Penske Corp. PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Penske Corp. faces regulatory scrutiny, shifting trade dynamics, and rapid tech adoption across logistics and mobility—our PESTLE snapshot highlights these external pressures and strategic opportunities for growth and risk mitigation. Purchase the full PESTLE analysis to get a detailed, actionable roadmap you can use in investment models, board decks, or market-entry plans.

Political factors

Global Trade Policy and Tariffs

Changes in international trade agreements and tariffs materially affect Penske Automotive Group’s global operations, with tariff-related import cost shifts driving up parts and vehicle expenses; in 2025 tariffs added an estimated 2–4% to imported vehicle costs in key markets. Ongoing trade tensions among the US, UK and Germany pressured margins and inventory turnover, forcing Penske to adjust pricing and hedging to protect a roughly $30–40 million annual impact on supply-chain costs.

Infrastructure Investment Legislation

Federal infrastructure bills, including the 2021 Bipartisan Infrastructure Law and subsequent 2024–25 allocations, boost transportation funding—$110B for roads and bridges through 2026—directly improving Penske’s logistics efficiency and margins by reducing detours and delays.

Higher public investment in highway maintenance and bridge repair lowers vehicle wear, cutting fleet maintenance costs; industry estimates suggest a 5–8% decline in heavy-truck maintenance spend per mile with improved infrastructure.

Penske tracks legislative moves to align fleet deployment with national priorities through 2025, positioning for increased contract wins in public-private projects and optimizing capital allocation across its trucking and logistics divisions.

Energy Security and Fuel Subsidies

Political choices on domestic energy and fuel subsidies materially affect Penske’s diesel fleet costs; U.S. diesel retail averaged about 4.03 USD/gal in 2025 Q4, down from 4.55 USD/gal in 2024, shifting OPEX forecasts for fleet logistics.

Incentives for alternative fuels—e.g., IRA tax credits boosting EV and hydrogen infrastructure with up to 30% investment credits—are steering Penske toward accelerated electric and hydrogen truck procurement.

Penske adjusts maintenance, leasing, and fuel services to reflect the political tilt between fossil fuel support and renewable subsidies, reallocating CAPEX toward charging and fuel-cell servicing as policy signals firm up.

International Market Stability

Penske’s large European operations make it sensitive to EU and UK political stability; shifts can alter regulations and tax policies impacting automotive retail and leasing demand—Europe accounted for roughly 28% of global vehicle leasing revenue in 2024, increasing exposure to regional policy changes.

Diversification across North America, Europe and Asia helped Penske limit market-specific political risk after 2023–24 regulatory shifts, with non-US revenue comprising about 34% of consolidated sales in FY 2024.

- Europe/UK political shifts can change taxes, emissions rules, and subsidies affecting demand

- Europe ~28% of global leasing revenue (2024)

- Non-US revenue ~34% of Penske consolidated sales (FY 2024)

Government Fleet Contracts

Penske frequently wins large government fleet and logistics contracts, including a 2023 US General Services Administration task order valued at roughly $150 million for vehicle maintenance and support services.

Political administration changes can reallocate federal and state procurement budgets—federal transport outsourcing fell 4% in 2024—impacting future contract pipelines for Penske.

Maintaining public-sector relationships requires continuous compliance with evolving procurement rules, transparency mandates, and audit readiness to retain multi-year contracts worth tens to hundreds of millions.

- Penske secured government work worth ~ $150M in 2023

- Federal outsourcing budgets down ~4% in 2024

- Contracts demand strict compliance, transparency, audit readiness

Penske margins hit by 2025 tariffs, infrastructure boost and fuel cost swings

Political shifts in trade, infrastructure and energy policy materially affect Penske’s margins and CAPEX: 2025 tariffs raised import costs ~2–4% (impact $30–40M annually), US infrastructure funding ~$110B to 2026 improves logistics, diesel averaged $4.03/gal in 2025 Q4 vs $4.55/gal in 2024, non‑US revenue ~34% FY2024, Europe ~28% of leasing revenue (2024).

| Metric | Value |

|---|---|

| Tariff impact | 2–4% ($30–40M) |

| Infrastructure funding | $110B to 2026 |

| Diesel (2025 Q4) | $4.03/gal |

| Non‑US revenue | 34% FY2024 |

What is included in the product

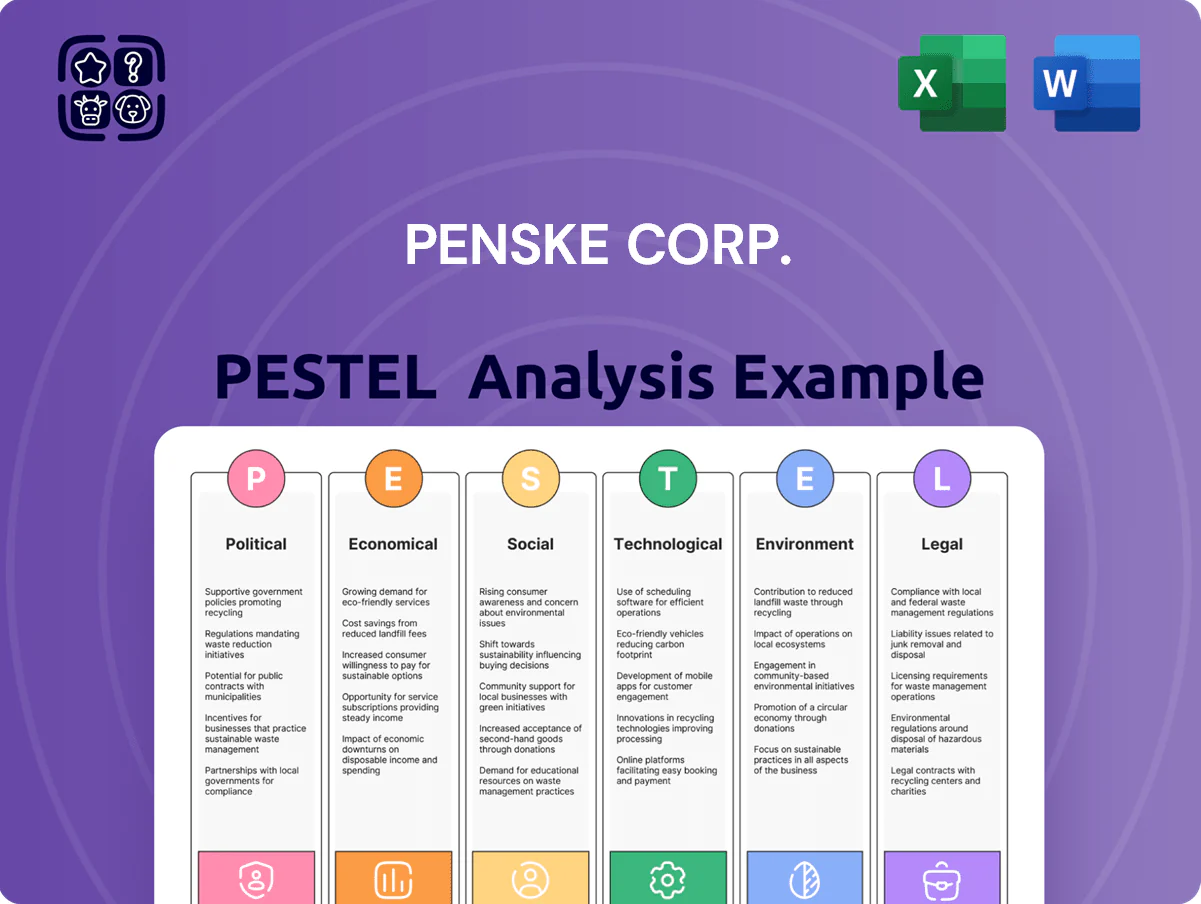

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Penske Corp.’s logistics, fleet, and equipment businesses, with data-driven trends, region- and industry-relevant examples, forward-looking scenario insights, and actionable implications to inform executives, investors, and strategists.

A concise PESTLE snapshot of Penske Corp. that distills regulatory, economic, social, technological, and environmental factors into an easily shareable slide or meeting handout to speed strategic alignment and risk discussion.

Economic factors

Interest Rate Environment

Fluctuations in central bank rates directly raise Penske’s financing costs for its ~300,000-vehicle fleet and consumer auto loans; the Fed funds rate rising to 5.25–5.50% in 2024–2025 increased interest expenses and compressed leasing margins.

Higher rates through 2025 slowed retail unit growth—US new-vehicle sales fell ~2–3% YoY in 2025, raising average monthly payments by $30–$50 and reducing demand for financed purchases.

Management has pursued debt restructuring, extending maturities and issuing lower-cost notes, while targeting capital efficiency improvements to protect EBITDA margins under prolonged restrictive monetary policy.

Consumer Spending and Credit Availability

Consumer spending and credit availability drive automotive retail; US auto loan originations fell 7% in 2024 vs 2023 amid rising rates, and consumer confidence averaged 66 in 2024, pressuring dealership traffic and vehicle demand.

During downturns or tighter credit, Penske faces lower new/used sales but mitigates risk through finance partnerships and captive-lender access that preserve purchase options.

Penske’s multi-brand portfolio—from luxury (Penske Automotive Group affiliates) to value channels—helps retain market share across segments when demand shifts.

Freight Market Volatility

Penske Logistics and Penske Truck Leasing are highly sensitive to freight market cycles; global freight volumes fell about 4-6% in 2023 but began recovering in 2024 with container throughput up ~3% year-over-year, directly affecting utilization and revenue per truck. Recessions compress tonnage demand and lower leased-asset utilization, while GDP growth boosts demand for supply-chain services. Penske mitigates volatility via flexible leasing and pay-per-use options that transfer operating risk to customers and preserved fleet utilization.

Global Inflationary Pressures

Persistent global inflation raised input costs for Penske—parts, labor, and equipment—contributing to U.S. CPI averaging 3.4% in 2024 and OEM parts cost increases near 5% year-over-year, prompting targeted pricing adjustments for rentals and fleet services.

Higher operational expenses must be weighed against competitive lease rates; Penske reported 2024 revenue growth of ~6% while maintaining margin compression, signaling careful rate balancing with long-term partners.

Penske leverages scale to negotiate supplier discounts and long-term contracts, reducing exposure to supply-chain inflation spikes and securing better pricing on vehicles and components.

- 2024 U.S. CPI ~3.4%

- OEM parts +5% YoY (est.)

- Penske 2024 revenue growth ~6%

- Use of scale for supplier discounts and long-term contracts

Currency Exchange Fluctuations

As a global operator, Penske faces currency risk when translating 2024-25 international dealership earnings into USD; a 10% GBP or EUR depreciation vs. the dollar can cut reported revenue and net income by several percentage points given material UK/EU sales exposure.

In 2024 Penske noted FX headwinds; treasury uses forwards and options—hedging over rolling 12–24 month horizons—to stabilize margins and protect operating cash flow against sudden FX swings.

- 10% GBP/EUR move can shift reported revenue by multiple percentage points

- 2024–25 FX headwinds recorded; hedging via forwards/options applied

- Hedging horizons typically 12–24 months to smooth earnings

Penske margins pressured by rising rates, costs and FX despite 6% revenue growth

Rising rates through 2025 increased financing costs for Penske’s ~300,000-vehicle fleet and compressed margins as US new-vehicle sales fell ~2–3% YoY; 2024 U.S. CPI ~3.4% and OEM parts +5% YoY raised operating costs while 2024 revenue grew ~6%. FX volatility (10% GBP/EUR moves) and freight cycle swings (container throughput +3% in 2024) further affect revenue; hedging and scale help mitigate impact.

| Metric | 2024–25 |

|---|---|

| Fleet size | ~300,000 |

| U.S. CPI | 3.4% |

| OEM parts cost | +5% YoY |

| Revenue growth | ~6% (2024) |

| New-vehicle sales | -2–3% YoY (2025) |

| Container throughput | +3% YoY (2024) |

| FX sensitivity | 10% GBP/EUR → several pp impact |

Preview the Actual Deliverable

Penske Corp. PESTLE Analysis

The preview shown here is the exact Penske Corp. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it includes political, economic, social, technological, legal, and environmental assessments specific to Penske with no placeholders or teasers.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Penske Corp. faces regulatory scrutiny, shifting trade dynamics, and rapid tech adoption across logistics and mobility—our PESTLE snapshot highlights these external pressures and strategic opportunities for growth and risk mitigation. Purchase the full PESTLE analysis to get a detailed, actionable roadmap you can use in investment models, board decks, or market-entry plans.

Political factors

Global Trade Policy and Tariffs

Changes in international trade agreements and tariffs materially affect Penske Automotive Group’s global operations, with tariff-related import cost shifts driving up parts and vehicle expenses; in 2025 tariffs added an estimated 2–4% to imported vehicle costs in key markets. Ongoing trade tensions among the US, UK and Germany pressured margins and inventory turnover, forcing Penske to adjust pricing and hedging to protect a roughly $30–40 million annual impact on supply-chain costs.

Infrastructure Investment Legislation

Federal infrastructure bills, including the 2021 Bipartisan Infrastructure Law and subsequent 2024–25 allocations, boost transportation funding—$110B for roads and bridges through 2026—directly improving Penske’s logistics efficiency and margins by reducing detours and delays.

Higher public investment in highway maintenance and bridge repair lowers vehicle wear, cutting fleet maintenance costs; industry estimates suggest a 5–8% decline in heavy-truck maintenance spend per mile with improved infrastructure.

Penske tracks legislative moves to align fleet deployment with national priorities through 2025, positioning for increased contract wins in public-private projects and optimizing capital allocation across its trucking and logistics divisions.

Energy Security and Fuel Subsidies

Political choices on domestic energy and fuel subsidies materially affect Penske’s diesel fleet costs; U.S. diesel retail averaged about 4.03 USD/gal in 2025 Q4, down from 4.55 USD/gal in 2024, shifting OPEX forecasts for fleet logistics.

Incentives for alternative fuels—e.g., IRA tax credits boosting EV and hydrogen infrastructure with up to 30% investment credits—are steering Penske toward accelerated electric and hydrogen truck procurement.

Penske adjusts maintenance, leasing, and fuel services to reflect the political tilt between fossil fuel support and renewable subsidies, reallocating CAPEX toward charging and fuel-cell servicing as policy signals firm up.

International Market Stability

Penske’s large European operations make it sensitive to EU and UK political stability; shifts can alter regulations and tax policies impacting automotive retail and leasing demand—Europe accounted for roughly 28% of global vehicle leasing revenue in 2024, increasing exposure to regional policy changes.

Diversification across North America, Europe and Asia helped Penske limit market-specific political risk after 2023–24 regulatory shifts, with non-US revenue comprising about 34% of consolidated sales in FY 2024.

- Europe/UK political shifts can change taxes, emissions rules, and subsidies affecting demand

- Europe ~28% of global leasing revenue (2024)

- Non-US revenue ~34% of Penske consolidated sales (FY 2024)

Government Fleet Contracts

Penske frequently wins large government fleet and logistics contracts, including a 2023 US General Services Administration task order valued at roughly $150 million for vehicle maintenance and support services.

Political administration changes can reallocate federal and state procurement budgets—federal transport outsourcing fell 4% in 2024—impacting future contract pipelines for Penske.

Maintaining public-sector relationships requires continuous compliance with evolving procurement rules, transparency mandates, and audit readiness to retain multi-year contracts worth tens to hundreds of millions.

- Penske secured government work worth ~ $150M in 2023

- Federal outsourcing budgets down ~4% in 2024

- Contracts demand strict compliance, transparency, audit readiness

Penske margins hit by 2025 tariffs, infrastructure boost and fuel cost swings

Political shifts in trade, infrastructure and energy policy materially affect Penske’s margins and CAPEX: 2025 tariffs raised import costs ~2–4% (impact $30–40M annually), US infrastructure funding ~$110B to 2026 improves logistics, diesel averaged $4.03/gal in 2025 Q4 vs $4.55/gal in 2024, non‑US revenue ~34% FY2024, Europe ~28% of leasing revenue (2024).

| Metric | Value |

|---|---|

| Tariff impact | 2–4% ($30–40M) |

| Infrastructure funding | $110B to 2026 |

| Diesel (2025 Q4) | $4.03/gal |

| Non‑US revenue | 34% FY2024 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Penske Corp.’s logistics, fleet, and equipment businesses, with data-driven trends, region- and industry-relevant examples, forward-looking scenario insights, and actionable implications to inform executives, investors, and strategists.

A concise PESTLE snapshot of Penske Corp. that distills regulatory, economic, social, technological, and environmental factors into an easily shareable slide or meeting handout to speed strategic alignment and risk discussion.

Economic factors

Interest Rate Environment

Fluctuations in central bank rates directly raise Penske’s financing costs for its ~300,000-vehicle fleet and consumer auto loans; the Fed funds rate rising to 5.25–5.50% in 2024–2025 increased interest expenses and compressed leasing margins.

Higher rates through 2025 slowed retail unit growth—US new-vehicle sales fell ~2–3% YoY in 2025, raising average monthly payments by $30–$50 and reducing demand for financed purchases.

Management has pursued debt restructuring, extending maturities and issuing lower-cost notes, while targeting capital efficiency improvements to protect EBITDA margins under prolonged restrictive monetary policy.

Consumer Spending and Credit Availability

Consumer spending and credit availability drive automotive retail; US auto loan originations fell 7% in 2024 vs 2023 amid rising rates, and consumer confidence averaged 66 in 2024, pressuring dealership traffic and vehicle demand.

During downturns or tighter credit, Penske faces lower new/used sales but mitigates risk through finance partnerships and captive-lender access that preserve purchase options.

Penske’s multi-brand portfolio—from luxury (Penske Automotive Group affiliates) to value channels—helps retain market share across segments when demand shifts.

Freight Market Volatility

Penske Logistics and Penske Truck Leasing are highly sensitive to freight market cycles; global freight volumes fell about 4-6% in 2023 but began recovering in 2024 with container throughput up ~3% year-over-year, directly affecting utilization and revenue per truck. Recessions compress tonnage demand and lower leased-asset utilization, while GDP growth boosts demand for supply-chain services. Penske mitigates volatility via flexible leasing and pay-per-use options that transfer operating risk to customers and preserved fleet utilization.

Global Inflationary Pressures

Persistent global inflation raised input costs for Penske—parts, labor, and equipment—contributing to U.S. CPI averaging 3.4% in 2024 and OEM parts cost increases near 5% year-over-year, prompting targeted pricing adjustments for rentals and fleet services.

Higher operational expenses must be weighed against competitive lease rates; Penske reported 2024 revenue growth of ~6% while maintaining margin compression, signaling careful rate balancing with long-term partners.

Penske leverages scale to negotiate supplier discounts and long-term contracts, reducing exposure to supply-chain inflation spikes and securing better pricing on vehicles and components.

- 2024 U.S. CPI ~3.4%

- OEM parts +5% YoY (est.)

- Penske 2024 revenue growth ~6%

- Use of scale for supplier discounts and long-term contracts

Currency Exchange Fluctuations

As a global operator, Penske faces currency risk when translating 2024-25 international dealership earnings into USD; a 10% GBP or EUR depreciation vs. the dollar can cut reported revenue and net income by several percentage points given material UK/EU sales exposure.

In 2024 Penske noted FX headwinds; treasury uses forwards and options—hedging over rolling 12–24 month horizons—to stabilize margins and protect operating cash flow against sudden FX swings.

- 10% GBP/EUR move can shift reported revenue by multiple percentage points

- 2024–25 FX headwinds recorded; hedging via forwards/options applied

- Hedging horizons typically 12–24 months to smooth earnings

Penske margins pressured by rising rates, costs and FX despite 6% revenue growth

Rising rates through 2025 increased financing costs for Penske’s ~300,000-vehicle fleet and compressed margins as US new-vehicle sales fell ~2–3% YoY; 2024 U.S. CPI ~3.4% and OEM parts +5% YoY raised operating costs while 2024 revenue grew ~6%. FX volatility (10% GBP/EUR moves) and freight cycle swings (container throughput +3% in 2024) further affect revenue; hedging and scale help mitigate impact.

| Metric | 2024–25 |

|---|---|

| Fleet size | ~300,000 |

| U.S. CPI | 3.4% |

| OEM parts cost | +5% YoY |

| Revenue growth | ~6% (2024) |

| New-vehicle sales | -2–3% YoY (2025) |

| Container throughput | +3% YoY (2024) |

| FX sensitivity | 10% GBP/EUR → several pp impact |

Preview the Actual Deliverable

Penske Corp. PESTLE Analysis

The preview shown here is the exact Penske Corp. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it includes political, economic, social, technological, legal, and environmental assessments specific to Penske with no placeholders or teasers.