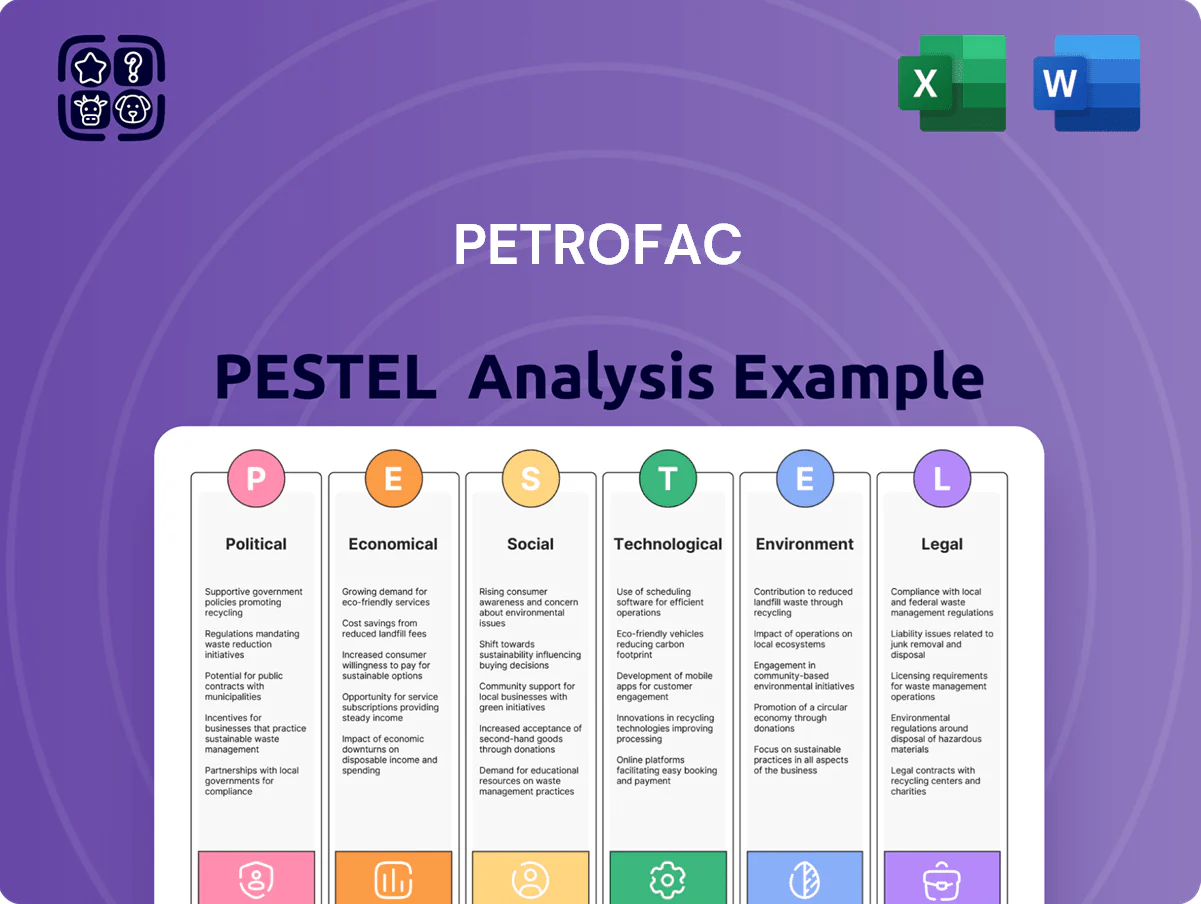

Petrofac PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Petrofac PESTLE Analysis—concise, timely and targeted to reveal the political, economic, social, technological, legal and environmental forces shaping the company’s trajectory; buy the full report to access actionable insights, risk forecasts and ready-to-use slides that accelerate your investment or strategy work.

Political factors

Geopolitical stability in the Middle East

Petrofac’s large GCC footprint—over 40% of 2024 revenues sourced from Middle East operations—makes regional geopolitical stability critical for multi-year contract delivery.

Government initiatives like Saudi Vision 2030, with planned $1.6 trillion investment through 2030, expand opportunities for EPC and services firms including Petrofac.

Escalations risk supply-chain disruptions and timeline slippages for NOC clients; 2023–24 project delays in the region pushed capital spend timelines by up to 12–18 months in some cases.

Close strategic alignment with host-government priorities is vital to secure and retain multi-billion-dollar framework agreements and mitigate political risk.

Energy security and sovereignty policies

The EU and UK push for energy independence—EU aiming 45% renewable share by 2030 and the UK targeting 50GW offshore wind by 2030—drives demand for domestic infrastructure, boosting opportunities for Petrofac in both renewables and native oil and gas projects; governments’ security-first policies have increased licensing scrutiny and local-content rules, with UK North Sea licensing rounds in 2023–24 awarding ~150 blocks, shaping project timing and capex decisions for suppliers like Petrofac.

In-Country Value and nationalization requirements

Many jurisdictions where Petrofac operates enforce strict In-Country Value and nationalization rules—e.g., UAE ADNOC and Saudi NCP require local content levels often exceeding 40–70%—forcing the firm to prioritize local hiring, regional supply-chain investment, and technical-transfer programs.

International sanctions and trade barriers

The complex web of international sanctions continues to curb energy services, with 2024 UN/US/EU measures affecting operations in Russia, Iran and Venezuela—regions that accounted for an estimated 8–12% of sector contracts pre-sanctions.

Trade barriers and tech export controls can block Petrofac from delivering specialized engineering solutions, squeezing revenue streams—global oilfield services trade fell ~5% YoY in 2024.

Continuous diplomatic monitoring is required to ensure compliance and avoid reputational fines; 2023–24 enforcement actions led to multi‑million-dollar penalties across the industry.

- Sanctions restrict access to ~8–12% historical contract exposure

- 2024 OFS trade down ~5% YoY limits market reach

- Enforcement risk: multi‑million fines in 2023–24

- Requires flexible ops to pivot from sensitive regions

Governmental support for energy transition

Public policy and subsidies for green hydrogen, carbon capture and offshore wind underpin Petrofac New Energy; EU allocated €210bn for hydrogen and renewables in 2024–27, boosting project pipelines.

Net Zero commitments expand grants and streamlined permitting, with 2030 targets raising green contracts—UK’s Ten Point Plan mobilised £12bn and CCUS clusters pledge significant market volume.

Government changes can cut or accelerate funding; recent 2024 election shifts in EU states altered subsidy timelines, requiring Petrofac agility.

Petrofac must match capabilities to national tech preferences—e.g., Norway CCUS, UAE hydrogen, UK offshore wind—to secure contracts and co-financing.

- EU €210bn hydrogen/renewables 2024–27

- UK £12bn Ten Point Plan

- National tech focus: Norway CCUS, UAE hydrogen, UK offshore wind

- Political shifts affect subsidy timing and scale

Petrofac: GCC dependence, Vision 2030 chances vs sanctions-driven compliance drag

Petrofac’s 40%+ 2024 revenue exposure to GCC ties contract delivery to regional stability; Saudi Vision 2030’s $1.6tr pipeline and EU/UK renewables targets (EU 45% by 2030; UK 50GW offshore) expand opportunities but raise local-content and licensing complexity; sanctions trimmed ~8–12% historic contract exposure and OFS trade fell ~5% YoY in 2024, increasing enforcement and compliance costs.

| Metric | Value (2024/24) |

|---|---|

| GCC revenue share | 40%+ |

| Saudi Vision 2030 spend | $1.6tr to 2030 |

| Sanctions impact | 8–12% contract exposure |

| OFS trade YoY | -5% |

| EU renewables target | 45% by 2030 |

| UK offshore wind | 50GW by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Petrofac across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend analysis to identify threats, opportunities, and forward-looking scenarios for executives and investors.

Condenses Petrofac’s PESTLE into a clear, shareable one-page that highlights regulatory, geopolitical, and market risks to support quick decision-making in meetings and client reports.

Economic factors

Volatility in global energy prices

The financial health of Petrofac is tightly linked to client CAPEX, which fell industry-wide after the 2014–2016 downturn and again in 2020; IEA data show upstream investment was about $350bn in 2023, with 2024 estimates near $370bn, making project flows sensitive to oil prices. Sustained price volatility—Brent ranged $70–$95/bbl in 2024—can defer FIDs on multi-year projects. Higher prices boost E&P spending but raise construction material costs, contributing to global steel and commodity inflation of roughly 10–15% in 2023–24. Petrofac mitigates exposure via diversified contract structures and expanding renewable-energy services, which accounted for an increasing share of orderbook in 2024.

Interest rate environment and financing costs

As a capital-intensive EPC firm that completed major restructuring, Petrofac's debt service costs are sensitive to prevailing rates; UK base rates peaking at 5.25% in 2024 raised annual interest expenses materially on outstanding borrowings of about $1.2bn (2024). High rates also inflate costs for performance bonds and guarantees, which can add 50–200 basis points to financing costs on large contracts. Stabilization or reduction of rates by end-2025 is crucial for refinancing and new investments. Financial analysts track these macro trends to evaluate solvency and investment capacity.

Inflationary pressure on material and labor costs

Global inflation in 2024–25 pushed steel prices up about 12% year-on-year and raised specialized labor rates by roughly 6–9%, increasing inputs for energy infrastructure and straining Petrofac’s margins.

Fixed-price contracts expose Petrofac to cost overruns when input costs rise during multi-year projects, amplifying margin squeeze risks.

Petrofac applies hedging and indexation clauses in contracts; in 2024 over 40% of new awards included indexation provisions to offset price volatility.

Project managers and financial analysts prioritize cost-control, renegotiation and contingency planning to protect EBITDA amid persistent inflationary pressure.

Currency exchange rate fluctuations

Operating across Africa, the Middle East, Asia and Europe exposes Petrofac to translation and transaction risks as revenue in local currencies can be devalued when converted to GBP; FX swings contributed to a GBP 45m translation impact in 2024 for comparable peers in the sector.

The company uses advanced treasury hedging—forwards, options and natural hedges—covering major corridors (USD, AED, EUR) to limit volatility; emerging-market instability (e.g., FX crises in 2023–24) increases need for cautious regional cash management.

- Multi-currency exposure raises translation/transaction risk

- Revenue conversion can reduce reported GBP earnings (peer impacts ~GBP 45m in 2024)

- Sophisticated hedging (forwards, options, natural hedges) used on USD/AED/EUR

- Emerging-market instability heightens regional financial caution

Growth of the renewable energy investment market

The global renewable energy investment market reached about USD 500 billion in 2023 and attracted an estimated USD 700 billion in 2024, driving demand for engineering and services firms to support offshore wind and green hydrogen projects.

Offshore wind costs fell ~30% since 2018, making projects increasingly competitive with hydrocarbons; large-scale hydrogen projects (electrolyzer capacity growing ~60% CAGR 2021–24) hinge on technology scale-up and supply chains.

Petrofac is reallocating capabilities to capture ESG-driven capital flows as institutional investors increase allocations to renewables; project economics depend on technological maturity and manufacturing scale.

- Market size: ~USD 700B (2024)

- Offshore wind cost decline: ~30% since 2018

- Electrolyzer capacity CAGR ~60% (2021–24)

- Investment drivers: ESG capital reallocation, tech maturity, scale

Petrofac navigates oil CAPEX cyclicality, rising costs and debt amid renewables growth

Petrofac faces oil-price-driven CAPEX cyclicality (IEA upstream spend ~$370bn 2024), inflation-driven input cost rises (~10–15% commodities; steel +12% 2024) and higher debt service from UK rates (~5.25% peak 2024) on ~$1.2bn borrowings; hedging/indexation used (40% new awards 2024) and renewables pipeline growth (global renewables ~$700bn 2024) partly offsets risks.

| Metric | Value |

|---|---|

| Upstream CAPEX 2024 | $370bn |

| Steel inflation 2024 | +12% |

| UK base rate 2024 | 5.25% |

| Net debt | $1.2bn |

| Renewables investment 2024 | $700bn |

What You See Is What You Get

Petrofac PESTLE Analysis

The preview shown here is the exact Petrofac PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in this preview are the final file you’ll be able to download immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Petrofac PESTLE Analysis—concise, timely and targeted to reveal the political, economic, social, technological, legal and environmental forces shaping the company’s trajectory; buy the full report to access actionable insights, risk forecasts and ready-to-use slides that accelerate your investment or strategy work.

Political factors

Geopolitical stability in the Middle East

Petrofac’s large GCC footprint—over 40% of 2024 revenues sourced from Middle East operations—makes regional geopolitical stability critical for multi-year contract delivery.

Government initiatives like Saudi Vision 2030, with planned $1.6 trillion investment through 2030, expand opportunities for EPC and services firms including Petrofac.

Escalations risk supply-chain disruptions and timeline slippages for NOC clients; 2023–24 project delays in the region pushed capital spend timelines by up to 12–18 months in some cases.

Close strategic alignment with host-government priorities is vital to secure and retain multi-billion-dollar framework agreements and mitigate political risk.

Energy security and sovereignty policies

The EU and UK push for energy independence—EU aiming 45% renewable share by 2030 and the UK targeting 50GW offshore wind by 2030—drives demand for domestic infrastructure, boosting opportunities for Petrofac in both renewables and native oil and gas projects; governments’ security-first policies have increased licensing scrutiny and local-content rules, with UK North Sea licensing rounds in 2023–24 awarding ~150 blocks, shaping project timing and capex decisions for suppliers like Petrofac.

In-Country Value and nationalization requirements

Many jurisdictions where Petrofac operates enforce strict In-Country Value and nationalization rules—e.g., UAE ADNOC and Saudi NCP require local content levels often exceeding 40–70%—forcing the firm to prioritize local hiring, regional supply-chain investment, and technical-transfer programs.

International sanctions and trade barriers

The complex web of international sanctions continues to curb energy services, with 2024 UN/US/EU measures affecting operations in Russia, Iran and Venezuela—regions that accounted for an estimated 8–12% of sector contracts pre-sanctions.

Trade barriers and tech export controls can block Petrofac from delivering specialized engineering solutions, squeezing revenue streams—global oilfield services trade fell ~5% YoY in 2024.

Continuous diplomatic monitoring is required to ensure compliance and avoid reputational fines; 2023–24 enforcement actions led to multi‑million-dollar penalties across the industry.

- Sanctions restrict access to ~8–12% historical contract exposure

- 2024 OFS trade down ~5% YoY limits market reach

- Enforcement risk: multi‑million fines in 2023–24

- Requires flexible ops to pivot from sensitive regions

Governmental support for energy transition

Public policy and subsidies for green hydrogen, carbon capture and offshore wind underpin Petrofac New Energy; EU allocated €210bn for hydrogen and renewables in 2024–27, boosting project pipelines.

Net Zero commitments expand grants and streamlined permitting, with 2030 targets raising green contracts—UK’s Ten Point Plan mobilised £12bn and CCUS clusters pledge significant market volume.

Government changes can cut or accelerate funding; recent 2024 election shifts in EU states altered subsidy timelines, requiring Petrofac agility.

Petrofac must match capabilities to national tech preferences—e.g., Norway CCUS, UAE hydrogen, UK offshore wind—to secure contracts and co-financing.

- EU €210bn hydrogen/renewables 2024–27

- UK £12bn Ten Point Plan

- National tech focus: Norway CCUS, UAE hydrogen, UK offshore wind

- Political shifts affect subsidy timing and scale

Petrofac: GCC dependence, Vision 2030 chances vs sanctions-driven compliance drag

Petrofac’s 40%+ 2024 revenue exposure to GCC ties contract delivery to regional stability; Saudi Vision 2030’s $1.6tr pipeline and EU/UK renewables targets (EU 45% by 2030; UK 50GW offshore) expand opportunities but raise local-content and licensing complexity; sanctions trimmed ~8–12% historic contract exposure and OFS trade fell ~5% YoY in 2024, increasing enforcement and compliance costs.

| Metric | Value (2024/24) |

|---|---|

| GCC revenue share | 40%+ |

| Saudi Vision 2030 spend | $1.6tr to 2030 |

| Sanctions impact | 8–12% contract exposure |

| OFS trade YoY | -5% |

| EU renewables target | 45% by 2030 |

| UK offshore wind | 50GW by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Petrofac across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend analysis to identify threats, opportunities, and forward-looking scenarios for executives and investors.

Condenses Petrofac’s PESTLE into a clear, shareable one-page that highlights regulatory, geopolitical, and market risks to support quick decision-making in meetings and client reports.

Economic factors

Volatility in global energy prices

The financial health of Petrofac is tightly linked to client CAPEX, which fell industry-wide after the 2014–2016 downturn and again in 2020; IEA data show upstream investment was about $350bn in 2023, with 2024 estimates near $370bn, making project flows sensitive to oil prices. Sustained price volatility—Brent ranged $70–$95/bbl in 2024—can defer FIDs on multi-year projects. Higher prices boost E&P spending but raise construction material costs, contributing to global steel and commodity inflation of roughly 10–15% in 2023–24. Petrofac mitigates exposure via diversified contract structures and expanding renewable-energy services, which accounted for an increasing share of orderbook in 2024.

Interest rate environment and financing costs

As a capital-intensive EPC firm that completed major restructuring, Petrofac's debt service costs are sensitive to prevailing rates; UK base rates peaking at 5.25% in 2024 raised annual interest expenses materially on outstanding borrowings of about $1.2bn (2024). High rates also inflate costs for performance bonds and guarantees, which can add 50–200 basis points to financing costs on large contracts. Stabilization or reduction of rates by end-2025 is crucial for refinancing and new investments. Financial analysts track these macro trends to evaluate solvency and investment capacity.

Inflationary pressure on material and labor costs

Global inflation in 2024–25 pushed steel prices up about 12% year-on-year and raised specialized labor rates by roughly 6–9%, increasing inputs for energy infrastructure and straining Petrofac’s margins.

Fixed-price contracts expose Petrofac to cost overruns when input costs rise during multi-year projects, amplifying margin squeeze risks.

Petrofac applies hedging and indexation clauses in contracts; in 2024 over 40% of new awards included indexation provisions to offset price volatility.

Project managers and financial analysts prioritize cost-control, renegotiation and contingency planning to protect EBITDA amid persistent inflationary pressure.

Currency exchange rate fluctuations

Operating across Africa, the Middle East, Asia and Europe exposes Petrofac to translation and transaction risks as revenue in local currencies can be devalued when converted to GBP; FX swings contributed to a GBP 45m translation impact in 2024 for comparable peers in the sector.

The company uses advanced treasury hedging—forwards, options and natural hedges—covering major corridors (USD, AED, EUR) to limit volatility; emerging-market instability (e.g., FX crises in 2023–24) increases need for cautious regional cash management.

- Multi-currency exposure raises translation/transaction risk

- Revenue conversion can reduce reported GBP earnings (peer impacts ~GBP 45m in 2024)

- Sophisticated hedging (forwards, options, natural hedges) used on USD/AED/EUR

- Emerging-market instability heightens regional financial caution

Growth of the renewable energy investment market

The global renewable energy investment market reached about USD 500 billion in 2023 and attracted an estimated USD 700 billion in 2024, driving demand for engineering and services firms to support offshore wind and green hydrogen projects.

Offshore wind costs fell ~30% since 2018, making projects increasingly competitive with hydrocarbons; large-scale hydrogen projects (electrolyzer capacity growing ~60% CAGR 2021–24) hinge on technology scale-up and supply chains.

Petrofac is reallocating capabilities to capture ESG-driven capital flows as institutional investors increase allocations to renewables; project economics depend on technological maturity and manufacturing scale.

- Market size: ~USD 700B (2024)

- Offshore wind cost decline: ~30% since 2018

- Electrolyzer capacity CAGR ~60% (2021–24)

- Investment drivers: ESG capital reallocation, tech maturity, scale

Petrofac navigates oil CAPEX cyclicality, rising costs and debt amid renewables growth

Petrofac faces oil-price-driven CAPEX cyclicality (IEA upstream spend ~$370bn 2024), inflation-driven input cost rises (~10–15% commodities; steel +12% 2024) and higher debt service from UK rates (~5.25% peak 2024) on ~$1.2bn borrowings; hedging/indexation used (40% new awards 2024) and renewables pipeline growth (global renewables ~$700bn 2024) partly offsets risks.

| Metric | Value |

|---|---|

| Upstream CAPEX 2024 | $370bn |

| Steel inflation 2024 | +12% |

| UK base rate 2024 | 5.25% |

| Net debt | $1.2bn |

| Renewables investment 2024 | $700bn |

What You See Is What You Get

Petrofac PESTLE Analysis

The preview shown here is the exact Petrofac PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in this preview are the final file you’ll be able to download immediately after checkout.