Passage Bio Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Passage Bio faces high competitive intensity driven by biotech incumbents and pipeline uncertainty, while supplier and buyer leverage vary with trial-stage partnerships and payer scrutiny; regulatory hurdles and substitute therapies add notable pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic implications tailored to Passage Bio.

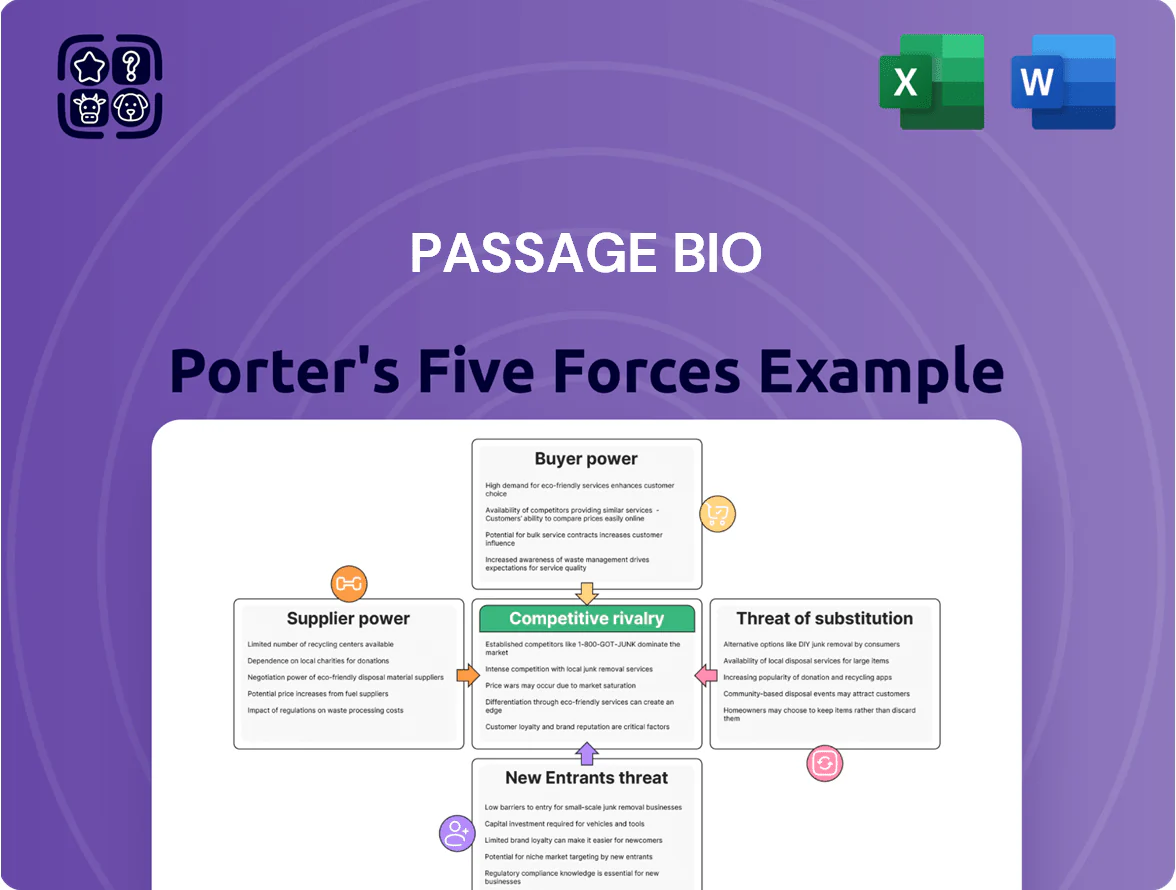

Suppliers Bargaining Power

Specialized AAV manufacturing capacity

Passage Bio depends on a handful of specialized CDMOs for high-quality AAV vectors; global AAV manufacturing capacity was estimated at ~200–300 clinical-grade batches/year in 2024, so suppliers hold pricing and scheduling leverage as Passage scales trials through 2025.

Intellectual property and licensing partners

Passage Bio depends on licensed capsids and delivery tech from the University of Pennsylvania/Gene Therapy Program, giving those licensors strong bargaining power over royalties, field restrictions, and sublicensing; in 2025 Passage reported R&D spend of $145m, so licensing cost shifts materially affect cash burn.

A licensor controlling modification or expansion rights can block or delay new indications, raising pipeline risk—any partnership change could jeopardize programs like PBGM01 and force costly renegotiations.

Given limited alternative IP—most AAV capsids are patented—supplier power remains high, implying sustained royalty and milestone liabilities and potential dilution if equity concessions are required.

Access to high-grade biological reagents

The synthesis of Passage Bio's gene therapies depends on medical-grade plasmids and reagents made by a handful of specialized suppliers, and roughly 70–80% of clinical-grade plasmid capacity in 2024 was concentrated among top five vendors, raising single-source risk. Any supplier disruption can delay GMP manufacturing runs and push trial timelines by months, increasing development costs; Passage Bio reported R&D expense of $137.4M in 2024, so delays materially affect burn. This supplier concentration lets vendors set prices and lead times in a niche market, compressing margins and forcing Passage to secure long-term contracts or dual sourcing to reduce risk.

Competition for specialized scientific talent

The pool of researchers and clinicians with dual expertise in gene therapy and CNS disorders is very small, driving up hiring costs; biotech hiring data show specialized gene-therapy scientist salaries rose ~12–18% YoY through 2024 and total compensation often exceeds $250k in hotspots like Boston and San Francisco.

As >150 new genomic-medicine startups entered the field by late 2025, competition pushed retention costs and contractor rates higher, raising operational spend and stretching R&D timelines.

- Small talent pool = high supplier power

- Salaries up ~12–18% YoY; comp >$250k in hotspots

- 150+ new startups by late 2025 increased demand

- Higher Opex and slower R&D cycles

Clinical trial site and investigator availability

Conducting trials for rare CNS disorders needs specialized centers and highly trained principal investigators; only about 50–100 US sites (est. 2024) can handle complex intrathecal or intraparenchymal administrations, giving those sites strong leverage.

Passage Bio must outbid larger pharma for site access, staff time, and scheduling; site contracting delays can add months and raise trial costs—site premiums of 10–30% over routine studies were reported in 2023.

Limited site capacity plus competing programs increases supplier bargaining power, raising risk to timelines and requiring higher site incentives and strategic partnerships.

- ~50–100 specialized US sites (2024)

- Site premiums 10–30% (2023 data)

- Competes with big pharma for investigators

- Delays add months, raise trial costs

Supplier squeeze: limited AAV capacity, dominant plasmid vendors drive high Passage costs

Suppliers—CDMOs, plasmid/reagent makers, licensors (UPenn), specialized sites and talent—hold high bargaining power for Passage Bio; 2024–25 data: global AAV clinical capacity ~200–300 batches/yr, top-5 plasmid vendors = 70–80% capacity, Passage R&D spend $137.4–145m, ~50–100 specialized US CNS sites, specialized scientist comp >$250k and +12–18% YoY.

| Category | Metric (year) |

|---|---|

| Global AAV capacity | ~200–300 batches/yr (2024) |

| Top-5 plasmid share | 70–80% (2024) |

| Passage R&D spend | $137.4–145M (2024–25) |

| Specialized US sites | ~50–100 (2024) |

| Specialist comp | >$250k; +12–18% YoY (2024) |

What is included in the product

Tailored exclusively for Passage Bio, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its market position and profitability.

A concise Passage Bio Porter's Five Forces one-sheet that highlights competitive intensity and collaboration opportunities to speed therapeutic strategy decisions and investor briefings.

Customers Bargaining Power

Concentrated payer influence on pricing

Payers—mainly Medicare, Medicaid, and large private insurers—hold strong leverage over Passage Bio because they negotiate reimbursement for therapies that can cost $1–3M per dose; in 2024 US specialty drug spend was $250B, pushing payers to demand discounts and outcomes-based contracts.

Adoption of outcome-based payment models

Value-based contracts tying payments to multi-year clinical milestones are rising; 2024 CMS pilots and several US payers now seek outcomes links in rare-disease deals, shifting reimbursement risk to manufacturers and strengthening customer bargaining power. Passage Bio faces higher negotiation pressure as payers demand performance data for GM1 and Krabbe treatments, often with payment spread over 3–5 years and potential rebates of 20–40% if targets fail. This raises cash-flow and capital needs— Passage Bio must model 5–10 year revenue deferrals and secure financing to cover up-front manufacturing and trial costs. Negotiating warranties, data rights, and stop-loss clauses will be key to keep therapies economically viable.

Influence of rare disease advocacy groups

Patient advocacy groups shape priorities and funding in rare diseases; for example, the National Organization for Rare Disorders (NORD) influenced policy that helped secure $1.1B for gene therapy R&D in 2024, steering Passage Bio toward high-impact indications.

These groups press for affordable access—campaigns have led to price negotiations cutting list prices by 20–40% in several orphan drug cases—so Passage Bio’s pricing and launch plans face strong public scrutiny.

The collective voice can sway payers and regulators; 72% of surveyed rare disease advocates in 2025 said they would actively oppose companies they view as exploitative, making advocacy alignment a commercial necessity for Passage Bio.

Limited patient populations in niche markets

- Low patient counts = high per-patient revenue impact

- Major centers control referral flows and protocols

- Loss of 10–20 patients can cut revenues by $10–60M

Governmental regulatory and health technology assessments

Government health technology assessment (HTA) bodies—like NICE in the UK and IQWiG in Germany—act as gatekeepers, assessing cost-effectiveness and can exclude therapies from public formularies; in 2024, NICE rejected or recommended use only in research for ~12% of new high-cost therapies, showing real veto power.

This creates high-stakes entry risk for Passage Bio: a negative HTA decision can block an entire national market, sharply limiting peak sales and reimbursement prospects—HTA-driven price pressure often cuts target prices by 20–50% versus list price.

- HTA vetoes affect national access

- NICE ~12% rejection rate (2024)

- Price cuts commonly 20–50%

- Market entry depends on favorable cost-benefit

Payers, HTAs & Advocacy Hold the Levers: Small Patient Shifts Risk $10–60M for Passage Bio

Payers, patient groups, centers, and HTAs wield strong leverage over Passage Bio—payers push outcomes-based deals (2024 US specialty drug spend $250B), advocacy influenced $1.1B gene therapy R&D (2024), NICE rejected ~12% high-cost therapies (2024), and losing 10–20 patients can swing $10–60M given $1–3M list prices.

| Stakeholder | Key metric |

|---|---|

| Payers | $250B specialty spend (2024) |

| Advocacy | $1.1B R&D influence (2024) |

| HTA | NICE ~12% rejection (2024) |

| Centers | Loss 10–20 pts = $10–60M |

What You See Is What You Get

Passage Bio Porter's Five Forces Analysis

This preview shows the exact Passage Bio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis file available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Passage Bio faces high competitive intensity driven by biotech incumbents and pipeline uncertainty, while supplier and buyer leverage vary with trial-stage partnerships and payer scrutiny; regulatory hurdles and substitute therapies add notable pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic implications tailored to Passage Bio.

Suppliers Bargaining Power

Specialized AAV manufacturing capacity

Passage Bio depends on a handful of specialized CDMOs for high-quality AAV vectors; global AAV manufacturing capacity was estimated at ~200–300 clinical-grade batches/year in 2024, so suppliers hold pricing and scheduling leverage as Passage scales trials through 2025.

Intellectual property and licensing partners

Passage Bio depends on licensed capsids and delivery tech from the University of Pennsylvania/Gene Therapy Program, giving those licensors strong bargaining power over royalties, field restrictions, and sublicensing; in 2025 Passage reported R&D spend of $145m, so licensing cost shifts materially affect cash burn.

A licensor controlling modification or expansion rights can block or delay new indications, raising pipeline risk—any partnership change could jeopardize programs like PBGM01 and force costly renegotiations.

Given limited alternative IP—most AAV capsids are patented—supplier power remains high, implying sustained royalty and milestone liabilities and potential dilution if equity concessions are required.

Access to high-grade biological reagents

The synthesis of Passage Bio's gene therapies depends on medical-grade plasmids and reagents made by a handful of specialized suppliers, and roughly 70–80% of clinical-grade plasmid capacity in 2024 was concentrated among top five vendors, raising single-source risk. Any supplier disruption can delay GMP manufacturing runs and push trial timelines by months, increasing development costs; Passage Bio reported R&D expense of $137.4M in 2024, so delays materially affect burn. This supplier concentration lets vendors set prices and lead times in a niche market, compressing margins and forcing Passage to secure long-term contracts or dual sourcing to reduce risk.

Competition for specialized scientific talent

The pool of researchers and clinicians with dual expertise in gene therapy and CNS disorders is very small, driving up hiring costs; biotech hiring data show specialized gene-therapy scientist salaries rose ~12–18% YoY through 2024 and total compensation often exceeds $250k in hotspots like Boston and San Francisco.

As >150 new genomic-medicine startups entered the field by late 2025, competition pushed retention costs and contractor rates higher, raising operational spend and stretching R&D timelines.

- Small talent pool = high supplier power

- Salaries up ~12–18% YoY; comp >$250k in hotspots

- 150+ new startups by late 2025 increased demand

- Higher Opex and slower R&D cycles

Clinical trial site and investigator availability

Conducting trials for rare CNS disorders needs specialized centers and highly trained principal investigators; only about 50–100 US sites (est. 2024) can handle complex intrathecal or intraparenchymal administrations, giving those sites strong leverage.

Passage Bio must outbid larger pharma for site access, staff time, and scheduling; site contracting delays can add months and raise trial costs—site premiums of 10–30% over routine studies were reported in 2023.

Limited site capacity plus competing programs increases supplier bargaining power, raising risk to timelines and requiring higher site incentives and strategic partnerships.

- ~50–100 specialized US sites (2024)

- Site premiums 10–30% (2023 data)

- Competes with big pharma for investigators

- Delays add months, raise trial costs

Supplier squeeze: limited AAV capacity, dominant plasmid vendors drive high Passage costs

Suppliers—CDMOs, plasmid/reagent makers, licensors (UPenn), specialized sites and talent—hold high bargaining power for Passage Bio; 2024–25 data: global AAV clinical capacity ~200–300 batches/yr, top-5 plasmid vendors = 70–80% capacity, Passage R&D spend $137.4–145m, ~50–100 specialized US CNS sites, specialized scientist comp >$250k and +12–18% YoY.

| Category | Metric (year) |

|---|---|

| Global AAV capacity | ~200–300 batches/yr (2024) |

| Top-5 plasmid share | 70–80% (2024) |

| Passage R&D spend | $137.4–145M (2024–25) |

| Specialized US sites | ~50–100 (2024) |

| Specialist comp | >$250k; +12–18% YoY (2024) |

What is included in the product

Tailored exclusively for Passage Bio, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its market position and profitability.

A concise Passage Bio Porter's Five Forces one-sheet that highlights competitive intensity and collaboration opportunities to speed therapeutic strategy decisions and investor briefings.

Customers Bargaining Power

Concentrated payer influence on pricing

Payers—mainly Medicare, Medicaid, and large private insurers—hold strong leverage over Passage Bio because they negotiate reimbursement for therapies that can cost $1–3M per dose; in 2024 US specialty drug spend was $250B, pushing payers to demand discounts and outcomes-based contracts.

Adoption of outcome-based payment models

Value-based contracts tying payments to multi-year clinical milestones are rising; 2024 CMS pilots and several US payers now seek outcomes links in rare-disease deals, shifting reimbursement risk to manufacturers and strengthening customer bargaining power. Passage Bio faces higher negotiation pressure as payers demand performance data for GM1 and Krabbe treatments, often with payment spread over 3–5 years and potential rebates of 20–40% if targets fail. This raises cash-flow and capital needs— Passage Bio must model 5–10 year revenue deferrals and secure financing to cover up-front manufacturing and trial costs. Negotiating warranties, data rights, and stop-loss clauses will be key to keep therapies economically viable.

Influence of rare disease advocacy groups

Patient advocacy groups shape priorities and funding in rare diseases; for example, the National Organization for Rare Disorders (NORD) influenced policy that helped secure $1.1B for gene therapy R&D in 2024, steering Passage Bio toward high-impact indications.

These groups press for affordable access—campaigns have led to price negotiations cutting list prices by 20–40% in several orphan drug cases—so Passage Bio’s pricing and launch plans face strong public scrutiny.

The collective voice can sway payers and regulators; 72% of surveyed rare disease advocates in 2025 said they would actively oppose companies they view as exploitative, making advocacy alignment a commercial necessity for Passage Bio.

Limited patient populations in niche markets

- Low patient counts = high per-patient revenue impact

- Major centers control referral flows and protocols

- Loss of 10–20 patients can cut revenues by $10–60M

Governmental regulatory and health technology assessments

Government health technology assessment (HTA) bodies—like NICE in the UK and IQWiG in Germany—act as gatekeepers, assessing cost-effectiveness and can exclude therapies from public formularies; in 2024, NICE rejected or recommended use only in research for ~12% of new high-cost therapies, showing real veto power.

This creates high-stakes entry risk for Passage Bio: a negative HTA decision can block an entire national market, sharply limiting peak sales and reimbursement prospects—HTA-driven price pressure often cuts target prices by 20–50% versus list price.

- HTA vetoes affect national access

- NICE ~12% rejection rate (2024)

- Price cuts commonly 20–50%

- Market entry depends on favorable cost-benefit

Payers, HTAs & Advocacy Hold the Levers: Small Patient Shifts Risk $10–60M for Passage Bio

Payers, patient groups, centers, and HTAs wield strong leverage over Passage Bio—payers push outcomes-based deals (2024 US specialty drug spend $250B), advocacy influenced $1.1B gene therapy R&D (2024), NICE rejected ~12% high-cost therapies (2024), and losing 10–20 patients can swing $10–60M given $1–3M list prices.

| Stakeholder | Key metric |

|---|---|

| Payers | $250B specialty spend (2024) |

| Advocacy | $1.1B R&D influence (2024) |

| HTA | NICE ~12% rejection (2024) |

| Centers | Loss 10–20 pts = $10–60M |

What You See Is What You Get

Passage Bio Porter's Five Forces Analysis

This preview shows the exact Passage Bio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis file available instantly after payment.