Pebblebrook Hotel PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how macro forces—from regulatory shifts and interest-rate cycles to changing travel trends and sustainability demands—are shaping Pebblebrook Hotel’s strategy and valuation; our concise PESTLE snapshot highlights key risks and opportunities to act on now. Purchase the full PESTLE analysis for a complete, actionable breakdown in editable formats to support investment decisions, strategic planning, or competitive benchmarking.

Political factors

Federal Reserve Monetary Policy

The Federal Reserve's rate policy through late 2025—with the federal funds rate at 5.25–5.50% as of Dec 2025 projections—directly raises Pebblebrook's borrowing costs and weighted average cost of capital.

As a hotel REIT reliant on debt for acquisitions and $600m+ annual capex trends, higher benchmarks compress dividend yield and payout flexibility.

Political pressure to hit a 2% inflation target and sustain sub-4% unemployment adds volatility to lodging demand and financing conditions.

Urban Governance and Public Safety

Political management of San Francisco, Seattle, and Portland materially affects Pebblebrook’s valuations and occupancy; San Francisco’s downtown office vacancy reached ~22% in Q4 2025, pressuring urban ADR and RevPAR recovery for Pebblebrook assets.

Local initiatives—San Francisco’s $500M safety and lighting program (2024–25) and Seattle’s $120M downtown activation grants—are critical to restoring business travel and leisure demand.

Shifts in city leadership or municipal infrastructure spending can accelerate recovery: a 10% rise in downtown foot traffic historically correlated with ~6–8% RevPAR gains for comparable urban hotels.

Geopolitical Stability and International Travel

The federal government's visa policies and diplomatic ties shape international arrivals to Pebblebrook's gateway cities; US travel bans or visa processing delays cut inbound flows—international arrivals to the US reached 39.4 million in 2023, still below 2019 levels, affecting upper-upscale occupancy and ADR.

Political stability in Europe and Asia supports high-spend leisure travel—in 2024 Asia-Pacific sourced ~30% of global outbound spend—critical for Pebblebrook's coastal and metro resorts.

Escalating trade tensions or new travel restrictions historically reduce demand: a 2019–2020 example saw US hotel RevPAR drop >50% in some markets, illustrating downside risk to coastal/metropolitan assets.

REIT Taxation and Regulatory Frameworks

Potential changes to federal tax codes affecting REIT treatment could shift institutional allocations; for context, U.S. REITs returned 2.3% YTD and yield averaged ~3.9% in 2025, so any loss of tax-advantaged status would pressure Pebblebrook’s appeal.

Ongoing political debate on corporate tax rates and dividend deductibility requires monitoring—after 2017 reforms, REIT payouts remained critical; a change could materially affect cash flow distribution policies.

Maintaining REIT tax status is essential to sustain the high yield investors expect from Pebblebrook in a competitive lodging market.

- REIT average yield ~3.9% (2025)

- U.S. REIT YTD return 2.3% (2025)

- Loss of tax advantages would materially reduce institutional demand

Government Infrastructure and Tourism Support

Federal and state funding for airport expansions and convention center upgrades—US DOT allocated $20.5 billion in 2024 for airport infrastructure and states committed over $6.8 billion to convention facility projects—serve as long-term growth levers for Pebblebrook by improving market connectivity and group demand.

Political decisions to host major events like the 2026 World Cup require public-private coordination and infrastructure readiness, driving near-term occupancy spikes and higher ADR in host markets where Pebblebrook has assets.

These government-led investments enhance accessibility and global appeal in Pebblebrook markets, supporting RevPAR upside; SLOT: recent studies estimate a 5–12% RevPAR lift in cities receiving major infrastructure upgrades.

- 2024 US DOT airport funding $20.5B

- State convention investments $6.8B+

- 2026 World Cup—occupancy/ADR spikes in host cities

- Estimated 5–12% RevPAR uplift from major upgrades

Rising Fed Rates Elevate Pebblebrook Costs as US Airport Funding Bolsters Recovery

Political factors: higher Fed rates (fed funds 5.25–5.50% projected 2025) raise Pebblebrook’s WACC and borrowing costs; municipal safety/activation funds (SF $500M, Seattle $120M) and $20.5B US DOT airport funding support demand recovery; REIT yield ~3.9% (2025) and tax/status changes pose material allocation risk; visa/political stability affect international arrivals (~39.4M in 2023).

| Metric | Value |

|---|---|

| Fed funds (proj 2025) | 5.25–5.50% |

| REIT yield (2025) | ~3.9% |

| US intl arrivals (2023) | 39.4M |

What is included in the product

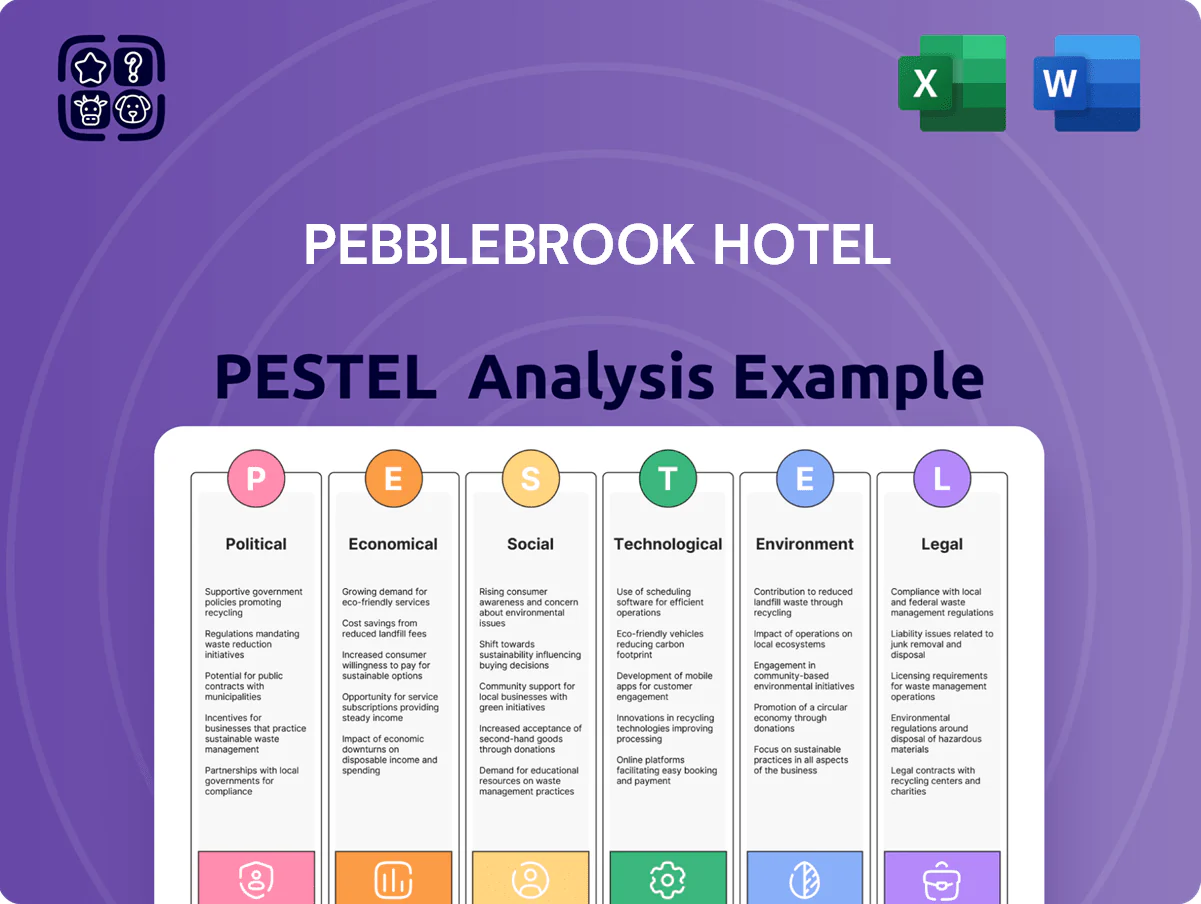

Explores how external macro-environmental factors uniquely affect Pebblebrook Hotel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists.

A concise, shareable Pebblebrook Hotel PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or strategy packs, and editable for region- or business-specific notes to streamline planning and risk discussions.

Economic factors

Discretionary Spending in the Upper Upscale Segment

By end-2025, high-income consumers drive Pebblebrook’s revenue—upper upscale ADRs rose ~6.2% YTD through Q3 2025 versus 2019 levels, reflecting resilient discretionary spending among top 20% earners.

Focus on luxury/lifestyle hotels targets travelers with higher disposable income; luxury RevPAR outperformed total US RevPAR by ~8 percentage points in 2024–2025.

Broader economic headwinds persist: IMF projected 2025 global growth ~3.0%, and a sharp corporate profit downturn could cut high-end business travel and group bookings, lowering occupancy and group ADRs.

Labor Market Dynamics and Wage Inflation

The hospitality sector faces tight labor supply, with U.S. leisure and hospitality employment still about 2.0 million below pre‑pandemic peak as of Dec 2025, pushing Pebblebrook to absorb rising payroll and benefit costs—wage growth for service workers averaged ~5.1% YoY in 2024–25. Pebblebrook must drive operational efficiencies (automation, labor scheduling) to protect margins while preserving guest service standards. Higher minimum wages in key markets and elevated turnover increase labor-related operating expenses and capital allocation decisions.

Real Estate Capital Markets and Cap Rates

Pebblebrook's asset valuations move with commercial cap rates; US hotel cap rates averaged about 7.0% in 2024 versus 6.2% in 2021, compressing or expanding NAV materially.

Rising rates and softer ADR trends reduced appraisals in 2024, hampering Pebblebrook's ability to recycle capital via sales—2024 dispositions slowed versus 2021–23 levels.

Investors track cap-rate shifts and NOI trends; a 50–100 bps cap-rate swing can change portfolio value by double-digit percentages, directly affecting REIT share valuation.

Inflationary Impact on Operating Expenses

Persistent inflation in utilities, F&B supplies, and maintenance has compressed Pebblebrook’s property-level NOI; US CPI for food rose 3.4% year-over-year in Jan 2026 and energy costs averaged up 8% in 2025, increasing operating spend across the portfolio.

Pebblebrook leverages scale to secure vendor discounts—management reported procurement savings of roughly 2–4% in 2024—but secular input-cost inflation remains a headwind to margins.

Revenue management is essential to shift costs to guests via ADR: Pebblebrook’s ADR rose ~10% in 2024 versus 2019, but further strategic pricing and channel mix optimization are needed to sustain NOI.

- Utility/F&B/maintenance inflation up materially in 2024–25

- Procurement scale yielded ~2–4% savings

- ADR growth (~10% vs 2019) used to offset costs

- Ongoing need for dynamic revenue management

Business Travel and Group Booking Recovery

Pebblebrook is shifting focus as hybrid work reshapes corporate travel volume and seasonality, prioritizing smaller, high-margin executive retreats and boutique conferences over large conventions.

In 2024 US corporate travel spend reached about $85 billion, still roughly 15-20% below 2019 levels in major urban markets, making the pace of budget normalization a critical variable for Pebblebrook’s 2026 revenue mix.

Targeting premium group offerings improves RevPAR resilience—Pebblebrook reported urban RevPAR recovery of ~90% of 2019 in 2024—but full convention demand recovery timing remains uncertain.

- Smaller, higher-margin groups prioritized

- 2024 corporate travel ~$85B US; major cities −15–20% vs 2019

- Urban RevPAR ~90% of 2019 in 2024

Affluent ADR lifts hotels but rising wages, energy and cap rates squeeze returns

Economic tailwinds: affluent demand drove ADR +10% vs 2019 and upper-upscale ADR +6.2% YTD Q3 2025; 2024–25 wage growth ~5.1% and utilities/energy +8% (2025) squeezed NOI; US hotel cap rates ~7.0% (2024) vs 6.2% (2021) impacting NAV; 2024 US corporate travel ~$85B (−15–20% vs 2019), urban RevPAR ~90% of 2019.

| Metric | Value |

|---|---|

| ADR vs 2019 | +10% |

| Upper-upscale ADR | +6.2% YTD Q3 2025 |

| Wage growth | ~5.1% |

| Energy costs (2025) | +8% |

| US hotel cap rate (2024) | ~7.0% |

| US corporate travel (2024) | $85B (−15–20% vs 2019) |

Preview the Actual Deliverable

Pebblebrook Hotel PESTLE Analysis

The preview shown here is the exact Pebblebrook Hotel PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how macro forces—from regulatory shifts and interest-rate cycles to changing travel trends and sustainability demands—are shaping Pebblebrook Hotel’s strategy and valuation; our concise PESTLE snapshot highlights key risks and opportunities to act on now. Purchase the full PESTLE analysis for a complete, actionable breakdown in editable formats to support investment decisions, strategic planning, or competitive benchmarking.

Political factors

Federal Reserve Monetary Policy

The Federal Reserve's rate policy through late 2025—with the federal funds rate at 5.25–5.50% as of Dec 2025 projections—directly raises Pebblebrook's borrowing costs and weighted average cost of capital.

As a hotel REIT reliant on debt for acquisitions and $600m+ annual capex trends, higher benchmarks compress dividend yield and payout flexibility.

Political pressure to hit a 2% inflation target and sustain sub-4% unemployment adds volatility to lodging demand and financing conditions.

Urban Governance and Public Safety

Political management of San Francisco, Seattle, and Portland materially affects Pebblebrook’s valuations and occupancy; San Francisco’s downtown office vacancy reached ~22% in Q4 2025, pressuring urban ADR and RevPAR recovery for Pebblebrook assets.

Local initiatives—San Francisco’s $500M safety and lighting program (2024–25) and Seattle’s $120M downtown activation grants—are critical to restoring business travel and leisure demand.

Shifts in city leadership or municipal infrastructure spending can accelerate recovery: a 10% rise in downtown foot traffic historically correlated with ~6–8% RevPAR gains for comparable urban hotels.

Geopolitical Stability and International Travel

The federal government's visa policies and diplomatic ties shape international arrivals to Pebblebrook's gateway cities; US travel bans or visa processing delays cut inbound flows—international arrivals to the US reached 39.4 million in 2023, still below 2019 levels, affecting upper-upscale occupancy and ADR.

Political stability in Europe and Asia supports high-spend leisure travel—in 2024 Asia-Pacific sourced ~30% of global outbound spend—critical for Pebblebrook's coastal and metro resorts.

Escalating trade tensions or new travel restrictions historically reduce demand: a 2019–2020 example saw US hotel RevPAR drop >50% in some markets, illustrating downside risk to coastal/metropolitan assets.

REIT Taxation and Regulatory Frameworks

Potential changes to federal tax codes affecting REIT treatment could shift institutional allocations; for context, U.S. REITs returned 2.3% YTD and yield averaged ~3.9% in 2025, so any loss of tax-advantaged status would pressure Pebblebrook’s appeal.

Ongoing political debate on corporate tax rates and dividend deductibility requires monitoring—after 2017 reforms, REIT payouts remained critical; a change could materially affect cash flow distribution policies.

Maintaining REIT tax status is essential to sustain the high yield investors expect from Pebblebrook in a competitive lodging market.

- REIT average yield ~3.9% (2025)

- U.S. REIT YTD return 2.3% (2025)

- Loss of tax advantages would materially reduce institutional demand

Government Infrastructure and Tourism Support

Federal and state funding for airport expansions and convention center upgrades—US DOT allocated $20.5 billion in 2024 for airport infrastructure and states committed over $6.8 billion to convention facility projects—serve as long-term growth levers for Pebblebrook by improving market connectivity and group demand.

Political decisions to host major events like the 2026 World Cup require public-private coordination and infrastructure readiness, driving near-term occupancy spikes and higher ADR in host markets where Pebblebrook has assets.

These government-led investments enhance accessibility and global appeal in Pebblebrook markets, supporting RevPAR upside; SLOT: recent studies estimate a 5–12% RevPAR lift in cities receiving major infrastructure upgrades.

- 2024 US DOT airport funding $20.5B

- State convention investments $6.8B+

- 2026 World Cup—occupancy/ADR spikes in host cities

- Estimated 5–12% RevPAR uplift from major upgrades

Rising Fed Rates Elevate Pebblebrook Costs as US Airport Funding Bolsters Recovery

Political factors: higher Fed rates (fed funds 5.25–5.50% projected 2025) raise Pebblebrook’s WACC and borrowing costs; municipal safety/activation funds (SF $500M, Seattle $120M) and $20.5B US DOT airport funding support demand recovery; REIT yield ~3.9% (2025) and tax/status changes pose material allocation risk; visa/political stability affect international arrivals (~39.4M in 2023).

| Metric | Value |

|---|---|

| Fed funds (proj 2025) | 5.25–5.50% |

| REIT yield (2025) | ~3.9% |

| US intl arrivals (2023) | 39.4M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Pebblebrook Hotel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists.

A concise, shareable Pebblebrook Hotel PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or strategy packs, and editable for region- or business-specific notes to streamline planning and risk discussions.

Economic factors

Discretionary Spending in the Upper Upscale Segment

By end-2025, high-income consumers drive Pebblebrook’s revenue—upper upscale ADRs rose ~6.2% YTD through Q3 2025 versus 2019 levels, reflecting resilient discretionary spending among top 20% earners.

Focus on luxury/lifestyle hotels targets travelers with higher disposable income; luxury RevPAR outperformed total US RevPAR by ~8 percentage points in 2024–2025.

Broader economic headwinds persist: IMF projected 2025 global growth ~3.0%, and a sharp corporate profit downturn could cut high-end business travel and group bookings, lowering occupancy and group ADRs.

Labor Market Dynamics and Wage Inflation

The hospitality sector faces tight labor supply, with U.S. leisure and hospitality employment still about 2.0 million below pre‑pandemic peak as of Dec 2025, pushing Pebblebrook to absorb rising payroll and benefit costs—wage growth for service workers averaged ~5.1% YoY in 2024–25. Pebblebrook must drive operational efficiencies (automation, labor scheduling) to protect margins while preserving guest service standards. Higher minimum wages in key markets and elevated turnover increase labor-related operating expenses and capital allocation decisions.

Real Estate Capital Markets and Cap Rates

Pebblebrook's asset valuations move with commercial cap rates; US hotel cap rates averaged about 7.0% in 2024 versus 6.2% in 2021, compressing or expanding NAV materially.

Rising rates and softer ADR trends reduced appraisals in 2024, hampering Pebblebrook's ability to recycle capital via sales—2024 dispositions slowed versus 2021–23 levels.

Investors track cap-rate shifts and NOI trends; a 50–100 bps cap-rate swing can change portfolio value by double-digit percentages, directly affecting REIT share valuation.

Inflationary Impact on Operating Expenses

Persistent inflation in utilities, F&B supplies, and maintenance has compressed Pebblebrook’s property-level NOI; US CPI for food rose 3.4% year-over-year in Jan 2026 and energy costs averaged up 8% in 2025, increasing operating spend across the portfolio.

Pebblebrook leverages scale to secure vendor discounts—management reported procurement savings of roughly 2–4% in 2024—but secular input-cost inflation remains a headwind to margins.

Revenue management is essential to shift costs to guests via ADR: Pebblebrook’s ADR rose ~10% in 2024 versus 2019, but further strategic pricing and channel mix optimization are needed to sustain NOI.

- Utility/F&B/maintenance inflation up materially in 2024–25

- Procurement scale yielded ~2–4% savings

- ADR growth (~10% vs 2019) used to offset costs

- Ongoing need for dynamic revenue management

Business Travel and Group Booking Recovery

Pebblebrook is shifting focus as hybrid work reshapes corporate travel volume and seasonality, prioritizing smaller, high-margin executive retreats and boutique conferences over large conventions.

In 2024 US corporate travel spend reached about $85 billion, still roughly 15-20% below 2019 levels in major urban markets, making the pace of budget normalization a critical variable for Pebblebrook’s 2026 revenue mix.

Targeting premium group offerings improves RevPAR resilience—Pebblebrook reported urban RevPAR recovery of ~90% of 2019 in 2024—but full convention demand recovery timing remains uncertain.

- Smaller, higher-margin groups prioritized

- 2024 corporate travel ~$85B US; major cities −15–20% vs 2019

- Urban RevPAR ~90% of 2019 in 2024

Affluent ADR lifts hotels but rising wages, energy and cap rates squeeze returns

Economic tailwinds: affluent demand drove ADR +10% vs 2019 and upper-upscale ADR +6.2% YTD Q3 2025; 2024–25 wage growth ~5.1% and utilities/energy +8% (2025) squeezed NOI; US hotel cap rates ~7.0% (2024) vs 6.2% (2021) impacting NAV; 2024 US corporate travel ~$85B (−15–20% vs 2019), urban RevPAR ~90% of 2019.

| Metric | Value |

|---|---|

| ADR vs 2019 | +10% |

| Upper-upscale ADR | +6.2% YTD Q3 2025 |

| Wage growth | ~5.1% |

| Energy costs (2025) | +8% |

| US hotel cap rate (2024) | ~7.0% |

| US corporate travel (2024) | $85B (−15–20% vs 2019) |

Preview the Actual Deliverable

Pebblebrook Hotel PESTLE Analysis

The preview shown here is the exact Pebblebrook Hotel PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.