Petrofac SWOT Analysis

Your Strategic Toolkit Starts Here

Petrofac’s technical expertise and global project track record position it well in energy services, yet cyclical oil markets, margin pressure, and legacy legal challenges weigh on near-term growth; emerging demand for energy transition services presents a strategic pivot opportunity.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

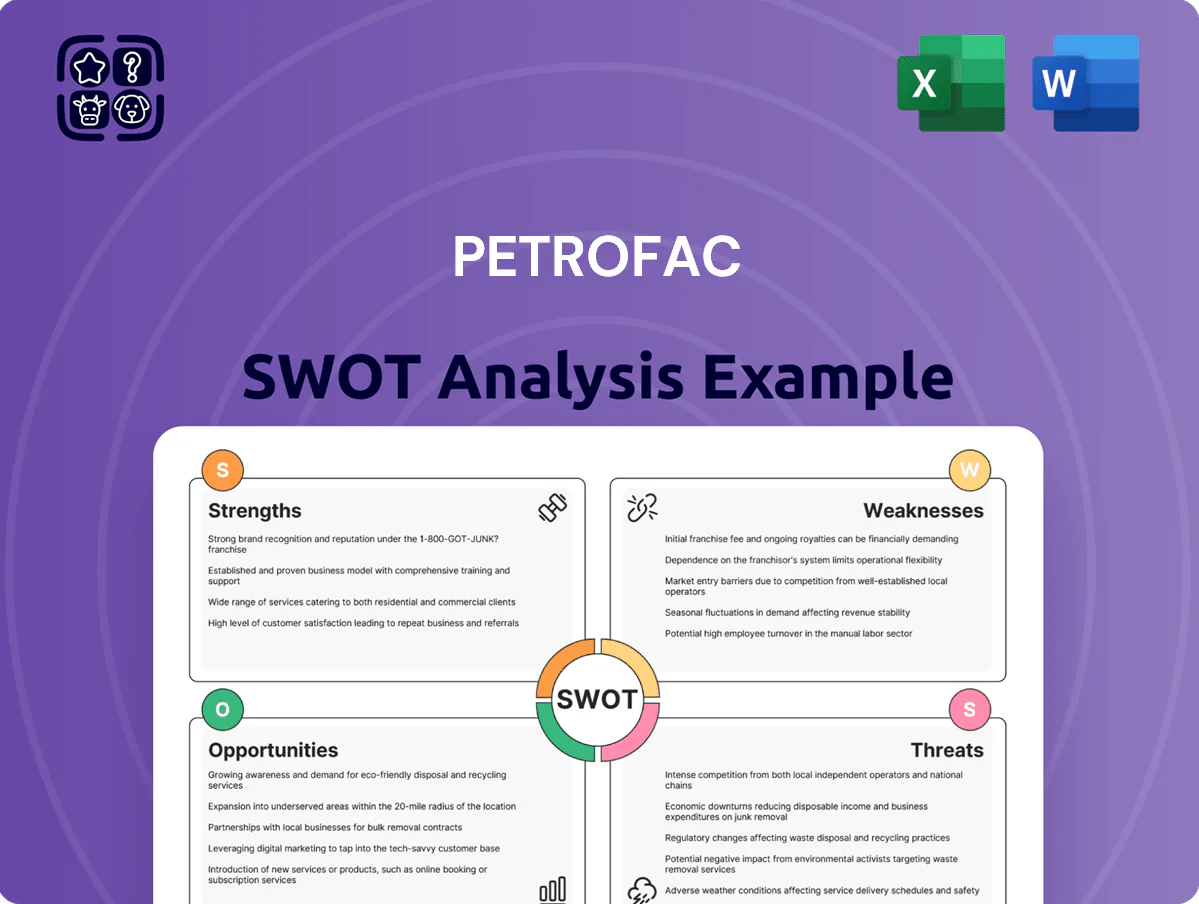

Strengths

Deep Technical Expertise Across Asset Life Cycle

Petrofac holds deep engineering expertise across the asset life cycle, delivering work from FEED (front-end engineering design) to decommissioning; it reported engineering revenues of $1.1bn in 2024, up 8% year-on-year.

Strong Geographic Footprint in Core Markets

Petrofac holds a dominant position in the Middle East and North Africa, where 60% of its 2024 revenue (about $1.2bn) came from MENA projects, keeping it at the heart of global hydrocarbon output; long-term contracts with National Oil Companies such as Saudi Aramco and ADNOC underpin a steady project pipeline; this regional focus yields cost efficiencies, shorter mobilization times, and local supply-chain advantages that rivals struggle to match.

Diversified Service Portfolio Including Renewables

Petrofac has pivoted from oil and gas into offshore wind and low-carbon services, winning 2024 contracts worth about $350m in renewables and aiming for 25% revenue from low‑carbon by 2028, which cushions cyclical fossil-fuel swings. By reusing offshore engineering capabilities, the firm reduces marginal cost per project and targets a larger addressable market—IEA sees offshore wind capacity rising 5x by 2030—boosting Petrofac’s growth runway.

Extensive Asset Solutions and Training Capabilities

- O&M ~40% of 2024 services revenue

- Training gross margins ~18–20%

- 25,000+ workers certified since 2019

- Recurring revenue cushions EPC cyclicality

Resilient Backlog and Order Intake

Heading into 2026, Petrofac has rebuilt its order book toward higher-quality, lower-risk contracts, with backlog at about $3.1bn as of Q3 2025, up 18% year-on-year, giving clearer revenue visibility and steadier cash flow.

The stronger backlog supports resource and procurement planning and reduces margin volatility seen under legacy contracts; disciplined bidding raised awarded project margin targets to mid-teens in 2025 from low-single digits in 2022.

This shift makes new contracts more accretive to EBITDA and lowers bid-to-win risk, improving credit metrics and working-capital forecasting.

- Backlog: $3.1bn (Q3 2025)

- Backlog +18% YoY

- Targeted margins: mid-teens (2025)

- Lower bid risk, better cash visibility

Engineering powerhouse: $1.1B EPC, $3.1B backlog, pivoting to 25% low‑carbon by 2028

Deep EPC-to-decommissioning engineering with $1.1bn engineering revenue (2024); MENA dominance: ~60% of 2024 revenue (~$1.2bn) with long-term NOC clients; pivot to low‑carbon: $350m renewables wins (2024), target 25% low‑carbon revenue by 2028; recurring O&M/training drove ~40% services revenue and 18–20% margins; backlog $3.1bn (Q3 2025, +18% YoY).

| Metric | Value |

|---|---|

| Engineering rev (2024) | $1.1bn |

| MENA share (2024) | 60% (~$1.2bn) |

| Renewables wins (2024) | $350m |

| O&M share | ~40% |

| Backlog (Q3 2025) | $3.1bn (+18% YoY) |

What is included in the product

Delivers a concise analysis of Petrofac’s internal strengths and weaknesses alongside external opportunities and threats, mapping the company’s competitive position and strategic risks.

Provides a concise Petrofac SWOT matrix for fast, visual strategy alignment, ideal for executives needing a quick snapshot of competitive positioning and risks.

Weaknesses

Historical Financial Leverage and Debt Constraints

Petrofac’s balance sheet has shown strain: net debt was about $1.1bn at FY2024 (year ended Dec 31, 2024), keeping leverage above 2.0x net debt/EBITDA and constraining capex and tech investment.

High debt limited bidding on giant EPC contracts needing multi‑year guarantees; management cited constrained headroom in 2024 risk disclosures.

Interest expense averaged ~$85m in 2024, pressuring free cash flow and reducing corporate agility for strategic moves.

Legacy Contract Performance Issues

Legacy fixed-price contracts caused cost overruns and delays that cut Petrofac’s margins; reported 2019–2023 contract write-downs exceeded $500m and contributed to a 2019–2022 negative EBIT swing, with underlying EBITDA margin falling to about 3% in 2022 from ~7% in 2018.

Restricted Access to Traditional Credit Markets

Petrofac’s past legal issues and 2020–2024 earnings volatility have tightened access to traditional bonding and bank credit, with reported net debt of about $400m at FY2024 increasing lender scrutiny.

As a result the firm relies on pricier alternative financing—asset-backed facilities and short-term dealer lines—that raise effective funding costs by several hundred basis points versus standard corporate loans.

This constrained credit profile caps project scale: management noted pipeline execution limited to mid-single-digit annual megaprojects versus pre-2019 capacity to run multiple large projects concurrently.

Dependency on Middle Eastern Market Concentration

Petrofac remains heavily exposed to the Middle East: about 58% of 2024 revenue came from GCC and nearby National Oil Companies, creating concentration risk if regional capex falls or political tensions escalate.

A sudden cut in NOC spending or sanctions could reduce group revenue by double-digit percentage points given backlog concentration; diversification into West Africa and the UK is underway but represented only ~22% of 2024 revenue.

- 58% of 2024 revenue from GCC/NOC clients

- ~22% revenue from diversifying regions (2024)

- High backlog concentration raises sensitivity to regional capex shifts

Reputational Recovery Post-Legal Settlements

- Past settlements: 2020-21, £77m impact

- Investor concern: 34% flagged governance (2024)

- Compliance cost: ~3–5% of 2024 Opex

Petrofac’s debt, legacy write‑downs and governance risks cap growth and raise execution risk

Petrofac’s high net debt (~$1.1bn at FY2024) and >2.0x net debt/EBITDA limit capex and bidding; interest costs (~$85m in 2024) squeeze FCF. Legacy fixed‑price contract write‑downs >$500m (2019–23) cut margins and capacity to run large EPC projects. Revenue concentration (58% GCC/NOCs in 2024) and lingering governance concerns (34% investors wary in 2024) raise execution and funding risks.

| Metric | Value (2024) |

|---|---|

| Net debt | $1.1bn |

| Net debt/EBITDA | >2.0x |

| Interest expense | $85m |

| Write‑downs (2019–23) | >$500m |

| GCC/NOC revenue | 58% |

| Investor governance concern | 34% |

Preview the Actual Deliverable

Petrofac SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, downloadable analysis. You’re viewing a live preview of the complete, editable document; buy now to unlock the full, detailed version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Petrofac’s technical expertise and global project track record position it well in energy services, yet cyclical oil markets, margin pressure, and legacy legal challenges weigh on near-term growth; emerging demand for energy transition services presents a strategic pivot opportunity.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Deep Technical Expertise Across Asset Life Cycle

Petrofac holds deep engineering expertise across the asset life cycle, delivering work from FEED (front-end engineering design) to decommissioning; it reported engineering revenues of $1.1bn in 2024, up 8% year-on-year.

Strong Geographic Footprint in Core Markets

Petrofac holds a dominant position in the Middle East and North Africa, where 60% of its 2024 revenue (about $1.2bn) came from MENA projects, keeping it at the heart of global hydrocarbon output; long-term contracts with National Oil Companies such as Saudi Aramco and ADNOC underpin a steady project pipeline; this regional focus yields cost efficiencies, shorter mobilization times, and local supply-chain advantages that rivals struggle to match.

Diversified Service Portfolio Including Renewables

Petrofac has pivoted from oil and gas into offshore wind and low-carbon services, winning 2024 contracts worth about $350m in renewables and aiming for 25% revenue from low‑carbon by 2028, which cushions cyclical fossil-fuel swings. By reusing offshore engineering capabilities, the firm reduces marginal cost per project and targets a larger addressable market—IEA sees offshore wind capacity rising 5x by 2030—boosting Petrofac’s growth runway.

Extensive Asset Solutions and Training Capabilities

- O&M ~40% of 2024 services revenue

- Training gross margins ~18–20%

- 25,000+ workers certified since 2019

- Recurring revenue cushions EPC cyclicality

Resilient Backlog and Order Intake

Heading into 2026, Petrofac has rebuilt its order book toward higher-quality, lower-risk contracts, with backlog at about $3.1bn as of Q3 2025, up 18% year-on-year, giving clearer revenue visibility and steadier cash flow.

The stronger backlog supports resource and procurement planning and reduces margin volatility seen under legacy contracts; disciplined bidding raised awarded project margin targets to mid-teens in 2025 from low-single digits in 2022.

This shift makes new contracts more accretive to EBITDA and lowers bid-to-win risk, improving credit metrics and working-capital forecasting.

- Backlog: $3.1bn (Q3 2025)

- Backlog +18% YoY

- Targeted margins: mid-teens (2025)

- Lower bid risk, better cash visibility

Engineering powerhouse: $1.1B EPC, $3.1B backlog, pivoting to 25% low‑carbon by 2028

Deep EPC-to-decommissioning engineering with $1.1bn engineering revenue (2024); MENA dominance: ~60% of 2024 revenue (~$1.2bn) with long-term NOC clients; pivot to low‑carbon: $350m renewables wins (2024), target 25% low‑carbon revenue by 2028; recurring O&M/training drove ~40% services revenue and 18–20% margins; backlog $3.1bn (Q3 2025, +18% YoY).

| Metric | Value |

|---|---|

| Engineering rev (2024) | $1.1bn |

| MENA share (2024) | 60% (~$1.2bn) |

| Renewables wins (2024) | $350m |

| O&M share | ~40% |

| Backlog (Q3 2025) | $3.1bn (+18% YoY) |

What is included in the product

Delivers a concise analysis of Petrofac’s internal strengths and weaknesses alongside external opportunities and threats, mapping the company’s competitive position and strategic risks.

Provides a concise Petrofac SWOT matrix for fast, visual strategy alignment, ideal for executives needing a quick snapshot of competitive positioning and risks.

Weaknesses

Historical Financial Leverage and Debt Constraints

Petrofac’s balance sheet has shown strain: net debt was about $1.1bn at FY2024 (year ended Dec 31, 2024), keeping leverage above 2.0x net debt/EBITDA and constraining capex and tech investment.

High debt limited bidding on giant EPC contracts needing multi‑year guarantees; management cited constrained headroom in 2024 risk disclosures.

Interest expense averaged ~$85m in 2024, pressuring free cash flow and reducing corporate agility for strategic moves.

Legacy Contract Performance Issues

Legacy fixed-price contracts caused cost overruns and delays that cut Petrofac’s margins; reported 2019–2023 contract write-downs exceeded $500m and contributed to a 2019–2022 negative EBIT swing, with underlying EBITDA margin falling to about 3% in 2022 from ~7% in 2018.

Restricted Access to Traditional Credit Markets

Petrofac’s past legal issues and 2020–2024 earnings volatility have tightened access to traditional bonding and bank credit, with reported net debt of about $400m at FY2024 increasing lender scrutiny.

As a result the firm relies on pricier alternative financing—asset-backed facilities and short-term dealer lines—that raise effective funding costs by several hundred basis points versus standard corporate loans.

This constrained credit profile caps project scale: management noted pipeline execution limited to mid-single-digit annual megaprojects versus pre-2019 capacity to run multiple large projects concurrently.

Dependency on Middle Eastern Market Concentration

Petrofac remains heavily exposed to the Middle East: about 58% of 2024 revenue came from GCC and nearby National Oil Companies, creating concentration risk if regional capex falls or political tensions escalate.

A sudden cut in NOC spending or sanctions could reduce group revenue by double-digit percentage points given backlog concentration; diversification into West Africa and the UK is underway but represented only ~22% of 2024 revenue.

- 58% of 2024 revenue from GCC/NOC clients

- ~22% revenue from diversifying regions (2024)

- High backlog concentration raises sensitivity to regional capex shifts

Reputational Recovery Post-Legal Settlements

- Past settlements: 2020-21, £77m impact

- Investor concern: 34% flagged governance (2024)

- Compliance cost: ~3–5% of 2024 Opex

Petrofac’s debt, legacy write‑downs and governance risks cap growth and raise execution risk

Petrofac’s high net debt (~$1.1bn at FY2024) and >2.0x net debt/EBITDA limit capex and bidding; interest costs (~$85m in 2024) squeeze FCF. Legacy fixed‑price contract write‑downs >$500m (2019–23) cut margins and capacity to run large EPC projects. Revenue concentration (58% GCC/NOCs in 2024) and lingering governance concerns (34% investors wary in 2024) raise execution and funding risks.

| Metric | Value (2024) |

|---|---|

| Net debt | $1.1bn |

| Net debt/EBITDA | >2.0x |

| Interest expense | $85m |

| Write‑downs (2019–23) | >$500m |

| GCC/NOC revenue | 58% |

| Investor governance concern | 34% |

Preview the Actual Deliverable

Petrofac SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, downloadable analysis. You’re viewing a live preview of the complete, editable document; buy now to unlock the full, detailed version.