Peyto Exploration & Development SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Peyto’s resilient cash flow and low-cost Montney foothold contrast with commodity sensitivity and limited diversification—our full SWOT unpacks how capital allocation, reserve quality, and ESG positioning will shape value. Purchase the complete SWOT analysis to access a research-backed, editable Word and Excel package with strategic recommendations and financial context for investors and advisors.

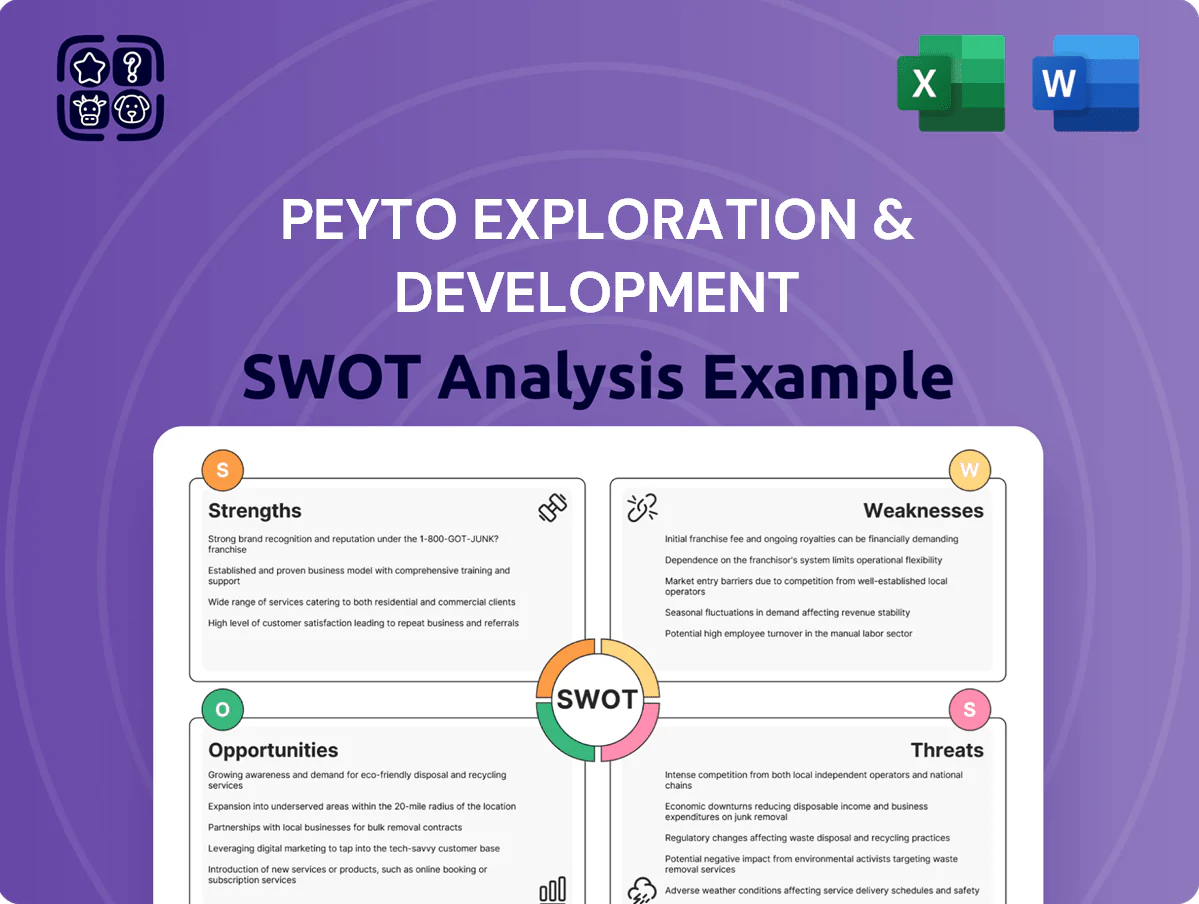

Strengths

Industry-Leading Low Cost Structure

Peyto keeps one of the lowest operating costs in Canada’s oil & gas sector, reporting $6.90/boe operating expenses in 2024, driven by a lean staffing model and fewer service contracts.

That efficiency helped generate free funds flow of C$410 million in 2024, sustaining payouts and buybacks even when AECO natural gas averaged C$2.75/GJ in H2 2024.

Ownership of Midstream Infrastructure

Peyto owns and operates most gas processing plants and gathering systems in the Deep Basin, giving control over production timing and cutting third-party processing fees—management reported 2024 third-party processing costs under 3% of operating expenses versus peers at ~8%.

This ownership secures priority access to capacity, lowers transport costs—estimated C$0.30/mcf savings in 2024—and supported Peyto’s EBITDA margin of 46% in 2024.

Concentrated Asset Base in Alberta Deep Basin

Peyto’s concentrated, long-life asset base in Alberta’s Deep Basin drives scale: 2024 production averaged ~75,000 boe/d with 2P reserves of ~550 mmboe, enabling the technical team to build deep geology expertise and optimize drilling for higher recovery and lower costs. The predictable reservoir performance supports five‑year production plans and capital efficiency—operating cash costs of ~$11/boe in 2024 illustrate repeatable margins and resource management.

High Operating Margins and Efficiency

The management team at Peyto Exploration & Development is known for disciplined capital allocation and a focus on per‑share metrics, targeting projects that clear a strict investment hurdle so capital is only deployed where it creates value.

This efficiency yielded adjusted funds from operations (AFFO) margins near 55% in 2024 and a return on capital employed (ROCE) around 18% for the five years ending 2024, showing resilience across cycles.

Prioritizing high‑return projects reduced capex per BOE to about CAD 12 in 2024, sustaining free cash flow and supporting buybacks and debt reduction.

- 2024 AFFO margin ~55%

- 5‑yr ROCE ~18% (to 2024)

- 2024 capex per BOE ~CAD 12

Strong Dividend and Capital Return History

Peyto has returned capital consistently, paying quarterly dividends and special returns; in 2024 it distributed about CAD 0.85 per share (total payouts ~CAD 220m), reflecting steady free cash flow generation from natural gas production.

The business targets disciplined spending: 2024 operating cash flow was ~CAD 520m while sustaining capex was ~CAD 140m, leaving ample surplus for distributions and balance-sheet strength.

- 2024 dividends ~CAD 0.85/share

- 2024 payouts ~CAD 220m

- 2024 operating cash flow ~CAD 520m

- Sustaining capex ~CAD 140m

Low-cost ops fuel C$410M FCF, 46% EBITDA and C$0.85/share payout in 2024

Low costs and owned processing drove C$410m FCF and 46% EBITDA margin in 2024; 75k boe/d, 2P ~550 mmboe, AFFO margin ~55%, ROCE ~18% (5‑yr to 2024); disciplined capex ~CAD12/boe and sustaining capex C$140m supported C$220m payouts (C$0.85/share).

| Metric | 2024 |

|---|---|

| Production | ~75k boe/d |

| 2P reserves | ~550 mmboe |

| FCF | C$410m |

| EBITDA margin | 46% |

What is included in the product

Provides a clear SWOT framework for analyzing Peyto Exploration & Development’s business strategy, highlighting its asset quality and operational efficiencies, internal vulnerabilities such as commodity exposure and capital constraints, external growth opportunities in gas demand and infrastructure optimization, and threats from price volatility, regulatory shifts, and competitive pressures.

Delivers a concise SWOT matrix for Peyto Exploration & Development to align strategy quickly and support investor and management decision-making.

Weaknesses

Geographic Concentration Risk

Peyto’s asset base is heavily concentrated in the Alberta Deep Basin, where ~85% of 2024 production (~112 mboe/d) and 90% of proved reserves sit, raising localized operational risk.

Regional regulatory shifts, winter freeze–thaw events, or a single pipeline outage could cut a material slice from cash flow and EBITDA given limited geographic spread.

Diversification is thin versus larger peers like Cenovus and Imperial, which lower region-specific exposure through multi-basin portfolios.

Commodity Price Sensitivity

Peyto’s revenue is highly sensitive to natural gas prices, which averaged US$2.60/MMBtu in 2025 YTD (AECO proxy ~C$2.40/MMBtu), exposing cash flow to price swings. The company hedged about 40% of 2025 volumes, which cushions but doesn’t eliminate risk—multiple quarters below C$2.50/MMBtu would pressure distributable cash. Limited liquids (oil/NGLs <5% of 2024 production) means little offset if gas markets stay weak.

Significant Debt from Recent Acquisitions

Following the late-2025 acquisition of Repsol’s Canadian assets, Peyto carries roughly CAD 1.1 billion of debt on its balance sheet, raising net debt/EBITDA to about 3.2x; interest expense runs near CAD 65 million annually, which tightens near-term cash flow.

That scale boost improves reserves and production but the interest and principal schedule could constrain capex and leave less room for dividend support.

Management must prioritize reducing leverage—targeting sub-2.5x net debt/EBITDA within 18–24 months—while phasing growth projects to avoid forced dividend cuts.

Limited Exposure to Liquids and Oil

Peyto’s production remains heavily weighted to dry natural gas, with liquids making up under 15% of volumes in 2024 versus peer averages near 35%, reducing revenue per boe and EBITDA margins compared with condensate/light‑oil heavy producers.

This mix raises sensitivity to North American gas price swings—AECO fell 30% in 2024—and limits upside from oil price rallies that boosted peers’ cash flow in 2023–24.

- Liquids <15% of production (2024)

- Peer liquids ~35% avg (2024)

- AECO -30% in 2024

- Lower $/boe and EBITDA margin vs oil-rich peers

Dependence on Regional Pipeline Access

Peyto’s sales are tied to Alberta’s AECO hub, so pipeline outages or capacity tightness can cut realized gas prices; AECO averaged about C$2.50/GJ in 2024 versus Henry Hub US$2.80/MMBtu, amplifying differentials.

Third-party midstream constraints—e.g., 2024 pipeline maintenance that trimmed takeaway by ~5–10%—pose a recurring bottleneck and risk to cash flow and production scheduling.

- AECO exposure: price differentials hit margins

- 2024 takeaway cuts ~5–10% from maintenance

- Dependence on midstream adds operational risk

Peyto: Alberta‑heavy dry‑gas play — C$2.50 AECO, CAD1.1bn net debt, 3.2x ND/EBITDA

Peyto is highly concentrated in Alberta (≈85% 2024 prod; 90% proved reserves), mostly dry gas (<15% liquids), making cash flow very sensitive to AECO gas swings (AECO ~C$2.50/GJ 2024; Henry Hub US$2.80/MMBtu). Post-2025 Repsol deal net debt ≈CAD1.1bn (net debt/EBITDA ~3.2x); interest ≈CAD65m/yr; midstream constraints trimmed takeaway ~5–10% in 2024.

| Metric | Value |

|---|---|

| 2024 production concentration | ~85% |

| Liquids % (2024) | <15% |

| AECO (2024) | C$2.50/GJ |

| Net debt | CAD1.1bn |

| Net debt/EBITDA | ~3.2x |

Preview Before You Purchase

Peyto Exploration & Development SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and contains the same structured strengths, weaknesses, opportunities, and threats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Peyto’s resilient cash flow and low-cost Montney foothold contrast with commodity sensitivity and limited diversification—our full SWOT unpacks how capital allocation, reserve quality, and ESG positioning will shape value. Purchase the complete SWOT analysis to access a research-backed, editable Word and Excel package with strategic recommendations and financial context for investors and advisors.

Strengths

Industry-Leading Low Cost Structure

Peyto keeps one of the lowest operating costs in Canada’s oil & gas sector, reporting $6.90/boe operating expenses in 2024, driven by a lean staffing model and fewer service contracts.

That efficiency helped generate free funds flow of C$410 million in 2024, sustaining payouts and buybacks even when AECO natural gas averaged C$2.75/GJ in H2 2024.

Ownership of Midstream Infrastructure

Peyto owns and operates most gas processing plants and gathering systems in the Deep Basin, giving control over production timing and cutting third-party processing fees—management reported 2024 third-party processing costs under 3% of operating expenses versus peers at ~8%.

This ownership secures priority access to capacity, lowers transport costs—estimated C$0.30/mcf savings in 2024—and supported Peyto’s EBITDA margin of 46% in 2024.

Concentrated Asset Base in Alberta Deep Basin

Peyto’s concentrated, long-life asset base in Alberta’s Deep Basin drives scale: 2024 production averaged ~75,000 boe/d with 2P reserves of ~550 mmboe, enabling the technical team to build deep geology expertise and optimize drilling for higher recovery and lower costs. The predictable reservoir performance supports five‑year production plans and capital efficiency—operating cash costs of ~$11/boe in 2024 illustrate repeatable margins and resource management.

High Operating Margins and Efficiency

The management team at Peyto Exploration & Development is known for disciplined capital allocation and a focus on per‑share metrics, targeting projects that clear a strict investment hurdle so capital is only deployed where it creates value.

This efficiency yielded adjusted funds from operations (AFFO) margins near 55% in 2024 and a return on capital employed (ROCE) around 18% for the five years ending 2024, showing resilience across cycles.

Prioritizing high‑return projects reduced capex per BOE to about CAD 12 in 2024, sustaining free cash flow and supporting buybacks and debt reduction.

- 2024 AFFO margin ~55%

- 5‑yr ROCE ~18% (to 2024)

- 2024 capex per BOE ~CAD 12

Strong Dividend and Capital Return History

Peyto has returned capital consistently, paying quarterly dividends and special returns; in 2024 it distributed about CAD 0.85 per share (total payouts ~CAD 220m), reflecting steady free cash flow generation from natural gas production.

The business targets disciplined spending: 2024 operating cash flow was ~CAD 520m while sustaining capex was ~CAD 140m, leaving ample surplus for distributions and balance-sheet strength.

- 2024 dividends ~CAD 0.85/share

- 2024 payouts ~CAD 220m

- 2024 operating cash flow ~CAD 520m

- Sustaining capex ~CAD 140m

Low-cost ops fuel C$410M FCF, 46% EBITDA and C$0.85/share payout in 2024

Low costs and owned processing drove C$410m FCF and 46% EBITDA margin in 2024; 75k boe/d, 2P ~550 mmboe, AFFO margin ~55%, ROCE ~18% (5‑yr to 2024); disciplined capex ~CAD12/boe and sustaining capex C$140m supported C$220m payouts (C$0.85/share).

| Metric | 2024 |

|---|---|

| Production | ~75k boe/d |

| 2P reserves | ~550 mmboe |

| FCF | C$410m |

| EBITDA margin | 46% |

What is included in the product

Provides a clear SWOT framework for analyzing Peyto Exploration & Development’s business strategy, highlighting its asset quality and operational efficiencies, internal vulnerabilities such as commodity exposure and capital constraints, external growth opportunities in gas demand and infrastructure optimization, and threats from price volatility, regulatory shifts, and competitive pressures.

Delivers a concise SWOT matrix for Peyto Exploration & Development to align strategy quickly and support investor and management decision-making.

Weaknesses

Geographic Concentration Risk

Peyto’s asset base is heavily concentrated in the Alberta Deep Basin, where ~85% of 2024 production (~112 mboe/d) and 90% of proved reserves sit, raising localized operational risk.

Regional regulatory shifts, winter freeze–thaw events, or a single pipeline outage could cut a material slice from cash flow and EBITDA given limited geographic spread.

Diversification is thin versus larger peers like Cenovus and Imperial, which lower region-specific exposure through multi-basin portfolios.

Commodity Price Sensitivity

Peyto’s revenue is highly sensitive to natural gas prices, which averaged US$2.60/MMBtu in 2025 YTD (AECO proxy ~C$2.40/MMBtu), exposing cash flow to price swings. The company hedged about 40% of 2025 volumes, which cushions but doesn’t eliminate risk—multiple quarters below C$2.50/MMBtu would pressure distributable cash. Limited liquids (oil/NGLs <5% of 2024 production) means little offset if gas markets stay weak.

Significant Debt from Recent Acquisitions

Following the late-2025 acquisition of Repsol’s Canadian assets, Peyto carries roughly CAD 1.1 billion of debt on its balance sheet, raising net debt/EBITDA to about 3.2x; interest expense runs near CAD 65 million annually, which tightens near-term cash flow.

That scale boost improves reserves and production but the interest and principal schedule could constrain capex and leave less room for dividend support.

Management must prioritize reducing leverage—targeting sub-2.5x net debt/EBITDA within 18–24 months—while phasing growth projects to avoid forced dividend cuts.

Limited Exposure to Liquids and Oil

Peyto’s production remains heavily weighted to dry natural gas, with liquids making up under 15% of volumes in 2024 versus peer averages near 35%, reducing revenue per boe and EBITDA margins compared with condensate/light‑oil heavy producers.

This mix raises sensitivity to North American gas price swings—AECO fell 30% in 2024—and limits upside from oil price rallies that boosted peers’ cash flow in 2023–24.

- Liquids <15% of production (2024)

- Peer liquids ~35% avg (2024)

- AECO -30% in 2024

- Lower $/boe and EBITDA margin vs oil-rich peers

Dependence on Regional Pipeline Access

Peyto’s sales are tied to Alberta’s AECO hub, so pipeline outages or capacity tightness can cut realized gas prices; AECO averaged about C$2.50/GJ in 2024 versus Henry Hub US$2.80/MMBtu, amplifying differentials.

Third-party midstream constraints—e.g., 2024 pipeline maintenance that trimmed takeaway by ~5–10%—pose a recurring bottleneck and risk to cash flow and production scheduling.

- AECO exposure: price differentials hit margins

- 2024 takeaway cuts ~5–10% from maintenance

- Dependence on midstream adds operational risk

Peyto: Alberta‑heavy dry‑gas play — C$2.50 AECO, CAD1.1bn net debt, 3.2x ND/EBITDA

Peyto is highly concentrated in Alberta (≈85% 2024 prod; 90% proved reserves), mostly dry gas (<15% liquids), making cash flow very sensitive to AECO gas swings (AECO ~C$2.50/GJ 2024; Henry Hub US$2.80/MMBtu). Post-2025 Repsol deal net debt ≈CAD1.1bn (net debt/EBITDA ~3.2x); interest ≈CAD65m/yr; midstream constraints trimmed takeaway ~5–10% in 2024.

| Metric | Value |

|---|---|

| 2024 production concentration | ~85% |

| Liquids % (2024) | <15% |

| AECO (2024) | C$2.50/GJ |

| Net debt | CAD1.1bn |

| Net debt/EBITDA | ~3.2x |

Preview Before You Purchase

Peyto Exploration & Development SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and contains the same structured strengths, weaknesses, opportunities, and threats.