Peyto Exploration & Development Business Model Canvas

Peyto Exploration: Concise Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind Peyto Exploration & Development’s business model—this concise Business Model Canvas exposes its value propositions, asset-led revenue streams, key partnerships, and cost drivers to show how the company scales and manages cyclicality; ideal for investors, analysts, and strategists seeking actionable, ready-to-use insights—download the complete Word & Excel files to benchmark, plan, or present with confidence.

Partnerships

Midstream Infrastructure Providers

Peyto partners with major pipeline operators such as TC Energy to secure firm transportation from the Deep Basin, often contracting multi-year capacity; in 2024 Peyto moved ~95% of its gas via contracted pipelines to Alberta and U.S. markets, protecting realized prices.

Oilfield Service Contractors

Peyto partners with drilling, completions and maintenance contractors to execute its ~C$350–400M annual capital program, relying on specialist rigs and frac fleets to target Spirit River and Cardium horizontals; multi‑year contracts improve cost predictability (helping keep LOE and F&D near recent levels) and enable newer techniques that cut cycle times by ~10–20% per well.

Financial Institutions and Lenders

Peyto secures capital via a syndicate of Canadian and international banks providing committed credit facilities and a US$300m revolving demand facility (2025), covering seasonal drilling peaks and M&A; these lines supported liquidity during 2024 capex of C$220m and helped keep net debt/EBITDA around 1.8x as of Q4 2025.

Government and Regulatory Bodies

Peyto partners with the Alberta Energy Regulator and provincial departments to meet environmental and safety rules, manage permitting, and comply with methane regulations that cut emissions 45% from 2019 levels under provincial targets updated in 2023.

Proactive regulator engagement preserves Peyto’s social license and underpins stable development of ~450 MMcf/d acreage exposure and FY2024 capital plan of C$120–140M.

- Compliance with AER and provincial rules

- Permitting for wells and facilities

- Adhering to methane rules (45% reduction vs 2019)

- Supports social license and 450 MMcf/d resource base

- Aligns with C$120–140M FY2024 capex

Joint Venture and Working Interest Partners

In the Deep Basin, Peyto forms joint ventures with peers to split exploration risk and capital; in 2024 JV-funded projects covered ~35% of Peyto’s capital program, cutting its net capex by about C$45m.

These JVs pool infrastructure and geological data to boost drill hit rates (Peyto reports a JV success uplift ~12%) and working-interest partners help spread the cash burden on multi-well pads and seismic programs.

- 2024: JVs financed ~35% of capex (~C$45m saved)

- JV drill success uplift ~12%

- Shared infrastructure reduces per-well cost

- Working-interest partners lower capital intensity of pads/seismic

Peyto locks 95% pipeline cover, C$350–400M capex with JV funding & US$300M RCF

Peyto secures long‑term pipeline capacity (TC Energy) moving ~95% of gas via contracts in 2024, uses multi‑year drilling/frac contracts to run a C$350–400M program, relies on bank credit lines including a US$300M RCF (2025) keeping net debt/EBITDA ~1.8x, meets AER methane cuts (45% vs 2019), and JV‑funding covered ~35% of 2024 capex (~C$45M saved).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Pipeline contracts | % gas via contract | ~95% |

| Contractors | Annual capex program | C$350–400M |

| Bank facilities | RCF | US$300M (2025) |

| Regulator | Emissions cut | 45% vs 2019 |

| JVs | Capex financed / savings | ~35% / ~C$45M |

What is included in the product

A concise Business Model Canvas for Peyto Exploration & Development mapping its asset-light upstream gas-focused value proposition, core customer segments (utilities, pipelines, industrial buyers), channels, key activities (exploration, development, midstream optimization), partners, revenue streams, cost structure, and capital allocation priorities, with linked SWOT insights and competitive advantages for investor presentations and strategic analysis.

High-level view of Peyto Exploration & Development’s business model with editable cells, streamlining analysis of upstream operations, revenue drivers, and cost structure.

Activities

Exploration and Drilling Operations

The core activity is systematic identification and extraction of natural gas and liquids in the Deep Basin, using horizontal drilling and multi-stage hydraulic fracturing to boost recovery from tight gas; Peyto produced ~280 MMcf/d of gas and 45,000 boe/d in 2024 while maintaining a 2024 reserve replacement ratio near 110%.

Facility Management and Processing

Peyto owns and operates most of its gas processing plants and gathering systems, running daily oversight of compressors, fractionators and scrubbers to separate gas, liquids and remove H2S/CO2; in 2024 Peyto processed ~300 MMcf/d and reported midstream revenue of CAD 48M, keeping unit operating costs low and offering toll-processing to third-party producers at competitive rates.

Commodity Marketing and Hedging

Peyto actively markets Alberta natural gas across hubs like AECO and Empress, using hub arbitrage to raise realized prices—achieving average realized gas prices of about C$6.50/GJ in 2024 versus AECO spot C$3.80/GJ.

The firm uses collars, swaps and basis hedges to protect cash flow; as of Q4 2024 roughly 70% of 2025 volumes were hedged, cutting price volatility and securing funding for capital and dividends.

Environmental Stewardship and Reclamation

Peyto monitors scope 1 and 2 emissions and funds asset retirement obligations (AROs) worth about CAD 220 million as of Dec 31, 2024, while deploying methane capture and water-recycling tech to cut fugitive emissions and freshwater use.

Regular site inspections and progressive reclamation restore land after production ends, supporting a 2030 target to reduce methane intensity by ~30% from 2020 levels.

- CAD 220M AROs (Dec 31, 2024)

- Methane capture systems deployed across major pads

- Water recycling programs cut freshwater drawdown

- Routine inspections; progressive land reclamation

- 2030 methane intensity reduction target ~30% vs 2020

Strategic Capital Allocation

Management reallocates cash flow between drilling and dividends, targeting projects with top IRRs; in 2025 Peyto prioritized Montney wells averaging break-evens near CAD 35/boe and returned CAD 0.18/share in quarterly dividends (2025 YTD), supporting per-share growth.

Here’s the quick math: rigorous DCF and scenario models rank opportunities by NPV/acre and payout period, favoring high-quality rock and operating cost cuts (2024 cash G&A down 8% YoY) to boost sustainable returns.

- Target break-even ~CAD 35/boe

- 2025 YTD dividend CAD 0.18/share

- 2024 G&A -8% YoY

- Decision metrics: IRR, NPV/acre, payback months

Montney-focused producer: strong 2024 cash flows, 70% hedged 2025, CAD35/boe breakeven

Core activities: exploration and extraction of Montney gas/liquids (2024 production ~280 MMcf/d gas, 45,000 boe/d; RRR ~110%), midstream processing (~300 MMcf/d; CAD 48M revenue 2024), marketing/hedging (realized C$6.50/GJ vs AECO C$3.80/GJ; ~70% 2025 volumes hedged), emissions/AROs (CAD 220M AROs; 2030 methane −30% target), capital allocation to high-IRR wells (target break-even ~CAD 35/boe; 2025 YTD dividend CAD 0.18/share).

| Metric | Value |

|---|---|

| 2024 gas prod | ~280 MMcf/d |

| 2024 boe/d | 45,000 |

| Reserve replacement | ~110% |

| Midstream rev 2024 | CAD 48M |

| Realized gas price 2024 | C$6.50/GJ |

| AECO spot 2024 | C$3.80/GJ |

| Hedged 2025 volumes | ~70% |

| AROs (Dec 31, 2024) | CAD 220M |

| Break-even target | ~CAD 35/boe |

| 2025 YTD dividend | CAD 0.18/share |

Delivered as Displayed

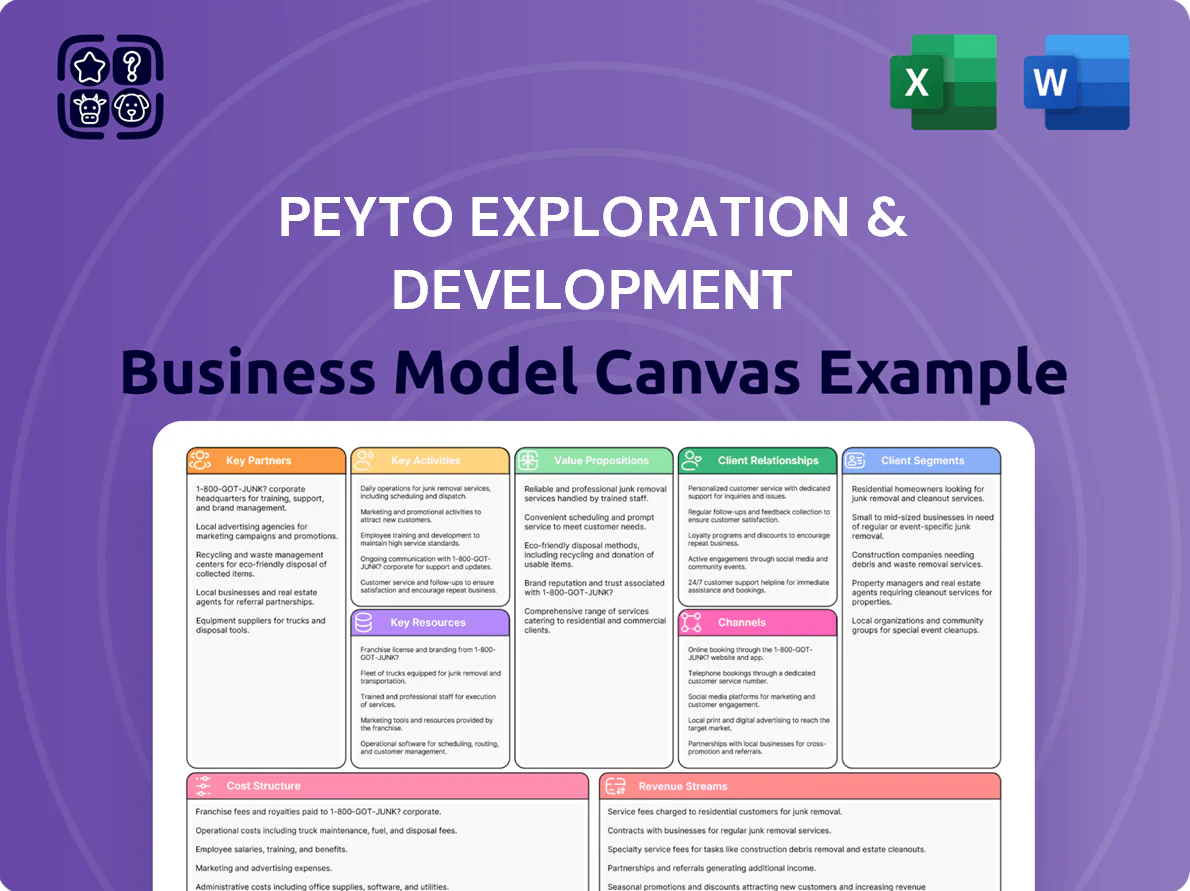

Business Model Canvas

The document you're previewing is the actual Peyto Exploration & Development Business Model Canvas—not a mockup—and it matches exactly the file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional, fully editable document, formatted and structured as shown, ready for use in Word and Excel.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Peyto Exploration: Concise Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind Peyto Exploration & Development’s business model—this concise Business Model Canvas exposes its value propositions, asset-led revenue streams, key partnerships, and cost drivers to show how the company scales and manages cyclicality; ideal for investors, analysts, and strategists seeking actionable, ready-to-use insights—download the complete Word & Excel files to benchmark, plan, or present with confidence.

Partnerships

Midstream Infrastructure Providers

Peyto partners with major pipeline operators such as TC Energy to secure firm transportation from the Deep Basin, often contracting multi-year capacity; in 2024 Peyto moved ~95% of its gas via contracted pipelines to Alberta and U.S. markets, protecting realized prices.

Oilfield Service Contractors

Peyto partners with drilling, completions and maintenance contractors to execute its ~C$350–400M annual capital program, relying on specialist rigs and frac fleets to target Spirit River and Cardium horizontals; multi‑year contracts improve cost predictability (helping keep LOE and F&D near recent levels) and enable newer techniques that cut cycle times by ~10–20% per well.

Financial Institutions and Lenders

Peyto secures capital via a syndicate of Canadian and international banks providing committed credit facilities and a US$300m revolving demand facility (2025), covering seasonal drilling peaks and M&A; these lines supported liquidity during 2024 capex of C$220m and helped keep net debt/EBITDA around 1.8x as of Q4 2025.

Government and Regulatory Bodies

Peyto partners with the Alberta Energy Regulator and provincial departments to meet environmental and safety rules, manage permitting, and comply with methane regulations that cut emissions 45% from 2019 levels under provincial targets updated in 2023.

Proactive regulator engagement preserves Peyto’s social license and underpins stable development of ~450 MMcf/d acreage exposure and FY2024 capital plan of C$120–140M.

- Compliance with AER and provincial rules

- Permitting for wells and facilities

- Adhering to methane rules (45% reduction vs 2019)

- Supports social license and 450 MMcf/d resource base

- Aligns with C$120–140M FY2024 capex

Joint Venture and Working Interest Partners

In the Deep Basin, Peyto forms joint ventures with peers to split exploration risk and capital; in 2024 JV-funded projects covered ~35% of Peyto’s capital program, cutting its net capex by about C$45m.

These JVs pool infrastructure and geological data to boost drill hit rates (Peyto reports a JV success uplift ~12%) and working-interest partners help spread the cash burden on multi-well pads and seismic programs.

- 2024: JVs financed ~35% of capex (~C$45m saved)

- JV drill success uplift ~12%

- Shared infrastructure reduces per-well cost

- Working-interest partners lower capital intensity of pads/seismic

Peyto locks 95% pipeline cover, C$350–400M capex with JV funding & US$300M RCF

Peyto secures long‑term pipeline capacity (TC Energy) moving ~95% of gas via contracts in 2024, uses multi‑year drilling/frac contracts to run a C$350–400M program, relies on bank credit lines including a US$300M RCF (2025) keeping net debt/EBITDA ~1.8x, meets AER methane cuts (45% vs 2019), and JV‑funding covered ~35% of 2024 capex (~C$45M saved).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Pipeline contracts | % gas via contract | ~95% |

| Contractors | Annual capex program | C$350–400M |

| Bank facilities | RCF | US$300M (2025) |

| Regulator | Emissions cut | 45% vs 2019 |

| JVs | Capex financed / savings | ~35% / ~C$45M |

What is included in the product

A concise Business Model Canvas for Peyto Exploration & Development mapping its asset-light upstream gas-focused value proposition, core customer segments (utilities, pipelines, industrial buyers), channels, key activities (exploration, development, midstream optimization), partners, revenue streams, cost structure, and capital allocation priorities, with linked SWOT insights and competitive advantages for investor presentations and strategic analysis.

High-level view of Peyto Exploration & Development’s business model with editable cells, streamlining analysis of upstream operations, revenue drivers, and cost structure.

Activities

Exploration and Drilling Operations

The core activity is systematic identification and extraction of natural gas and liquids in the Deep Basin, using horizontal drilling and multi-stage hydraulic fracturing to boost recovery from tight gas; Peyto produced ~280 MMcf/d of gas and 45,000 boe/d in 2024 while maintaining a 2024 reserve replacement ratio near 110%.

Facility Management and Processing

Peyto owns and operates most of its gas processing plants and gathering systems, running daily oversight of compressors, fractionators and scrubbers to separate gas, liquids and remove H2S/CO2; in 2024 Peyto processed ~300 MMcf/d and reported midstream revenue of CAD 48M, keeping unit operating costs low and offering toll-processing to third-party producers at competitive rates.

Commodity Marketing and Hedging

Peyto actively markets Alberta natural gas across hubs like AECO and Empress, using hub arbitrage to raise realized prices—achieving average realized gas prices of about C$6.50/GJ in 2024 versus AECO spot C$3.80/GJ.

The firm uses collars, swaps and basis hedges to protect cash flow; as of Q4 2024 roughly 70% of 2025 volumes were hedged, cutting price volatility and securing funding for capital and dividends.

Environmental Stewardship and Reclamation

Peyto monitors scope 1 and 2 emissions and funds asset retirement obligations (AROs) worth about CAD 220 million as of Dec 31, 2024, while deploying methane capture and water-recycling tech to cut fugitive emissions and freshwater use.

Regular site inspections and progressive reclamation restore land after production ends, supporting a 2030 target to reduce methane intensity by ~30% from 2020 levels.

- CAD 220M AROs (Dec 31, 2024)

- Methane capture systems deployed across major pads

- Water recycling programs cut freshwater drawdown

- Routine inspections; progressive land reclamation

- 2030 methane intensity reduction target ~30% vs 2020

Strategic Capital Allocation

Management reallocates cash flow between drilling and dividends, targeting projects with top IRRs; in 2025 Peyto prioritized Montney wells averaging break-evens near CAD 35/boe and returned CAD 0.18/share in quarterly dividends (2025 YTD), supporting per-share growth.

Here’s the quick math: rigorous DCF and scenario models rank opportunities by NPV/acre and payout period, favoring high-quality rock and operating cost cuts (2024 cash G&A down 8% YoY) to boost sustainable returns.

- Target break-even ~CAD 35/boe

- 2025 YTD dividend CAD 0.18/share

- 2024 G&A -8% YoY

- Decision metrics: IRR, NPV/acre, payback months

Montney-focused producer: strong 2024 cash flows, 70% hedged 2025, CAD35/boe breakeven

Core activities: exploration and extraction of Montney gas/liquids (2024 production ~280 MMcf/d gas, 45,000 boe/d; RRR ~110%), midstream processing (~300 MMcf/d; CAD 48M revenue 2024), marketing/hedging (realized C$6.50/GJ vs AECO C$3.80/GJ; ~70% 2025 volumes hedged), emissions/AROs (CAD 220M AROs; 2030 methane −30% target), capital allocation to high-IRR wells (target break-even ~CAD 35/boe; 2025 YTD dividend CAD 0.18/share).

| Metric | Value |

|---|---|

| 2024 gas prod | ~280 MMcf/d |

| 2024 boe/d | 45,000 |

| Reserve replacement | ~110% |

| Midstream rev 2024 | CAD 48M |

| Realized gas price 2024 | C$6.50/GJ |

| AECO spot 2024 | C$3.80/GJ |

| Hedged 2025 volumes | ~70% |

| AROs (Dec 31, 2024) | CAD 220M |

| Break-even target | ~CAD 35/boe |

| 2025 YTD dividend | CAD 0.18/share |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Peyto Exploration & Development Business Model Canvas—not a mockup—and it matches exactly the file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional, fully editable document, formatted and structured as shown, ready for use in Word and Excel.