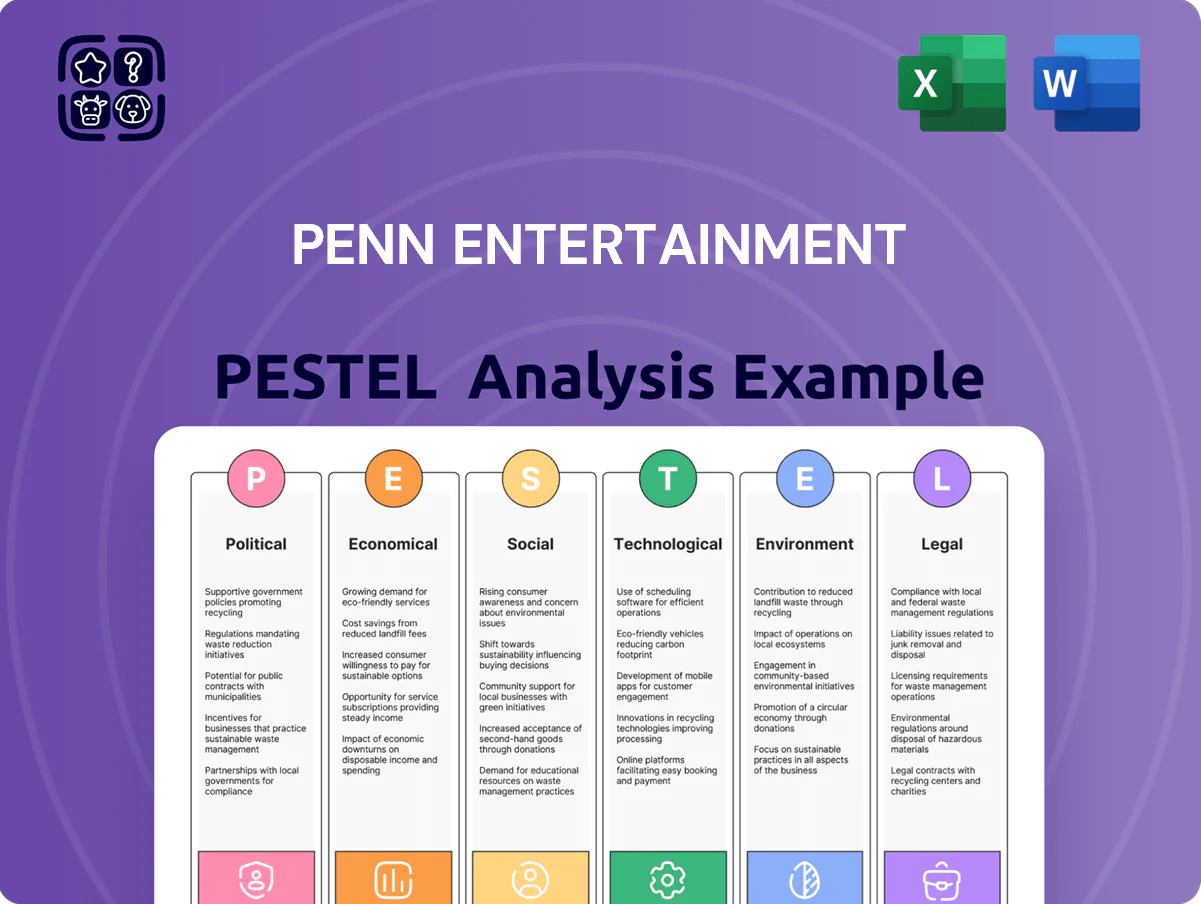

PENN Entertainment PESTLE Analysis

Skip the Research. Get the Strategy.

Navigate regulatory shifts, digital disruption, and shifting consumer preferences with our focused PESTLE snapshot for PENN Entertainment—designed to reveal the external forces shaping strategy and valuation; buy the full PESTLE to unlock detailed risk assessments, scenario-driven insights, and practical recommendations you can use now.

Political factors

State legalization of online betting

The continued rollout of sports betting and iCasino laws across North America directly dictates PENN Entertainment’s addressable market; as of 2025, 38 US states have authorized sports wagering and 8 allow online casinos, shaping PENN’s expansion opportunities. Growing state interest in new tax revenue has led to tax rates ranging from low single digits to over 30% of gross gaming revenue, materially affecting EBITDA margins. Political shifts toward legalization—including recent approvals in Ohio (2023) and Maryland (2024)—offer significant upside, while conservative reversals or stricter taxation in key markets could stall topline growth and capex deployment.

Federal oversight and excise taxes

PENN faces federal scrutiny over interstate gaming and SEC financial reporting; in 2025 the company reported $5.9bn revenue and $441m adjusted EBITDA, metrics closely watched by regulators for compliance.

Proposals to raise federal excise taxes on wagering from 0.25% to 1.0% would cut ESPN BET margins materially; a 0.75ppt increase could reduce platform EBIT by roughly $50–$150m annually based on 2024 US handle trends.

Maintaining constructive ties with federal agencies is crucial to prevent policy that would place digital gaming at a tax disadvantage versus streaming and sports media, protecting PENN’s competitive economics.

Disney and ESPN partnership dynamics

The long-term ESPN branding agreement ties PENN to Disney's political exposure, meaning controversies like Disney's 2023 Florida disputes or potential regulatory scrutiny could spill over to PENN’s reputation and licensing; Disney reported $82.7B revenue in FY2023, underscoring its influence. PENN must align strategy with its media partner’s evolving political sway to protect market access and retain brand equity amid regulatory shifts.

Lobbying for iCasino expansion

PENN intensifies lobbying for iCasino legalization, citing higher gross margins—online casino gross margin can exceed 30% vs ~10–15% for sports betting—aiming to replicate stakes in states like New Jersey where online gaming generated $4.5B in GGR in 2023.

Success hinges on convincing legislators of tax revenue gains and built-in consumer protections; PENN reported $1.1B lobbying/advocacy-related public policy engagement in filings through 2024–2025 initiatives.

Key barrier: political opposition from land-based operators and anti-gambling groups, which slowed iCasino bills in several states despite projected state tax receipts of $500M–$1B annually in early-adopter markets.

- PENN lobbying focus: higher-margin iCasino expansion

- Comparable data: NJ iCasino GGR $4.5B (2023)

- Company disclosures: significant advocacy spend through 2024–25

- Main hurdle: resistance from land operators and anti-gambling groups

Regulatory stability in retail markets

Regulatory stability in states hosting PENN Entertainment's 43 casinos is critical: state policy shifts can alter expected cash flows for property-level EBITDA, with Pennsylvania and Michigan contributing ~35% of FY2024 revenue of $5.9B, so zoning, smoking bans or tax hikes materially affect valuations.

PENN must sustain local engagement and political ties—legal and community relations budgets and lobbying (PENN spent ~$12M on selling, general and administrative lobbying-related activities in 2024) reduce risk of adverse policy changes that could impair operational efficiency.

- 43 casinos across states; FY2024 revenue $5.9B

- Pennsylvania + Michigan ≈35% of revenue

- Smoking/zoning/tax shifts can compress property EBITDA multiples

- Lobbying/community spend (~$12M in 2024) mitigates local-policy risk

PENN's expansion vs. rising taxes, regs and PA/MI concentration threaten margins

Political factors: legalization expansion (38 states sports betting, 8 iCasino by 2025) drives PENN’s TAM and capex; state tax rates vary widely (low single digits to >30% GGR) impacting EBITDA; federal proposals (excise to 1.0%) and SEC scrutiny threaten margins and compliance; ESPN tie to Disney and local policy shifts in PA/MI (~35% FY2024 revenue) create reputational and cash-flow risks.

| Metric | Value |

|---|---|

| US states legal sports betting (2025) | 38 |

| States allow iCasino (2025) | 8 |

| FY2024 revenue | $5.9B |

| PA+MI share FY2024 | ~35% |

| PENN 2024 lobbying spend | ~$12M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact PENN Entertainment, using current market and regulatory trends to identify risks, opportunities, and strategic implications for executives and investors.

A concise, PESTLE-organized summary of PENN Entertainment that can be dropped into presentations or shared across teams to streamline external risk assessment and market-positioning discussions.

Economic factors

Consumer discretionary spending trends

PENN’s retail and digital revenue is highly tied to disposable income; US real disposable personal income fell 0.2% month-over-month in Dec 2025, which can pressure casino visitation and online wagering. During high inflation—US CPI 3.4% year-over-year in 2025—leisure budgets shrink, and PENN’s Q4 2025 same-store gaming revenue growth slowed to low single digits. Tracking wage growth (average hourly earnings up 3.6% YoY in 2025) and the Conference Board consumer confidence index (102 in Dec 2025) helps forecast betting volumes and retail foot traffic across PENN’s ecosystem.

Interest rates and debt servicing

PENN carries roughly $7.5 billion of net debt as of FY2025, largely from acquisitions and development; a 100 bps rise in interest rates would increase annual interest expense materially and pressure free cash flow. Fluctuating rates raise refinancing risk for near-term maturities, with about $1.2 billion of debt due within three years, constraining flexibility. Management must temper acquisitive growth with disciplined leverage targets to maintain covenant compliance and liquidity under monetary tightening.

Cost of customer acquisition

The digital gaming market demands heavy marketing spend; industry CAC rose ~18% in 2023-24, with top operators spending $200–$400+ per deposited user, pressuring margins for ESPN BET.

Advertising market inflation and CPM increases—up ~20% YoY in 2024—raise media-placement costs, squeezing profitability for sportsbook brands reliant on paid acquisition.

PENN leverages ESPN’s organic reach—ESPN’s digital network delivered ~150M monthly unique visitors in 2024—to lower CAC versus peers, aiming for a more sustainable unit economics for ESPN BET.

Regional economic health

Many of PENN's retail casinos sit in regional markets tied to local employment; U.S. regional unemployment averaged 3.6% in 2024, so dips in hiring can cut discretionary gaming spend.

Sector-specific downturns—2024 U.S. manufacturing output fell 0.3% Y/Y in some Midwestern states—can disproportionately lower foot traffic and gaming revenue at nearby properties.

Diversification across 40+ properties in 18 states helps PENN hedge localized shocks; in 2024 regional markets accounted for roughly 65% of consolidated adjusted property EBITDA.

- 2024 U.S. unemployment 3.6% — impacts discretionary spend

- Manufacturing output down 0.3% Y/Y in parts of Midwest (2024)

- 40+ properties, 18 states; ~65% of adjusted property EBITDA from regional markets (2024)

Market saturation and competition

The rapid expansion of the North American gaming market has intensified competition for a finite pool of consumer dollars, with commercial gaming revenue in the U.S. reaching about $64.5 billion in 2023 and growing ~4% in 2024, pressuring margins as new entrants and online operators expand market share.

Economic pressure stems from new players and aggressive pricing, forcing PENN to invest in product innovation and loyalty offers; PENN reported Q3 2025 adjusted EBITDA of $429 million, highlighting the need to protect pricing power and retention amid crowding.

- U.S. gaming revenue ~64.5B (2023); ~4% growth in 2024

- PENN Q3 2025 adjusted EBITDA $429M

- Competition from online entrants and regional expansions compresses margins

- Continuous innovation and loyalty investments required to sustain market share

PENN faces income-squeeze and refinancing risk as visitation and debt pressures rise

PENN’s revenue sensitive to disposable income—US real DPI -0.2% MoM Dec 2025; CPI 3.4% YoY (2025) and AHE +3.6% YoY affect visitation. Net debt ~$7.5B (FY2025) with ~$1.2B maturities next 3 years raises refinancing risk. U.S. gaming revenue ~$64.5B (2023), ~4% growth in 2024; Q3 2025 adj. EBITDA $429M; ESPN digital reach ~150M monthly (2024).

| Metric | Value |

|---|---|

| Net debt FY2025 | $7.5B |

| Near-term maturities | $1.2B |

| US DPI change Dec 2025 | -0.2% MoM |

| CPI 2025 | 3.4% YoY |

| Q3 2025 EBITDA | $429M |

Full Version Awaits

PENN Entertainment PESTLE Analysis

The preview shown here is the exact PENN Entertainment PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Navigate regulatory shifts, digital disruption, and shifting consumer preferences with our focused PESTLE snapshot for PENN Entertainment—designed to reveal the external forces shaping strategy and valuation; buy the full PESTLE to unlock detailed risk assessments, scenario-driven insights, and practical recommendations you can use now.

Political factors

State legalization of online betting

The continued rollout of sports betting and iCasino laws across North America directly dictates PENN Entertainment’s addressable market; as of 2025, 38 US states have authorized sports wagering and 8 allow online casinos, shaping PENN’s expansion opportunities. Growing state interest in new tax revenue has led to tax rates ranging from low single digits to over 30% of gross gaming revenue, materially affecting EBITDA margins. Political shifts toward legalization—including recent approvals in Ohio (2023) and Maryland (2024)—offer significant upside, while conservative reversals or stricter taxation in key markets could stall topline growth and capex deployment.

Federal oversight and excise taxes

PENN faces federal scrutiny over interstate gaming and SEC financial reporting; in 2025 the company reported $5.9bn revenue and $441m adjusted EBITDA, metrics closely watched by regulators for compliance.

Proposals to raise federal excise taxes on wagering from 0.25% to 1.0% would cut ESPN BET margins materially; a 0.75ppt increase could reduce platform EBIT by roughly $50–$150m annually based on 2024 US handle trends.

Maintaining constructive ties with federal agencies is crucial to prevent policy that would place digital gaming at a tax disadvantage versus streaming and sports media, protecting PENN’s competitive economics.

Disney and ESPN partnership dynamics

The long-term ESPN branding agreement ties PENN to Disney's political exposure, meaning controversies like Disney's 2023 Florida disputes or potential regulatory scrutiny could spill over to PENN’s reputation and licensing; Disney reported $82.7B revenue in FY2023, underscoring its influence. PENN must align strategy with its media partner’s evolving political sway to protect market access and retain brand equity amid regulatory shifts.

Lobbying for iCasino expansion

PENN intensifies lobbying for iCasino legalization, citing higher gross margins—online casino gross margin can exceed 30% vs ~10–15% for sports betting—aiming to replicate stakes in states like New Jersey where online gaming generated $4.5B in GGR in 2023.

Success hinges on convincing legislators of tax revenue gains and built-in consumer protections; PENN reported $1.1B lobbying/advocacy-related public policy engagement in filings through 2024–2025 initiatives.

Key barrier: political opposition from land-based operators and anti-gambling groups, which slowed iCasino bills in several states despite projected state tax receipts of $500M–$1B annually in early-adopter markets.

- PENN lobbying focus: higher-margin iCasino expansion

- Comparable data: NJ iCasino GGR $4.5B (2023)

- Company disclosures: significant advocacy spend through 2024–25

- Main hurdle: resistance from land operators and anti-gambling groups

Regulatory stability in retail markets

Regulatory stability in states hosting PENN Entertainment's 43 casinos is critical: state policy shifts can alter expected cash flows for property-level EBITDA, with Pennsylvania and Michigan contributing ~35% of FY2024 revenue of $5.9B, so zoning, smoking bans or tax hikes materially affect valuations.

PENN must sustain local engagement and political ties—legal and community relations budgets and lobbying (PENN spent ~$12M on selling, general and administrative lobbying-related activities in 2024) reduce risk of adverse policy changes that could impair operational efficiency.

- 43 casinos across states; FY2024 revenue $5.9B

- Pennsylvania + Michigan ≈35% of revenue

- Smoking/zoning/tax shifts can compress property EBITDA multiples

- Lobbying/community spend (~$12M in 2024) mitigates local-policy risk

PENN's expansion vs. rising taxes, regs and PA/MI concentration threaten margins

Political factors: legalization expansion (38 states sports betting, 8 iCasino by 2025) drives PENN’s TAM and capex; state tax rates vary widely (low single digits to >30% GGR) impacting EBITDA; federal proposals (excise to 1.0%) and SEC scrutiny threaten margins and compliance; ESPN tie to Disney and local policy shifts in PA/MI (~35% FY2024 revenue) create reputational and cash-flow risks.

| Metric | Value |

|---|---|

| US states legal sports betting (2025) | 38 |

| States allow iCasino (2025) | 8 |

| FY2024 revenue | $5.9B |

| PA+MI share FY2024 | ~35% |

| PENN 2024 lobbying spend | ~$12M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact PENN Entertainment, using current market and regulatory trends to identify risks, opportunities, and strategic implications for executives and investors.

A concise, PESTLE-organized summary of PENN Entertainment that can be dropped into presentations or shared across teams to streamline external risk assessment and market-positioning discussions.

Economic factors

Consumer discretionary spending trends

PENN’s retail and digital revenue is highly tied to disposable income; US real disposable personal income fell 0.2% month-over-month in Dec 2025, which can pressure casino visitation and online wagering. During high inflation—US CPI 3.4% year-over-year in 2025—leisure budgets shrink, and PENN’s Q4 2025 same-store gaming revenue growth slowed to low single digits. Tracking wage growth (average hourly earnings up 3.6% YoY in 2025) and the Conference Board consumer confidence index (102 in Dec 2025) helps forecast betting volumes and retail foot traffic across PENN’s ecosystem.

Interest rates and debt servicing

PENN carries roughly $7.5 billion of net debt as of FY2025, largely from acquisitions and development; a 100 bps rise in interest rates would increase annual interest expense materially and pressure free cash flow. Fluctuating rates raise refinancing risk for near-term maturities, with about $1.2 billion of debt due within three years, constraining flexibility. Management must temper acquisitive growth with disciplined leverage targets to maintain covenant compliance and liquidity under monetary tightening.

Cost of customer acquisition

The digital gaming market demands heavy marketing spend; industry CAC rose ~18% in 2023-24, with top operators spending $200–$400+ per deposited user, pressuring margins for ESPN BET.

Advertising market inflation and CPM increases—up ~20% YoY in 2024—raise media-placement costs, squeezing profitability for sportsbook brands reliant on paid acquisition.

PENN leverages ESPN’s organic reach—ESPN’s digital network delivered ~150M monthly unique visitors in 2024—to lower CAC versus peers, aiming for a more sustainable unit economics for ESPN BET.

Regional economic health

Many of PENN's retail casinos sit in regional markets tied to local employment; U.S. regional unemployment averaged 3.6% in 2024, so dips in hiring can cut discretionary gaming spend.

Sector-specific downturns—2024 U.S. manufacturing output fell 0.3% Y/Y in some Midwestern states—can disproportionately lower foot traffic and gaming revenue at nearby properties.

Diversification across 40+ properties in 18 states helps PENN hedge localized shocks; in 2024 regional markets accounted for roughly 65% of consolidated adjusted property EBITDA.

- 2024 U.S. unemployment 3.6% — impacts discretionary spend

- Manufacturing output down 0.3% Y/Y in parts of Midwest (2024)

- 40+ properties, 18 states; ~65% of adjusted property EBITDA from regional markets (2024)

Market saturation and competition

The rapid expansion of the North American gaming market has intensified competition for a finite pool of consumer dollars, with commercial gaming revenue in the U.S. reaching about $64.5 billion in 2023 and growing ~4% in 2024, pressuring margins as new entrants and online operators expand market share.

Economic pressure stems from new players and aggressive pricing, forcing PENN to invest in product innovation and loyalty offers; PENN reported Q3 2025 adjusted EBITDA of $429 million, highlighting the need to protect pricing power and retention amid crowding.

- U.S. gaming revenue ~64.5B (2023); ~4% growth in 2024

- PENN Q3 2025 adjusted EBITDA $429M

- Competition from online entrants and regional expansions compresses margins

- Continuous innovation and loyalty investments required to sustain market share

PENN faces income-squeeze and refinancing risk as visitation and debt pressures rise

PENN’s revenue sensitive to disposable income—US real DPI -0.2% MoM Dec 2025; CPI 3.4% YoY (2025) and AHE +3.6% YoY affect visitation. Net debt ~$7.5B (FY2025) with ~$1.2B maturities next 3 years raises refinancing risk. U.S. gaming revenue ~$64.5B (2023), ~4% growth in 2024; Q3 2025 adj. EBITDA $429M; ESPN digital reach ~150M monthly (2024).

| Metric | Value |

|---|---|

| Net debt FY2025 | $7.5B |

| Near-term maturities | $1.2B |

| US DPI change Dec 2025 | -0.2% MoM |

| CPI 2025 | 3.4% YoY |

| Q3 2025 EBITDA | $429M |

Full Version Awaits

PENN Entertainment PESTLE Analysis

The preview shown here is the exact PENN Entertainment PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.