Pebblebrook Hotel Business Model Canvas

Pebblebrook Hotels: Compact Business Model Canvas for Scaling Value in Hospitality

Unlock the full strategic blueprint behind Pebblebrook Hotel's business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue streams to show how the company scales and captures value in hospitality markets.

Partnerships

Third-Party Management Companies

Pebblebrook partners with operators including Davidson Hospitality Group, Noble House Hotels and Resorts, and Viceroy Hotels and Resorts to run daily operations, covering 70+ properties and helping sustain average RevPAR growth of ~6% in 2024. These third‑party managers deliver hands‑on operational expertise so the REIT can focus on asset management and deploy $300m+ in strategic capital allocation while keeping service standards across boutique and branded hotels.

Global Hotel Brand Franchisors

Pebblebrook holds franchise ties with Marriott, Hilton, and Hyatt, giving access to global distribution systems and loyalty networks that lifted RevPAR 2024: up 6.2% to $141.50 across the portfolio. These agreements drive occupancy—Pebblebrook reported 2024 consolidated occupancy of ~72.8%—and extend international brand recognition and marketing reach to thousands of bookings daily.

Financial Institutions and Capital Providers

Maintaining strong ties with commercial banks, institutional investors, and rating agencies is critical for securing the debt and equity capital Pebblebrook needs for acquisitions; these partners back revolving credit facilities and term loans that underpin liquidity and growth. As of late 2025, with the 10-year Treasury near 4.5% and Moody’s/S&P focus on cashflow metrics, these relationships help refinance ~$600M of maturing debt and manage cost of capital.

Construction and Design Firms

Construction and design firms execute Pebblebrook's strategic renovations and repositionings, turning underperforming assets into lifestyle hotels; recent 2024 repositionings averaged capex of $25k–$45k per key with projected RevPAR gains of 15–25% within 12–18 months.

Close coordination keeps projects on time and within budget, limiting guest-displacement revenue loss—Pebblebrook targets <90% schedule adherence and <5% budget variance on capital projects.

- Capex per key: $25k–$45k

- Target RevPAR uplift: 15–25% in 12–18 months

- Schedule adherence target: >90%

- Budget variance target: <5%

Online Travel Agency Platforms

Pebblebrook partners with Expedia Group and Booking Holdings to boost visibility and capture international and leisure demand, especially in off-peak periods when direct bookings fall; in 2024 OTA channels drove ~28% of chainwide bookings and helped lift occupancy in soft months by ~4–6 percentage points.

These partnerships carry commission rates typically of 15–25%, trading margin for market penetration in competitive urban and resort markets.

- OTA share ≈28% of bookings (2024)

- Off-peak occupancy lift ≈4–6 pp

- Typical commission 15–25%

Pebblebrook: Partner‑led repositioning boosts RevPAR to $141.50; target +15–25%

Pebblebrook leverages third‑party operators (Davidson, Noble House, Viceroy), major franchisors (Marriott, Hilton, Hyatt), OTAs (Expedia, Booking), lenders/investors, and construction partners to drive RevPAR, distribution, liquidity, and repositioning; 2024 metrics: RevPAR $141.50 (+6.2%), occupancy 72.8%, OTA share 28%, capex/key $25k–$45k, target RevPAR uplift 15–25%.

| Partner | Role | Key 2024/2025 Metric |

|---|---|---|

| Operators | Daily ops | 70+ properties |

| Franchisors | Distribution | RevPAR $141.50 (+6.2%) |

| OTAs | Demand | 28% bookings; 15–25% commission |

| Capital providers | Debt/equity | Refinance ~$600M (2025) |

| Construction | Repositioning | Capex/key $25k–$45k; +15–25% RevPAR |

What is included in the product

A concise, investor-ready Business Model Canvas for Pebblebrook focusing on upscale urban hotel ownership and asset-light management, covering customer segments, channels, value propositions, revenue streams, key partners, activities, resources, cost structure, and stakeholder insights.

High-level view of Pebblebrook Hotel Trust’s business model with editable cells — quickly pinpoint revenue drivers, asset strategies, and guest segmentation to relieve analysis bottlenecks for investors and operators.

Activities

Strategic Portfolio Asset Management

Pebblebrook runs continuous asset-level reviews to ensure each hotel meets target ROI, tracking RevPAR, EBITDA margin, and Net Promoter/guest satisfaction; in 2024 the firm cited portfolio RevPAR recovery to about 95% of 2019 levels and consolidated EBITDA margins near 35% as benchmarks. This data-driven process triggers property capex, repositioning, or operator changes to lift cash flow—typical capex per renovation ranges $5k–$45k per key depending on segment.

Capital Recycling and Disposition

Pebblebrook sells non-core hotels—25 dispositions totaling $420m in 2024—to fund buys in high-growth U.S. urban and resort markets, keeping the portfolio concentrated in upper-upscale brands.

By exiting mature assets at a 12–15% cap rate spread above acquisition targets, the firm reinvested $360m in 2024 into higher-appreciation deals aiming for 8–10% annual NOI growth.

Property Redevelopment and Repositioning

Pebblebrook’s core skill is transforming hotels to raise average daily rate (ADR) and occupancy via full renovations of rooms, lobbies, and F&B to match modern traveler tastes; recent repositionings drove ADR uplifts of 12–25% and NOI increases of 15–40% within 12–24 months.

Market Analysis and Acquisition

The executive team runs rigorous market research to find acquisition targets in major US urban and resort markets, using local GDP growth, occupancy and ADR (average daily rate) trends, and STR-reported tourism projections through 2025; in 2024 Pebblebrook targeted assets where RevPAR gains of 15–30% post-renovation were realistic based on city-level demand recovery.

- Focus: top 25 MSAs and leisure metros

- Metrics: occupancy, ADR, RevPAR, local GDP

- 2024 target uplift: 15–30% RevPAR

- Horizon: tourism projections to 2025+

- Playbook: operational + renovation value-add

Investor Relations and Financial Compliance

Pebblebrook, a publicly traded REIT (PEB, NYSE), must provide clear SEC-compliant disclosure including quarterly 10-Q/8-K filings and annual 10-Ks, host earnings calls, and present at investor conferences to sustain transparency and liquidity; in 2024 PEB paid $0.95 per share in dividends and reported FFO per share of $1.60 for the year.

- Quarterly earnings, 10-Q/8-K filings

- Annual 10-K and investor presentations

- Dividend distribution management ($0.95 in 2024)

- Conference participation to preserve stock liquidity

Pebblebrook: $420M disposals fund $360M reinvestment, targeting 15–30% RevPAR lift

Pebblebrook runs asset reviews to hit target ROI (2024: RevPAR ~95% of 2019; EBITDA margin ~35%), disposes non-core hotels (25 properties, $420m in 2024) to fund $360m reinvestment, targets 15–30% RevPAR uplift post-renovation, and paid $0.95 dividend with FFO $1.60/share in 2024.

| Metric | 2024 |

|---|---|

| RevPAR vs 2019 | ~95% |

| EBITDA margin | ~35% |

| Dispositions | 25; $420m |

| Reinvested | $360m |

| Dividend | $0.95/sh |

| FFO/share | $1.60 |

Preview Before You Purchase

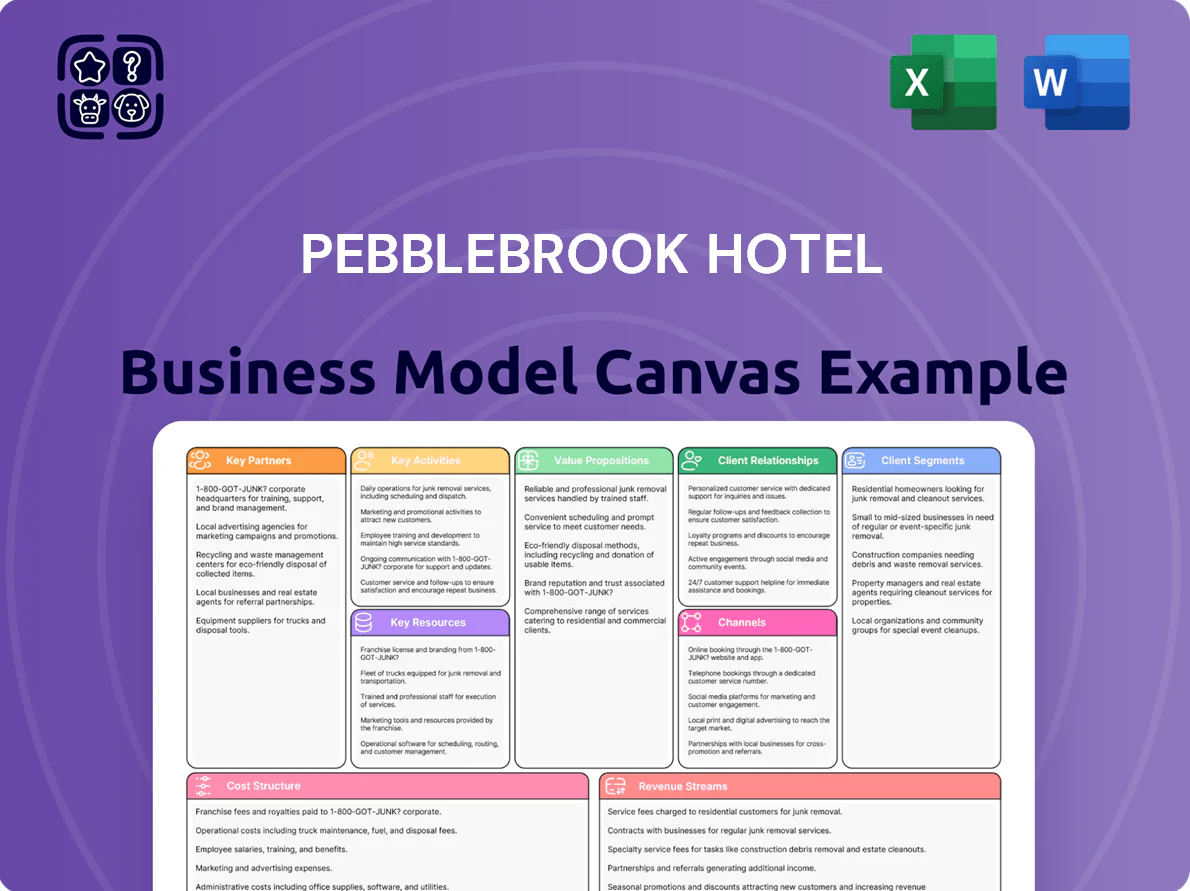

Business Model Canvas

The Pebblebrook Hotel Business Model Canvas shown here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase and includes the same structure, content, and formatting.

When you complete your order, you’ll instantly get this exact document—ready to edit, present, and use in Word and Excel formats with no hidden pages or altered layouts.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Pebblebrook Hotels: Compact Business Model Canvas for Scaling Value in Hospitality

Unlock the full strategic blueprint behind Pebblebrook Hotel's business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue streams to show how the company scales and captures value in hospitality markets.

Partnerships

Third-Party Management Companies

Pebblebrook partners with operators including Davidson Hospitality Group, Noble House Hotels and Resorts, and Viceroy Hotels and Resorts to run daily operations, covering 70+ properties and helping sustain average RevPAR growth of ~6% in 2024. These third‑party managers deliver hands‑on operational expertise so the REIT can focus on asset management and deploy $300m+ in strategic capital allocation while keeping service standards across boutique and branded hotels.

Global Hotel Brand Franchisors

Pebblebrook holds franchise ties with Marriott, Hilton, and Hyatt, giving access to global distribution systems and loyalty networks that lifted RevPAR 2024: up 6.2% to $141.50 across the portfolio. These agreements drive occupancy—Pebblebrook reported 2024 consolidated occupancy of ~72.8%—and extend international brand recognition and marketing reach to thousands of bookings daily.

Financial Institutions and Capital Providers

Maintaining strong ties with commercial banks, institutional investors, and rating agencies is critical for securing the debt and equity capital Pebblebrook needs for acquisitions; these partners back revolving credit facilities and term loans that underpin liquidity and growth. As of late 2025, with the 10-year Treasury near 4.5% and Moody’s/S&P focus on cashflow metrics, these relationships help refinance ~$600M of maturing debt and manage cost of capital.

Construction and Design Firms

Construction and design firms execute Pebblebrook's strategic renovations and repositionings, turning underperforming assets into lifestyle hotels; recent 2024 repositionings averaged capex of $25k–$45k per key with projected RevPAR gains of 15–25% within 12–18 months.

Close coordination keeps projects on time and within budget, limiting guest-displacement revenue loss—Pebblebrook targets <90% schedule adherence and <5% budget variance on capital projects.

- Capex per key: $25k–$45k

- Target RevPAR uplift: 15–25% in 12–18 months

- Schedule adherence target: >90%

- Budget variance target: <5%

Online Travel Agency Platforms

Pebblebrook partners with Expedia Group and Booking Holdings to boost visibility and capture international and leisure demand, especially in off-peak periods when direct bookings fall; in 2024 OTA channels drove ~28% of chainwide bookings and helped lift occupancy in soft months by ~4–6 percentage points.

These partnerships carry commission rates typically of 15–25%, trading margin for market penetration in competitive urban and resort markets.

- OTA share ≈28% of bookings (2024)

- Off-peak occupancy lift ≈4–6 pp

- Typical commission 15–25%

Pebblebrook: Partner‑led repositioning boosts RevPAR to $141.50; target +15–25%

Pebblebrook leverages third‑party operators (Davidson, Noble House, Viceroy), major franchisors (Marriott, Hilton, Hyatt), OTAs (Expedia, Booking), lenders/investors, and construction partners to drive RevPAR, distribution, liquidity, and repositioning; 2024 metrics: RevPAR $141.50 (+6.2%), occupancy 72.8%, OTA share 28%, capex/key $25k–$45k, target RevPAR uplift 15–25%.

| Partner | Role | Key 2024/2025 Metric |

|---|---|---|

| Operators | Daily ops | 70+ properties |

| Franchisors | Distribution | RevPAR $141.50 (+6.2%) |

| OTAs | Demand | 28% bookings; 15–25% commission |

| Capital providers | Debt/equity | Refinance ~$600M (2025) |

| Construction | Repositioning | Capex/key $25k–$45k; +15–25% RevPAR |

What is included in the product

A concise, investor-ready Business Model Canvas for Pebblebrook focusing on upscale urban hotel ownership and asset-light management, covering customer segments, channels, value propositions, revenue streams, key partners, activities, resources, cost structure, and stakeholder insights.

High-level view of Pebblebrook Hotel Trust’s business model with editable cells — quickly pinpoint revenue drivers, asset strategies, and guest segmentation to relieve analysis bottlenecks for investors and operators.

Activities

Strategic Portfolio Asset Management

Pebblebrook runs continuous asset-level reviews to ensure each hotel meets target ROI, tracking RevPAR, EBITDA margin, and Net Promoter/guest satisfaction; in 2024 the firm cited portfolio RevPAR recovery to about 95% of 2019 levels and consolidated EBITDA margins near 35% as benchmarks. This data-driven process triggers property capex, repositioning, or operator changes to lift cash flow—typical capex per renovation ranges $5k–$45k per key depending on segment.

Capital Recycling and Disposition

Pebblebrook sells non-core hotels—25 dispositions totaling $420m in 2024—to fund buys in high-growth U.S. urban and resort markets, keeping the portfolio concentrated in upper-upscale brands.

By exiting mature assets at a 12–15% cap rate spread above acquisition targets, the firm reinvested $360m in 2024 into higher-appreciation deals aiming for 8–10% annual NOI growth.

Property Redevelopment and Repositioning

Pebblebrook’s core skill is transforming hotels to raise average daily rate (ADR) and occupancy via full renovations of rooms, lobbies, and F&B to match modern traveler tastes; recent repositionings drove ADR uplifts of 12–25% and NOI increases of 15–40% within 12–24 months.

Market Analysis and Acquisition

The executive team runs rigorous market research to find acquisition targets in major US urban and resort markets, using local GDP growth, occupancy and ADR (average daily rate) trends, and STR-reported tourism projections through 2025; in 2024 Pebblebrook targeted assets where RevPAR gains of 15–30% post-renovation were realistic based on city-level demand recovery.

- Focus: top 25 MSAs and leisure metros

- Metrics: occupancy, ADR, RevPAR, local GDP

- 2024 target uplift: 15–30% RevPAR

- Horizon: tourism projections to 2025+

- Playbook: operational + renovation value-add

Investor Relations and Financial Compliance

Pebblebrook, a publicly traded REIT (PEB, NYSE), must provide clear SEC-compliant disclosure including quarterly 10-Q/8-K filings and annual 10-Ks, host earnings calls, and present at investor conferences to sustain transparency and liquidity; in 2024 PEB paid $0.95 per share in dividends and reported FFO per share of $1.60 for the year.

- Quarterly earnings, 10-Q/8-K filings

- Annual 10-K and investor presentations

- Dividend distribution management ($0.95 in 2024)

- Conference participation to preserve stock liquidity

Pebblebrook: $420M disposals fund $360M reinvestment, targeting 15–30% RevPAR lift

Pebblebrook runs asset reviews to hit target ROI (2024: RevPAR ~95% of 2019; EBITDA margin ~35%), disposes non-core hotels (25 properties, $420m in 2024) to fund $360m reinvestment, targets 15–30% RevPAR uplift post-renovation, and paid $0.95 dividend with FFO $1.60/share in 2024.

| Metric | 2024 |

|---|---|

| RevPAR vs 2019 | ~95% |

| EBITDA margin | ~35% |

| Dispositions | 25; $420m |

| Reinvested | $360m |

| Dividend | $0.95/sh |

| FFO/share | $1.60 |

Preview Before You Purchase

Business Model Canvas

The Pebblebrook Hotel Business Model Canvas shown here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase and includes the same structure, content, and formatting.

When you complete your order, you’ll instantly get this exact document—ready to edit, present, and use in Word and Excel formats with no hidden pages or altered layouts.