Perdue Farms PESTLE Analysis

Your Competitive Advantage Starts with This Report

Perdue Farms faces a complex external landscape—from regulatory scrutiny and shifting consumer food preferences to supply-chain and climate risks—our PESTLE distills these forces into strategic implications you can act on. Gain investor-grade insights and scenario-ready recommendations tailored to Perdue’s operations. Download the full PESTLE now for the complete, editable analysis and make smarter, faster decisions.

Political factors

Trade Policy and International Export Relations

Perdue Farms depends on trade agreements to export poultry and grain; exports to Mexico and China comprised an estimated 18% of its 2024 shipments, so tariff shifts can cut revenue materially.

Tariff hikes or non-tariff barriers—e.g., China’s 2019 temporary poultry restrictions and Mexico’s 2022 SPS measures—have historically swung Perdue’s market share by several percentage points.

Political instability or rising protectionism forces Perdue to reroute supply chains; in 2023-24 rerouting added an estimated 2–4% to logistics costs and compressed margins.

Federal Agricultural Subsidies and Farm Bill Legislation

Perdue Farms faces direct exposure to the U.S. Farm Bill: 2023–24 federal commodity and crop insurance programs channel roughly $20–30 billion annually in support to grain producers, directly moderating corn and soybean prices that determine Perdue’s feed costs, its largest operating expense (feed typically ~40–45% of live production costs). Political shifts toward conservation or renewable mandates could raise feed prices by 5–15% and reshape margins for Perdue and its ~6,000 independent growers.

U.S. Department of Agriculture Regulatory Oversight

USDA mandates on food safety, inspection and labeling set binding protocols for Perdue, with FSIS inspections and HACCP compliance impacting processing; in 2024 USDA funding rose to $166.5 billion, supporting stricter enforcement and training programs that raise compliance costs for poultry processors.

Labor Migration and Immigration Policy

The meat processing sector relies heavily on immigrant labor; Perdue Farms employed ~24,000 workers in 2024 across processing and poultry with an industry average immigrant share near 32% (USDA/FAIR 2024), so restrictive immigration reform or cuts to H-2B/H-2A visa programs can cause acute labor shortages and raise recruitment costs.

Political shifts after 2024 proposals tightening border enforcement could increase Perdue’s hourly labor costs by an estimated 5–12% due to higher wages, overtime and training, affecting margins in a sector with low single-digit operating margins.

Perdue’s plant staffing resilience is therefore directly tied to federal and state labor and border policies, union/legislative actions, and visa program stability that influence turnover and productivity.

- Perdue workforce ~24,000 (2024)

- Industry immigrant share ~32% (2024)

- Potential labor cost impact 5–12% if visa access tightens

- Staffing tied to federal/state border and labor policy

Biosecurity and Disease Management Protocols

Government-led responses to outbreaks like HPAI require coordinated federal and state action; in 2022–2024 HPAI led to the depopulation of over 68 million domestic birds in the U.S., illustrating regulatory reach and disruption risk to Perdue’s supply chain and revenues.

State and federal agencies can restrict movements or order culling, creating immediate operational and political risk that can halt production and increase costs through lost inventory and containment measures.

Perdue collaborates with USDA, state departments of agriculture, and industry groups to implement biosecurity protocols protecting the national food supply and mitigating potential economic losses.

- 2022–24 HPAI: >68 million birds depopulated in U.S.

- Regulatory power: movement bans, mandatory culling

- Perdue action: active coordination with USDA and states

Perdue faces trade, HPAI and labor risks—18% exports, feed 40–45%, labor +5–12%

Perdue’s revenue and margins are sensitive to trade, tariffs, Farm Bill support, USDA regulation, HPAI controls, and immigration policy; exports ~18% of 2024 shipments, workforce ~24,000, feed = 40–45% of live production cost, 2022–24 HPAI depopulated >68M birds, potential labor cost rise 5–12% if visa tightening occurs.

| Metric | 2024/2022–24 |

|---|---|

| Export share | ~18% |

| Workforce | ~24,000 |

| Feed share | 40–45% |

| HPAI impact | >68M birds |

| Labor cost risk | +5–12% |

What is included in the product

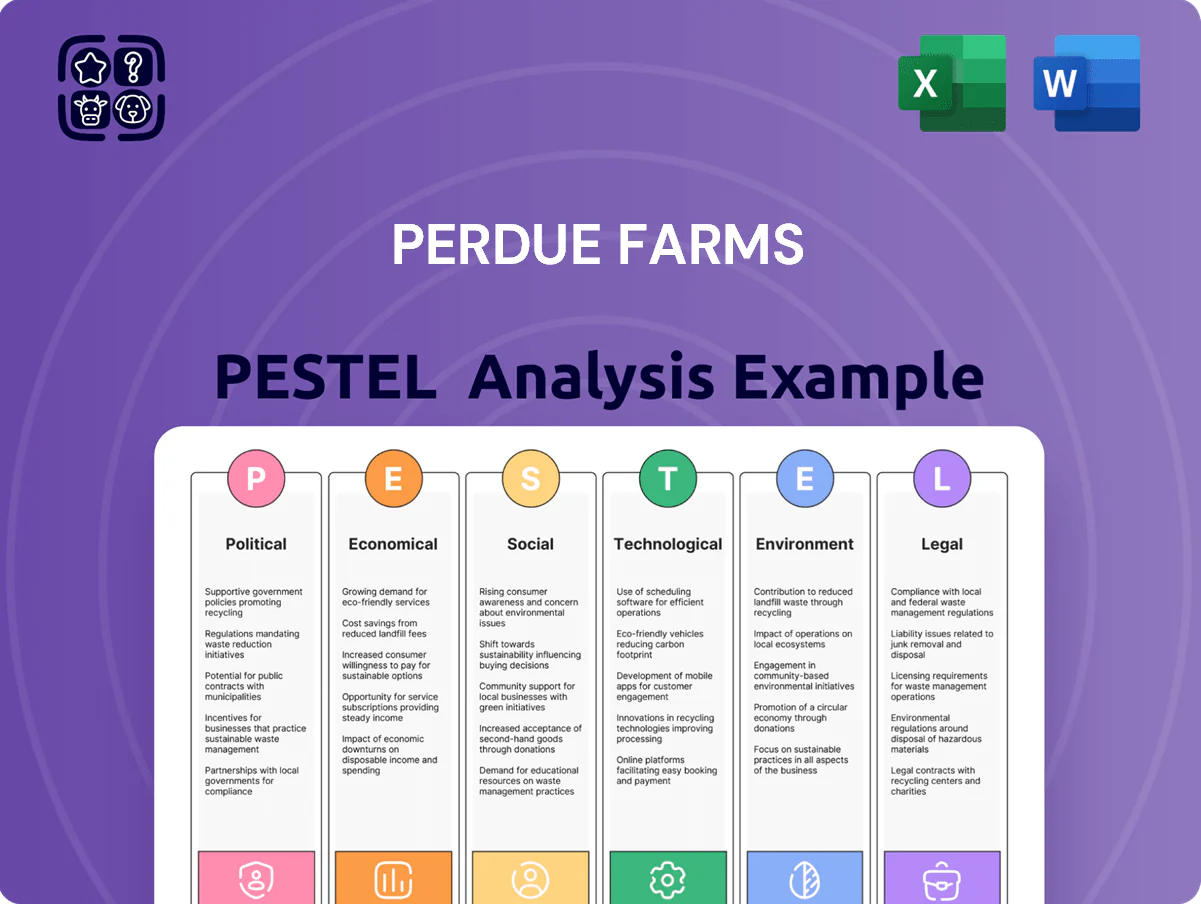

Explores how external macro-environmental factors uniquely affect Perdue Farms across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by relevant data and current trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE snapshot of Perdue Farms for quick reference in meetings or presentations, easily shareable and editable so teams can annotate region- or line-specific risks and opportunities.

Economic factors

Fluctuations in Commodity Feed Costs

Volatility in corn and soybean prices is a core economic risk for Perdue, with U.S. corn futures up ~28% year-over-year and soybean futures up ~18% as of Jan 2026, driving feed-cost inflation that can erode poultry margins; poor global harvests or export demand shocks can sharply raise production costs. Perdue uses futures and options hedging and forward contracts to stabilize input costs and protect consumer pricing, reducing feed-cost exposure.

Consumer Purchasing Power and Inflationary Pressures

Rising US inflation (CPI 3.4% in 2024) shifts shoppers toward cheaper proteins, boosting chicken demand vs beef; USDA noted 2024 retail chicken prices were ~15% lower than beef year-over-year, favoring Perdue.

Perdue’s pricing must offset feed and energy cost rises—corn and soybean meal up ~12% in 2024—while keeping affordability for median US household real wages stagnant.

Sustained downturns compress margins: Perdue reported 2024 operating margin pressure industry-wide, forcing trade promotions and cost controls to protect volume and market share.

Labor Market Dynamics and Wage Inflation

Competitive labor markets and rising state minimum wages—e.g., 2024 increases to $15+ in 10 states and multiple localities—raise Perdue Farms processing and distribution costs, squeezing margins as labor comprises ~20–30% of poultry processing expenses. Perdue must boost retention and pay, reflected in 2024 SG&A pressures and wage-driven labor cost inflation near 4–6% year-over-year. Automation investments are accelerating: capital expenditures rose in 2023–2024 to modernize plants and offset human capital inflation.

Energy and Logistics Cost Volatility

Fuel and energy prices materially affect Perdue Farms’ COGS; diesel rose ~15% in 2024 vs 2023, pushing transport expenses higher across its 50-state network.

Global oil volatility in 2024-2025 raised shipping rates ~10–20%, increasing inbound feed and outbound product costs for Perdue’s integrated supply chain.

Efficiency programs—route optimization, on-site solar (Perdue reported installing >10 MW by 2024) and HVAC upgrades—are key to protecting margins.

- Diesel +15% (2024), shipping rates +10–20% (2024–25)

- Perdue installed >10 MW solar by 2024

- Logistics and energy initiatives directly reduce COGS pressure

Interest Rates and Capital Investment Debt

Perdue Farms, which invests heavily in processing and cold-chain infrastructure, is sensitive to the Federal Reserve’s rate moves; the Fed funds rate rose to a target range of 5.25–5.50% by Dec 2024, raising borrowing costs for capital projects.

Higher rates increase debt service on new plant expansions and tech integrations, potentially delaying projects and compressing returns on investments.

Perdue’s ability to finance long-term growth depends on the prevailing macro rate environment and access to credit markets.

- Fed funds 5.25–5.50% (Dec 2024)

- Higher rates raise debt service, slow capex

- Capital-intensive projects at risk of delay

Perdue Battles Rising Feed, Fuel & Rates with Hedging, Solar >10MW and Automation

Feed, energy, labor and rates drove 2024–25 cost pressure: corn +28% YoY (Jan 2026), soy +18%, diesel +15% (2024), shipping +10–20% (2024–25), Fed funds 5.25–5.50% (Dec 2024); Perdue hedges inputs, invests >10 MW solar, automation and route optimization to protect margins and capex flexibility.

| Metric | Value |

|---|---|

| Corn futures | +28% YoY |

| Soy futures | +18% YoY |

| Diesel (2024) | +15% |

| Shipping | +10–20% |

| Fed funds | 5.25–5.50% |

| Solar installed | >10 MW |

What You See Is What You Get

Perdue Farms PESTLE Analysis

The preview shown here is the exact Perdue Farms PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no surprises. The content, layout, and structure visible in the preview are identical to the downloadable file you’ll get immediately after payment. Everything displayed is part of the final, professionally structured report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Perdue Farms faces a complex external landscape—from regulatory scrutiny and shifting consumer food preferences to supply-chain and climate risks—our PESTLE distills these forces into strategic implications you can act on. Gain investor-grade insights and scenario-ready recommendations tailored to Perdue’s operations. Download the full PESTLE now for the complete, editable analysis and make smarter, faster decisions.

Political factors

Trade Policy and International Export Relations

Perdue Farms depends on trade agreements to export poultry and grain; exports to Mexico and China comprised an estimated 18% of its 2024 shipments, so tariff shifts can cut revenue materially.

Tariff hikes or non-tariff barriers—e.g., China’s 2019 temporary poultry restrictions and Mexico’s 2022 SPS measures—have historically swung Perdue’s market share by several percentage points.

Political instability or rising protectionism forces Perdue to reroute supply chains; in 2023-24 rerouting added an estimated 2–4% to logistics costs and compressed margins.

Federal Agricultural Subsidies and Farm Bill Legislation

Perdue Farms faces direct exposure to the U.S. Farm Bill: 2023–24 federal commodity and crop insurance programs channel roughly $20–30 billion annually in support to grain producers, directly moderating corn and soybean prices that determine Perdue’s feed costs, its largest operating expense (feed typically ~40–45% of live production costs). Political shifts toward conservation or renewable mandates could raise feed prices by 5–15% and reshape margins for Perdue and its ~6,000 independent growers.

U.S. Department of Agriculture Regulatory Oversight

USDA mandates on food safety, inspection and labeling set binding protocols for Perdue, with FSIS inspections and HACCP compliance impacting processing; in 2024 USDA funding rose to $166.5 billion, supporting stricter enforcement and training programs that raise compliance costs for poultry processors.

Labor Migration and Immigration Policy

The meat processing sector relies heavily on immigrant labor; Perdue Farms employed ~24,000 workers in 2024 across processing and poultry with an industry average immigrant share near 32% (USDA/FAIR 2024), so restrictive immigration reform or cuts to H-2B/H-2A visa programs can cause acute labor shortages and raise recruitment costs.

Political shifts after 2024 proposals tightening border enforcement could increase Perdue’s hourly labor costs by an estimated 5–12% due to higher wages, overtime and training, affecting margins in a sector with low single-digit operating margins.

Perdue’s plant staffing resilience is therefore directly tied to federal and state labor and border policies, union/legislative actions, and visa program stability that influence turnover and productivity.

- Perdue workforce ~24,000 (2024)

- Industry immigrant share ~32% (2024)

- Potential labor cost impact 5–12% if visa access tightens

- Staffing tied to federal/state border and labor policy

Biosecurity and Disease Management Protocols

Government-led responses to outbreaks like HPAI require coordinated federal and state action; in 2022–2024 HPAI led to the depopulation of over 68 million domestic birds in the U.S., illustrating regulatory reach and disruption risk to Perdue’s supply chain and revenues.

State and federal agencies can restrict movements or order culling, creating immediate operational and political risk that can halt production and increase costs through lost inventory and containment measures.

Perdue collaborates with USDA, state departments of agriculture, and industry groups to implement biosecurity protocols protecting the national food supply and mitigating potential economic losses.

- 2022–24 HPAI: >68 million birds depopulated in U.S.

- Regulatory power: movement bans, mandatory culling

- Perdue action: active coordination with USDA and states

Perdue faces trade, HPAI and labor risks—18% exports, feed 40–45%, labor +5–12%

Perdue’s revenue and margins are sensitive to trade, tariffs, Farm Bill support, USDA regulation, HPAI controls, and immigration policy; exports ~18% of 2024 shipments, workforce ~24,000, feed = 40–45% of live production cost, 2022–24 HPAI depopulated >68M birds, potential labor cost rise 5–12% if visa tightening occurs.

| Metric | 2024/2022–24 |

|---|---|

| Export share | ~18% |

| Workforce | ~24,000 |

| Feed share | 40–45% |

| HPAI impact | >68M birds |

| Labor cost risk | +5–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Perdue Farms across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by relevant data and current trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE snapshot of Perdue Farms for quick reference in meetings or presentations, easily shareable and editable so teams can annotate region- or line-specific risks and opportunities.

Economic factors

Fluctuations in Commodity Feed Costs

Volatility in corn and soybean prices is a core economic risk for Perdue, with U.S. corn futures up ~28% year-over-year and soybean futures up ~18% as of Jan 2026, driving feed-cost inflation that can erode poultry margins; poor global harvests or export demand shocks can sharply raise production costs. Perdue uses futures and options hedging and forward contracts to stabilize input costs and protect consumer pricing, reducing feed-cost exposure.

Consumer Purchasing Power and Inflationary Pressures

Rising US inflation (CPI 3.4% in 2024) shifts shoppers toward cheaper proteins, boosting chicken demand vs beef; USDA noted 2024 retail chicken prices were ~15% lower than beef year-over-year, favoring Perdue.

Perdue’s pricing must offset feed and energy cost rises—corn and soybean meal up ~12% in 2024—while keeping affordability for median US household real wages stagnant.

Sustained downturns compress margins: Perdue reported 2024 operating margin pressure industry-wide, forcing trade promotions and cost controls to protect volume and market share.

Labor Market Dynamics and Wage Inflation

Competitive labor markets and rising state minimum wages—e.g., 2024 increases to $15+ in 10 states and multiple localities—raise Perdue Farms processing and distribution costs, squeezing margins as labor comprises ~20–30% of poultry processing expenses. Perdue must boost retention and pay, reflected in 2024 SG&A pressures and wage-driven labor cost inflation near 4–6% year-over-year. Automation investments are accelerating: capital expenditures rose in 2023–2024 to modernize plants and offset human capital inflation.

Energy and Logistics Cost Volatility

Fuel and energy prices materially affect Perdue Farms’ COGS; diesel rose ~15% in 2024 vs 2023, pushing transport expenses higher across its 50-state network.

Global oil volatility in 2024-2025 raised shipping rates ~10–20%, increasing inbound feed and outbound product costs for Perdue’s integrated supply chain.

Efficiency programs—route optimization, on-site solar (Perdue reported installing >10 MW by 2024) and HVAC upgrades—are key to protecting margins.

- Diesel +15% (2024), shipping rates +10–20% (2024–25)

- Perdue installed >10 MW solar by 2024

- Logistics and energy initiatives directly reduce COGS pressure

Interest Rates and Capital Investment Debt

Perdue Farms, which invests heavily in processing and cold-chain infrastructure, is sensitive to the Federal Reserve’s rate moves; the Fed funds rate rose to a target range of 5.25–5.50% by Dec 2024, raising borrowing costs for capital projects.

Higher rates increase debt service on new plant expansions and tech integrations, potentially delaying projects and compressing returns on investments.

Perdue’s ability to finance long-term growth depends on the prevailing macro rate environment and access to credit markets.

- Fed funds 5.25–5.50% (Dec 2024)

- Higher rates raise debt service, slow capex

- Capital-intensive projects at risk of delay

Perdue Battles Rising Feed, Fuel & Rates with Hedging, Solar >10MW and Automation

Feed, energy, labor and rates drove 2024–25 cost pressure: corn +28% YoY (Jan 2026), soy +18%, diesel +15% (2024), shipping +10–20% (2024–25), Fed funds 5.25–5.50% (Dec 2024); Perdue hedges inputs, invests >10 MW solar, automation and route optimization to protect margins and capex flexibility.

| Metric | Value |

|---|---|

| Corn futures | +28% YoY |

| Soy futures | +18% YoY |

| Diesel (2024) | +15% |

| Shipping | +10–20% |

| Fed funds | 5.25–5.50% |

| Solar installed | >10 MW |

What You See Is What You Get

Perdue Farms PESTLE Analysis

The preview shown here is the exact Perdue Farms PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no surprises. The content, layout, and structure visible in the preview are identical to the downloadable file you’ll get immediately after payment. Everything displayed is part of the final, professionally structured report.