Petsmart PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, consumer trends, and technological advances are reshaping Petsmart’s competitive landscape—our concise PESTLE highlights key risks and opportunities you need to know; buy the full analysis to get the complete, actionable report and ready-to-use slides for strategy or investment decisions.

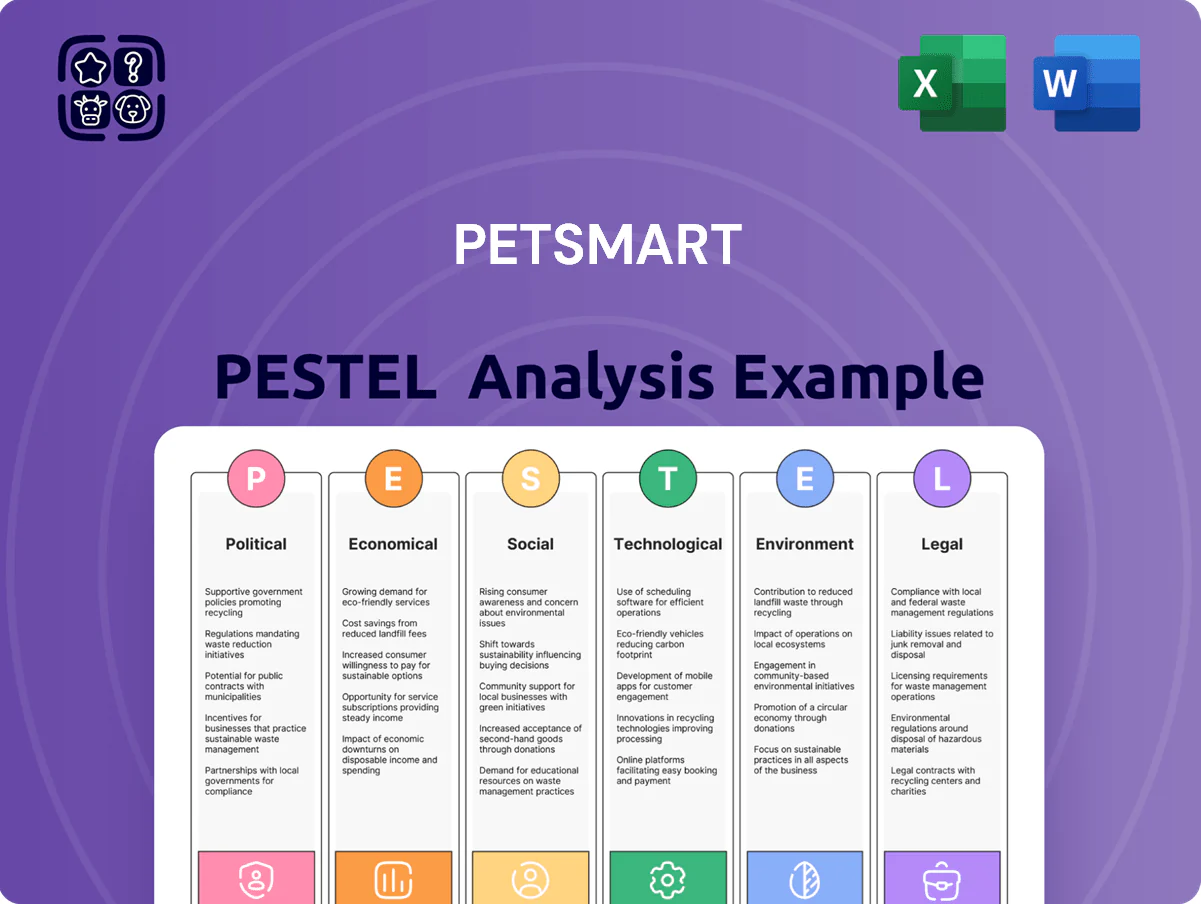

Political factors

Trade Policies and Tariffs

Changes in international trade agreements and tariffs on imported pet supplies, especially from China, raised PetSmart’s landed costs by an estimated 4–7% in 2024–2025, squeezing gross margins on private-label lines that accounted for roughly 18% of merchandise sales. Geopolitical tensions through late 2025 increased freight volatility; ocean freight rates spiked ~35% in 2024 vs 2023, driving higher COGS and prompting SKU-level price adjustments. Management must balance competitive retail pricing with margin protection, leveraging supplier diversification and tariff mitigation strategies to preserve EBITDA.

Animal Welfare Legislation

Government regulations tightening standards for sale and care of live animals raise compliance costs for retailers; U.S. state laws banning pet store sales of mill-bred dogs/cats increased from under 5 in 2018 to 22 by 2025, aligning with PetSmart’s adoption-centric strategy and supporting its Humane Adoption Centers that handled ~118,000 adoptions in FY2024.

Labor Regulations and Minimum Wage

Political shifts toward higher federal or state minimum wages—e.g., 2025 proposals to raise the US federal minimum to $15–16/hr and 2024 state increases in California and New York to $16–18/hr—would raise PetSmart’s labor costs across ~1,650 stores, potentially adding tens of millions annually to operating expenses.

New labor laws on benefits, healthcare mandates and expanded union rights—union wins in some retail sectors rose 12% in 2023—require PetSmart to adapt HR policies, adjust total compensation packages and model increased fixed labor overhead in budgets.

To remain competitive while preserving margins, PetSmart must balance wage and benefit increases with staffing efficiency, automation in repeat tasks, and optimized scheduling; a 5–10% payroll cost rise could compress store-level EBITDA if not offset by productivity gains.

Taxation Policies

Corporate tax rates and recent proposals—such as the US federal rate debates and 2024 state-level shifts—affect PetSmart’s net margins; a 1% tax increase could reduce after-tax earnings by roughly $20–30 million given 2023 U.S. EBITDA around $2–3 billion.

Changes to state sales tax exemptions for pet food or vet services (e.g., selective exemptions in 5 states in 2024) alter consumer spending and basket composition, impacting same-store sales.

Emerging proposals for luxury taxes on high-end pet services could cut demand in the premium segment by an estimated 5–10%, pressuring average transaction value.

Monitoring fiscal policy shifts supports accurate long-term financial forecasting and capital allocation decisions.

- 1% corporate tax hike → ~$20–30M EBITDA impact

- 5 states with selective exemptions in 2024

- Luxury tax risk could reduce premium demand 5–10%

Government Support for Small Businesses

Government initiatives that grant tax incentives or $50m+ small-business aid programs to independent retailers raise local competitive pressure on PetSmart, particularly in urban/suburban niches where boutique stores capture premium customers.

Such policies can erode PetSmart’s share in targeted ZIP codes despite its $8.6bn 2023 revenue; the firm counters by marketing community investments and 1,600+ rescue partnerships to reinforce local relevance.

- Small-business grants/tax breaks boost local boutiques

- PetSmart 2023 revenue: $8.6bn; >1,600 animal welfare partnerships

- Local incentives can reduce market share in specific demographics

- Company emphasizes community programs to mitigate impact

Political headwinds—tariffs, freight, regs and tax risks squeeze margins; mitigation: diversify

Political risks—tariffs (+4–7% landed costs 2024–25), higher freight (+35% 2024), rising minimum wages ($15–18 proposals), tighter animal-sale laws (22 states by 2025), potential 1% corporate tax hike (~$20–30M EBITDA hit) and luxury/sales-tax changes—pressure margins and same-store sales; mitigation: supplier diversification, automation, adoption-focus and targeted community programs.

| Metric | 2024–25 |

|---|---|

| Tariff impact | +4–7% |

| Ocean freight | +35% |

| States banning mill sales | 22 |

| EBITDA hit per 1% tax | $20–30M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Petsmart across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise, PESTLE-segmented summary of PetSmart’s external risks and opportunities for quick inclusion in presentations or strategy sessions, editable for regional or business-line nuance and easily shared across teams.

Economic factors

Inflationary Pressures on Discretionary Income

Persistent inflation through late 2025—US CPI running near 3.5–4% year-over-year in H2 2025—eroded discretionary income, prompting some pet owners to trade down to value pet-food brands, with private-label share rising ~2–3 percentage points in 2024–25.

Pet food remained relatively resilient, but discretionary services such as grooming and Doggie Day Camp saw weaker demand; industry reports showed a 5–8% slowdown in pet services spend in 2025 versus 2024.

PetSmart counters with tiered pricing, expanded private-label options and its loyalty program (more than 65 million members by 2025) to retain budget-conscious customers during economic fluctuations.

Supply Chain Resilience and Costs

Fluctuations in global shipping costs—Baltic Dry Index swings of +48% in 2024—and rising U.S. truckload rates (up ~12% YoY in 2024) have pressured availability and retail pricing of specialized pet products at PetSmart, increasing landed costs and occasional stockouts.

Volatility in raw-material markets—soy and corn feed prices rose ~15% in 2024 while animal protein costs jumped ~10%—forces PetSmart to strengthen inventory management and diversify suppliers to protect margins.

Efficient supply‑chain operations, including greater use of regional distribution centers and vendor-managed inventory, are critical to preserving PetSmart’s one-stop-shop value proposition and containing fulfillment costs amid tightening logistics margins.

Interest Rate Environment

The prevailing interest rate environment affects PetSmart’s cost of debt and capacity for M&A; US benchmark rates (Fed funds ~5.25–5.50% in 2024) raised average corporate borrowing costs, constraining large-scale store openings and capex in 2024–2025.

High rates slowed expansion and tech investments, while a stabilizing rate outlook in 2025 — markets pricing ~50–100bps easing by end-2025 — offers more predictable financing for multi-year infrastructure projects.

Growth of the Pet Premiumization Trend

Despite economic headwinds, pet humanization is fueling demand for premium products and health services; US pet industry spending hit a record $136.8B in 2023 and rose to an estimated $142B in 2024, with premium food and veterinary services growing faster than overall categories.

Consumers increasingly treat pets as family—52% of owners in 2024 reported spending more on specialized diets and advanced care, enabling PetSmart to scale luxury brands and expand Banfield clinics and in-store veterinary revenue streams.

- 2024 US pet spending ~142B; premium segments outpace overall growth

- 52% of owners increased spend on specialized diets/advanced care in 2024

- PetSmart leverages trend via luxury product assortments and Banfield expansion

Employment Levels and Consumer Confidence

PetSmart tracks these indicators to shift marketing and promotions, reallocating budget toward high-margin services during strong labor markets.

- Unemployment ~5.0% (Dec 2025); Consumer Confidence ~105 (2025)

- PetSmart services revenue +6% YoY (2024)

- Marketing reallocated to services during strong employment

Rising costs push shoppers to private‑label as US pet spend hits $142B in 2024

Inflation and higher borrowing costs through 2024–25 squeezed discretionary spend, shifting customers to private‑label (share +2–3ppt) while premium and vet services grew; pet industry US spend rose to ~$142B in 2024. Supply‑chain and commodity cost spikes (feed +15% in 2024, shipping BDI +48% in 2024) raised landed costs, pushing PetSmart to expand private label, loyalty (65M members) and regional DCs.

| Metric | Value |

|---|---|

| US pet spend 2024 | $142B |

| Private‑label share change | +2–3ppt (2024–25) |

| Feed price change 2024 | +15% |

| BDI 2024 swing | +48% |

Preview Before You Purchase

Petsmart PESTLE Analysis

The preview shown here is the exact Petsmart PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, consumer trends, and technological advances are reshaping Petsmart’s competitive landscape—our concise PESTLE highlights key risks and opportunities you need to know; buy the full analysis to get the complete, actionable report and ready-to-use slides for strategy or investment decisions.

Political factors

Trade Policies and Tariffs

Changes in international trade agreements and tariffs on imported pet supplies, especially from China, raised PetSmart’s landed costs by an estimated 4–7% in 2024–2025, squeezing gross margins on private-label lines that accounted for roughly 18% of merchandise sales. Geopolitical tensions through late 2025 increased freight volatility; ocean freight rates spiked ~35% in 2024 vs 2023, driving higher COGS and prompting SKU-level price adjustments. Management must balance competitive retail pricing with margin protection, leveraging supplier diversification and tariff mitigation strategies to preserve EBITDA.

Animal Welfare Legislation

Government regulations tightening standards for sale and care of live animals raise compliance costs for retailers; U.S. state laws banning pet store sales of mill-bred dogs/cats increased from under 5 in 2018 to 22 by 2025, aligning with PetSmart’s adoption-centric strategy and supporting its Humane Adoption Centers that handled ~118,000 adoptions in FY2024.

Labor Regulations and Minimum Wage

Political shifts toward higher federal or state minimum wages—e.g., 2025 proposals to raise the US federal minimum to $15–16/hr and 2024 state increases in California and New York to $16–18/hr—would raise PetSmart’s labor costs across ~1,650 stores, potentially adding tens of millions annually to operating expenses.

New labor laws on benefits, healthcare mandates and expanded union rights—union wins in some retail sectors rose 12% in 2023—require PetSmart to adapt HR policies, adjust total compensation packages and model increased fixed labor overhead in budgets.

To remain competitive while preserving margins, PetSmart must balance wage and benefit increases with staffing efficiency, automation in repeat tasks, and optimized scheduling; a 5–10% payroll cost rise could compress store-level EBITDA if not offset by productivity gains.

Taxation Policies

Corporate tax rates and recent proposals—such as the US federal rate debates and 2024 state-level shifts—affect PetSmart’s net margins; a 1% tax increase could reduce after-tax earnings by roughly $20–30 million given 2023 U.S. EBITDA around $2–3 billion.

Changes to state sales tax exemptions for pet food or vet services (e.g., selective exemptions in 5 states in 2024) alter consumer spending and basket composition, impacting same-store sales.

Emerging proposals for luxury taxes on high-end pet services could cut demand in the premium segment by an estimated 5–10%, pressuring average transaction value.

Monitoring fiscal policy shifts supports accurate long-term financial forecasting and capital allocation decisions.

- 1% corporate tax hike → ~$20–30M EBITDA impact

- 5 states with selective exemptions in 2024

- Luxury tax risk could reduce premium demand 5–10%

Government Support for Small Businesses

Government initiatives that grant tax incentives or $50m+ small-business aid programs to independent retailers raise local competitive pressure on PetSmart, particularly in urban/suburban niches where boutique stores capture premium customers.

Such policies can erode PetSmart’s share in targeted ZIP codes despite its $8.6bn 2023 revenue; the firm counters by marketing community investments and 1,600+ rescue partnerships to reinforce local relevance.

- Small-business grants/tax breaks boost local boutiques

- PetSmart 2023 revenue: $8.6bn; >1,600 animal welfare partnerships

- Local incentives can reduce market share in specific demographics

- Company emphasizes community programs to mitigate impact

Political headwinds—tariffs, freight, regs and tax risks squeeze margins; mitigation: diversify

Political risks—tariffs (+4–7% landed costs 2024–25), higher freight (+35% 2024), rising minimum wages ($15–18 proposals), tighter animal-sale laws (22 states by 2025), potential 1% corporate tax hike (~$20–30M EBITDA hit) and luxury/sales-tax changes—pressure margins and same-store sales; mitigation: supplier diversification, automation, adoption-focus and targeted community programs.

| Metric | 2024–25 |

|---|---|

| Tariff impact | +4–7% |

| Ocean freight | +35% |

| States banning mill sales | 22 |

| EBITDA hit per 1% tax | $20–30M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Petsmart across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise, PESTLE-segmented summary of PetSmart’s external risks and opportunities for quick inclusion in presentations or strategy sessions, editable for regional or business-line nuance and easily shared across teams.

Economic factors

Inflationary Pressures on Discretionary Income

Persistent inflation through late 2025—US CPI running near 3.5–4% year-over-year in H2 2025—eroded discretionary income, prompting some pet owners to trade down to value pet-food brands, with private-label share rising ~2–3 percentage points in 2024–25.

Pet food remained relatively resilient, but discretionary services such as grooming and Doggie Day Camp saw weaker demand; industry reports showed a 5–8% slowdown in pet services spend in 2025 versus 2024.

PetSmart counters with tiered pricing, expanded private-label options and its loyalty program (more than 65 million members by 2025) to retain budget-conscious customers during economic fluctuations.

Supply Chain Resilience and Costs

Fluctuations in global shipping costs—Baltic Dry Index swings of +48% in 2024—and rising U.S. truckload rates (up ~12% YoY in 2024) have pressured availability and retail pricing of specialized pet products at PetSmart, increasing landed costs and occasional stockouts.

Volatility in raw-material markets—soy and corn feed prices rose ~15% in 2024 while animal protein costs jumped ~10%—forces PetSmart to strengthen inventory management and diversify suppliers to protect margins.

Efficient supply‑chain operations, including greater use of regional distribution centers and vendor-managed inventory, are critical to preserving PetSmart’s one-stop-shop value proposition and containing fulfillment costs amid tightening logistics margins.

Interest Rate Environment

The prevailing interest rate environment affects PetSmart’s cost of debt and capacity for M&A; US benchmark rates (Fed funds ~5.25–5.50% in 2024) raised average corporate borrowing costs, constraining large-scale store openings and capex in 2024–2025.

High rates slowed expansion and tech investments, while a stabilizing rate outlook in 2025 — markets pricing ~50–100bps easing by end-2025 — offers more predictable financing for multi-year infrastructure projects.

Growth of the Pet Premiumization Trend

Despite economic headwinds, pet humanization is fueling demand for premium products and health services; US pet industry spending hit a record $136.8B in 2023 and rose to an estimated $142B in 2024, with premium food and veterinary services growing faster than overall categories.

Consumers increasingly treat pets as family—52% of owners in 2024 reported spending more on specialized diets and advanced care, enabling PetSmart to scale luxury brands and expand Banfield clinics and in-store veterinary revenue streams.

- 2024 US pet spending ~142B; premium segments outpace overall growth

- 52% of owners increased spend on specialized diets/advanced care in 2024

- PetSmart leverages trend via luxury product assortments and Banfield expansion

Employment Levels and Consumer Confidence

PetSmart tracks these indicators to shift marketing and promotions, reallocating budget toward high-margin services during strong labor markets.

- Unemployment ~5.0% (Dec 2025); Consumer Confidence ~105 (2025)

- PetSmart services revenue +6% YoY (2024)

- Marketing reallocated to services during strong employment

Rising costs push shoppers to private‑label as US pet spend hits $142B in 2024

Inflation and higher borrowing costs through 2024–25 squeezed discretionary spend, shifting customers to private‑label (share +2–3ppt) while premium and vet services grew; pet industry US spend rose to ~$142B in 2024. Supply‑chain and commodity cost spikes (feed +15% in 2024, shipping BDI +48% in 2024) raised landed costs, pushing PetSmart to expand private label, loyalty (65M members) and regional DCs.

| Metric | Value |

|---|---|

| US pet spend 2024 | $142B |

| Private‑label share change | +2–3ppt (2024–25) |

| Feed price change 2024 | +15% |

| BDI 2024 swing | +48% |

Preview Before You Purchase

Petsmart PESTLE Analysis

The preview shown here is the exact Petsmart PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.