PEXA Boston Consulting Group Matrix

Download Your Competitive Advantage

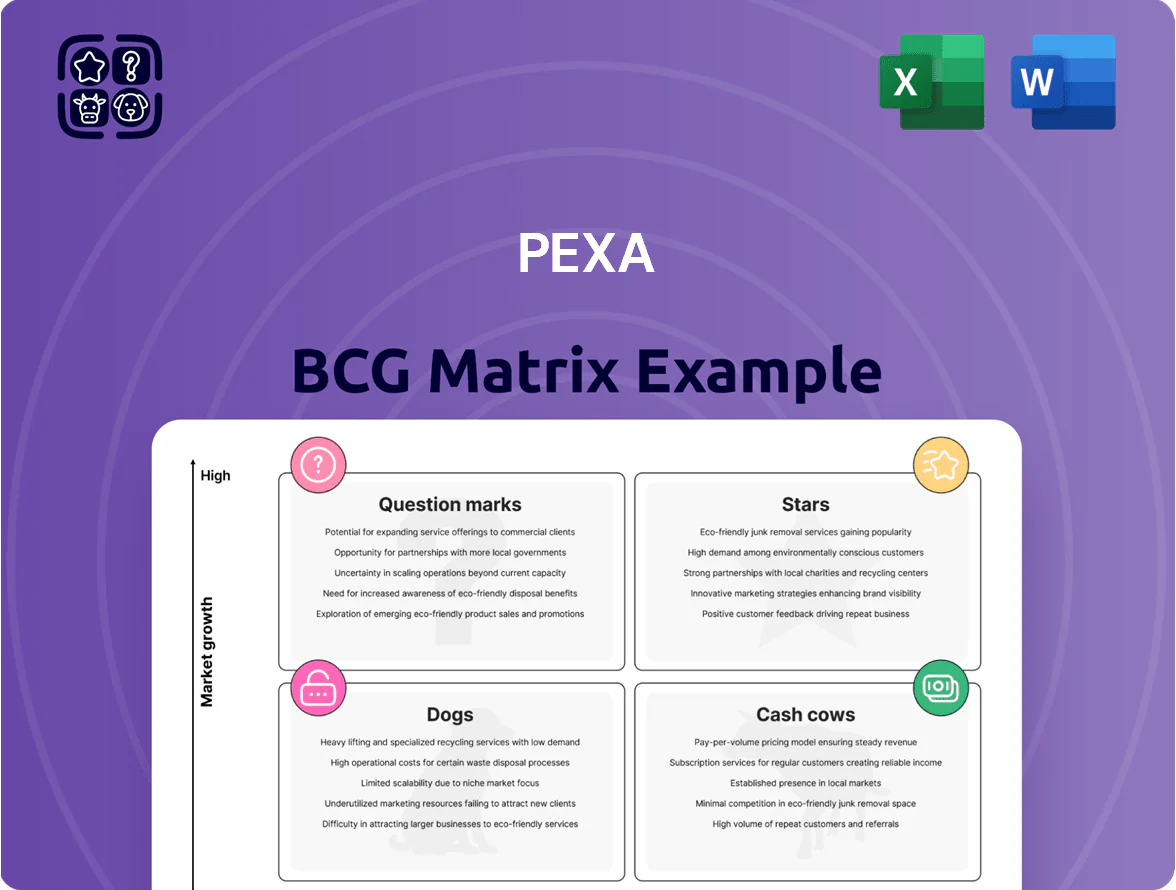

The PEXA BCG Matrix snapshot highlights which business lines are accelerating, sustaining, or consuming value amid industry shifts—essential for prioritizing investment and divestment decisions. This preview outlines key quadrant placements and immediate implications for growth and cash management. Purchase the full BCG Matrix to access quadrant-by-quadrant data, actionable strategies, and ready-to-use Word and Excel deliverables that save research time and sharpen your competitive plan.

Stars

PEXA UK Remortgage Platform

PEXA UK Remortgage Platform is in a high-growth market as UK remortgages shift from paper to digital; UK digital conveyancing volumes rose 28% in 2025 to ~1.1m transactions, driving strong addressable demand.

Onboarding Tier 1 lender NatWest in Jan 2026 accelerates share gains—PEXA cited a 12-point uplift in lender connectivity in H2 2025, positioning the product as a rising star internationally.

This product is a primary growth engine and needs heavy sales and marketing spend; management targets £25–30m FY2026 investment to win network effects among ~45k conveyancers and 20 major lenders.

PEXA International Sale and Purchase

Launched in 2025, PEXA International Sale and Purchase targets the largest segment of the UK property market—around 1.2 million conveyancing transactions annually—positioning it in the BCG Matrix as a Star due to rapid market share gains during rollout.

Currently in high-growth mode, it is expanding from pilot deals to full-scale rollout; revenue run-rate is early but pilots showed 40% faster transaction velocity versus incumbents.

It consumes heavy cash for API integrations, onboarding, and compliance—estimated £25–40m in 2025 capex and R&D—but promises the biggest long-term upside for replicating PEXA’s AU margins.

PEXAPay Payment System

PEXAPay is the high-growth payments backbone for international settlements in the UK property ecosystem, processing an estimated £18.4bn in cross-border flows in 2025 and growing ~28% year-over-year.

It secures fund exchange via ISO 20022 messaging and tokenised rails, and is pivotal for major banks adopting PEXAGo, which showed a 42% uptake among top-10 UK lenders in 2025.

Continued capex—industry estimates suggest £65–85m over 2026–2028—is critical to keep a competitive lead over fintech challengers.

PEXA Exchange Refinance Australia

PEXA Exchange Refinance Australia is a star: refinance volumes jumped 16% in late 2025 as borrowers chased lower rates, and PEXA holds a leading share in this high-activity sub-sector of the mature Australian market.

The product line benefits from renewed growth as homeowners seek better deals, driving higher transaction frequency and fee income while reinforcing platform dominance.

- 16% volume rise in late 2025

- High market share in refinance segment

- Renewed growth cycle from rate shifts

- Increased transaction fees and frequency

PEXA Strategic AML Solutions

PEXA is positioning PEXA Strategic AML Solutions as a Star: with July 2026 AML/digital ID rules, addressable market growth is estimated at +18% CAGR to 2028 and PEXA expects to capture a leading share by investing A$40–60m in FY25–26 to scale tooling for 20,000+ lawyer and bank users.

- New regs live July 2026 — spike in compliance spend

- PEXA investing A$40–60m FY25–26

- Targeting 20,000+ users (law firms, banks)

- Market growth ~18% CAGR to 2028

PEXA targets rapid share gains with £90–140m/A$40–60m push to seize 45–60% network wins

PEXA’s Stars: UK Remortgage Platform, PEXAPay, AU Refinance, and Strategic AML show rapid share gains in high-growth markets; combined 2025/26 invest of ~£90–140m/A$40–60m aims to capture ~45–60% network effects in target segments, driving fee and volume upside.

| Product | 2025 Metric | Capex FY25–26 |

|---|---|---|

| UK Remortgage | 1.1m digital txns; +28% | £25–30m |

| PEXAPay | £18.4bn flows; +28% | £65–85m |

| AU Refinance | +16% vol | — |

| AML | 18% CAGR to 2028 | A$40–60m |

What is included in the product

Comprehensive BCG Matrix analysis of PEXA’s portfolio with strategic recommendations, risks per quadrant, and investment priorities.

One-page PEXA BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

PEXA Exchange Australia Core

PEXA Exchange Australia Core dominates with roughly 90% market share of all property transactions and in FY2024 delivered about A$150m EBITDA on A$220m revenue, reflecting EBITDA margins near 68%, making it the group's primary cash generator.

As a near-monopoly in a mature market, it funds international expansion and R&D—PEXA allocated A$45m in 2024 to overseas growth and new digital products, covering most capex and strategic investments.

PEXA Transfer Settlements Australia

Property transfer settlements are a stable, mature revenue stream requiring minimal new marketing spend; PEXA reported 5.6 million transactions in FY2024, generating ~A$143m in settlement fees, up 4% year-on-year.

PEXA Workspace for Conveyancers

PEXA Workspace for Conveyancers is the industry-standard digital workspace used by over 18,000 Australian lawyers and conveyancers as of Dec 2025, creating high switching costs and strong user lock-in.

It requires low incremental investment—development capex under A$10m annually in FY2025—while sustaining dominant workflow integration across settlements.

As a foundational cash generator, Workspace delivered ~A$75m EBITDA in FY2025 and benefits from Australia’s relatively stable housing turnover (≈1.2m dwellings sold in 2024).

PEXA National Lodgement Services

PEXA National Lodgement Services is a cash cow: digital lodgement of land documents is a mature service PEXA has refined over a decade, and the 2025 completion of the Northern Territory rollout leaves minimal geographic expansion while sustaining near-total market share.

High-throughput infrastructure yields strong unit economics—industry reports show >60% gross margins on lodgements and annual processing volumes ~25M documents (FY2024–25), locking stable, repeatable cash flow.

- Near-100% market share in all Australian jurisdictions (NT rollout completed 2025)

- ~25 million documents processed annually (FY2024–25)

- Gross margin >60% per document

- Limited geographic upside; focus on yield and efficiency

PEXA Financial Institution Integration

PEXA's deep technical integrations with Australia's major banks yield steady volumes—institutional settlements handled ~65% of platform transactions in FY2024, producing recurring cash flow and ~A$40–50m EBITDA contribution annually to the group.

These connections are high switching-cost assets, hard for competitors to displace, so PEXA stays the primary channel for institutional property settlements and needs only maintenance-level capex.

- ~65% platform transactions: institutional

- A$40–50m annual EBITDA

- Low maintenance capex

- High switching costs, durable market position

PEXA: Dominant Exchange, Strong Cash Flows—A$150m EBITDA + A$115–125m from Workspace

PEXA's core businesses are cash cows: Exchange Australia Core (≈90% share) drove ~A$150m EBITDA on A$220m revenue in FY2024; Workspace and Lodgement together added ~A$115–125m EBITDA in FY2025 with low capex; institutional flows (~65% of transactions) contribute A$40–50m EBITDA and stable volumes (5.6M settlements, ~25M documents FY2024–25).

| Metric | Value |

|---|---|

| Exchange share | ≈90% |

| Exchange FY2024 EBITDA | A$150m |

| Revenue FY2024 | A$220m |

| Settlements | 5.6M (2024) |

| Documents | ≈25M (FY2024–25) |

| Institutional % | ≈65% |

| Group capex |

Delivered as Shown

PEXA BCG Matrix

The file you're previewing on this page is the final BCG Matrix report you'll receive after purchase; no watermarks, no demo content—just a fully formatted, ready-to-use strategic analysis crafted for clarity and decision-making.

This preview is the exact document you'll download post-purchase, built with market-backed insights and professional layout so you can present, edit, or print without further revisions.

Once purchased, the complete file is delivered directly to your inbox—instantly available for use in business planning, investor decks, or client presentations.

You're viewing the authentic BCG Matrix report that becomes yours with a one-time purchase, prepared by strategy professionals and formatted for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The PEXA BCG Matrix snapshot highlights which business lines are accelerating, sustaining, or consuming value amid industry shifts—essential for prioritizing investment and divestment decisions. This preview outlines key quadrant placements and immediate implications for growth and cash management. Purchase the full BCG Matrix to access quadrant-by-quadrant data, actionable strategies, and ready-to-use Word and Excel deliverables that save research time and sharpen your competitive plan.

Stars

PEXA UK Remortgage Platform

PEXA UK Remortgage Platform is in a high-growth market as UK remortgages shift from paper to digital; UK digital conveyancing volumes rose 28% in 2025 to ~1.1m transactions, driving strong addressable demand.

Onboarding Tier 1 lender NatWest in Jan 2026 accelerates share gains—PEXA cited a 12-point uplift in lender connectivity in H2 2025, positioning the product as a rising star internationally.

This product is a primary growth engine and needs heavy sales and marketing spend; management targets £25–30m FY2026 investment to win network effects among ~45k conveyancers and 20 major lenders.

PEXA International Sale and Purchase

Launched in 2025, PEXA International Sale and Purchase targets the largest segment of the UK property market—around 1.2 million conveyancing transactions annually—positioning it in the BCG Matrix as a Star due to rapid market share gains during rollout.

Currently in high-growth mode, it is expanding from pilot deals to full-scale rollout; revenue run-rate is early but pilots showed 40% faster transaction velocity versus incumbents.

It consumes heavy cash for API integrations, onboarding, and compliance—estimated £25–40m in 2025 capex and R&D—but promises the biggest long-term upside for replicating PEXA’s AU margins.

PEXAPay Payment System

PEXAPay is the high-growth payments backbone for international settlements in the UK property ecosystem, processing an estimated £18.4bn in cross-border flows in 2025 and growing ~28% year-over-year.

It secures fund exchange via ISO 20022 messaging and tokenised rails, and is pivotal for major banks adopting PEXAGo, which showed a 42% uptake among top-10 UK lenders in 2025.

Continued capex—industry estimates suggest £65–85m over 2026–2028—is critical to keep a competitive lead over fintech challengers.

PEXA Exchange Refinance Australia

PEXA Exchange Refinance Australia is a star: refinance volumes jumped 16% in late 2025 as borrowers chased lower rates, and PEXA holds a leading share in this high-activity sub-sector of the mature Australian market.

The product line benefits from renewed growth as homeowners seek better deals, driving higher transaction frequency and fee income while reinforcing platform dominance.

- 16% volume rise in late 2025

- High market share in refinance segment

- Renewed growth cycle from rate shifts

- Increased transaction fees and frequency

PEXA Strategic AML Solutions

PEXA is positioning PEXA Strategic AML Solutions as a Star: with July 2026 AML/digital ID rules, addressable market growth is estimated at +18% CAGR to 2028 and PEXA expects to capture a leading share by investing A$40–60m in FY25–26 to scale tooling for 20,000+ lawyer and bank users.

- New regs live July 2026 — spike in compliance spend

- PEXA investing A$40–60m FY25–26

- Targeting 20,000+ users (law firms, banks)

- Market growth ~18% CAGR to 2028

PEXA targets rapid share gains with £90–140m/A$40–60m push to seize 45–60% network wins

PEXA’s Stars: UK Remortgage Platform, PEXAPay, AU Refinance, and Strategic AML show rapid share gains in high-growth markets; combined 2025/26 invest of ~£90–140m/A$40–60m aims to capture ~45–60% network effects in target segments, driving fee and volume upside.

| Product | 2025 Metric | Capex FY25–26 |

|---|---|---|

| UK Remortgage | 1.1m digital txns; +28% | £25–30m |

| PEXAPay | £18.4bn flows; +28% | £65–85m |

| AU Refinance | +16% vol | — |

| AML | 18% CAGR to 2028 | A$40–60m |

What is included in the product

Comprehensive BCG Matrix analysis of PEXA’s portfolio with strategic recommendations, risks per quadrant, and investment priorities.

One-page PEXA BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

PEXA Exchange Australia Core

PEXA Exchange Australia Core dominates with roughly 90% market share of all property transactions and in FY2024 delivered about A$150m EBITDA on A$220m revenue, reflecting EBITDA margins near 68%, making it the group's primary cash generator.

As a near-monopoly in a mature market, it funds international expansion and R&D—PEXA allocated A$45m in 2024 to overseas growth and new digital products, covering most capex and strategic investments.

PEXA Transfer Settlements Australia

Property transfer settlements are a stable, mature revenue stream requiring minimal new marketing spend; PEXA reported 5.6 million transactions in FY2024, generating ~A$143m in settlement fees, up 4% year-on-year.

PEXA Workspace for Conveyancers

PEXA Workspace for Conveyancers is the industry-standard digital workspace used by over 18,000 Australian lawyers and conveyancers as of Dec 2025, creating high switching costs and strong user lock-in.

It requires low incremental investment—development capex under A$10m annually in FY2025—while sustaining dominant workflow integration across settlements.

As a foundational cash generator, Workspace delivered ~A$75m EBITDA in FY2025 and benefits from Australia’s relatively stable housing turnover (≈1.2m dwellings sold in 2024).

PEXA National Lodgement Services

PEXA National Lodgement Services is a cash cow: digital lodgement of land documents is a mature service PEXA has refined over a decade, and the 2025 completion of the Northern Territory rollout leaves minimal geographic expansion while sustaining near-total market share.

High-throughput infrastructure yields strong unit economics—industry reports show >60% gross margins on lodgements and annual processing volumes ~25M documents (FY2024–25), locking stable, repeatable cash flow.

- Near-100% market share in all Australian jurisdictions (NT rollout completed 2025)

- ~25 million documents processed annually (FY2024–25)

- Gross margin >60% per document

- Limited geographic upside; focus on yield and efficiency

PEXA Financial Institution Integration

PEXA's deep technical integrations with Australia's major banks yield steady volumes—institutional settlements handled ~65% of platform transactions in FY2024, producing recurring cash flow and ~A$40–50m EBITDA contribution annually to the group.

These connections are high switching-cost assets, hard for competitors to displace, so PEXA stays the primary channel for institutional property settlements and needs only maintenance-level capex.

- ~65% platform transactions: institutional

- A$40–50m annual EBITDA

- Low maintenance capex

- High switching costs, durable market position

PEXA: Dominant Exchange, Strong Cash Flows—A$150m EBITDA + A$115–125m from Workspace

PEXA's core businesses are cash cows: Exchange Australia Core (≈90% share) drove ~A$150m EBITDA on A$220m revenue in FY2024; Workspace and Lodgement together added ~A$115–125m EBITDA in FY2025 with low capex; institutional flows (~65% of transactions) contribute A$40–50m EBITDA and stable volumes (5.6M settlements, ~25M documents FY2024–25).

| Metric | Value |

|---|---|

| Exchange share | ≈90% |

| Exchange FY2024 EBITDA | A$150m |

| Revenue FY2024 | A$220m |

| Settlements | 5.6M (2024) |

| Documents | ≈25M (FY2024–25) |

| Institutional % | ≈65% |

| Group capex |

Delivered as Shown

PEXA BCG Matrix

The file you're previewing on this page is the final BCG Matrix report you'll receive after purchase; no watermarks, no demo content—just a fully formatted, ready-to-use strategic analysis crafted for clarity and decision-making.

This preview is the exact document you'll download post-purchase, built with market-backed insights and professional layout so you can present, edit, or print without further revisions.

Once purchased, the complete file is delivered directly to your inbox—instantly available for use in business planning, investor decks, or client presentations.

You're viewing the authentic BCG Matrix report that becomes yours with a one-time purchase, prepared by strategy professionals and formatted for immediate application.