Paysafe Porter's Five Forces Analysis

Don't Miss the Bigger Picture

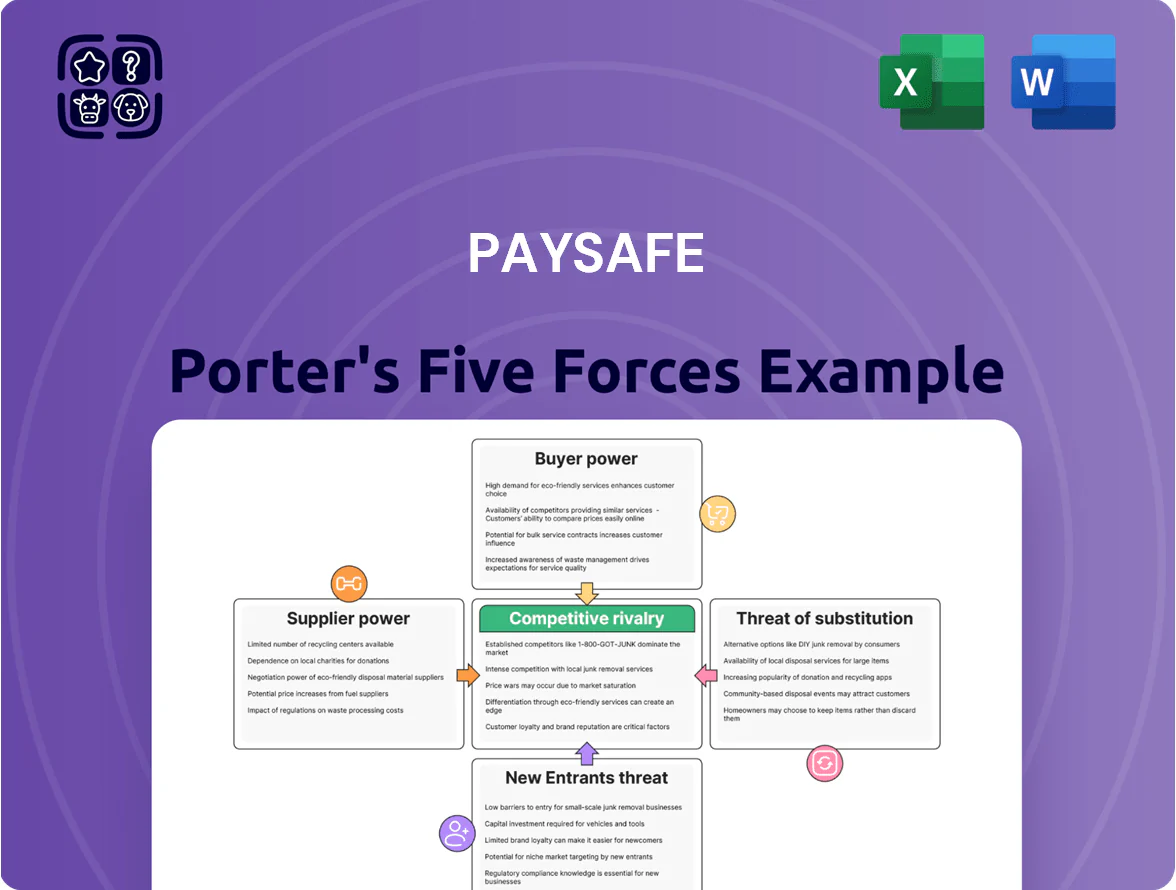

Paysafe faces moderate buyer power and strong competitive rivalry amid fast-evolving digital payments and regulatory pressure, while supplier influence and substitute threats vary by segment; barriers to entry are meaningful but lowering with fintech innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Paysafe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Global Card Networks

Paysafe depends heavily on Visa and Mastercard for card acquiring and issuing across wallets and processing, with these networks controlling interchange fees and rules that shape Paysafe’s costs; in 2024 Visa and Mastercard combined processed ~90% of global card volume, keeping supplier power high.

Reliance on Cloud Infrastructure Providers

Cloud providers like Amazon Web Services (AWS) and Microsoft Azure power Paysafe’s payments platform, hosting transaction processing and customer data; in 2024 Paysafe reported ~1.6 billion transactions, so uptime and latency matter. Switching providers would incur large technical debt and migration costs—estimates for similar firms run $50–200 million and 6–18 months—creating supplier leverage over SLAs and pricing. Still, the cloud market’s competition (AWS 33%, Azure 24% market share in 2024) limits unilateral price shocks, and multi-region, multi-cloud strategies can cap vendor power.

Banking and Liquidity Partners

Paysafe relies on dozens of correspondent banks and local partners to provide liquidity and settlement rails for Skrill and Neteller; in 2024 Paysafe reported 4.6 billion USD in digital wallet GMV, so bank access directly affects cash flow and reconciliation.

Regulatory shifts—like 2024 EU AML updates and higher capital requirements—raise compliance costs; a single large bank withdrawing services can increase cost of funds by hundreds of basis points and slow settlements.

Specialized Compliance and KYC Software

Third-party compliance and KYC software vendors are vital to Paysafe’s regulatory standing, handling identity verification and AML screening that keep its payment rails compliant.

As global AML regulations tightened in 2023–2025, KYC vendor demand rose; industry spend on identity verification hit about $8.5B in 2024, raising supplier importance.

Paysafe’s need for high-tier security gives these niche suppliers moderate bargaining power—switching costs and certification demands limit alternatives but several vetted providers exist.

- 2024 identity-verification market ≈ $8.5B

- Tightening AML laws 2023–25 increased vendor reliance

- High switching costs → moderate supplier power

- Multiple certified vendors cap supplier leverage

Competition for Specialized Fintech Talent

The fintech sector competes fiercely for engineers, cybersecurity experts, and compliance specialists; global tech hiring premiums rose 18% in 2024, making skilled labor a strong supplier of human capital.

Paysafe must match market pay—average fintech senior engineer comp in 2024 was ~$170k total comp in the US—and offer benefits to retain staff for ongoing product innovation.

High attrition raises R&D costs and delays feature rollouts; Paysafe’s hiring spend could rise 10–20% if turnover exceeds industry avg (13% in 2024).

- Specialized skills = high supplier power

- 2024 senior engineer comp ~ $170k (US)

- Tech hiring premiums +18% (2024)

- Industry turnover ~13%; +10–20% hiring cost risk

Paysafe under supplier pressure: card networks, cloud, KYC & rising tech costs

Paysafe faces moderate–high supplier power: card networks (Visa/Mastercard ~90% card volume in 2024) and cloud providers (AWS 33%, Azure 24%) set fees/SLAs; correspondent banks and KYC vendors (identity market ~$8.5B in 2024) add compliance and liquidity risks; tech talent costs rose ~18% in 2024 (senior engineer ~ $170k US), raising switching and hiring costs.

| Supplier | 2024 metric |

|---|---|

| Card networks | ~90% volume |

| Cloud | AWS 33%, Azure 24% |

| KYC market | $8.5B |

| Talent | +18% pay; $170k |

What is included in the product

Tailored Porter's Five Forces analysis for Paysafe, uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats that shape its pricing power and profitability.

Compact Porter's Five Forces summary tailored for Paysafe—one-sheet clarity to speed strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Digital Wallet Users

Individual Skrill and Neteller users can move funds to other digital wallets or bank accounts with near-zero fees and instant transfers, so switching is easy; industry data show 67% of EU e-wallet users changed providers at least once in 2024. This low switching cost forces Paysafe to keep fees competitive (Skrill average P2P fee ~0.5% in 2024) and fund generous rewards; loyalty instead hinges on use cases like online gaming and cross-border FX transfers, which account for roughly 45% of transaction volume.

High Volume Merchant Bargaining Strength

Price Sensitivity in Specialized Verticals

In specialized verticals like forex and online gambling, merchants tie revenue to transaction success rates and fees, so even a 0.5% fee gap or a 0.2% success-rate drop can move millions in volume; Paysafe saw gaming volume growth of ~18% in 2024, highlighting sensitivity to costs. Merchants commonly use multi-homing—running 2–4 gateways—to ensure redundancy and lower fees, increasing their leverage. That ease of switching raises merchant bargaining power, pressuring providers on price and uptime.

Increasing Demand for Integrated Payment Solutions

Modern merchants demand seamless integration across cards, digital wallets, BNPL, and cash-online like Paysafecard; global digital payments volume hit $8.9 trillion in 2024 (Worldpay), raising expectations for unified platforms.

As merchants push for all-in-one providers, their bargaining power rises—80% of merchants in a 2023 Juniper survey said pricing and integration drove provider switches—pressuring Paysafe to add features without raising fees.

Paysafe must keep investing in APIs, partnerships, and fee-competitive bundles; otherwise churn risk grows—merchant attrition for under-integrated providers can exceed 15% annually in fragmented markets.

- Global digital payments: $8.9T (2024)

- 80% merchants prioritize integration (Juniper, 2023)

- Merchant churn risk >15% if integration lags

- Action: invest in APIs, partnerships, bundled pricing

Availability of Alternative Payment Aggregators

The proliferation of payment aggregators and fintech startups gives SMBs more choices than ever; global fintech funding was $60.4B in 2024, fueling entrants that target niche merchants.

If Paysafe does not maintain a user-friendly interface and 24/7 support, customers can migrate to platforms like Stripe or Adyen, which processed $1.2T and $400B in 2024 transaction volume respectively.

This abundance of choice keeps bargaining power with business customers, pressuring Paysafe on fees, integrations, and service SLAs.

- Paysafe must match UI, API depth, and 24/7 support

- Stripe/Adyen scale gives pricing leverage over smaller PSPs

- SMB churn risk rises if onboarding >14 days

Paysafe at Risk: Customers’ Power and Merchant Concentration Threaten Double‑Digit Churn

Customers—both individual e-wallet users and merchants—hold strong bargaining power: 67% of EU e-wallet users switched providers in 2024, top 10 merchants can represent 20–30% of vertical revenue, and merchants commonly run 2–4 gateways. Paysafe must cut fees, offer deep APIs, 24/7 support, and bundled pricing to avoid >15% churn risk; losing a major client can shave double-digit regional revenue.

| Metric | Value (2024) |

|---|---|

| EU e-wallet switching | 67% |

| Top-10 merchant revenue share | 20–30% |

| Gaming volume growth | 18% |

| Global payments volume | $8.9T |

| Fintech funding | $60.4B |

| SMB churn risk if poor integration | >15% |

Same Document Delivered

Paysafe Porter's Five Forces Analysis

This preview shows the exact Paysafe Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the same ready-to-use analysis available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Paysafe faces moderate buyer power and strong competitive rivalry amid fast-evolving digital payments and regulatory pressure, while supplier influence and substitute threats vary by segment; barriers to entry are meaningful but lowering with fintech innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Paysafe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Global Card Networks

Paysafe depends heavily on Visa and Mastercard for card acquiring and issuing across wallets and processing, with these networks controlling interchange fees and rules that shape Paysafe’s costs; in 2024 Visa and Mastercard combined processed ~90% of global card volume, keeping supplier power high.

Reliance on Cloud Infrastructure Providers

Cloud providers like Amazon Web Services (AWS) and Microsoft Azure power Paysafe’s payments platform, hosting transaction processing and customer data; in 2024 Paysafe reported ~1.6 billion transactions, so uptime and latency matter. Switching providers would incur large technical debt and migration costs—estimates for similar firms run $50–200 million and 6–18 months—creating supplier leverage over SLAs and pricing. Still, the cloud market’s competition (AWS 33%, Azure 24% market share in 2024) limits unilateral price shocks, and multi-region, multi-cloud strategies can cap vendor power.

Banking and Liquidity Partners

Paysafe relies on dozens of correspondent banks and local partners to provide liquidity and settlement rails for Skrill and Neteller; in 2024 Paysafe reported 4.6 billion USD in digital wallet GMV, so bank access directly affects cash flow and reconciliation.

Regulatory shifts—like 2024 EU AML updates and higher capital requirements—raise compliance costs; a single large bank withdrawing services can increase cost of funds by hundreds of basis points and slow settlements.

Specialized Compliance and KYC Software

Third-party compliance and KYC software vendors are vital to Paysafe’s regulatory standing, handling identity verification and AML screening that keep its payment rails compliant.

As global AML regulations tightened in 2023–2025, KYC vendor demand rose; industry spend on identity verification hit about $8.5B in 2024, raising supplier importance.

Paysafe’s need for high-tier security gives these niche suppliers moderate bargaining power—switching costs and certification demands limit alternatives but several vetted providers exist.

- 2024 identity-verification market ≈ $8.5B

- Tightening AML laws 2023–25 increased vendor reliance

- High switching costs → moderate supplier power

- Multiple certified vendors cap supplier leverage

Competition for Specialized Fintech Talent

The fintech sector competes fiercely for engineers, cybersecurity experts, and compliance specialists; global tech hiring premiums rose 18% in 2024, making skilled labor a strong supplier of human capital.

Paysafe must match market pay—average fintech senior engineer comp in 2024 was ~$170k total comp in the US—and offer benefits to retain staff for ongoing product innovation.

High attrition raises R&D costs and delays feature rollouts; Paysafe’s hiring spend could rise 10–20% if turnover exceeds industry avg (13% in 2024).

- Specialized skills = high supplier power

- 2024 senior engineer comp ~ $170k (US)

- Tech hiring premiums +18% (2024)

- Industry turnover ~13%; +10–20% hiring cost risk

Paysafe under supplier pressure: card networks, cloud, KYC & rising tech costs

Paysafe faces moderate–high supplier power: card networks (Visa/Mastercard ~90% card volume in 2024) and cloud providers (AWS 33%, Azure 24%) set fees/SLAs; correspondent banks and KYC vendors (identity market ~$8.5B in 2024) add compliance and liquidity risks; tech talent costs rose ~18% in 2024 (senior engineer ~ $170k US), raising switching and hiring costs.

| Supplier | 2024 metric |

|---|---|

| Card networks | ~90% volume |

| Cloud | AWS 33%, Azure 24% |

| KYC market | $8.5B |

| Talent | +18% pay; $170k |

What is included in the product

Tailored Porter's Five Forces analysis for Paysafe, uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats that shape its pricing power and profitability.

Compact Porter's Five Forces summary tailored for Paysafe—one-sheet clarity to speed strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Digital Wallet Users

Individual Skrill and Neteller users can move funds to other digital wallets or bank accounts with near-zero fees and instant transfers, so switching is easy; industry data show 67% of EU e-wallet users changed providers at least once in 2024. This low switching cost forces Paysafe to keep fees competitive (Skrill average P2P fee ~0.5% in 2024) and fund generous rewards; loyalty instead hinges on use cases like online gaming and cross-border FX transfers, which account for roughly 45% of transaction volume.

High Volume Merchant Bargaining Strength

Price Sensitivity in Specialized Verticals

In specialized verticals like forex and online gambling, merchants tie revenue to transaction success rates and fees, so even a 0.5% fee gap or a 0.2% success-rate drop can move millions in volume; Paysafe saw gaming volume growth of ~18% in 2024, highlighting sensitivity to costs. Merchants commonly use multi-homing—running 2–4 gateways—to ensure redundancy and lower fees, increasing their leverage. That ease of switching raises merchant bargaining power, pressuring providers on price and uptime.

Increasing Demand for Integrated Payment Solutions

Modern merchants demand seamless integration across cards, digital wallets, BNPL, and cash-online like Paysafecard; global digital payments volume hit $8.9 trillion in 2024 (Worldpay), raising expectations for unified platforms.

As merchants push for all-in-one providers, their bargaining power rises—80% of merchants in a 2023 Juniper survey said pricing and integration drove provider switches—pressuring Paysafe to add features without raising fees.

Paysafe must keep investing in APIs, partnerships, and fee-competitive bundles; otherwise churn risk grows—merchant attrition for under-integrated providers can exceed 15% annually in fragmented markets.

- Global digital payments: $8.9T (2024)

- 80% merchants prioritize integration (Juniper, 2023)

- Merchant churn risk >15% if integration lags

- Action: invest in APIs, partnerships, bundled pricing

Availability of Alternative Payment Aggregators

The proliferation of payment aggregators and fintech startups gives SMBs more choices than ever; global fintech funding was $60.4B in 2024, fueling entrants that target niche merchants.

If Paysafe does not maintain a user-friendly interface and 24/7 support, customers can migrate to platforms like Stripe or Adyen, which processed $1.2T and $400B in 2024 transaction volume respectively.

This abundance of choice keeps bargaining power with business customers, pressuring Paysafe on fees, integrations, and service SLAs.

- Paysafe must match UI, API depth, and 24/7 support

- Stripe/Adyen scale gives pricing leverage over smaller PSPs

- SMB churn risk rises if onboarding >14 days

Paysafe at Risk: Customers’ Power and Merchant Concentration Threaten Double‑Digit Churn

Customers—both individual e-wallet users and merchants—hold strong bargaining power: 67% of EU e-wallet users switched providers in 2024, top 10 merchants can represent 20–30% of vertical revenue, and merchants commonly run 2–4 gateways. Paysafe must cut fees, offer deep APIs, 24/7 support, and bundled pricing to avoid >15% churn risk; losing a major client can shave double-digit regional revenue.

| Metric | Value (2024) |

|---|---|

| EU e-wallet switching | 67% |

| Top-10 merchant revenue share | 20–30% |

| Gaming volume growth | 18% |

| Global payments volume | $8.9T |

| Fintech funding | $60.4B |

| SMB churn risk if poor integration | >15% |

Same Document Delivered

Paysafe Porter's Five Forces Analysis

This preview shows the exact Paysafe Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're viewing the final deliverable: the same ready-to-use analysis available instantly after payment.