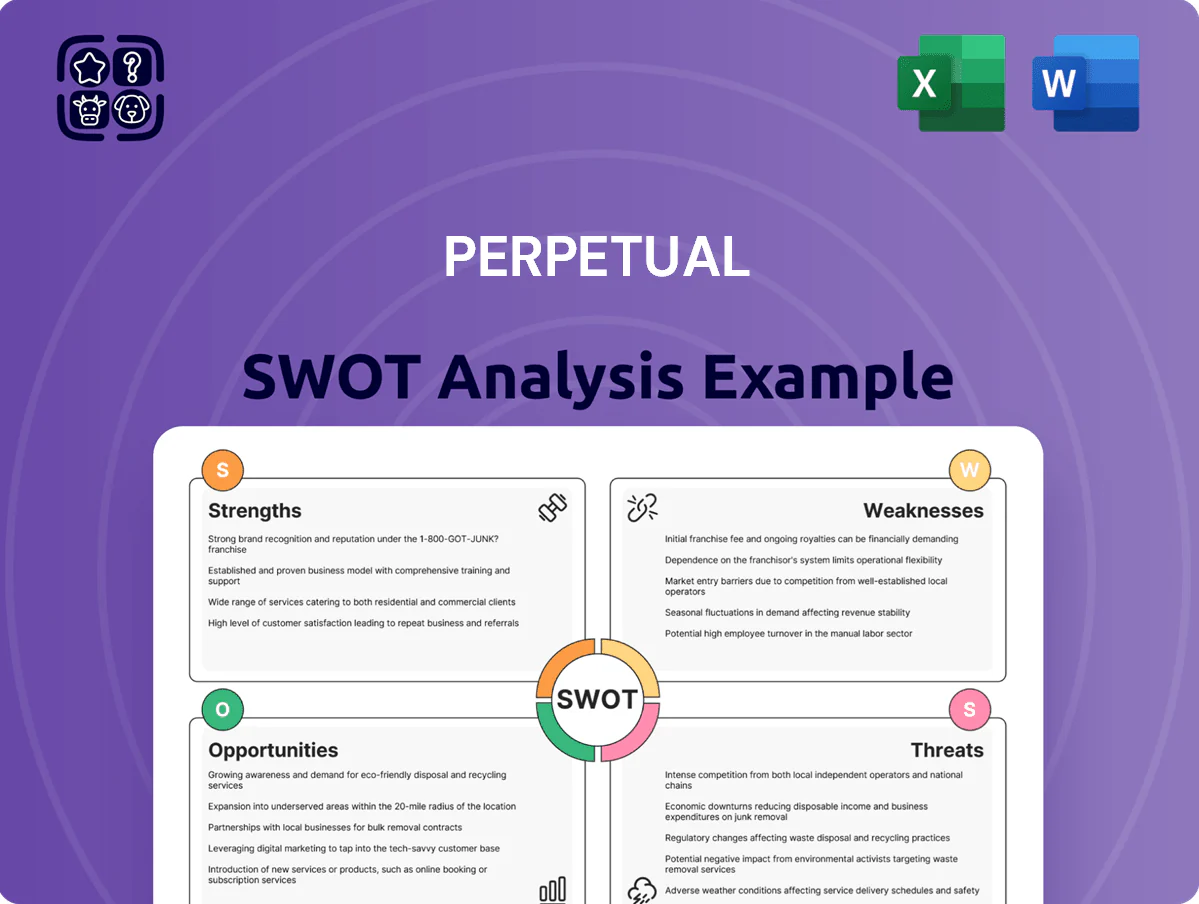

Perpetual SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Perpetual’s snapshot reveals core strengths, market risks, and strategic opportunities—yet the full SWOT delivers the clarity you need to act. Purchase the complete analysis for an investor-ready Word report and editable Excel matrix, packed with research-backed insights, tactical recommendations, and financial context to support planning, pitching, or portfolio decisions.

Strengths

Global Multi-Boutique Model

Perpetual’s global multi-boutique model houses brands like Pendal, Barrow Hanley, and J O Hambro, letting each boutique keep its distinct investment process and culture while accessing a shared global distribution platform. This mix boosted group FUM to about A$150bn by end-2025, and increased institutional win-rate: 18% more mandates year-over-year in 2024–25. The setup widens alpha-seeking strategy choices for institutional clients.

Strong Brand Equity and Reputation

Perpetual, founded in 1886, leverages 137+ years of history to hold strong brand equity in Australia and rising global recognition; its FY2024 group funds under management (FUM) of A$73.6bn and 87% institutional retention rate underscore market trust.

The firm is tied to fiduciary excellence and disciplined value investing, helping secure long-term mandates such as the A$12bn+ Perpetual Wholesale Income Fund and lowering client churn during volatility.

This reputation raises barriers to entry for smaller rivals and supported a 2024 net inflow rebound of A$1.1bn amid market stress, reinforcing client confidence.

Geographic Revenue Diversification

Following the 2021 integration of Pendal Group, Perpetual shifted from an Australia-centric base to a diversified footprint across the US, UK and Europe; by late 2025 international AUM represented about 45% of total AUM (≈A$70bn of A$155bn), reducing reliance on the domestic market.

Enhanced Strategic Focus

- 100% capital to investment & distribution

- FY25 AUM ~AUD 75.3bn

- Forward P/E ~11.2x post-deal

- Clear pure-play valuation

Robust Institutional Distribution Network

Perpetual maintains long-term relationships with major global institutional clients, including pension funds, endowments and sovereign wealth funds managing over US$2.5trn combined, which drives stable fee income and high-retention mandates.

Its distribution teams sit in London, New York, Sydney and Singapore, enabling rapid cross-border scaling: 2024 product launches saw AUM ramp to A$4.2bn within 12 months on average.

- Access to >US$2.5trn institutional pool

- Teams in 4 hubs: London, NY, Sydney, Singapore

- 2024 launches averaged A$4.2bn AUM in 12 months

Perpetual: 137‑Year Asset Manager — A$75.3bn AUM, A$150bn FUM, 87% Institutional Retention

Perpetual’s multi-boutique model, pure-play asset manager focus and 137‑year brand drive scale: FY25 AUM ~A$75.3bn, group FUM ≈A$150bn (end‑2025), 87% institutional retention, 18% lift in mandates 2024–25, forward P/E ~11.2x; global hubs (London, NY, Sydney, Singapore) access >US$2.5trn institutional pool.

| Metric | Value |

|---|---|

| FY25 AUM | A$75.3bn |

| Group FUM (end‑2025) | A$150bn |

| Institutional retention | 87% |

| Mandate win ↑ (24–25) | 18% |

| Forward P/E | ~11.2x |

What is included in the product

Provides a concise SWOT overview of Perpetual, highlighting its core strengths and weaknesses while identifying key market opportunities and external threats shaping its strategic outlook.

Perpetual SWOT Analysis auto-updates and centralizes strategic inputs to reduce manual tracking, giving teams a reliable, real-time snapshot for faster, aligned decision-making.

Weaknesses

Revenue Sensitivity to Market Cycles

As a pure-play asset manager, Perpetual’s earnings track global equity and bond markets: a 20% S&P/ASX 200 drop in 2022 cut AUM by ~18% and fees fell ~15% y/y, showing high sensitivity.

A 2023 MSCI World 12% decline would similarly reduce management fees and cause earnings volatility; empirical beta to markets was ~0.9 over 2019–2024.

After selling corporate trust services in 2021, Perpetual lost ~A$120m of steady fee income, removing a non-market buffer and raising profit cyclicality.

Active Management Outflow Pressures

Perpetual is still concentrated in active strategies that lost about A$18bn to passive funds industry-wide in 2024, leaving the firm exposed as passive market share reached ~40% of Australian retail AUM by end-2024.

If boutiques miss 3- or 5-year benchmarks, redemption risk rises sharply—historically 25–40% of flows retracted within 12 months after sustained underperformance.

Maintaining alpha is harder: global equity active managers’ median 5-year excess return fell under 0.5% by Dec 2024, pressuring Perpetual’s teams to outperform at lower margins.

Loss of Diversified Earnings Streams

The sale of Perpetual’s Wealth Management and Corporate Trust arms removed a key internal hedge, cutting sticky, recurring fee income that had insulated revenues from market swings; those divestments reduced fee-based revenue by about A$180m annually as of 2024, increasing reliance on performance-linked investment income.

Without those businesses, Perpetual’s earnings mix shifted toward market-sensitive returns, raising measured volatility; by end-2025 the firm’s operating leverage and beta to equity markets is materially higher versus its 2019–21 profile.

High Operational Cost Base

Perpetual’s multi-boutique model drives high operating costs—compliance, IT, and top-tier PM pay—pushing FY2024 operating margin down; group SG&A rose 6.2% to AU$420m in 2024, squeezing margins when AUM growth is flat.

Despite AU$3–5m annual cost cuts in 2023–24, the firm must match hedge fund/PE pay to retain talent, raising fixed compensation and pressuring profits during stagnant AUM.

- SG&A AU$420m (2024)

- SG&A +6.2% YoY

- Cost cuts AU$3–5m (2023–24)

- High pay keeps churn risk vs hedge funds/PE

Integration and Cultural Complexity

- 28% staff report cultural misalignment

- 12.4% voluntary exits in 2025

- $1.1bn net outflows Q3 2025

Perpetual under pressure: AUM plunge, A$180m fee loss, A$1.1bn outflows

Perpetual’s weaknesses: high market sensitivity (AUM down ~18% after ASX200 -20% in 2022; emp. beta ~0.9), loss of A$180m recurring fees from divestments, active-only exposure as passive hit ~40% retail AUM (A$18bn shift 2024), SG&A AU$420m (+6.2% YoY), cultural misalignment 28% and voluntary exits 12.4% causing Q3 2025 outflows A$1.1bn.

| Metric | Value |

|---|---|

| AUM sensitivity | -18% (2022) |

| Lost recurring fees | A$180m |

| SG&A | AU$420m (+6.2%) |

| Staff misalign/exits | 28% / 12.4% |

| Q3 2025 outflows | A$1.1bn |

Preview Before You Purchase

Perpetual SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Perpetual’s snapshot reveals core strengths, market risks, and strategic opportunities—yet the full SWOT delivers the clarity you need to act. Purchase the complete analysis for an investor-ready Word report and editable Excel matrix, packed with research-backed insights, tactical recommendations, and financial context to support planning, pitching, or portfolio decisions.

Strengths

Global Multi-Boutique Model

Perpetual’s global multi-boutique model houses brands like Pendal, Barrow Hanley, and J O Hambro, letting each boutique keep its distinct investment process and culture while accessing a shared global distribution platform. This mix boosted group FUM to about A$150bn by end-2025, and increased institutional win-rate: 18% more mandates year-over-year in 2024–25. The setup widens alpha-seeking strategy choices for institutional clients.

Strong Brand Equity and Reputation

Perpetual, founded in 1886, leverages 137+ years of history to hold strong brand equity in Australia and rising global recognition; its FY2024 group funds under management (FUM) of A$73.6bn and 87% institutional retention rate underscore market trust.

The firm is tied to fiduciary excellence and disciplined value investing, helping secure long-term mandates such as the A$12bn+ Perpetual Wholesale Income Fund and lowering client churn during volatility.

This reputation raises barriers to entry for smaller rivals and supported a 2024 net inflow rebound of A$1.1bn amid market stress, reinforcing client confidence.

Geographic Revenue Diversification

Following the 2021 integration of Pendal Group, Perpetual shifted from an Australia-centric base to a diversified footprint across the US, UK and Europe; by late 2025 international AUM represented about 45% of total AUM (≈A$70bn of A$155bn), reducing reliance on the domestic market.

Enhanced Strategic Focus

- 100% capital to investment & distribution

- FY25 AUM ~AUD 75.3bn

- Forward P/E ~11.2x post-deal

- Clear pure-play valuation

Robust Institutional Distribution Network

Perpetual maintains long-term relationships with major global institutional clients, including pension funds, endowments and sovereign wealth funds managing over US$2.5trn combined, which drives stable fee income and high-retention mandates.

Its distribution teams sit in London, New York, Sydney and Singapore, enabling rapid cross-border scaling: 2024 product launches saw AUM ramp to A$4.2bn within 12 months on average.

- Access to >US$2.5trn institutional pool

- Teams in 4 hubs: London, NY, Sydney, Singapore

- 2024 launches averaged A$4.2bn AUM in 12 months

Perpetual: 137‑Year Asset Manager — A$75.3bn AUM, A$150bn FUM, 87% Institutional Retention

Perpetual’s multi-boutique model, pure-play asset manager focus and 137‑year brand drive scale: FY25 AUM ~A$75.3bn, group FUM ≈A$150bn (end‑2025), 87% institutional retention, 18% lift in mandates 2024–25, forward P/E ~11.2x; global hubs (London, NY, Sydney, Singapore) access >US$2.5trn institutional pool.

| Metric | Value |

|---|---|

| FY25 AUM | A$75.3bn |

| Group FUM (end‑2025) | A$150bn |

| Institutional retention | 87% |

| Mandate win ↑ (24–25) | 18% |

| Forward P/E | ~11.2x |

What is included in the product

Provides a concise SWOT overview of Perpetual, highlighting its core strengths and weaknesses while identifying key market opportunities and external threats shaping its strategic outlook.

Perpetual SWOT Analysis auto-updates and centralizes strategic inputs to reduce manual tracking, giving teams a reliable, real-time snapshot for faster, aligned decision-making.

Weaknesses

Revenue Sensitivity to Market Cycles

As a pure-play asset manager, Perpetual’s earnings track global equity and bond markets: a 20% S&P/ASX 200 drop in 2022 cut AUM by ~18% and fees fell ~15% y/y, showing high sensitivity.

A 2023 MSCI World 12% decline would similarly reduce management fees and cause earnings volatility; empirical beta to markets was ~0.9 over 2019–2024.

After selling corporate trust services in 2021, Perpetual lost ~A$120m of steady fee income, removing a non-market buffer and raising profit cyclicality.

Active Management Outflow Pressures

Perpetual is still concentrated in active strategies that lost about A$18bn to passive funds industry-wide in 2024, leaving the firm exposed as passive market share reached ~40% of Australian retail AUM by end-2024.

If boutiques miss 3- or 5-year benchmarks, redemption risk rises sharply—historically 25–40% of flows retracted within 12 months after sustained underperformance.

Maintaining alpha is harder: global equity active managers’ median 5-year excess return fell under 0.5% by Dec 2024, pressuring Perpetual’s teams to outperform at lower margins.

Loss of Diversified Earnings Streams

The sale of Perpetual’s Wealth Management and Corporate Trust arms removed a key internal hedge, cutting sticky, recurring fee income that had insulated revenues from market swings; those divestments reduced fee-based revenue by about A$180m annually as of 2024, increasing reliance on performance-linked investment income.

Without those businesses, Perpetual’s earnings mix shifted toward market-sensitive returns, raising measured volatility; by end-2025 the firm’s operating leverage and beta to equity markets is materially higher versus its 2019–21 profile.

High Operational Cost Base

Perpetual’s multi-boutique model drives high operating costs—compliance, IT, and top-tier PM pay—pushing FY2024 operating margin down; group SG&A rose 6.2% to AU$420m in 2024, squeezing margins when AUM growth is flat.

Despite AU$3–5m annual cost cuts in 2023–24, the firm must match hedge fund/PE pay to retain talent, raising fixed compensation and pressuring profits during stagnant AUM.

- SG&A AU$420m (2024)

- SG&A +6.2% YoY

- Cost cuts AU$3–5m (2023–24)

- High pay keeps churn risk vs hedge funds/PE

Integration and Cultural Complexity

- 28% staff report cultural misalignment

- 12.4% voluntary exits in 2025

- $1.1bn net outflows Q3 2025

Perpetual under pressure: AUM plunge, A$180m fee loss, A$1.1bn outflows

Perpetual’s weaknesses: high market sensitivity (AUM down ~18% after ASX200 -20% in 2022; emp. beta ~0.9), loss of A$180m recurring fees from divestments, active-only exposure as passive hit ~40% retail AUM (A$18bn shift 2024), SG&A AU$420m (+6.2% YoY), cultural misalignment 28% and voluntary exits 12.4% causing Q3 2025 outflows A$1.1bn.

| Metric | Value |

|---|---|

| AUM sensitivity | -18% (2022) |

| Lost recurring fees | A$180m |

| SG&A | AU$420m (+6.2%) |

| Staff misalign/exits | 28% / 12.4% |

| Q3 2025 outflows | A$1.1bn |

Preview Before You Purchase

Perpetual SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.