PDI, Inc. Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PDI, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dominance

PDI depends on hyperscalers such as AWS and Azure to host its SaaS ERP and pricing engines, making supplier power high since migrating would cost tens of millions and months of downtime; a 2024 Flexera report shows enterprises spend 32% of cloud bills on inefficiency, raising lock-in risk. By 2025 this reliance for uptime and security remains a key vulnerability for PDI, impacting SLAs and incident exposure.

Specialized Data Feed Providers

The accuracy of PDI fuel-pricing software depends on real-time data from a handful of global energy aggregators; in 2024 the top 3 providers handled roughly 70% of exchanged price feeds, giving them pricing power. These vendors can demand higher licensing fees or tighter usage terms—industry reports show feed costs rose 12–20% YoY in 2023–24—so if PDI cannot secure competitive rates, EBITDA margins on its pricing-optimization products could fall by 3–6 percentage points.

High-Skilled Software Engineering Talent

The pool of developers skilled in petroleum logistics and legacy ERP integration is small; industry estimates show niche cloud-ERP specialists command 25–40% salary premiums versus general devs as of 2025, boosting supplier leverage.

Competition from Amazon, Google, and Microsoft for these profiles gives employees and boutique recruiters strong bargaining power, raising hiring costs and time-to-fill.

Maintaining and evolving complex ERP codebases pushed PDI's labor-related expenses up an estimated 12–18% in 2024, slowing product release cadence and raising operational costs.

Cybersecurity Service Dependency

As a facilitator of critical infrastructure and financial transactions, PDI relies on high-end security audit and protection services; vendors of advanced threat-detection tools command leverage because a breach can cost oil & gas firms $5.2M average per incident (IBM 2024) and wipe years of trust.

Those vendors set pricing tiers PDI often must accept to maintain continuous PCI and NIST compliance, raising supplier bargaining power and adding predictable annual security spend pressure—top-tier managed detection can be 0.5–1.5% of revenue for comparable firms.

- High leverage: breach avg cost $5.2M (IBM 2024)

- Compliance-driven buys: PCI, NIST required

- Limited vendor substitutes for advanced detection

- Annual security spend ~0.5–1.5% revenue

Hardware Component Constraints

- Hardware shortages can delay deployments, deferring software revenue

- Embedded controller prices rose ~20% in 2024 (IHS Markit)

- Dependency on specific POS/IoT vendors concentrates supplier power

Supplier squeeze: hyperscaler lock‑in, rising feed & talent costs erode PDI margins

PDI faces high supplier power: hyperscaler lock-in (migration = tens of millions, Flexera 2024: 32% cloud inefficiency), top-3 price-feed providers ~70% share (feed costs +12–20% YoY 2023–24) and niche devs commanding 25–40% pay premium (2025). Security vendors leverage due to $5.2M breach avg (IBM 2024); managed detection = 0.5–1.5% revenue. Hardware shortages raised embedded controller prices ~20% (IHS Markit 2024), deferring installs and revenue.

| Supplier | Key stat | Impact |

|---|---|---|

| Hyperscalers | 32% cloud inefficiency (Flexera 2024) | High lock-in, costly migration |

| Price feeds | Top-3 ≈70% share; +12–20% YoY | Raises product costs, -3–6 ppt EBITDA |

| Dev talent | 25–40% salary premium (2025) | Higher Opex, slower releases |

| Security vendors | $5.2M breach avg (IBM 2024) | Must buy premium protection; 0.5–1.5% rev |

| Hardware OEMs | Embedded price +20% (IHS 2024) | Deploy delays, deferred revenue |

What is included in the product

Tailored Porter's Five Forces analysis for PDI, Inc., uncovering competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and identifying disruptive forces and strategic levers to protect market share and profitability.

Clear one-sheet Porter's Five Forces summary for PDI, Inc.—instantly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Consolidation of Large Retail Chains

Consolidation concentrates buying power: the top 5 global convenience operators run over 75,000 sites combined (2024 estimate), letting them demand double-digit discounts on software licensing and service-level terms.

PDI faces continuous pressure to deliver bespoke integrations and features—custom work that cuts margins—because losing a single chain worth tens of millions in ARR would materially affect revenue.

High Switching Costs Benefit

The integration of PDI’s ERP into retail fuel operations creates high switching friction: training, custom integrations, and synced logistics often make migration costs exceed $250k–$1M for mid-size wholesalers, per industry case studies through 2024. Once staff and supply chains are tied to PDI, technical lock-in reduces customers’ leverage at renewals, limiting bargaining power even for large chains that might otherwise demand steep concessions.

Demand for Integrated Data Analytics

Modern customers demand AI-driven predictive analytics for inventory and pricing, not just records; 72% of supply-chain leaders said predictive analytics is a top priority in a 2024 Gartner survey, pushing PDI to invest in ML models and visualization tools.

Price Sensitivity in Low-Margin Industries

- Margins <3% raise price sensitivity

- Payback 6–18 months vs upfront fees

- Fuel price volatility ~15% YoY (2024–25)

- Demand for tiered/flexible pricing rising

Independent Operator Fragmentation

Independent Operator Fragmentation reduces average customer bargaining power: while top chains (≈10% of market revenues) push hard on price, roughly 70% of fuel/convenience retailers are small independents with limited leverage as of 2024.

These smaller clients often accept PDI’s standard pricing and features, lacking scale to demand customization or deep discounts; PDI’s cloud SaaS gross margins (reported ~65% in FY2024) remain protected in this segment.

PDI can sustain higher margins by selling standardized, scalable cloud solutions that need minimal onboarding—average implementation time 30–60 days for independents—so support costs stay low.

- ~70% independents, low bargaining power

- Top chains ≈10% revenue pressure

- PDI SaaS gross margin ~65% (FY2024)

- Typical independent onboarding 30–60 days

Chains wield discounts, independents drive SaaS lock-in; AI analytics now 72% priority

Buyers split: top chains (~10% revenue) wield strong leverage, demanding double-digit discounts; independents (~70%) have low leverage and accept standard SaaS. High switching costs (training, integrations) create lock-in—migration often $250k–$1M—reducing renewal bargaining. Price sensitivity is acute (margins <3%); SaaS gross margin ~65% (FY2024). Demand for AI/predictive analytics rising (72% priority, 2024).

| Metric | Value |

|---|---|

| Top-chain market share | ≈10% |

| Independents | ≈70% |

| Migration cost | $250k–$1M |

| SaaS gross margin (FY2024) | ~65% |

| Predictive analytics priority (2024) | 72% |

Preview the Actual Deliverable

PDI, Inc. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of PDI, Inc. you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

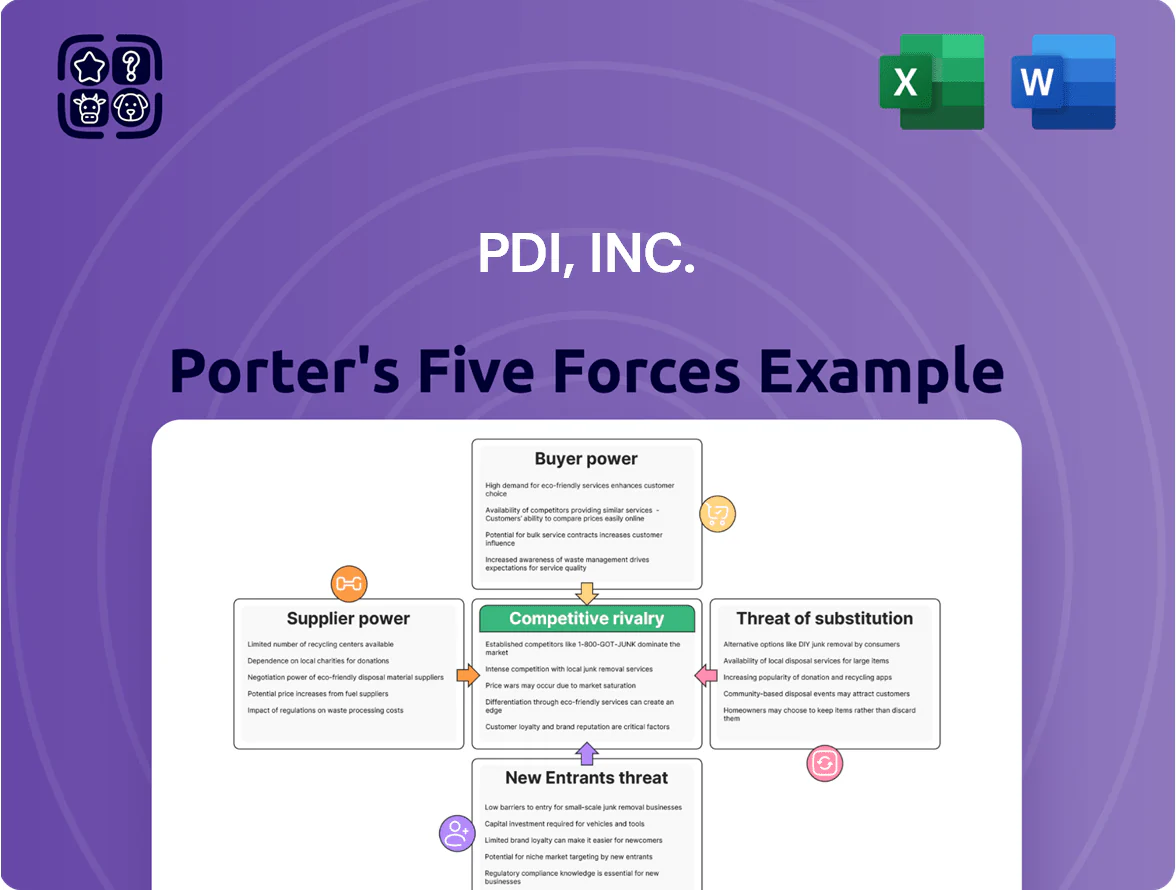

It contains a complete assessment of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry—ready for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PDI, Inc.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Dominance

PDI depends on hyperscalers such as AWS and Azure to host its SaaS ERP and pricing engines, making supplier power high since migrating would cost tens of millions and months of downtime; a 2024 Flexera report shows enterprises spend 32% of cloud bills on inefficiency, raising lock-in risk. By 2025 this reliance for uptime and security remains a key vulnerability for PDI, impacting SLAs and incident exposure.

Specialized Data Feed Providers

The accuracy of PDI fuel-pricing software depends on real-time data from a handful of global energy aggregators; in 2024 the top 3 providers handled roughly 70% of exchanged price feeds, giving them pricing power. These vendors can demand higher licensing fees or tighter usage terms—industry reports show feed costs rose 12–20% YoY in 2023–24—so if PDI cannot secure competitive rates, EBITDA margins on its pricing-optimization products could fall by 3–6 percentage points.

High-Skilled Software Engineering Talent

The pool of developers skilled in petroleum logistics and legacy ERP integration is small; industry estimates show niche cloud-ERP specialists command 25–40% salary premiums versus general devs as of 2025, boosting supplier leverage.

Competition from Amazon, Google, and Microsoft for these profiles gives employees and boutique recruiters strong bargaining power, raising hiring costs and time-to-fill.

Maintaining and evolving complex ERP codebases pushed PDI's labor-related expenses up an estimated 12–18% in 2024, slowing product release cadence and raising operational costs.

Cybersecurity Service Dependency

As a facilitator of critical infrastructure and financial transactions, PDI relies on high-end security audit and protection services; vendors of advanced threat-detection tools command leverage because a breach can cost oil & gas firms $5.2M average per incident (IBM 2024) and wipe years of trust.

Those vendors set pricing tiers PDI often must accept to maintain continuous PCI and NIST compliance, raising supplier bargaining power and adding predictable annual security spend pressure—top-tier managed detection can be 0.5–1.5% of revenue for comparable firms.

- High leverage: breach avg cost $5.2M (IBM 2024)

- Compliance-driven buys: PCI, NIST required

- Limited vendor substitutes for advanced detection

- Annual security spend ~0.5–1.5% revenue

Hardware Component Constraints

- Hardware shortages can delay deployments, deferring software revenue

- Embedded controller prices rose ~20% in 2024 (IHS Markit)

- Dependency on specific POS/IoT vendors concentrates supplier power

Supplier squeeze: hyperscaler lock‑in, rising feed & talent costs erode PDI margins

PDI faces high supplier power: hyperscaler lock-in (migration = tens of millions, Flexera 2024: 32% cloud inefficiency), top-3 price-feed providers ~70% share (feed costs +12–20% YoY 2023–24) and niche devs commanding 25–40% pay premium (2025). Security vendors leverage due to $5.2M breach avg (IBM 2024); managed detection = 0.5–1.5% revenue. Hardware shortages raised embedded controller prices ~20% (IHS Markit 2024), deferring installs and revenue.

| Supplier | Key stat | Impact |

|---|---|---|

| Hyperscalers | 32% cloud inefficiency (Flexera 2024) | High lock-in, costly migration |

| Price feeds | Top-3 ≈70% share; +12–20% YoY | Raises product costs, -3–6 ppt EBITDA |

| Dev talent | 25–40% salary premium (2025) | Higher Opex, slower releases |

| Security vendors | $5.2M breach avg (IBM 2024) | Must buy premium protection; 0.5–1.5% rev |

| Hardware OEMs | Embedded price +20% (IHS 2024) | Deploy delays, deferred revenue |

What is included in the product

Tailored Porter's Five Forces analysis for PDI, Inc., uncovering competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and identifying disruptive forces and strategic levers to protect market share and profitability.

Clear one-sheet Porter's Five Forces summary for PDI, Inc.—instantly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Consolidation of Large Retail Chains

Consolidation concentrates buying power: the top 5 global convenience operators run over 75,000 sites combined (2024 estimate), letting them demand double-digit discounts on software licensing and service-level terms.

PDI faces continuous pressure to deliver bespoke integrations and features—custom work that cuts margins—because losing a single chain worth tens of millions in ARR would materially affect revenue.

High Switching Costs Benefit

The integration of PDI’s ERP into retail fuel operations creates high switching friction: training, custom integrations, and synced logistics often make migration costs exceed $250k–$1M for mid-size wholesalers, per industry case studies through 2024. Once staff and supply chains are tied to PDI, technical lock-in reduces customers’ leverage at renewals, limiting bargaining power even for large chains that might otherwise demand steep concessions.

Demand for Integrated Data Analytics

Modern customers demand AI-driven predictive analytics for inventory and pricing, not just records; 72% of supply-chain leaders said predictive analytics is a top priority in a 2024 Gartner survey, pushing PDI to invest in ML models and visualization tools.

Price Sensitivity in Low-Margin Industries

- Margins <3% raise price sensitivity

- Payback 6–18 months vs upfront fees

- Fuel price volatility ~15% YoY (2024–25)

- Demand for tiered/flexible pricing rising

Independent Operator Fragmentation

Independent Operator Fragmentation reduces average customer bargaining power: while top chains (≈10% of market revenues) push hard on price, roughly 70% of fuel/convenience retailers are small independents with limited leverage as of 2024.

These smaller clients often accept PDI’s standard pricing and features, lacking scale to demand customization or deep discounts; PDI’s cloud SaaS gross margins (reported ~65% in FY2024) remain protected in this segment.

PDI can sustain higher margins by selling standardized, scalable cloud solutions that need minimal onboarding—average implementation time 30–60 days for independents—so support costs stay low.

- ~70% independents, low bargaining power

- Top chains ≈10% revenue pressure

- PDI SaaS gross margin ~65% (FY2024)

- Typical independent onboarding 30–60 days

Chains wield discounts, independents drive SaaS lock-in; AI analytics now 72% priority

Buyers split: top chains (~10% revenue) wield strong leverage, demanding double-digit discounts; independents (~70%) have low leverage and accept standard SaaS. High switching costs (training, integrations) create lock-in—migration often $250k–$1M—reducing renewal bargaining. Price sensitivity is acute (margins <3%); SaaS gross margin ~65% (FY2024). Demand for AI/predictive analytics rising (72% priority, 2024).

| Metric | Value |

|---|---|

| Top-chain market share | ≈10% |

| Independents | ≈70% |

| Migration cost | $250k–$1M |

| SaaS gross margin (FY2024) | ~65% |

| Predictive analytics priority (2024) | 72% |

Preview the Actual Deliverable

PDI, Inc. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of PDI, Inc. you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

It contains a complete assessment of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry—ready for immediate application.