PetroChina Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

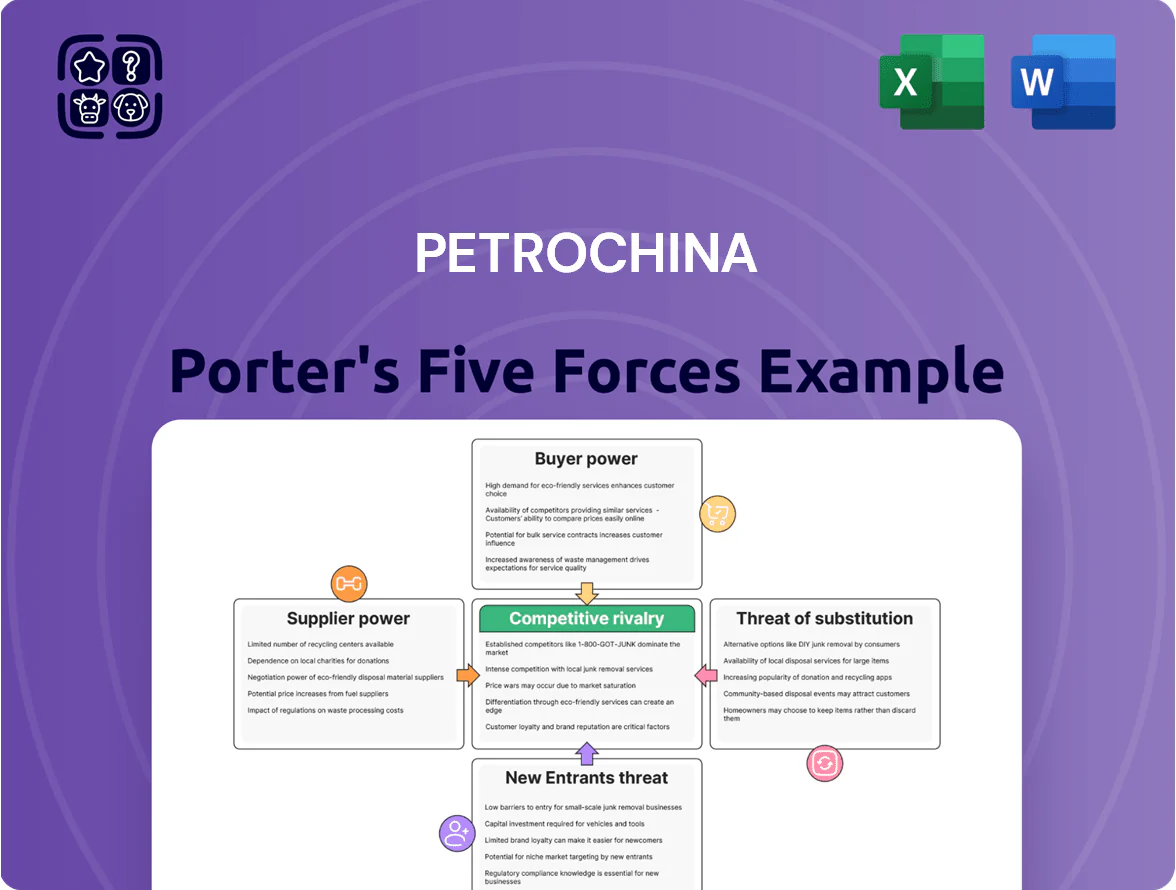

PetroChina faces moderate supplier power, significant regulatory and geopolitical pressures, and intense rivalry from both national and international oil majors, while barriers to entry remain high but technological shifts and renewables pose growing substitute threats; this snapshot highlights key tensions shaping margin resilience and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PetroChina’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Specialized Oilfield Service Providers

PetroChina depends on advanced services for deepwater and unconventional extraction, with roughly 18% of 2024 upstream capex ($6.3B of $35B group capex) tied to high-tech drilling and completion contracts.

Internal subsidiaries handle many projects, but complex exploration still sources international suppliers—Schlumberger, Halliburton equivalents—holding proprietary tech.

These specialized suppliers exert moderate leverage due to patents and scarce expert crews, keeping service margins around 25–35% in 2024 offshore tenders.

Influence of International Equipment Manufacturers

The procurement of high-tech drilling rigs and refinery modules relies on few global makers (e.g., Schlumberger, Halliburton, Siemens), giving suppliers notable leverage; global rig OEM concentration saw top five firms hold ~62% market share in 2024. As PetroChina scales carbon capture and hydrogen projects by late 2025, scarce green-tech vendors raise supplier bargaining power. Still, PetroChina’s 2024 capex of RMB 160 billion and huge purchase volumes secure multi-year contracts and discounts that partly offset supplier leverage.

Internal Group Synergies with CNPC

CNPC (China National Petroleum Corporation) supplies PetroChina with crude, chemicals, drilling rigs and pipeline services, creating vertical integration that cut external supplier risk; in 2024 CNPC accounted for roughly 62% of PetroChina’s upstream inputs, stabilizing costs and volumes. This internal sourcing reduces third-party hold-up risk, yields more predictable unit production costs (2024 upstream cash OPEX ~US$9.8/boe) and limits independent suppliers’ bargaining power.

Global Commodity Price Volatility

Suppliers of crude and feedstocks price on global markets beyond PetroChina's control; Brent averaged 86.3 USD/bbl in 2025 YTD, raising feedstock costs and squeezing refining margins.

As a major crude importer, PetroChina is exposed to OPEC+ cuts and supply moves by Russia and the US, which drove a 7–12% swing in Asian crude premiums in 2025 and hit refining throughput economics.

External price dependence raises supplier power, directly lifting COGS and eroding refinery GRM (gross refinery margin) which fell to ~3.8 USD/bbl in Q1 2025.

- Brent 2025 YTD 86.3 USD/bbl

- Asian crude premium volatility 7–12% (2025)

- GRM ~3.8 USD/bbl Q1 2025

Labor and Specialized Engineering Talent

The demand for petroleum engineers and data scientists for digital oilfield work creates tight labor markets; China reported a 12% shortage in energy-related STEM hires in 2024, raising wage pressure for PetroChina.

Scarcity of renewables-integration specialists gives suppliers of talent leverage as PetroChina shifts to low-carbon projects; industry hiring premiums reached 18% in 2024 for green-energy engineers.

PetroChina must match market pay and clear career paths—2024 training budgets rose 9% across Chinese NOCs—to retain skills vital for multi-energy operations.

- 12% STEM hire gap (China, 2024)

- 18% wage premium for green-energy engineers (2024)

- 9% rise in NOC training budgets (2024)

Deepwater suppliers boost margins as CNPC integration and higher Brent raise feedstock risk

Suppliers have moderate bargaining power: proprietary deepwater tech and concentrated rig OEMs (top-5 = 62% market share, 2024) lift margins to 25–35% on offshore services, while CNPC vertical integration (62% of upstream inputs, 2024) and PetroChina’s RMB160bn capex (2024) cut external risk; Brent 2025 YTD 86.3 USD/bbl and Q1 2025 GRM ~3.8 USD/bbl increase feedstock exposure.

| Metric | Value |

|---|---|

| Top-5 rig OEM share (2024) | 62% |

| Offshore service margins (2024) | 25–35% |

| CNPC share of inputs (2024) | 62% |

| PetroChina capex (2024) | RMB160bn |

| Brent (2025 YTD) | 86.3 USD/bbl |

| GRM Q1 2025 | 3.8 USD/bbl |

What is included in the product

Tailored Porter’s Five Forces analysis for PetroChina that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise Porter's Five Forces summary for PetroChina—distilling competitive pressures into a one-sheet view to speed strategic decisions and investor briefings.

Customers Bargaining Power

State-Regulated Pricing Mechanisms

The National Development and Reform Commission (NDRC) sets retail prices for refined oil and natural gas, capping PetroChina’s ability to fully pass cost rises; in 2024 regulated fuel margins compressed by about 6–8% industrywide, trimming downstream EBITDA.

With China’s 2023 retail fuel price bands and 2024 gas subsidy policies, the state effectively proxies consumers, limiting individual bargaining but forcing PetroChina to absorb volatility—state priorities lean to social stability over higher corporate margins.

Industrial and Manufacturing Demand

Large industrial clients and chemical makers account for roughly 60% of PetroChina’s 2024 natural gas and petrochemical volumes, so these bulk buyers can secure long-term contracts with volume clauses and indexed pricing; in 2024 PetroChina reported gas sales of 370 billion cubic meters across China, reflecting this exposure. Their option to switch to coal, renewables, or relocate capacity gives them moderate bargaining power, pressuring margins during commodity price declines.

Aviation and Logistics Sector Leverage

Retail Consumer Sensitivity and Brand Loyalty

Individual motorists show high price sensitivity but little direct bargaining power; by 2025 over 70% of urban Chinese drivers use mobile apps to compare fuel prices within 5 km, shrinking price stickiness.

Digital payment and loyalty platforms (PetroChina’s DCC app had ~120 million users in 2024) make switching to Sinopec or independents easier, forcing PetroChina to boost non-fuel retail and convenience services to protect margins.

Investments focus on forecourt retail, foodservice, and loyalty discounts; PetroChina reported a 15% rise in non-fuel revenue per station in 2023, highlighting the shift.

- >70% drivers use price-comparison apps (2025 est.)

- PetroChina DCC ~120M users (2024)

- Non-fuel revenue per station +15% (2023)

- Higher retention via convenience & loyalty

Transition to Alternative Energy Vehicles

The rapid rise of electric vehicles in China—EV sales hit 8.1 million units in 2024, ~40% of new car sales—lets consumers exit the petroleum market, shrinking gasoline demand and increasing bargaining power of remaining fuel buyers.

As EV adoption narrows PetroChina’s total addressable market, the company is installing >60,000 charging piles and planning hydrogen refueling pilots in 2025 to retain customers and diversify revenue.

- EVs 2024: 8.1M units (~40% new sales)

- Gasoline market shrinks, buyers gain leverage

- PetroChina: >60,000 charging piles installed (2024)

- Hydrogen refueling pilots planned for 2025

Customers’ clout rises as price caps and EV/retail shifts push fuel to services

Customers hold moderate-to-high bargaining power: the state caps retail prices (NDRC) reducing pass-through; large industrials and airlines (≈12–15% refined sales) negotiate volume-indexed contracts; retail motorists are price-sensitive but fragmented; EV growth (8.1M sales in 2024) and PetroChina’s DCC (≈120M users in 2024) and >60,000 chargers shift revenue to non-fuel services.

| Metric | 2023–2025 |

|---|---|

| Gas sales | 370 bcm (2024) |

| Refined fuel share—major buyers | 12–15% (2024) |

| DCC users | ≈120M (2024) |

| EV sales | 8.1M (2024) |

| Charging piles | >60,000 installed (2024) |

Same Document Delivered

PetroChina Porter's Five Forces Analysis

This preview shows the exact PetroChina Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or sample pages; the full, professionally formatted document is ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

PetroChina faces moderate supplier power, significant regulatory and geopolitical pressures, and intense rivalry from both national and international oil majors, while barriers to entry remain high but technological shifts and renewables pose growing substitute threats; this snapshot highlights key tensions shaping margin resilience and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PetroChina’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Specialized Oilfield Service Providers

PetroChina depends on advanced services for deepwater and unconventional extraction, with roughly 18% of 2024 upstream capex ($6.3B of $35B group capex) tied to high-tech drilling and completion contracts.

Internal subsidiaries handle many projects, but complex exploration still sources international suppliers—Schlumberger, Halliburton equivalents—holding proprietary tech.

These specialized suppliers exert moderate leverage due to patents and scarce expert crews, keeping service margins around 25–35% in 2024 offshore tenders.

Influence of International Equipment Manufacturers

The procurement of high-tech drilling rigs and refinery modules relies on few global makers (e.g., Schlumberger, Halliburton, Siemens), giving suppliers notable leverage; global rig OEM concentration saw top five firms hold ~62% market share in 2024. As PetroChina scales carbon capture and hydrogen projects by late 2025, scarce green-tech vendors raise supplier bargaining power. Still, PetroChina’s 2024 capex of RMB 160 billion and huge purchase volumes secure multi-year contracts and discounts that partly offset supplier leverage.

Internal Group Synergies with CNPC

CNPC (China National Petroleum Corporation) supplies PetroChina with crude, chemicals, drilling rigs and pipeline services, creating vertical integration that cut external supplier risk; in 2024 CNPC accounted for roughly 62% of PetroChina’s upstream inputs, stabilizing costs and volumes. This internal sourcing reduces third-party hold-up risk, yields more predictable unit production costs (2024 upstream cash OPEX ~US$9.8/boe) and limits independent suppliers’ bargaining power.

Global Commodity Price Volatility

Suppliers of crude and feedstocks price on global markets beyond PetroChina's control; Brent averaged 86.3 USD/bbl in 2025 YTD, raising feedstock costs and squeezing refining margins.

As a major crude importer, PetroChina is exposed to OPEC+ cuts and supply moves by Russia and the US, which drove a 7–12% swing in Asian crude premiums in 2025 and hit refining throughput economics.

External price dependence raises supplier power, directly lifting COGS and eroding refinery GRM (gross refinery margin) which fell to ~3.8 USD/bbl in Q1 2025.

- Brent 2025 YTD 86.3 USD/bbl

- Asian crude premium volatility 7–12% (2025)

- GRM ~3.8 USD/bbl Q1 2025

Labor and Specialized Engineering Talent

The demand for petroleum engineers and data scientists for digital oilfield work creates tight labor markets; China reported a 12% shortage in energy-related STEM hires in 2024, raising wage pressure for PetroChina.

Scarcity of renewables-integration specialists gives suppliers of talent leverage as PetroChina shifts to low-carbon projects; industry hiring premiums reached 18% in 2024 for green-energy engineers.

PetroChina must match market pay and clear career paths—2024 training budgets rose 9% across Chinese NOCs—to retain skills vital for multi-energy operations.

- 12% STEM hire gap (China, 2024)

- 18% wage premium for green-energy engineers (2024)

- 9% rise in NOC training budgets (2024)

Deepwater suppliers boost margins as CNPC integration and higher Brent raise feedstock risk

Suppliers have moderate bargaining power: proprietary deepwater tech and concentrated rig OEMs (top-5 = 62% market share, 2024) lift margins to 25–35% on offshore services, while CNPC vertical integration (62% of upstream inputs, 2024) and PetroChina’s RMB160bn capex (2024) cut external risk; Brent 2025 YTD 86.3 USD/bbl and Q1 2025 GRM ~3.8 USD/bbl increase feedstock exposure.

| Metric | Value |

|---|---|

| Top-5 rig OEM share (2024) | 62% |

| Offshore service margins (2024) | 25–35% |

| CNPC share of inputs (2024) | 62% |

| PetroChina capex (2024) | RMB160bn |

| Brent (2025 YTD) | 86.3 USD/bbl |

| GRM Q1 2025 | 3.8 USD/bbl |

What is included in the product

Tailored Porter’s Five Forces analysis for PetroChina that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise Porter's Five Forces summary for PetroChina—distilling competitive pressures into a one-sheet view to speed strategic decisions and investor briefings.

Customers Bargaining Power

State-Regulated Pricing Mechanisms

The National Development and Reform Commission (NDRC) sets retail prices for refined oil and natural gas, capping PetroChina’s ability to fully pass cost rises; in 2024 regulated fuel margins compressed by about 6–8% industrywide, trimming downstream EBITDA.

With China’s 2023 retail fuel price bands and 2024 gas subsidy policies, the state effectively proxies consumers, limiting individual bargaining but forcing PetroChina to absorb volatility—state priorities lean to social stability over higher corporate margins.

Industrial and Manufacturing Demand

Large industrial clients and chemical makers account for roughly 60% of PetroChina’s 2024 natural gas and petrochemical volumes, so these bulk buyers can secure long-term contracts with volume clauses and indexed pricing; in 2024 PetroChina reported gas sales of 370 billion cubic meters across China, reflecting this exposure. Their option to switch to coal, renewables, or relocate capacity gives them moderate bargaining power, pressuring margins during commodity price declines.

Aviation and Logistics Sector Leverage

Retail Consumer Sensitivity and Brand Loyalty

Individual motorists show high price sensitivity but little direct bargaining power; by 2025 over 70% of urban Chinese drivers use mobile apps to compare fuel prices within 5 km, shrinking price stickiness.

Digital payment and loyalty platforms (PetroChina’s DCC app had ~120 million users in 2024) make switching to Sinopec or independents easier, forcing PetroChina to boost non-fuel retail and convenience services to protect margins.

Investments focus on forecourt retail, foodservice, and loyalty discounts; PetroChina reported a 15% rise in non-fuel revenue per station in 2023, highlighting the shift.

- >70% drivers use price-comparison apps (2025 est.)

- PetroChina DCC ~120M users (2024)

- Non-fuel revenue per station +15% (2023)

- Higher retention via convenience & loyalty

Transition to Alternative Energy Vehicles

The rapid rise of electric vehicles in China—EV sales hit 8.1 million units in 2024, ~40% of new car sales—lets consumers exit the petroleum market, shrinking gasoline demand and increasing bargaining power of remaining fuel buyers.

As EV adoption narrows PetroChina’s total addressable market, the company is installing >60,000 charging piles and planning hydrogen refueling pilots in 2025 to retain customers and diversify revenue.

- EVs 2024: 8.1M units (~40% new sales)

- Gasoline market shrinks, buyers gain leverage

- PetroChina: >60,000 charging piles installed (2024)

- Hydrogen refueling pilots planned for 2025

Customers’ clout rises as price caps and EV/retail shifts push fuel to services

Customers hold moderate-to-high bargaining power: the state caps retail prices (NDRC) reducing pass-through; large industrials and airlines (≈12–15% refined sales) negotiate volume-indexed contracts; retail motorists are price-sensitive but fragmented; EV growth (8.1M sales in 2024) and PetroChina’s DCC (≈120M users in 2024) and >60,000 chargers shift revenue to non-fuel services.

| Metric | 2023–2025 |

|---|---|

| Gas sales | 370 bcm (2024) |

| Refined fuel share—major buyers | 12–15% (2024) |

| DCC users | ≈120M (2024) |

| EV sales | 8.1M (2024) |

| Charging piles | >60,000 installed (2024) |

Same Document Delivered

PetroChina Porter's Five Forces Analysis

This preview shows the exact PetroChina Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or sample pages; the full, professionally formatted document is ready for instant download and use.