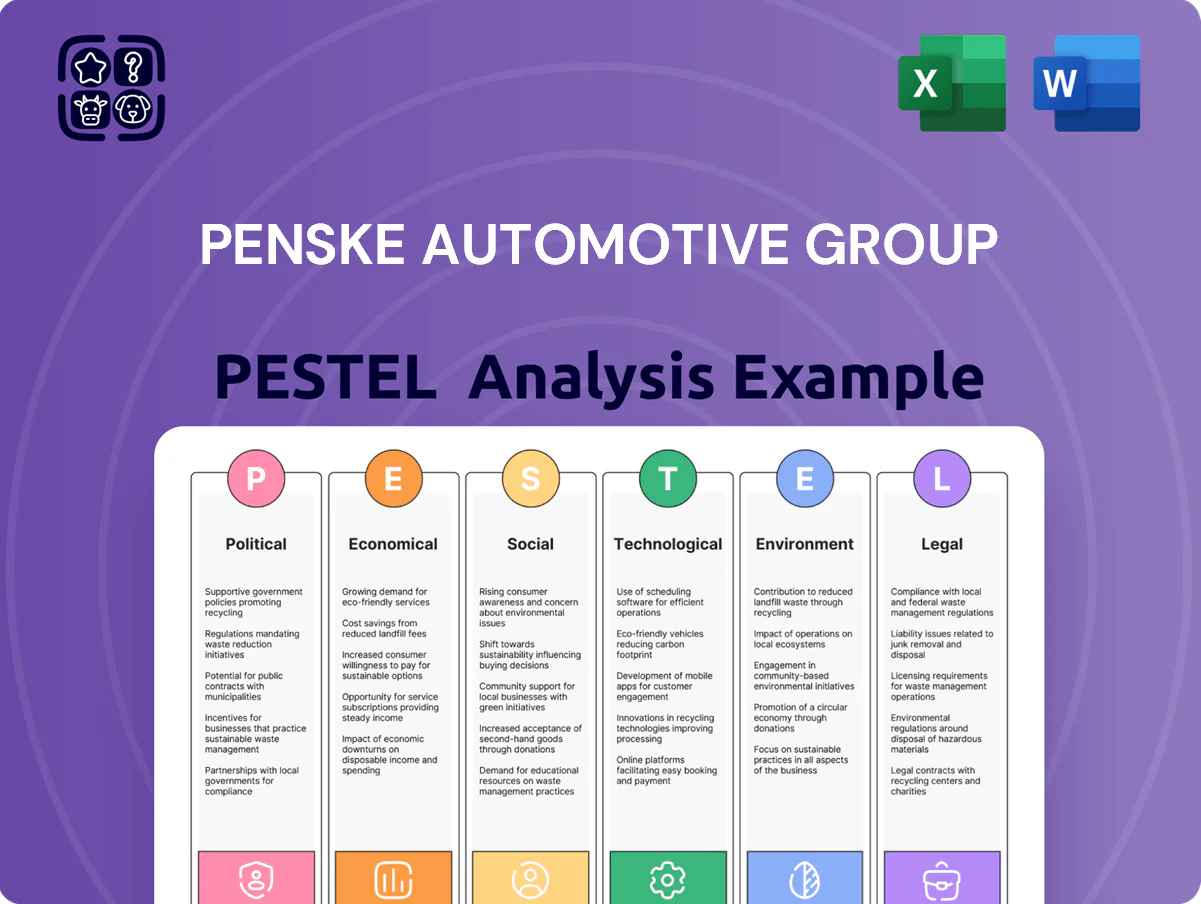

Penske Automotive Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Penske Automotive Group faces regulatory pressures, shifting consumer demand, and rapid technological change that are reshaping its margins and dealer network strategy; our PESTLE highlights these forces and pinpoints the biggest risks and opportunities for investors and managers. Buy the full analysis to get a ready-to-use, editable report with deep insights and actionable recommendations tailored to Penske’s competitive landscape.

Political factors

International Trade Agreements and Tariffs

Trade policies between the US, UK and Germany materially affect Penske Automotive Group’s vehicle inventory costs; for example, US auto imports faced average tariffs of 2.5% while UK post-Brexit admin costs rose 5–8% for EU-origin parts in 2024, pushing supply-chain landed costs higher.

A 1–3 percentage-point rise in import duties or new cross-border restrictions can widen margins on luxury brands like Mercedes and BMW—Penske’s Q4 2024 wholesale vehicle purchases increased 4.2% YoY—squeezing retail gross margins.

These tariff shifts and trade frictions complicate pricing across Penske’s international dealership network of over 700 locations, forcing dynamic repricing to preserve competitive margins and affecting inventory turnover rates.

Government Subsidies for Electric Vehicles

Political decisions on extending or ending federal EV tax credits materially affect U.S. BEV demand; the Inflation Reduction Act’s tax credit changes reduced eligible models from about 200 in 2023 to ~100 by mid-2025, pressuring retail volumes. As subsidies shift toward charging infrastructure—federal CHIPS-like grants and $7.5B for EV chargers—Penske must rebalance inventory toward hybrid and compliant BEV models to protect margins. 2025 legislation tightened domestic content rules, making only vehicles meeting North American sourcing thresholds eligible, increasing procurement complexity and affecting turnover.

Geopolitical Stability in Global Markets

Operations in Europe and the UK expose Penske Automotive Group to regional political volatility and post-election regulatory shifts that in 2024–25 contributed to sterling and euro swings of roughly 6–8% vs USD, increasing FX translation risk on the company’s €3.2bn European revenues; political instability also dampens demand for high-ticket vehicles, with EU new-car registrations down 2.8% in 2024, prompting Penske to closely monitor elections and regulatory changes to hedge currency and adjust inventory across its footprint.

Commercial Transportation Regulations

Government mandates on freight standards and fuel efficiency drive demand for Penske’s truck leasing and logistics, with U.S. EPA and CARB rules pushing fleet upgrades that supported Premier Truck Group revenue growth; Penske reported total revenue of $17.6 billion in 2024, with commercial vehicle services a key contributor.

Political pressure to modernize ports and highways spurs new fleet standards internationally, raising capex for operators but creating lease and maintenance opportunities for Penske’s international distribution arms.

- Regulatory-driven fleet renewal increases demand for leasing/maintenance.

- 2024 revenue $17.6B underscores fleet services importance.

- Infrastructure updates create growth avenues for international distribution.

Taxation Policies and Corporate Rates

Changes in corporate tax structures in Penske Automotive Group’s primary US market directly impact net income and capital allocation; the effective tax rate fell to 18.1% in FY2024, boosting after-tax cash flow for investments.

Recent legislative focus on minimum corporate taxes and closing loopholes, including proposals targeting global intangible low-taxed income, forces more sophisticated tax planning and may raise the firm’s blended rate.

Higher statutory or minimum taxes would reduce available liquidity for acquisitions and dividends—PAG held $1.6 billion in cash and equivalents at end-FY2024, a key buffer for M&A and shareholder returns.

- FY2024 effective tax rate 18.1%

- Cash & equivalents $1.6B (FY2024)

- Legislative pressure could raise blended rate, tightening M&A/dividend capacity

Penske margins and capital at risk from tariffs, EV credits, FX swings and tax shifts

Political shifts—tariff changes, EV credit rules, regional election-driven FX swings, and tighter tax proposals—directly affect Penske’s margins, inventory mix, and capital allocation: FY2024 revenue $17.6B, European revenue €3.2B, cash $1.6B, effective tax rate 18.1%, EU new-car registrations -2.8% (2024), UK/EUR FX swings ~6–8% (2024–25).

| Metric | Value (2024/25) |

|---|---|

| Total revenue | $17.6B |

| Europe revenue | €3.2B |

| Cash & equivalents | $1.6B |

| Effective tax rate | 18.1% |

| EU new-car registrations | -2.8% |

| FX swings (GBP/EUR vs USD) | ~6–8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Penske Automotive Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans or investor materials.

A concise, visually segmented PESTLE summary of Penske Automotive Group that teams can drop into presentations or planning sessions for quick alignment on external risks, market drivers, and strategic implications.

Economic factors

Interest Rate Environment and Financing Costs

Fluctuations in central bank rates directly change floorplan financing costs for Penske, where a 100bp rise can add materially to interest expense on its ~100,000-unit retail inventory; US Fed hikes through 2022–2023 pushed auto finance spreads up, raising dealer carrying costs in 2024. Higher rates also lifted average new-vehicle loan APRs to ~7.5%–8% in 2024, weighing on consumer demand and used-car volumes. Penske’s F&I income, which contributed roughly 11% of total retail gross profit in recent years, is sensitive to these monetary shifts.

Consumer Disposable Income Trends

Demand for luxury brands at Penske Automotive Group closely follows the wealth effect; US upper‑middle income households saw real disposable personal income drop 0.3% year‑over‑year in 2024 Q4, weighing on premium new-vehicle purchases. Inflation (CPI 3.4% in 2024) and rate hikes pushed many buyers toward used inventory—used-vehicle transactions rose 6% in 2024. Monitoring wage growth (average hourly earnings up 4.2% in 2024) and unemployment (3.7% as of Dec 2024) helps Penske forecast premium segment volumes.

Used Vehicle Valuation and Residual Values

Used-vehicle profitability for Penske hinges on stabilizing pre-owned prices; U.S. used retail prices fell about 7% year-over-year in 2024, pressuring margins on aging inventory.

Recovery in new-vehicle supply—chip availability improving with global production up ~4% in 2024—raises trade-in volumes and can compress resale spreads as more late-model returns enter the market.

Penske leverages analytics from its Cox Automotive partnership and ROC platform to target a sub-30-day inventory turnover goal, reducing average depreciation and protecting residual value realization.

Currency Exchange Rate Volatility

Currency swings materially affect Penske: in FY2024 roughly 30% of revenue came from GBP/EUR operations, so a 5% USD strengthening reduced reported revenue by ~1.5% and diluted EPS by an estimated $0.05 in 2024.

US–EU economic divergence heightens translational risk, altering consolidated equity and OCI when sterling/euro weaken versus the dollar.

Management uses forward contracts and natural hedges; net FX exposure was reduced by ~60% via hedging at end-2024.

- ~30% revenue from GBP/EUR (FY2024)

- 5% USD appreciation ≈ 1.5% revenue headwind

- Hedging covered ~60% of net exposure (end-2024)

Global Supply Chain and Inflationary Costs

Rising labor, parts and logistics costs compressed Penske Automotive Group’s U.S. service margins in 2024–2025; parts inflation averaged ~6–8% year-over-year and hourly wage growth in automotive service roles rose ~5% in 2024.

Broader inflation (U.S. CPI ~3.4% in 2024) forced periodic service-price adjustments and tighter cost controls to protect EBITDA in aftersales operations.

Securing resilient commercial-parts supply chains remains critical to meet heavy trucking demand—Penske’s fleet and commercial divisions saw parts revenue growth ~7% in 2024, highlighting dependency on stable inventory flows.

- Parts inflation ~6–8% YoY (2024)

- Service wages +5% (2024)

- U.S. CPI ~3.4% (2024)

- Parts revenue growth ~7% for commercial divisions (2024)

Higher rates and FX headwinds dent margins as used prices fall and parts grow

Higher rates raised floorplan costs and retail APRs (~7.5%–8% in 2024), damping demand; used prices fell ~7% YoY (2024) while new production rose ~4% (2024). FX (≈30% revenue GBP/EUR) meant a 5% USD gain cut revenue ~1.5%; hedging covered ~60% exposure (end‑2024). Parts inflation ~6–8% and service wages +5% (2024) compressed margins; parts revenue in commercial divisions grew ~7% (2024).

| Metric | 2024 |

|---|---|

| New prod change | +4% |

| Used price YoY | -7% |

| Avg new APR | 7.5%–8% |

| FX revenue mix | ~30% GBP/EUR |

| Hedge coverage | ~60% |

| Parts inflation | 6%–8% |

| Service wages | +5% |

| Commercial parts rev | +7% |

Same Document Delivered

Penske Automotive Group PESTLE Analysis

The preview shown here is the exact Penske Automotive Group PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and insights visible now are the final file available for immediate download with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Penske Automotive Group faces regulatory pressures, shifting consumer demand, and rapid technological change that are reshaping its margins and dealer network strategy; our PESTLE highlights these forces and pinpoints the biggest risks and opportunities for investors and managers. Buy the full analysis to get a ready-to-use, editable report with deep insights and actionable recommendations tailored to Penske’s competitive landscape.

Political factors

International Trade Agreements and Tariffs

Trade policies between the US, UK and Germany materially affect Penske Automotive Group’s vehicle inventory costs; for example, US auto imports faced average tariffs of 2.5% while UK post-Brexit admin costs rose 5–8% for EU-origin parts in 2024, pushing supply-chain landed costs higher.

A 1–3 percentage-point rise in import duties or new cross-border restrictions can widen margins on luxury brands like Mercedes and BMW—Penske’s Q4 2024 wholesale vehicle purchases increased 4.2% YoY—squeezing retail gross margins.

These tariff shifts and trade frictions complicate pricing across Penske’s international dealership network of over 700 locations, forcing dynamic repricing to preserve competitive margins and affecting inventory turnover rates.

Government Subsidies for Electric Vehicles

Political decisions on extending or ending federal EV tax credits materially affect U.S. BEV demand; the Inflation Reduction Act’s tax credit changes reduced eligible models from about 200 in 2023 to ~100 by mid-2025, pressuring retail volumes. As subsidies shift toward charging infrastructure—federal CHIPS-like grants and $7.5B for EV chargers—Penske must rebalance inventory toward hybrid and compliant BEV models to protect margins. 2025 legislation tightened domestic content rules, making only vehicles meeting North American sourcing thresholds eligible, increasing procurement complexity and affecting turnover.

Geopolitical Stability in Global Markets

Operations in Europe and the UK expose Penske Automotive Group to regional political volatility and post-election regulatory shifts that in 2024–25 contributed to sterling and euro swings of roughly 6–8% vs USD, increasing FX translation risk on the company’s €3.2bn European revenues; political instability also dampens demand for high-ticket vehicles, with EU new-car registrations down 2.8% in 2024, prompting Penske to closely monitor elections and regulatory changes to hedge currency and adjust inventory across its footprint.

Commercial Transportation Regulations

Government mandates on freight standards and fuel efficiency drive demand for Penske’s truck leasing and logistics, with U.S. EPA and CARB rules pushing fleet upgrades that supported Premier Truck Group revenue growth; Penske reported total revenue of $17.6 billion in 2024, with commercial vehicle services a key contributor.

Political pressure to modernize ports and highways spurs new fleet standards internationally, raising capex for operators but creating lease and maintenance opportunities for Penske’s international distribution arms.

- Regulatory-driven fleet renewal increases demand for leasing/maintenance.

- 2024 revenue $17.6B underscores fleet services importance.

- Infrastructure updates create growth avenues for international distribution.

Taxation Policies and Corporate Rates

Changes in corporate tax structures in Penske Automotive Group’s primary US market directly impact net income and capital allocation; the effective tax rate fell to 18.1% in FY2024, boosting after-tax cash flow for investments.

Recent legislative focus on minimum corporate taxes and closing loopholes, including proposals targeting global intangible low-taxed income, forces more sophisticated tax planning and may raise the firm’s blended rate.

Higher statutory or minimum taxes would reduce available liquidity for acquisitions and dividends—PAG held $1.6 billion in cash and equivalents at end-FY2024, a key buffer for M&A and shareholder returns.

- FY2024 effective tax rate 18.1%

- Cash & equivalents $1.6B (FY2024)

- Legislative pressure could raise blended rate, tightening M&A/dividend capacity

Penske margins and capital at risk from tariffs, EV credits, FX swings and tax shifts

Political shifts—tariff changes, EV credit rules, regional election-driven FX swings, and tighter tax proposals—directly affect Penske’s margins, inventory mix, and capital allocation: FY2024 revenue $17.6B, European revenue €3.2B, cash $1.6B, effective tax rate 18.1%, EU new-car registrations -2.8% (2024), UK/EUR FX swings ~6–8% (2024–25).

| Metric | Value (2024/25) |

|---|---|

| Total revenue | $17.6B |

| Europe revenue | €3.2B |

| Cash & equivalents | $1.6B |

| Effective tax rate | 18.1% |

| EU new-car registrations | -2.8% |

| FX swings (GBP/EUR vs USD) | ~6–8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Penske Automotive Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans or investor materials.

A concise, visually segmented PESTLE summary of Penske Automotive Group that teams can drop into presentations or planning sessions for quick alignment on external risks, market drivers, and strategic implications.

Economic factors

Interest Rate Environment and Financing Costs

Fluctuations in central bank rates directly change floorplan financing costs for Penske, where a 100bp rise can add materially to interest expense on its ~100,000-unit retail inventory; US Fed hikes through 2022–2023 pushed auto finance spreads up, raising dealer carrying costs in 2024. Higher rates also lifted average new-vehicle loan APRs to ~7.5%–8% in 2024, weighing on consumer demand and used-car volumes. Penske’s F&I income, which contributed roughly 11% of total retail gross profit in recent years, is sensitive to these monetary shifts.

Consumer Disposable Income Trends

Demand for luxury brands at Penske Automotive Group closely follows the wealth effect; US upper‑middle income households saw real disposable personal income drop 0.3% year‑over‑year in 2024 Q4, weighing on premium new-vehicle purchases. Inflation (CPI 3.4% in 2024) and rate hikes pushed many buyers toward used inventory—used-vehicle transactions rose 6% in 2024. Monitoring wage growth (average hourly earnings up 4.2% in 2024) and unemployment (3.7% as of Dec 2024) helps Penske forecast premium segment volumes.

Used Vehicle Valuation and Residual Values

Used-vehicle profitability for Penske hinges on stabilizing pre-owned prices; U.S. used retail prices fell about 7% year-over-year in 2024, pressuring margins on aging inventory.

Recovery in new-vehicle supply—chip availability improving with global production up ~4% in 2024—raises trade-in volumes and can compress resale spreads as more late-model returns enter the market.

Penske leverages analytics from its Cox Automotive partnership and ROC platform to target a sub-30-day inventory turnover goal, reducing average depreciation and protecting residual value realization.

Currency Exchange Rate Volatility

Currency swings materially affect Penske: in FY2024 roughly 30% of revenue came from GBP/EUR operations, so a 5% USD strengthening reduced reported revenue by ~1.5% and diluted EPS by an estimated $0.05 in 2024.

US–EU economic divergence heightens translational risk, altering consolidated equity and OCI when sterling/euro weaken versus the dollar.

Management uses forward contracts and natural hedges; net FX exposure was reduced by ~60% via hedging at end-2024.

- ~30% revenue from GBP/EUR (FY2024)

- 5% USD appreciation ≈ 1.5% revenue headwind

- Hedging covered ~60% of net exposure (end-2024)

Global Supply Chain and Inflationary Costs

Rising labor, parts and logistics costs compressed Penske Automotive Group’s U.S. service margins in 2024–2025; parts inflation averaged ~6–8% year-over-year and hourly wage growth in automotive service roles rose ~5% in 2024.

Broader inflation (U.S. CPI ~3.4% in 2024) forced periodic service-price adjustments and tighter cost controls to protect EBITDA in aftersales operations.

Securing resilient commercial-parts supply chains remains critical to meet heavy trucking demand—Penske’s fleet and commercial divisions saw parts revenue growth ~7% in 2024, highlighting dependency on stable inventory flows.

- Parts inflation ~6–8% YoY (2024)

- Service wages +5% (2024)

- U.S. CPI ~3.4% (2024)

- Parts revenue growth ~7% for commercial divisions (2024)

Higher rates and FX headwinds dent margins as used prices fall and parts grow

Higher rates raised floorplan costs and retail APRs (~7.5%–8% in 2024), damping demand; used prices fell ~7% YoY (2024) while new production rose ~4% (2024). FX (≈30% revenue GBP/EUR) meant a 5% USD gain cut revenue ~1.5%; hedging covered ~60% exposure (end‑2024). Parts inflation ~6–8% and service wages +5% (2024) compressed margins; parts revenue in commercial divisions grew ~7% (2024).

| Metric | 2024 |

|---|---|

| New prod change | +4% |

| Used price YoY | -7% |

| Avg new APR | 7.5%–8% |

| FX revenue mix | ~30% GBP/EUR |

| Hedge coverage | ~60% |

| Parts inflation | 6%–8% |

| Service wages | +5% |

| Commercial parts rev | +7% |

Same Document Delivered

Penske Automotive Group PESTLE Analysis

The preview shown here is the exact Penske Automotive Group PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and insights visible now are the final file available for immediate download with no placeholders or surprises.