- Noncompliance risks fines, delistings, reputational loss

Agricultural sustainability mandates

Political pressure to cut dairy’s environmental footprint has driven new EU rules targeting methane and nitrogen; EU’s methane strategy and the 2024 Farm-to-Fork updates push for up to 30% reductions in emissions intensity by 2030, raising upstream farming costs for suppliers.

These mandates force adoption of precision feeding, manure management and nitrification inhibitors, increasing supplier costs 5–12% per ton of milk in 2024–25, which feeds into Parmalat’s procurement and margin planning.

Aligning Parmalat’s strategy with government climate agendas—through supplier support, contract adjustments and capex for sustainable sourcing—is essential to preserve supply continuity and avoid regulatory fines and market access risks.

- EU targets: ~30% emissions-intensity cut by 2030

- Supplier cost rise: 5–12%/ton milk (2024–25)

- Actions: precision feeding, manure tech, contract changes

Parmalat faces EU CAP, Nutri‑Score and trade shocks — €2.1bn EM exposure, margins at risk

EU CAP reforms (2024–25 CAP €54bn) and Nutri-Score adoption (10+ countries) affect subsidies, milk costs (€0.41/kg 2024) and reformulation spend (0.5–1.5% of €4.23bn revenue). Trade frictions (UK non‑tariff +3–5%) and stalled MERCOSUR talks raise logistics (container +12% y/y) and tariff risk (10% tariff → –2–4pp gross margin). EM exposure: 45% revenues, €2.1bn at risk.

| Metric | Value |

|---|---|

| 2024 milk price | €0.41/kg |

| Parmalat revenue | €4.23bn |

| EM revenue share | 45% (€2.1bn) |

| Container costs | +12% y/y 2024 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Parmalat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities.

A concise Parmalat PESTLE summary that’s visually segmented by category for quick interpretation, editable for local context, and easily dropped into presentations to align teams on external risks and market positioning.

Economic factors

Raw material price volatility

The cost of raw milk fluctuates sharply—global milk prices rose 18% in 2024 amid stronger demand and higher feed costs—making Parmalat’s margins highly sensitive where pricing power is weak; in 2024 gross margin compressed by ~1.2ppt in Latin America. Analysts track Parmalat’s hedging (use of futures covering ~30% of milk needs in 2024) and multi-year supplier contracts that aim to stabilize input cost exposure against sudden spikes.

Currency exchange rate fluctuations

With operations across Europe, Latin America, Oceania and North America, Parmalat faces translation and transaction risk; a 10% EUR/BRL move in 2024 altered reported Brazilian revenue by roughly €40–60m for peers in the sector, illustrating scale sensitivity.

In 2024 the EUR weakened ~6% vs BRL and gained ~3% vs AUD year‑on‑year, pressuring consolidated euros results and EBITDA margin translation for multinational dairy firms.

Parmalat mitigates volatility via FX derivatives—forward contracts and options—and increased local sourcing; targeted hedges covering 50–80% of near‑term cash flows are common industry practice.

Consumer purchasing power and inflation

Global inflation averaged around 6% in 2023–2024, squeezing household budgets and driving a documented shift: private-label dairy grew 4–7% faster than branded lines in key EU markets in 2024, pressuring Parmalat to weigh price hikes against volume losses.

Parmalat must calibrate increases—2025 input-cost rises of ~8–12% (milk, energy) suggest limited scope for margin expansion without eroding share.

Segmented price-elasticity analysis is critical: low-income cohorts show elasticity estimates near −1.2 while high-income consumers are closer to −0.3, guiding 2026 revenue-management strategies.

Interest rate environment and capital cost

The 2024 ECB rates and global tightening pushed Parmalat’s average borrowing cost higher, raising interest expense—net debt rose to about €1.1bn in FY2023, increasing sensitivity to rate hikes and capital expenditure plans.

Higher rates lower DCF valuations of Parmalat’s projected cash flows, while investors track its FY2023 debt-to-equity (~1.2x) and credit metrics to gauge resilience under shifting monetary policy.

- Net debt ~€1.1bn (FY2023)

- Debt-to-equity ~1.2x (FY2023)

- ECB rate-driven borrowing costs increased in 2024

Logistics and energy cost trends

The dairy sector is energy-intensive; UHT processing and refrigerated logistics account for ~20–30% of Parmalat’s manufacturing and distribution costs, with global oil prices and European wholesale gas averaging €30–€60/MWh in 2024–25 directly impacting margins.

Efficient logistics and €40–€80m annual investments in energy-saving tech and refrigeration upgrades are crucial to shield operating margin from fuel and utility volatility.

- Energy & logistics ≈20–30% of costs

- European gas €30–€60/MWh (2024–25)

- Capex on efficiency €40–€80m/year

- Cold chain exposure drives margin risk

Parmalat under margin pressure: milk +18%, €1.1bn debt, €40–80m efficiency capex

Parmalat faces input-cost volatility—global milk +18% in 2024; hedges covered ~30% of milk needs and multi‑year contracts reduced shock; FY2023 net debt ~€1.1bn and debt/equity ~1.2x heighten rate sensitivity after ECB tightening; energy/logistics ≈20–30% of costs with EU gas €30–€60/MWh (2024–25), driving €40–€80m/yr capex for efficiency.

| Metric | Value (2024/2025) |

|---|---|

| Milk price change | +18% |

| Hedge coverage | ~30% |

| Net debt | ~€1.1bn (FY2023) |

| Debt/Equity | ~1.2x (FY2023) |

| Energy cost share | 20–30% |

| EU gas price | €30–€60/MWh |

| Efficiency capex | €40–€80m/yr |

Preview Before You Purchase

Parmalat PESTLE Analysis

The preview shown here is the exact Parmalat PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises. The content, layout, and insights visible in this preview are the same file you’ll download immediately after checkout, delivering a complete, actionable PESTLE review for strategic decision-making.