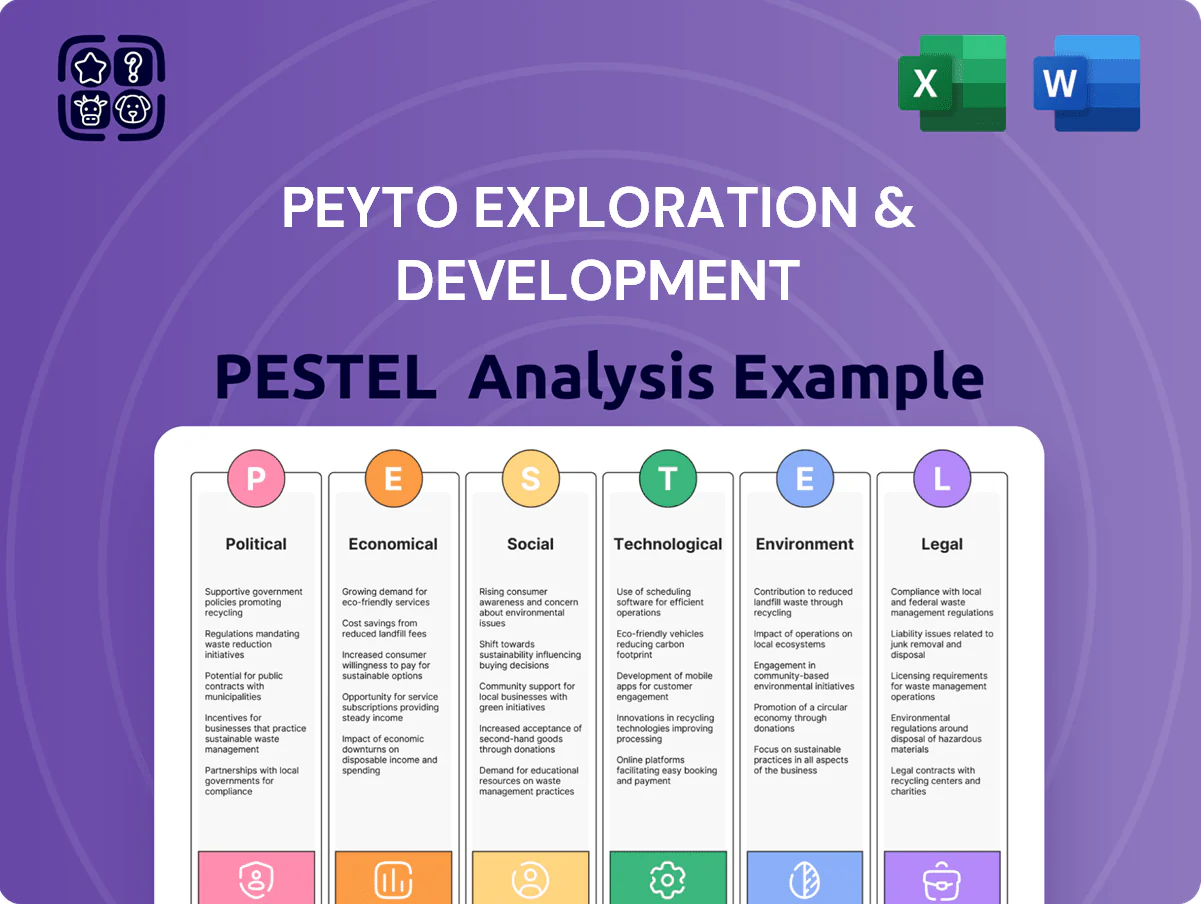

Peyto Exploration & Development PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Peyto Exploration & Development—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures will shape its outlook; purchase the full report for detailed, actionable insights you can use in investment theses, strategy sessions, or competitive analysis.

Political factors

Federal and Provincial Regulatory Friction

The federal-provincial dispute over emissions caps—highlighted by Ottawa’s 2030 target to cut GHGs 40-45% vs 2005 and Alberta’s 2023 legal challenge—creates compliance uncertainty for Peyto, which reported Scope 1+2 emissions of ~1.1 Mt CO2e in 2024; shifting rules could raise operating costs and capex for CCS or methane abatement.

Indigenous Consultation and Land Rights

Engagement with Indigenous communities in Alberta's Deep Basin is a political priority for Peyto as delays and litigation over Treaty rights can add months and millions to projects; in 2024 Alberta recorded 18 major project disputes involving Indigenous consultation. Strengthening meaningful consultation and negotiating Indigenous equity participation—now seen in deals averaging 5–15% stake in resource projects—reduces risk and supports environmental stewardship commitments tied to permitting and financing.

Energy Export and Infrastructure Policy

Federal approval of pipelines and LNG export terminals directly affects Peyto’s access to Asia; Canada approved LNG Canada Phase 1 (14 mtpa) and in 2024 federal permits sped project timelines, underpinning export capacity that could absorb ~1–2 bcfd of incremental Montney gas from producers like Peyto.

Carbon Pricing and Fiscal Policy

The federal carbon tax, rising to C$65/tCO2e in 2023 and scheduled targets of C$170/tCO2e by 2030 under federal plans, materially raises Peyto’s operating costs and influences capex allocations across its thermal and emissions-reduction projects.

Political shifts in Ottawa or provincial program changes (e.g., Alberta’s Technology Innovation and Emissions Reduction fund adjustments) can alter royalties or tax credits, creating sudden impacts on cash flow and project IRRs.

Peyto needs active lobbying and industry association engagement to preserve competitive fiscal treatment versus U.S. peers; failure could widen cost differentials and reduce investment appeal.

- Federal carbon tax: C$65/tCO2e (2023), rising toward C$170/tCO2e by 2030

- Provincial program variability can change royalty/tax incentives, affecting IRR

- Active lobbying needed to maintain competitive fiscal policy versus global energy jurisdictions

Geopolitical Influence on Energy Security

Global political instability boosts demand for Canadian natural gas; Canada exported C$62.1B of energy products in 2024, underlining Peyto’s strategic position supplying allies seeking stable sources.

Western diversification away from Russia and others favors LNG markets where Canadian players can gain market share, supporting Peyto’s export potential amid higher price volatility.

However, sanctions and trade disputes risk delays and 10–20% cost uplifts for specialized drilling equipment, threatening project timelines and margins.

- 2024 Canadian energy exports C$62.1B

- Equipment cost risk: +10–20%

- Increased LNG demand benefits domestic producers

Canada energy outlook: rising carbon costs, regulatory risks, and export opportunity

Federal-provincial GHG policy uncertainty (Ottawa 2030 target −40–45% vs 2005; Alberta legal challenge) risks higher capex for CCS/methane abatement; Peyto reported Scope 1+2 ≈1.1 Mt CO2e in 2024. Indigenous consultation delays (18 major disputes in AB, 2024) and shifting royalties/tax credits change IRRs; federal carbon tax C$65/tCO2e (2023) rising toward C$170/t by 2030 raises operating costs. Export infrastructure approvals (LNG Canada 14 mtpa) support 1–2 bcfd potential offtake; 2024 Canadian energy exports C$62.1B.

| Metric | 2024 / Target |

|---|---|

| Scope 1+2 emissions | ≈1.1 Mt CO2e |

| Federal carbon tax | C$65/t (2023) → C$170/t by 2030 |

| Alberta disputes | 18 major project disputes (2024) |

| Canadian energy exports | C$62.1B (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Peyto Exploration & Development across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tied to Canadian oil & gas market dynamics and regional policy trends to identify risks and opportunities for executives, investors, and strategists.

A compact PESTLE summary for Peyto Exploration & Development that clarifies regulatory, environmental, market and geopolitical risks—ready to drop into presentations or share across teams to streamline risk discussions and strategic planning.

Economic factors

Natural Gas Price Volatility

Peyto's revenue is highly sensitive to AECO and NYMEX natural gas price swings; in 2024 AECO averaged ~C$2.85/GJ and Henry Hub (NYMEX) averaged US$2.55/MMBtu, driving earnings volatility.

By 2025, added LNG capacity in Western Canada—projected 5–10 mtpa of export capacity—should narrow the AECO–Henry Hub differential, potentially tightening Canadian prices toward US benchmarks.

Peyto's robust hedging program covered ~60–70% of 2024 production, providing predictable cash flow to support C$150–200 million annual capex and its sustainable dividend policy.

Inflationary Pressures and Capital Costs

Persistent inflation in the energy services sector has driven labor, steel and equipment costs up about 8–12% Y/Y in 2024, pressuring well-level costs for drilling and completions.

Peyto offsets these pressures through an industry-leading low-cost structure and ownership of midstream assets, cutting third-party transport and processing expenses and supporting lower operating cash costs per boe (reported ~$6–8/boe in 2024).

With Canadian bank prime and corporate yields elevated—Bank of Canada policy rate ~5% in 2024 and term borrowing costs higher than a decade ago—maintaining capital efficiency is essential to preserve margins.

Impact of Interest Rates on Debt Service

The Bank of Canada’s policy rate at 5.00% (Feb 2025) raises Peyto’s cost of servicing its $800m+ revolving facilities and $500m+ long-term debt after the Repsol asset acquisition, pressuring interest expense and 2024–2025 net earnings sensitivity to rate shifts.

Active debt repayment and sustaining a BBB+ senior credit profile helped Peyto secure ~US$/CDN cheaper spreads in 2024, preserving access to affordable capital amid potential rate volatility.

Labor Market Dynamics in Alberta

The Alberta oil patch faces tight competition for skilled labor as a wave of retirements and growth in renewables and hydrogen projects squeeze supply; Alberta recorded a 5.4% decline in oil-and-gas core workforce participation from 2019–2024 while renewable hiring rose 18% (2023–2024).

Wage inflation pressures hiring costs—average field operator wages rose ~12% and senior engineer pay climbed ~15% in Alberta between 2021–2024—raising OPEX for producers.

Peyto emphasizes automation and process optimization, investing in digital well monitoring and robotics to protect production; capital deployment toward efficiency reduced per-BOE operating costs by ~8% in 2023 vs 2021.

- Retirements + renewables growth tighten labor supply

- Field/operator wages +12%, senior engineers +15% (2021–2024)

- Peyto cuts per-BOE OPEX ~8% via automation (2023 vs 2021)

Currency Exchange Rate Fluctuations

As a Canadian producer selling gas often priced in USD, Peyto's revenue in CAD rises when the Canadian dollar weakens; CAD fell ~6% vs USD in 2024, boosting foreign‑denominated receipts for Canadian exporters.

However, a weaker CAD raises costs for imported rigs and compressors—capital equipment that can represent millions per project—eroding net margins if not hedged.

Financial planning must use FX risk management: Peyto should model sensitivities (e.g., a 5% CAD depreciation increases USD revenue in CAD by ~5%) and employ hedges or USD debt to protect purchasing power and competitiveness.

- 2024 CAD vs USD change ~-6%

- 5% CAD depreciation → ~5% lift in CAD‑reported USD revenues

- Imported capex exposure: significant cost inflation risk without hedging

Peyto: Gas-price swings, higher costs & hedges shape 2024 revenue outlook

Peyto faces gas-price-driven revenue volatility (AECO C$2.85/GJ 2024; HH US$2.55/MMBtu), rising service costs (+8–12% Y/Y 2024), higher borrowing costs (BoC ~5% 2024–Feb 2025), ~C$6–8/boe opex, hedging covering ~60–70% 2024 production, CAD −6% vs USD 2024 boosting CAD revenues but raising imported capex costs.

| Metric | 2024/2025 |

|---|---|

| AECO | C$2.85/GJ |

| HH | US$2.55/MMBtu |

| Opex | C$6–8/boe |

| Hedged | 60–70% |

| BoC rate | ~5% |

| CAD vs USD | −6% |

Same Document Delivered

Peyto Exploration & Development PESTLE Analysis

The preview shown here is the exact Peyto Exploration & Development PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the same content, layout, and insights as the downloadable document, with no placeholders or teasers. After checkout you’ll immediately get this exact, final version for analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Peyto Exploration & Development—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures will shape its outlook; purchase the full report for detailed, actionable insights you can use in investment theses, strategy sessions, or competitive analysis.

Political factors

Federal and Provincial Regulatory Friction

The federal-provincial dispute over emissions caps—highlighted by Ottawa’s 2030 target to cut GHGs 40-45% vs 2005 and Alberta’s 2023 legal challenge—creates compliance uncertainty for Peyto, which reported Scope 1+2 emissions of ~1.1 Mt CO2e in 2024; shifting rules could raise operating costs and capex for CCS or methane abatement.

Indigenous Consultation and Land Rights

Engagement with Indigenous communities in Alberta's Deep Basin is a political priority for Peyto as delays and litigation over Treaty rights can add months and millions to projects; in 2024 Alberta recorded 18 major project disputes involving Indigenous consultation. Strengthening meaningful consultation and negotiating Indigenous equity participation—now seen in deals averaging 5–15% stake in resource projects—reduces risk and supports environmental stewardship commitments tied to permitting and financing.

Energy Export and Infrastructure Policy

Federal approval of pipelines and LNG export terminals directly affects Peyto’s access to Asia; Canada approved LNG Canada Phase 1 (14 mtpa) and in 2024 federal permits sped project timelines, underpinning export capacity that could absorb ~1–2 bcfd of incremental Montney gas from producers like Peyto.

Carbon Pricing and Fiscal Policy

The federal carbon tax, rising to C$65/tCO2e in 2023 and scheduled targets of C$170/tCO2e by 2030 under federal plans, materially raises Peyto’s operating costs and influences capex allocations across its thermal and emissions-reduction projects.

Political shifts in Ottawa or provincial program changes (e.g., Alberta’s Technology Innovation and Emissions Reduction fund adjustments) can alter royalties or tax credits, creating sudden impacts on cash flow and project IRRs.

Peyto needs active lobbying and industry association engagement to preserve competitive fiscal treatment versus U.S. peers; failure could widen cost differentials and reduce investment appeal.

- Federal carbon tax: C$65/tCO2e (2023), rising toward C$170/tCO2e by 2030

- Provincial program variability can change royalty/tax incentives, affecting IRR

- Active lobbying needed to maintain competitive fiscal policy versus global energy jurisdictions

Geopolitical Influence on Energy Security

Global political instability boosts demand for Canadian natural gas; Canada exported C$62.1B of energy products in 2024, underlining Peyto’s strategic position supplying allies seeking stable sources.

Western diversification away from Russia and others favors LNG markets where Canadian players can gain market share, supporting Peyto’s export potential amid higher price volatility.

However, sanctions and trade disputes risk delays and 10–20% cost uplifts for specialized drilling equipment, threatening project timelines and margins.

- 2024 Canadian energy exports C$62.1B

- Equipment cost risk: +10–20%

- Increased LNG demand benefits domestic producers

Canada energy outlook: rising carbon costs, regulatory risks, and export opportunity

Federal-provincial GHG policy uncertainty (Ottawa 2030 target −40–45% vs 2005; Alberta legal challenge) risks higher capex for CCS/methane abatement; Peyto reported Scope 1+2 ≈1.1 Mt CO2e in 2024. Indigenous consultation delays (18 major disputes in AB, 2024) and shifting royalties/tax credits change IRRs; federal carbon tax C$65/tCO2e (2023) rising toward C$170/t by 2030 raises operating costs. Export infrastructure approvals (LNG Canada 14 mtpa) support 1–2 bcfd potential offtake; 2024 Canadian energy exports C$62.1B.

| Metric | 2024 / Target |

|---|---|

| Scope 1+2 emissions | ≈1.1 Mt CO2e |

| Federal carbon tax | C$65/t (2023) → C$170/t by 2030 |

| Alberta disputes | 18 major project disputes (2024) |

| Canadian energy exports | C$62.1B (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Peyto Exploration & Development across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tied to Canadian oil & gas market dynamics and regional policy trends to identify risks and opportunities for executives, investors, and strategists.

A compact PESTLE summary for Peyto Exploration & Development that clarifies regulatory, environmental, market and geopolitical risks—ready to drop into presentations or share across teams to streamline risk discussions and strategic planning.

Economic factors

Natural Gas Price Volatility

Peyto's revenue is highly sensitive to AECO and NYMEX natural gas price swings; in 2024 AECO averaged ~C$2.85/GJ and Henry Hub (NYMEX) averaged US$2.55/MMBtu, driving earnings volatility.

By 2025, added LNG capacity in Western Canada—projected 5–10 mtpa of export capacity—should narrow the AECO–Henry Hub differential, potentially tightening Canadian prices toward US benchmarks.

Peyto's robust hedging program covered ~60–70% of 2024 production, providing predictable cash flow to support C$150–200 million annual capex and its sustainable dividend policy.

Inflationary Pressures and Capital Costs

Persistent inflation in the energy services sector has driven labor, steel and equipment costs up about 8–12% Y/Y in 2024, pressuring well-level costs for drilling and completions.

Peyto offsets these pressures through an industry-leading low-cost structure and ownership of midstream assets, cutting third-party transport and processing expenses and supporting lower operating cash costs per boe (reported ~$6–8/boe in 2024).

With Canadian bank prime and corporate yields elevated—Bank of Canada policy rate ~5% in 2024 and term borrowing costs higher than a decade ago—maintaining capital efficiency is essential to preserve margins.

Impact of Interest Rates on Debt Service

The Bank of Canada’s policy rate at 5.00% (Feb 2025) raises Peyto’s cost of servicing its $800m+ revolving facilities and $500m+ long-term debt after the Repsol asset acquisition, pressuring interest expense and 2024–2025 net earnings sensitivity to rate shifts.

Active debt repayment and sustaining a BBB+ senior credit profile helped Peyto secure ~US$/CDN cheaper spreads in 2024, preserving access to affordable capital amid potential rate volatility.

Labor Market Dynamics in Alberta

The Alberta oil patch faces tight competition for skilled labor as a wave of retirements and growth in renewables and hydrogen projects squeeze supply; Alberta recorded a 5.4% decline in oil-and-gas core workforce participation from 2019–2024 while renewable hiring rose 18% (2023–2024).

Wage inflation pressures hiring costs—average field operator wages rose ~12% and senior engineer pay climbed ~15% in Alberta between 2021–2024—raising OPEX for producers.

Peyto emphasizes automation and process optimization, investing in digital well monitoring and robotics to protect production; capital deployment toward efficiency reduced per-BOE operating costs by ~8% in 2023 vs 2021.

- Retirements + renewables growth tighten labor supply

- Field/operator wages +12%, senior engineers +15% (2021–2024)

- Peyto cuts per-BOE OPEX ~8% via automation (2023 vs 2021)

Currency Exchange Rate Fluctuations

As a Canadian producer selling gas often priced in USD, Peyto's revenue in CAD rises when the Canadian dollar weakens; CAD fell ~6% vs USD in 2024, boosting foreign‑denominated receipts for Canadian exporters.

However, a weaker CAD raises costs for imported rigs and compressors—capital equipment that can represent millions per project—eroding net margins if not hedged.

Financial planning must use FX risk management: Peyto should model sensitivities (e.g., a 5% CAD depreciation increases USD revenue in CAD by ~5%) and employ hedges or USD debt to protect purchasing power and competitiveness.

- 2024 CAD vs USD change ~-6%

- 5% CAD depreciation → ~5% lift in CAD‑reported USD revenues

- Imported capex exposure: significant cost inflation risk without hedging

Peyto: Gas-price swings, higher costs & hedges shape 2024 revenue outlook

Peyto faces gas-price-driven revenue volatility (AECO C$2.85/GJ 2024; HH US$2.55/MMBtu), rising service costs (+8–12% Y/Y 2024), higher borrowing costs (BoC ~5% 2024–Feb 2025), ~C$6–8/boe opex, hedging covering ~60–70% 2024 production, CAD −6% vs USD 2024 boosting CAD revenues but raising imported capex costs.

| Metric | 2024/2025 |

|---|---|

| AECO | C$2.85/GJ |

| HH | US$2.55/MMBtu |

| Opex | C$6–8/boe |

| Hedged | 60–70% |

| BoC rate | ~5% |

| CAD vs USD | −6% |

Same Document Delivered

Peyto Exploration & Development PESTLE Analysis

The preview shown here is the exact Peyto Exploration & Development PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the same content, layout, and insights as the downloadable document, with no placeholders or teasers. After checkout you’ll immediately get this exact, final version for analysis and decision-making.