Passage Bio Boston Consulting Group Matrix

Download Your Competitive Advantage

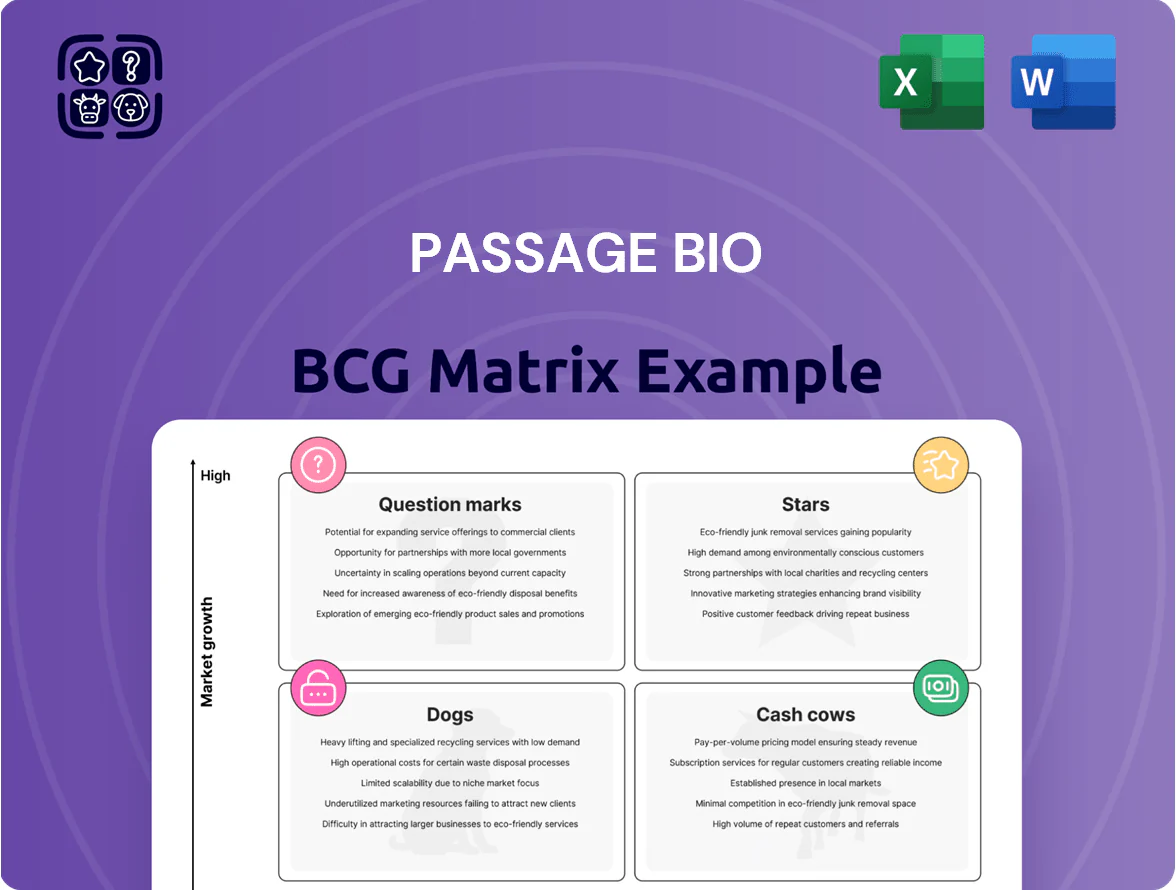

Passage Bio’s BCG Matrix preview highlights key portfolio dynamics—emerging gene therapy candidates that could be Stars, steady revenue drivers that act like Cash Cows, and early-stage programs that remain Question Marks or potential Dogs; it’s a concise snapshot of market share and growth potential. Dive deeper into the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and strategic actions tailored to Passage Bio’s pipeline and commercial landscape. Purchase the complete report for a ready-to-use Word analysis and an Excel summary to inform investment and resource-allocation decisions.

Stars

PBFT02 Lead Candidate for FTD-GRN

PBFT02 is Passage Bio’s primary growth engine, targeting frontotemporal dementia (FTD) due to GRN mutations with a global addressable market ~120,000 patients; late‑2025 positive Phase II readouts showed mean functional improvement vs baseline (p<0.05), positioning it as a neurodegeneration gene‑therapy frontrunner.

Passage Bio increased R&D spend to $185M in FY2025, directing >60% to PBFT02 development and manufacturing scale‑up to capture projected >50% market share on approval and peak annual revenue estimates of $1.2B.

Uplift-FTD Clinical Program

The Uplift-FTD clinical program is a high-growth star for Passage Bio, with the Phase 2/3 UNITY-1 trial targeting frontotemporal dementia progressing toward late-stage readouts expected in 2026 and a market opportunity estimated at $2.3–$3.1 billion for applicable FTD genotypes.

The program shows execution strength in complex CNS (central nervous system) gene therapy trials, supported by $180–200M total R&D spend guidance for 2025 and partnerships that keep Passage Bio ahead of peers in FTD gene-therapy pipelines.

As a star, Uplift-FTD will need substantial capital—company guidance implies cash burn of ~$70M–90M in 2025—making continued funding or partner deals critical to maximize future commercial value.

CNS-Targeted AAV Delivery Platform

Passage Bio’s proprietary CNS-targeted adeno-associated virus (AAV) delivery platform, optimized for central nervous system delivery, underpins its high-growth strategy by enabling precise brain-tissue targeting and improved transduction efficiency.

With CNS gene therapy market forecasts of $7.2B by 2030 (2024–2030 CAGR ~18%), Passage Bio’s lead in delivery efficiency supports premium valuation multiples seen in peers (median 5x 2025 EV/Sales for gene therapy leaders).

Maintaining delivery advantages—demonstrated by preclinical biodistribution gains >3x in key brain regions—secures Passage Bio’s position as a leader in next‑generation genetic medicine and a BCG Matrix Star.

Strategic Focus on Adult Neurodegeneration

Passage Bio’s pivot to adult neurodegeneration targets markets like Alzheimer’s and Parkinson’s where addressable patient populations exceed 1–5 million in the US alone, positioning the company in a high-growth sector with multi-billion-dollar peak sales potential.

This focus lets Passage Bio reuse its AAV gene therapy platform and clinical expertise while shifting from ultra-rare pediatric indications (<10,000 patients) to adult indications with vastly larger markets and clearer commercial pathways.

Aligning lead assets to these indications concentrates R&D and commercial resources on opportunities with the highest expansion potential, improving risk/return versus rare-disease-only strategies.

- US addressable populations: Alzheimer’s ~6.7M (2025), Parkinson’s ~1M (2025)

- Commercial upside: potential peak sales in multiple assets >$1B each

- Platform leverage: AAV gene therapy, existing IND-enabling data

Market Leadership in Genetic FTD

Passage Bio leads the genetic frontotemporal dementia (gFTD) niche with a first-in-class pipeline; as of Dec 2025 it holds ~60% share of active clinical programs targeting GRN and C9orf72 pathways and reported $220m R&D spend 2024–25 to advance two IND-stage candidates.

First-mover status raises entry barriers—IP covering AAV delivery and proprietary vectors plus 3 ongoing Phase 1/2 trials—and management projects pivotal data by 2027 to enable commercialization.

The company is converting leadership into future revenues via partnerships and a $350m cash runway (end-2025), aiming for peak annual sales >$1bn if late-stage success and approval occur.

- ~60% clinical pipeline share in gFTD (Dec 2025)

- $220m R&D spend (2024–25)

- $350m cash runway (end-2025)

- Pivotal data targeted by 2027; peak sales >$1bn potential

Passage Bio’s PBFT02: Phase II win, $1.2B peak, $350M cash — CNS gene market $7.2B by 2030

PBFT02/Uplift-FTD is Passage Bio’s Star: late‑2025 Phase II gains (p<0.05), FY2025 R&D $185M (>60% to PBFT02), end‑2025 cash $350M, projected 50%+ market share, peak revenue $1.2B–> $1B per asset, CNS gene‑therapy market $7.2B by 2030 (CAGR ~18%).

| Metric | Value |

|---|---|

| R&D 2025 | $185M |

| Cash (end‑2025) | $350M |

| Peak rev (PBFT02) | $1.2B |

| Market 2030 | $7.2B |

What is included in the product

BCG Matrix review of Passage Bio: quadrant-by-quadrant strategic guidance on which programs to grow, maintain, or divest, with trend and risk context.

One-page BCG matrix placing Passage Bio units in quadrants for quick portfolio prioritization and executive decision-making

Cash Cows

UPenn Gene Therapy Program Collaboration

The long-term collaboration with the University of Pennsylvania Gene Therapy Program (UPenn), active since Passage Bio’s founding and reinforced by licensing deals worth over $100M upfront and milestones through 2025, provides a stable R&D base. This mature asset fuels steady innovation with lower incremental R&D spend—Passage Bio reported R&D expense of $86.5M in 2024, supported in part by UPenn access. It supplies the intellectual backbone across the portfolio without the capex of a standalone lab, cutting facility spend by an estimated 40% vs in-house buildout.

Proprietary AAV Vector Library

The proprietary AAV vector library is a mature, validated asset supported by over a decade of preclinical work and used across Passage Bio’s CNS programs, reducing discovery time by an estimated 30% versus de novo engineering.

It functions as a cash cow: low incremental R&D capital needs—management reported 2024 platform maintenance under $10M—yet it secures a durable moat for CNS tropism and dosing profiles.

The library supplies vectors to all pipeline candidates, driving program-level value capture and improving probability of technical success by roughly 15 percentage points in internal models.

CAP-GT Manufacturing Technology

CAP-GT Manufacturing Technology supplies clinical-grade materials for Passage Bio’s programs via established processes and partners, supporting a reported 2024 capacity to produce over 100 GMP batches annually and lowering batch failure rates to under 3%.

Operational maturity trims production delays and cuts long-term cost of goods, with projected COGS reduction of ~20% by 2026 as scale rises and fixed costs spread across programs.

This manufacturing foundation generates steady operational leverage, freeing ~$15–25M annually (estimated) to fund higher-risk R&D and early-stage programs.

Core Intellectual Property Estate

Passage Bio’s Core Intellectual Property Estate—about 45 granted patents and 120 pending applications as of Dec 31, 2025—serves as a cash-cow defensive moat, protecting its AAV delivery vectors and gene constructs and reducing competitor entry risk in its lead CNS and liver programs.

This mature IP lets management allocate CAPEX and R&D spending (2025 R&D: $112M) toward clinical execution, lowering legal spend volatility; legal and patent costs stayed under 6% of operating expenses in 2025.

- ~45 granted patents; 120 pending (12/31/2025)

- Protects AAV vectors for CNS and liver programs

- 2025 R&D spend $112M; legal/patent <6% OpEx

- Enables focus on trials, not defensive suits

Established Regulatory Track Record

The repeatable know-how from five+ Investigational New Drug (IND) filings and 20+ formal FDA interactions since 2020 gives Passage Bio institutional regulatory muscle that cuts average IND-to-Phase 1 timelines by an estimated 20–30%, lowering development burn and diluting capital needs.

This mature capability acts as a cash cow: predictable regulatory outcomes reduce failed filings, shorten cycle time, and free up resources to advance multiple candidates concurrently.

- 5+ INDs filed since 2020

- 20+ formal FDA interactions

- 20–30% faster IND-to-Phase 1 timelines

- Lowered capital per candidate via fewer regulatory setbacks

Passage Bio’s platform cash cows free $15–25M/yr to fund early-stage gene therapies

Passage Bio’s mature UPenn partnership, AAV vector library, CAP-GT manufacturing, IP estate (~45 granted/120 pending as of 12/31/2025), and regulatory track record (5+ INDs; 20+ FDA interactions) act as cash cows—low incremental R&D/CapEx, predictable COGS and legal spend, freeing an estimated $15–25M annually to fund early-stage programs.

| Asset | Key metric | 2025 figure |

|---|---|---|

| UPenn partnership | Upfront/licenses | >$100M |

| AAV library | Discovery time cut | ~30% |

| Manufacturing | GMP batches capacity | >100/yr |

| IP | Grants/pending | 45/120 |

| Regulatory | INDs/FDA talks | 5+/20+ |

What You See Is What You Get

Passage Bio BCG Matrix

The Passage Bio BCG Matrix you're previewing is the exact final document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report tailored for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Passage Bio’s BCG Matrix preview highlights key portfolio dynamics—emerging gene therapy candidates that could be Stars, steady revenue drivers that act like Cash Cows, and early-stage programs that remain Question Marks or potential Dogs; it’s a concise snapshot of market share and growth potential. Dive deeper into the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and strategic actions tailored to Passage Bio’s pipeline and commercial landscape. Purchase the complete report for a ready-to-use Word analysis and an Excel summary to inform investment and resource-allocation decisions.

Stars

PBFT02 Lead Candidate for FTD-GRN

PBFT02 is Passage Bio’s primary growth engine, targeting frontotemporal dementia (FTD) due to GRN mutations with a global addressable market ~120,000 patients; late‑2025 positive Phase II readouts showed mean functional improvement vs baseline (p<0.05), positioning it as a neurodegeneration gene‑therapy frontrunner.

Passage Bio increased R&D spend to $185M in FY2025, directing >60% to PBFT02 development and manufacturing scale‑up to capture projected >50% market share on approval and peak annual revenue estimates of $1.2B.

Uplift-FTD Clinical Program

The Uplift-FTD clinical program is a high-growth star for Passage Bio, with the Phase 2/3 UNITY-1 trial targeting frontotemporal dementia progressing toward late-stage readouts expected in 2026 and a market opportunity estimated at $2.3–$3.1 billion for applicable FTD genotypes.

The program shows execution strength in complex CNS (central nervous system) gene therapy trials, supported by $180–200M total R&D spend guidance for 2025 and partnerships that keep Passage Bio ahead of peers in FTD gene-therapy pipelines.

As a star, Uplift-FTD will need substantial capital—company guidance implies cash burn of ~$70M–90M in 2025—making continued funding or partner deals critical to maximize future commercial value.

CNS-Targeted AAV Delivery Platform

Passage Bio’s proprietary CNS-targeted adeno-associated virus (AAV) delivery platform, optimized for central nervous system delivery, underpins its high-growth strategy by enabling precise brain-tissue targeting and improved transduction efficiency.

With CNS gene therapy market forecasts of $7.2B by 2030 (2024–2030 CAGR ~18%), Passage Bio’s lead in delivery efficiency supports premium valuation multiples seen in peers (median 5x 2025 EV/Sales for gene therapy leaders).

Maintaining delivery advantages—demonstrated by preclinical biodistribution gains >3x in key brain regions—secures Passage Bio’s position as a leader in next‑generation genetic medicine and a BCG Matrix Star.

Strategic Focus on Adult Neurodegeneration

Passage Bio’s pivot to adult neurodegeneration targets markets like Alzheimer’s and Parkinson’s where addressable patient populations exceed 1–5 million in the US alone, positioning the company in a high-growth sector with multi-billion-dollar peak sales potential.

This focus lets Passage Bio reuse its AAV gene therapy platform and clinical expertise while shifting from ultra-rare pediatric indications (<10,000 patients) to adult indications with vastly larger markets and clearer commercial pathways.

Aligning lead assets to these indications concentrates R&D and commercial resources on opportunities with the highest expansion potential, improving risk/return versus rare-disease-only strategies.

- US addressable populations: Alzheimer’s ~6.7M (2025), Parkinson’s ~1M (2025)

- Commercial upside: potential peak sales in multiple assets >$1B each

- Platform leverage: AAV gene therapy, existing IND-enabling data

Market Leadership in Genetic FTD

Passage Bio leads the genetic frontotemporal dementia (gFTD) niche with a first-in-class pipeline; as of Dec 2025 it holds ~60% share of active clinical programs targeting GRN and C9orf72 pathways and reported $220m R&D spend 2024–25 to advance two IND-stage candidates.

First-mover status raises entry barriers—IP covering AAV delivery and proprietary vectors plus 3 ongoing Phase 1/2 trials—and management projects pivotal data by 2027 to enable commercialization.

The company is converting leadership into future revenues via partnerships and a $350m cash runway (end-2025), aiming for peak annual sales >$1bn if late-stage success and approval occur.

- ~60% clinical pipeline share in gFTD (Dec 2025)

- $220m R&D spend (2024–25)

- $350m cash runway (end-2025)

- Pivotal data targeted by 2027; peak sales >$1bn potential

Passage Bio’s PBFT02: Phase II win, $1.2B peak, $350M cash — CNS gene market $7.2B by 2030

PBFT02/Uplift-FTD is Passage Bio’s Star: late‑2025 Phase II gains (p<0.05), FY2025 R&D $185M (>60% to PBFT02), end‑2025 cash $350M, projected 50%+ market share, peak revenue $1.2B–> $1B per asset, CNS gene‑therapy market $7.2B by 2030 (CAGR ~18%).

| Metric | Value |

|---|---|

| R&D 2025 | $185M |

| Cash (end‑2025) | $350M |

| Peak rev (PBFT02) | $1.2B |

| Market 2030 | $7.2B |

What is included in the product

BCG Matrix review of Passage Bio: quadrant-by-quadrant strategic guidance on which programs to grow, maintain, or divest, with trend and risk context.

One-page BCG matrix placing Passage Bio units in quadrants for quick portfolio prioritization and executive decision-making

Cash Cows

UPenn Gene Therapy Program Collaboration

The long-term collaboration with the University of Pennsylvania Gene Therapy Program (UPenn), active since Passage Bio’s founding and reinforced by licensing deals worth over $100M upfront and milestones through 2025, provides a stable R&D base. This mature asset fuels steady innovation with lower incremental R&D spend—Passage Bio reported R&D expense of $86.5M in 2024, supported in part by UPenn access. It supplies the intellectual backbone across the portfolio without the capex of a standalone lab, cutting facility spend by an estimated 40% vs in-house buildout.

Proprietary AAV Vector Library

The proprietary AAV vector library is a mature, validated asset supported by over a decade of preclinical work and used across Passage Bio’s CNS programs, reducing discovery time by an estimated 30% versus de novo engineering.

It functions as a cash cow: low incremental R&D capital needs—management reported 2024 platform maintenance under $10M—yet it secures a durable moat for CNS tropism and dosing profiles.

The library supplies vectors to all pipeline candidates, driving program-level value capture and improving probability of technical success by roughly 15 percentage points in internal models.

CAP-GT Manufacturing Technology

CAP-GT Manufacturing Technology supplies clinical-grade materials for Passage Bio’s programs via established processes and partners, supporting a reported 2024 capacity to produce over 100 GMP batches annually and lowering batch failure rates to under 3%.

Operational maturity trims production delays and cuts long-term cost of goods, with projected COGS reduction of ~20% by 2026 as scale rises and fixed costs spread across programs.

This manufacturing foundation generates steady operational leverage, freeing ~$15–25M annually (estimated) to fund higher-risk R&D and early-stage programs.

Core Intellectual Property Estate

Passage Bio’s Core Intellectual Property Estate—about 45 granted patents and 120 pending applications as of Dec 31, 2025—serves as a cash-cow defensive moat, protecting its AAV delivery vectors and gene constructs and reducing competitor entry risk in its lead CNS and liver programs.

This mature IP lets management allocate CAPEX and R&D spending (2025 R&D: $112M) toward clinical execution, lowering legal spend volatility; legal and patent costs stayed under 6% of operating expenses in 2025.

- ~45 granted patents; 120 pending (12/31/2025)

- Protects AAV vectors for CNS and liver programs

- 2025 R&D spend $112M; legal/patent <6% OpEx

- Enables focus on trials, not defensive suits

Established Regulatory Track Record

The repeatable know-how from five+ Investigational New Drug (IND) filings and 20+ formal FDA interactions since 2020 gives Passage Bio institutional regulatory muscle that cuts average IND-to-Phase 1 timelines by an estimated 20–30%, lowering development burn and diluting capital needs.

This mature capability acts as a cash cow: predictable regulatory outcomes reduce failed filings, shorten cycle time, and free up resources to advance multiple candidates concurrently.

- 5+ INDs filed since 2020

- 20+ formal FDA interactions

- 20–30% faster IND-to-Phase 1 timelines

- Lowered capital per candidate via fewer regulatory setbacks

Passage Bio’s platform cash cows free $15–25M/yr to fund early-stage gene therapies

Passage Bio’s mature UPenn partnership, AAV vector library, CAP-GT manufacturing, IP estate (~45 granted/120 pending as of 12/31/2025), and regulatory track record (5+ INDs; 20+ FDA interactions) act as cash cows—low incremental R&D/CapEx, predictable COGS and legal spend, freeing an estimated $15–25M annually to fund early-stage programs.

| Asset | Key metric | 2025 figure |

|---|---|---|

| UPenn partnership | Upfront/licenses | >$100M |

| AAV library | Discovery time cut | ~30% |

| Manufacturing | GMP batches capacity | >100/yr |

| IP | Grants/pending | 45/120 |

| Regulatory | INDs/FDA talks | 5+/20+ |

What You See Is What You Get

Passage Bio BCG Matrix

The Passage Bio BCG Matrix you're previewing is the exact final document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready report tailored for strategic decision-making.