Power Finance PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our targeted PESTLE Analysis of Power Finance—highlighting regulatory, economic, and technological forces shaping the firm’s trajectory; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access a comprehensive, editable breakdown that speeds decision-making and reveals growth and risk opportunities.

Political factors

Government Infrastructure Mandates

The Revamped Distribution Sector Scheme (RDSS) through 2025 offers a clear roadmap for PFC’s lending, with central funding of up to INR 3.03 trillion allocated to DISCOM reforms; PFC, as a nodal agency, monitors and disburses these funds, enhancing state DISCOM operational efficiency and reducing AT&C losses (national average ~20% in FY2023); this alignment secures a steady pipeline of government-backed financing and mitigates credit risk for large-scale projects.

Maharatna Status Autonomy

PFC’s Maharatna status grants financial autonomy including enhanced powers for equity investments up to 15% of net worth and faster approvals for JV decisions, enabling deployment of large ticket funding—PFC reported total assets of Rs 6.2 lakh crore in FY2024 and can now commit larger sums without frequent ministerial clearance.

International Energy Alliances

Government engagement in global climate forums and bilateral energy pacts has helped Power Finance Corporation access low-cost international funding, including a $1.5bn green loan consortium in 2023 and concessional lines linked to COP28 commitments; India’s leadership in the International Solar Alliance expands PFC’s scope to finance cross-border solar projects, while diplomatic ties aided favorable terms from ADB, World Bank and foreign investors, reducing blended funding costs by an estimated 80–150 bps in 2024.

State-Level Policy Alignment

The success of PFCs lending portfolio hinges on state-level political stability and policy consistency across India; in FY2024 PFC reported 68% of its loans to state power utilities, exposing it to regional policy shifts.

Changes in government can alter PPAs or delay subsidies, contributing to aggregate outstanding dues of Rs 2.1 lakh crore to state utilities as of Mar 2025, raising recovery risk.

PFC must actively engage with state administrations and monitor political cycles to protect cash flows and project viability.

- 68% of loans to state utilities (FY2024)

- Outstanding state utility dues Rs 2.1 lakh crore (Mar 2025)

- Risk: PPA changes, subsidy delays, political turnover

Public Sector Divestment Trends

Government divestment policies affect PFC’s market valuation and capital structure; the Centre held 69.46% in PFC as of FY2024, and any accelerated privatization could lower sovereign support, raising funding costs and credit spreads.

Maintaining majority ownership preserves strategic control and credit comfort—PFC’s standalone AAA/Stable ratings by ICRA and CRISIL in 2024 reflect this—yet policy shifts toward privatization would increase perceived market risk.

Investors watch political signals closely: announced disinvestment targets (Rs 10 lakh crore+ for FY2024–25 across PSUs) and cabinet decisions can rapidly alter PFC’s risk-premium and share performance.

- Centre stake FY2024: 69.46%

- Disinvestment target FY2024–25: Rs 10 lakh crore+

- Credit ratings FY2024: AAA/Stable (ICRA, CRISIL)

PFC: Strong state-backed AAA credentials amid high utility exposure and privatization risk

PFC benefits from RDSS funding (INR 3.03 tn through 2025) and Maharatna powers (assets Rs 6.2 lakh crore FY2024) but remains exposed to state political risk—68% loans to utilities and Rs 2.1 lakh crore dues (Mar 2025); Centre stake 69.46% (FY2024) underpins AAA/Stable ratings, while disinvestment targets (Rs 10+ lakh crore FY2024–25) could raise funding costs if privatization accelerates.

| Metric | Value |

|---|---|

| RDSS funding | INR 3.03 tn |

| PFC assets (FY2024) | Rs 6.2 lakh crore |

| % loans to state utilities | 68% |

| Outstanding dues (Mar 2025) | Rs 2.1 lakh crore |

| Centre stake (FY2024) | 69.46% |

| Disinvestment target (FY2024–25) | Rs 10+ lakh crore |

| Ratings (FY2024) | AAA/Stable |

What is included in the product

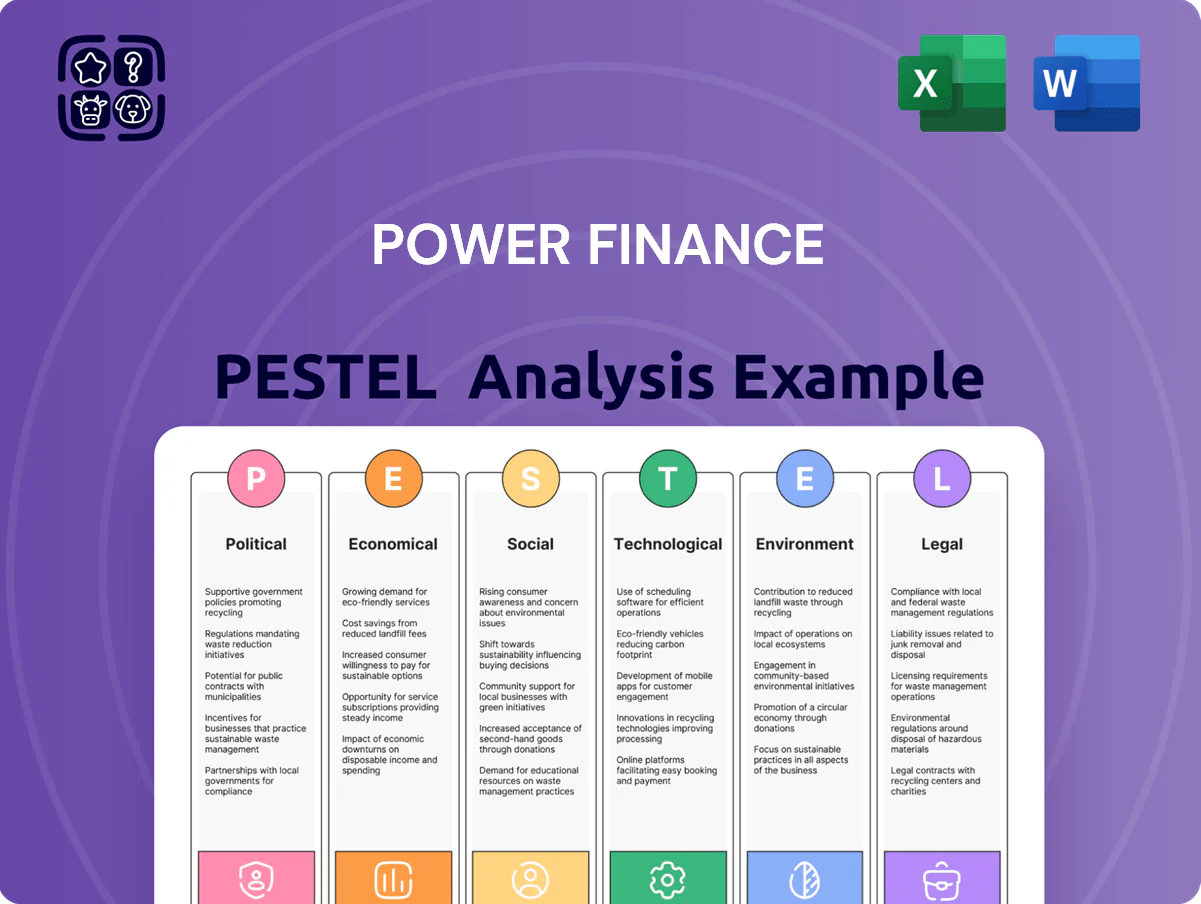

Explores how external macro-environmental factors uniquely affect Power Finance across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify sector-specific risks and opportunities.

A concise, visually segmented PESTLE summary tailored to Power Finance that simplifies external risk assessment for rapid inclusion in presentations or planning sessions, and is easily shareable and editable for team alignment.

Economic factors

Interest Rate Volatility

Fluctuations in the Reserve Bank of India’s policy rate — which stood at 6.50% in December 2025 after a cumulative 250 bps hiking cycle since 2022 — directly raise PFC’s borrowing costs and compress lending margins.

Maintaining a favorable net interest margin (PFC reported NIM of 1.9% in FY2024) requires sophisticated asset-liability management to offset monetary tightening and protect spread.

As a dominant issuer in domestic debt markets with outstanding borrowings over Rs 5.5 trillion (FY2024), PFC’s profitability remains tightly correlated to the prevailing interest rate environment as of late 2025.

Domestic GDP and Power Demand

India’s GDP growth forecast of ~6.5–7% for FY2025–26 supports rising electricity demand, with peak demand reaching ~230 GW in 2024 and total electricity consumption up ~7% YoY to ~1,600 TWh in 2024; this fuels large capex in generation and transmission where Power Finance Corporation (PFC)—which disbursed ~INR 1.1 lakh crore in FY2024—remains a primary financier. The tight GDP–energy elasticity ensures steady demand for PFC’s loans, bond underwriting, and credit-enhancement products.

Global Credit Ratings

PFC’s ability to raise capital at competitive rates is tied to its international credit ratings, which typically track India’s sovereign rating (India: BBB-/Baa3 as of 2025 consensus), affecting borrowing spreads and investor appetite.

National fiscal discipline and GDP growth (India GDP ~7.2% in 2024) bolster confidence in PFC’s debt, lowering yields demanded by global investors.

High ratings enable access to global bond markets; PFC issued dollar bonds in 2024, diversifying funding and reducing reliance on domestic liquidity.

Currency Exchange Risks

A significant portion of Power Finance Corporation’s resource mobilization—around 18% of FY2024 borrowings—comes from foreign currency loans, exposing PFC to INR/USD volatility that rose 9.5% during 2022–2023.

While hedging via forwards and swaps mitigates routine exposures, extreme INR depreciation (peak rate ~83.6/USD in 2023) can materially raise debt servicing costs and interest margins.

Ongoing global rate shifts and commodity-driven FX pressures require proactive Treasury strategies to preserve net income and maintain credit metrics.

- ~18% FY2024 foreign debt share

- INR/USD peaked ~83.6 in 2023

- 9.5% FX volatility (2022–23)

Inflationary Pressure on Projects

Rising inflation pushes up costs for steel, cement and wages in PFC-financed power projects; India’s WPI inflation averaged 4.9% in 2024, elevating capex estimates by 5–12% on recent projects.

Cost overruns compress borrower cashflows and can raise NPAs; thermal and renewable borrowers saw stressed DSCRs fall by 0.1–0.3x in 2023–24 under inflation shocks.

PFC should apply rigorous sensitivity tests—scenarios at 4%, 7% and 10% inflation—to stress-test tariffs, DSCR and loan tenor adjustments.

- Inflation (WPI 2024): 4.9%

- Estimated capex rise: 5–12%

- DSCR hit in stress: −0.1 to −0.3x

- Recommended stress scenarios: 4%, 7%, 10%

PFC margins under pressure: rising rates, FX exposure and higher capex strain profits

Interest-rate hikes (RBI policy 6.50% Dec 2025) raise PFC borrowing costs and compress NIM (1.9% FY2024); outstanding debt >Rs 5.5tn (FY2024) ties profitability to rates. GDP ~6.5–7% FY2025–26 and 7.2% (2024) boost electricity demand and lending; FX exposure (~18% foreign debt) and INR/USD volatility (peak 83.6 in 2023) raise hedging needs; WPI 4.9% (2024) lifts capex 5–12%, stressing DSCR.

| Metric | Value |

|---|---|

| RBI rate Dec 2025 | 6.50% |

| NIM FY2024 | 1.9% |

| Outstanding debt FY2024 | Rs 5.5tn+ |

| Foreign debt share | ~18% |

| INR/USD peak | 83.6 (2023) |

| WPI 2024 | 4.9% |

Preview Before You Purchase

Power Finance PESTLE Analysis

The preview shown here is the exact Power Finance PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in the preview are identical to the downloadable file you’ll get immediately after checkout, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our targeted PESTLE Analysis of Power Finance—highlighting regulatory, economic, and technological forces shaping the firm’s trajectory; ideal for investors and strategists seeking actionable foresight. Purchase the full report to access a comprehensive, editable breakdown that speeds decision-making and reveals growth and risk opportunities.

Political factors

Government Infrastructure Mandates

The Revamped Distribution Sector Scheme (RDSS) through 2025 offers a clear roadmap for PFC’s lending, with central funding of up to INR 3.03 trillion allocated to DISCOM reforms; PFC, as a nodal agency, monitors and disburses these funds, enhancing state DISCOM operational efficiency and reducing AT&C losses (national average ~20% in FY2023); this alignment secures a steady pipeline of government-backed financing and mitigates credit risk for large-scale projects.

Maharatna Status Autonomy

PFC’s Maharatna status grants financial autonomy including enhanced powers for equity investments up to 15% of net worth and faster approvals for JV decisions, enabling deployment of large ticket funding—PFC reported total assets of Rs 6.2 lakh crore in FY2024 and can now commit larger sums without frequent ministerial clearance.

International Energy Alliances

Government engagement in global climate forums and bilateral energy pacts has helped Power Finance Corporation access low-cost international funding, including a $1.5bn green loan consortium in 2023 and concessional lines linked to COP28 commitments; India’s leadership in the International Solar Alliance expands PFC’s scope to finance cross-border solar projects, while diplomatic ties aided favorable terms from ADB, World Bank and foreign investors, reducing blended funding costs by an estimated 80–150 bps in 2024.

State-Level Policy Alignment

The success of PFCs lending portfolio hinges on state-level political stability and policy consistency across India; in FY2024 PFC reported 68% of its loans to state power utilities, exposing it to regional policy shifts.

Changes in government can alter PPAs or delay subsidies, contributing to aggregate outstanding dues of Rs 2.1 lakh crore to state utilities as of Mar 2025, raising recovery risk.

PFC must actively engage with state administrations and monitor political cycles to protect cash flows and project viability.

- 68% of loans to state utilities (FY2024)

- Outstanding state utility dues Rs 2.1 lakh crore (Mar 2025)

- Risk: PPA changes, subsidy delays, political turnover

Public Sector Divestment Trends

Government divestment policies affect PFC’s market valuation and capital structure; the Centre held 69.46% in PFC as of FY2024, and any accelerated privatization could lower sovereign support, raising funding costs and credit spreads.

Maintaining majority ownership preserves strategic control and credit comfort—PFC’s standalone AAA/Stable ratings by ICRA and CRISIL in 2024 reflect this—yet policy shifts toward privatization would increase perceived market risk.

Investors watch political signals closely: announced disinvestment targets (Rs 10 lakh crore+ for FY2024–25 across PSUs) and cabinet decisions can rapidly alter PFC’s risk-premium and share performance.

- Centre stake FY2024: 69.46%

- Disinvestment target FY2024–25: Rs 10 lakh crore+

- Credit ratings FY2024: AAA/Stable (ICRA, CRISIL)

PFC: Strong state-backed AAA credentials amid high utility exposure and privatization risk

PFC benefits from RDSS funding (INR 3.03 tn through 2025) and Maharatna powers (assets Rs 6.2 lakh crore FY2024) but remains exposed to state political risk—68% loans to utilities and Rs 2.1 lakh crore dues (Mar 2025); Centre stake 69.46% (FY2024) underpins AAA/Stable ratings, while disinvestment targets (Rs 10+ lakh crore FY2024–25) could raise funding costs if privatization accelerates.

| Metric | Value |

|---|---|

| RDSS funding | INR 3.03 tn |

| PFC assets (FY2024) | Rs 6.2 lakh crore |

| % loans to state utilities | 68% |

| Outstanding dues (Mar 2025) | Rs 2.1 lakh crore |

| Centre stake (FY2024) | 69.46% |

| Disinvestment target (FY2024–25) | Rs 10+ lakh crore |

| Ratings (FY2024) | AAA/Stable |

What is included in the product

Explores how external macro-environmental factors uniquely affect Power Finance across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify sector-specific risks and opportunities.

A concise, visually segmented PESTLE summary tailored to Power Finance that simplifies external risk assessment for rapid inclusion in presentations or planning sessions, and is easily shareable and editable for team alignment.

Economic factors

Interest Rate Volatility

Fluctuations in the Reserve Bank of India’s policy rate — which stood at 6.50% in December 2025 after a cumulative 250 bps hiking cycle since 2022 — directly raise PFC’s borrowing costs and compress lending margins.

Maintaining a favorable net interest margin (PFC reported NIM of 1.9% in FY2024) requires sophisticated asset-liability management to offset monetary tightening and protect spread.

As a dominant issuer in domestic debt markets with outstanding borrowings over Rs 5.5 trillion (FY2024), PFC’s profitability remains tightly correlated to the prevailing interest rate environment as of late 2025.

Domestic GDP and Power Demand

India’s GDP growth forecast of ~6.5–7% for FY2025–26 supports rising electricity demand, with peak demand reaching ~230 GW in 2024 and total electricity consumption up ~7% YoY to ~1,600 TWh in 2024; this fuels large capex in generation and transmission where Power Finance Corporation (PFC)—which disbursed ~INR 1.1 lakh crore in FY2024—remains a primary financier. The tight GDP–energy elasticity ensures steady demand for PFC’s loans, bond underwriting, and credit-enhancement products.

Global Credit Ratings

PFC’s ability to raise capital at competitive rates is tied to its international credit ratings, which typically track India’s sovereign rating (India: BBB-/Baa3 as of 2025 consensus), affecting borrowing spreads and investor appetite.

National fiscal discipline and GDP growth (India GDP ~7.2% in 2024) bolster confidence in PFC’s debt, lowering yields demanded by global investors.

High ratings enable access to global bond markets; PFC issued dollar bonds in 2024, diversifying funding and reducing reliance on domestic liquidity.

Currency Exchange Risks

A significant portion of Power Finance Corporation’s resource mobilization—around 18% of FY2024 borrowings—comes from foreign currency loans, exposing PFC to INR/USD volatility that rose 9.5% during 2022–2023.

While hedging via forwards and swaps mitigates routine exposures, extreme INR depreciation (peak rate ~83.6/USD in 2023) can materially raise debt servicing costs and interest margins.

Ongoing global rate shifts and commodity-driven FX pressures require proactive Treasury strategies to preserve net income and maintain credit metrics.

- ~18% FY2024 foreign debt share

- INR/USD peaked ~83.6 in 2023

- 9.5% FX volatility (2022–23)

Inflationary Pressure on Projects

Rising inflation pushes up costs for steel, cement and wages in PFC-financed power projects; India’s WPI inflation averaged 4.9% in 2024, elevating capex estimates by 5–12% on recent projects.

Cost overruns compress borrower cashflows and can raise NPAs; thermal and renewable borrowers saw stressed DSCRs fall by 0.1–0.3x in 2023–24 under inflation shocks.

PFC should apply rigorous sensitivity tests—scenarios at 4%, 7% and 10% inflation—to stress-test tariffs, DSCR and loan tenor adjustments.

- Inflation (WPI 2024): 4.9%

- Estimated capex rise: 5–12%

- DSCR hit in stress: −0.1 to −0.3x

- Recommended stress scenarios: 4%, 7%, 10%

PFC margins under pressure: rising rates, FX exposure and higher capex strain profits

Interest-rate hikes (RBI policy 6.50% Dec 2025) raise PFC borrowing costs and compress NIM (1.9% FY2024); outstanding debt >Rs 5.5tn (FY2024) ties profitability to rates. GDP ~6.5–7% FY2025–26 and 7.2% (2024) boost electricity demand and lending; FX exposure (~18% foreign debt) and INR/USD volatility (peak 83.6 in 2023) raise hedging needs; WPI 4.9% (2024) lifts capex 5–12%, stressing DSCR.

| Metric | Value |

|---|---|

| RBI rate Dec 2025 | 6.50% |

| NIM FY2024 | 1.9% |

| Outstanding debt FY2024 | Rs 5.5tn+ |

| Foreign debt share | ~18% |

| INR/USD peak | 83.6 (2023) |

| WPI 2024 | 4.9% |

Preview Before You Purchase

Power Finance PESTLE Analysis

The preview shown here is the exact Power Finance PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in the preview are identical to the downloadable file you’ll get immediately after checkout, with no placeholders or surprises.