Phoenix Holdings Boston Consulting Group Matrix

Actionable Strategy Starts Here

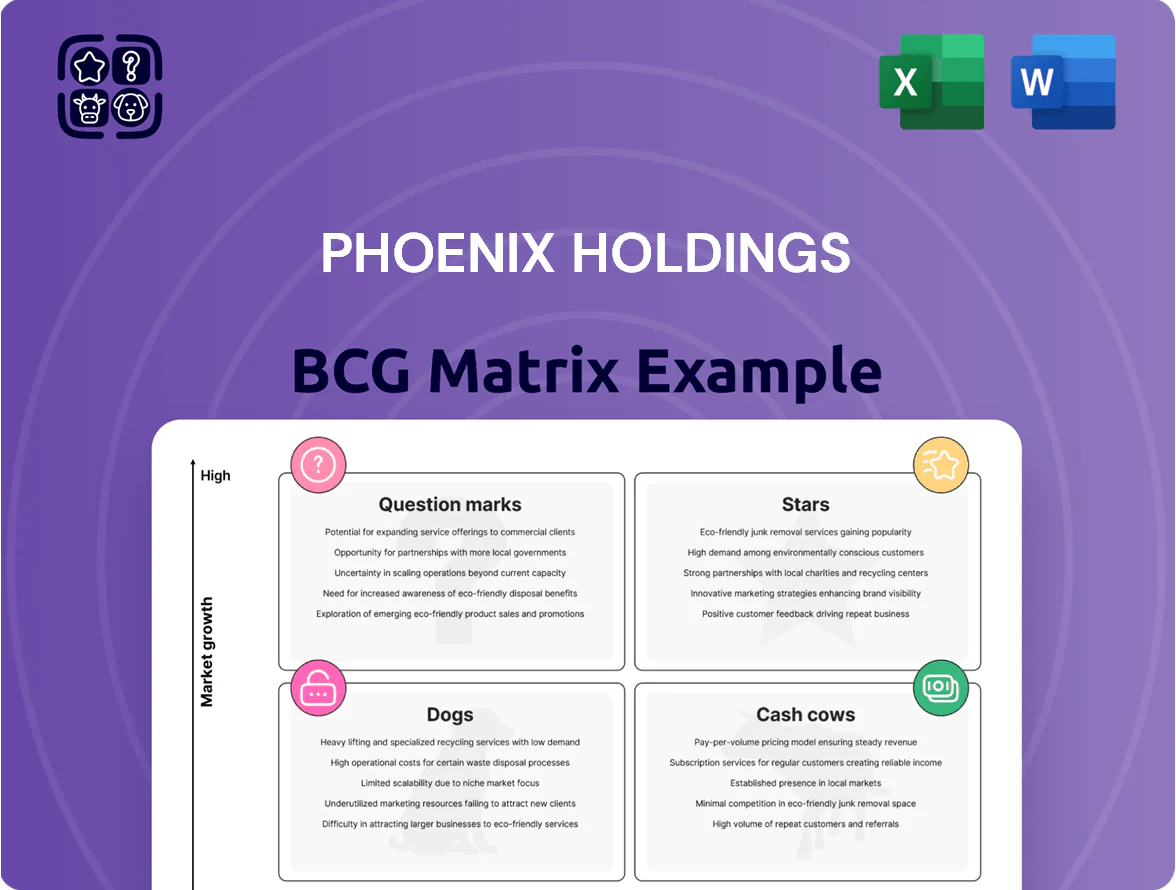

Phoenix Holdings sits at a pivotal crossroads—some business lines show strong market share in growing segments while others lag amid stiff competition, signaling clear priorities for reinvestment or divestment. This snapshot highlights strategic tensions and opportunities but is only a preview of our quadrant-level analysis and actionable recommendations. Purchase the full BCG Matrix to receive a complete Word report and Excel summary with data-backed placements, tailored strategic moves, and ready-to-present visuals to guide your next investment or portfolio decision.

Stars

Health and Long-Term Care Insurance

Phoenix Holdings dominates Israel’s health and long-term care market, holding about 38% market share in private health insurance and seeing segment premiums grow ~11% CAGR 2020–2024 to NIS 2.1 billion; aging demographics and rising out-of-pocket medical spend drive continued expansion.

The unit needs heavy upfront capital for customer acquisition—marketing and distribution capex ~NIS 220m in 2024—but returns high top-line growth, delivering ~18% revenue growth in 2024 as market leader.

By end-2025 Phoenix integrated digital health platforms and personalized underwriting (AI risk models), cutting claims leakage 6 percentage points and raising persistency to 82%, widening its lead over traditional rivals.

Alternative Investment Management

Phoenix Holdings’ Alternative Investment Management has doubled assets under management to $24.6bn by 2025, driven by aggressive expansion into private equity, infrastructure, and credit funds that captured strong search-for-yield flows.

Institutional and private investors shifted away from volatile public markets in 2023–25, helping Phoenix’s specialized vehicles grow market share to an estimated 6.2% in regional alternatives.

These units consume cash for deal sourcing and platform scaling—capex and carry funded ~$420m in 2024—but are positioned as the future high-margin core, targeting 18–22% EBITDA margins as scale matures.

Digital Insurance and Fintech Ventures

Phoenix Holdings’ Digital Insurance and Fintech Ventures (Phoenix Smart) targets Israel’s under-45, tech-savvy cohort, securing roughly 28% of new online policy sales in 2024 and growing at ~22% CAGR since 2021.

Market shifts show direct, mobile-first insurance uptake rising to 41% of retail premium flows in 2024, pressuring traditional agents and positioning this segment as a BCG Stars unit.

Phoenix’s continued investment—≈ILS 120m in AI and automation through 2023–24—remains essential to defend share versus insurtech entrants and sustain 15–20% margin improvements from process automation.

Corporate and Commercial P&C Insurance

Phoenix leads Israel’s corporate P&C market, underwriting complex cyber, liability, and property risks for tech and industry; in 2025 commercial premiums rose ~8% YoY to NIS 3.1bn, driven by cyber demand up ~22%.

The firm’s capacity and syndicate leadership closed 18 large deals in 2025 exceeding NIS 150m each, making Phoenix the preferred partner for high-limit corporate placements.

- 2025 commercial premiums NIS 3.1bn

- cyber premium growth ~22% YoY

- 18 deals > NIS 150m in 2025

- strong syndicate leadership and high capacity

Wealth Management for High Net Worth Individuals

Phoenix Excellence wealth management has captured roughly 22% of Israel’s HNW segment, helping Phoenix Holdings lead the private-wealth market while AUM rose 18% year-over-year to ₪48.6 billion in 2025; the unit shows star characteristics: strong market share and rapid AUM growth but high cash burn for talent and bespoke product development.

- Market share ~22% (HNW Israel, 2025)

- AUM +18% YoY to ₪48.6B (2025)

- High cash consumption: increased advisory hiring, tech, bespoke products

- Leader status: scale enables product pricing power

Phoenix’s Growth Engines: Health, Alternatives, Digital, P&C & Wealth Power 2025

Phoenix’s Stars: Health & LTC (38% share; premiums NIS 2.1bn; 11% CAGR 2020–24), Alternative Investments (AUM $24.6bn, 6.2% alt. market share, targeting 18–22% EBITDA), Digital/Fintech (28% online sales, 22% CAGR since 2021), Corporate P&C (NIS 3.1bn premiums 2025; cyber +22%), Wealth (22% HNW share; AUM ₪48.6bn; +18% YoY).

| Unit | Key metric 2025 | Growth/notes |

|---|---|---|

| Health | NIS 2.1bn; 38% share | 11% CAGR 2020–24 |

| Alternatives | $24.6bn AUM | 6.2% share; 18–22% target EBITDA |

| Digital | 28% online sales | 22% CAGR |

| Corp P&C | NIS 3.1bn | cyber +22% |

| Wealth | ₪48.6bn AUM; 22% HNW | +18% YoY |

What is included in the product

Concise BCG Matrix review of Phoenix Holdings’ units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Phoenix Holdings unit in a quadrant for rapid portfolio prioritization and executive decisions.

Cash Cows

Pension and Provident Fund Management

Phoenix Holdings’ Pension and Provident Fund Management is a cash cow: it oversees about NIS 120 billion in assets under management (2025), generating stable management fees with low incremental operating costs and ~15% EBITDA margin contribution. Israel’s mandatory pension contributions (approx. 7%–18% of wages) ensure steady net inflows of ~NIS 6–8 billion annually, reducing marketing spend. These funds finance Phoenix’s growth initiatives and support dividends, with payouts of ~NIS 450 million in 2024.

Legacy Life Insurance Portfolios

Legacy life insurance portfolios—mainly fixed-premium, multi-decade policies—deliver steady, predictable cash flow, contributing about 28% of Phoenix Holdings’ operating cash in FY2024 (₤420m of ₤1.5bn total operating cash).

Given low market growth, Phoenix prioritizes cost-to-serve cuts and a 92% retention rate over new sales, preserving margins while reducing lapse-related reserve volatility.

Cash from these books funded 65% of 2024 corporate debt service and seeded a ₤120m digital transformation fund launched in Q1 2025.

Excellence Investment House Brokerage

Excellence Investment House Brokerage, one of Israel’s oldest brokers, holds a leading market share of about 18% in retail equity trading as of 2025, operating in a mature market where annual volume growth is under 2%.

Despite slowing retail brokerage growth, its transaction volumes generated NIS 420 million in fee revenue in 2024, providing steady cash flow.

The unit needs low capital expenditure—operating margin near 28% in 2024—so it requires minimal reinvestment versus digital segments.

As a cash cow, it supplies predictable liquidity to Phoenix Holdings, funding growth areas and dividends without stressing the balance sheet.

Standard Motor and Home Insurance

Standard Motor and Home Insurance are cash cows in Phoenix Holdings’ BCG matrix: the UK retail property & casualty (P&C) auto and home market grew ~1% in 2024 with combined market share leaders holding ~45% of premiums; Phoenix retains a top-three position via strong brand loyalty and a 30%+ combined operating margin driven by efficient claims processing.

They need moderate maintenance marketing—renewal campaigns and digital servicing—costing ~3–4% of written premiums, yet generate steady free cash flow that funds group R&D and newer growth bets.

- Market growth ~1% (2024)

- Phoenix top-three share; leaders ~45% of premiums

- Combined operating margin >30%

- Marketing spend ~3–4% of premiums

- Primary cash source for group innovation

Real Estate Yield-Bearing Assets

Phoenix Holdings owns income-producing real estate—about NIS 4.2 billion (2025 book value) across office and retail centers in Israel, generating ~NIS 260 million annual net rental income and a 6.2% yield, anchoring steady cash flow in a mature market with low new-supply volatility.

These holdings deliver largely passive cash flow, fund solvency buffers, and offer modest capital appreciation tied to Israel’s urban leasing demand and constrained development pipeline.

- Portfolio value: NIS 4.2 billion (2025)

- Annual net rental income: ~NIS 260 million

- Net yield: ~6.2% (2025)

- Role: Passive cash flow supporting solvency

Phoenix’s cash cows: strong pension AUM, high margins, steady cash funding growth

Phoenix’s cash cows (Pension AUM NIS 120bn, legacy life, brokerage, UK P&C, real estate NIS 4.2bn) generate steady free cash: ~NIS 6–8bn pension inflows, ~15% EBITDA from pension ops, NIS 420m brokerage fees (2024), >30% combined P&C margin, NIS 260m rental income (6.2% yield) — funding dividends, 65% of 2024 debt service, and a ₤120m 2025 digital fund.

| Unit | Key 2024–25 metrics |

|---|---|

| Pension & Provident | AUM NIS 120bn; inflows NIS 6–8bn; ~15% EBITDA |

| Legacy life | 28% operating cash (FY2024) |

| Brokerage | 18% share; NIS 420m fees; 28% margin |

| UK P&C | ~30%+ margin; market growth ~1% |

| Real estate | Value NIS 4.2bn; income NIS 260m; yield 6.2% |

What You’re Viewing Is Included

Phoenix Holdings BCG Matrix

The file you're previewing is the exact Phoenix Holdings BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted for immediate use in presentations, strategy sessions, or client deliverables.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Phoenix Holdings sits at a pivotal crossroads—some business lines show strong market share in growing segments while others lag amid stiff competition, signaling clear priorities for reinvestment or divestment. This snapshot highlights strategic tensions and opportunities but is only a preview of our quadrant-level analysis and actionable recommendations. Purchase the full BCG Matrix to receive a complete Word report and Excel summary with data-backed placements, tailored strategic moves, and ready-to-present visuals to guide your next investment or portfolio decision.

Stars

Health and Long-Term Care Insurance

Phoenix Holdings dominates Israel’s health and long-term care market, holding about 38% market share in private health insurance and seeing segment premiums grow ~11% CAGR 2020–2024 to NIS 2.1 billion; aging demographics and rising out-of-pocket medical spend drive continued expansion.

The unit needs heavy upfront capital for customer acquisition—marketing and distribution capex ~NIS 220m in 2024—but returns high top-line growth, delivering ~18% revenue growth in 2024 as market leader.

By end-2025 Phoenix integrated digital health platforms and personalized underwriting (AI risk models), cutting claims leakage 6 percentage points and raising persistency to 82%, widening its lead over traditional rivals.

Alternative Investment Management

Phoenix Holdings’ Alternative Investment Management has doubled assets under management to $24.6bn by 2025, driven by aggressive expansion into private equity, infrastructure, and credit funds that captured strong search-for-yield flows.

Institutional and private investors shifted away from volatile public markets in 2023–25, helping Phoenix’s specialized vehicles grow market share to an estimated 6.2% in regional alternatives.

These units consume cash for deal sourcing and platform scaling—capex and carry funded ~$420m in 2024—but are positioned as the future high-margin core, targeting 18–22% EBITDA margins as scale matures.

Digital Insurance and Fintech Ventures

Phoenix Holdings’ Digital Insurance and Fintech Ventures (Phoenix Smart) targets Israel’s under-45, tech-savvy cohort, securing roughly 28% of new online policy sales in 2024 and growing at ~22% CAGR since 2021.

Market shifts show direct, mobile-first insurance uptake rising to 41% of retail premium flows in 2024, pressuring traditional agents and positioning this segment as a BCG Stars unit.

Phoenix’s continued investment—≈ILS 120m in AI and automation through 2023–24—remains essential to defend share versus insurtech entrants and sustain 15–20% margin improvements from process automation.

Corporate and Commercial P&C Insurance

Phoenix leads Israel’s corporate P&C market, underwriting complex cyber, liability, and property risks for tech and industry; in 2025 commercial premiums rose ~8% YoY to NIS 3.1bn, driven by cyber demand up ~22%.

The firm’s capacity and syndicate leadership closed 18 large deals in 2025 exceeding NIS 150m each, making Phoenix the preferred partner for high-limit corporate placements.

- 2025 commercial premiums NIS 3.1bn

- cyber premium growth ~22% YoY

- 18 deals > NIS 150m in 2025

- strong syndicate leadership and high capacity

Wealth Management for High Net Worth Individuals

Phoenix Excellence wealth management has captured roughly 22% of Israel’s HNW segment, helping Phoenix Holdings lead the private-wealth market while AUM rose 18% year-over-year to ₪48.6 billion in 2025; the unit shows star characteristics: strong market share and rapid AUM growth but high cash burn for talent and bespoke product development.

- Market share ~22% (HNW Israel, 2025)

- AUM +18% YoY to ₪48.6B (2025)

- High cash consumption: increased advisory hiring, tech, bespoke products

- Leader status: scale enables product pricing power

Phoenix’s Growth Engines: Health, Alternatives, Digital, P&C & Wealth Power 2025

Phoenix’s Stars: Health & LTC (38% share; premiums NIS 2.1bn; 11% CAGR 2020–24), Alternative Investments (AUM $24.6bn, 6.2% alt. market share, targeting 18–22% EBITDA), Digital/Fintech (28% online sales, 22% CAGR since 2021), Corporate P&C (NIS 3.1bn premiums 2025; cyber +22%), Wealth (22% HNW share; AUM ₪48.6bn; +18% YoY).

| Unit | Key metric 2025 | Growth/notes |

|---|---|---|

| Health | NIS 2.1bn; 38% share | 11% CAGR 2020–24 |

| Alternatives | $24.6bn AUM | 6.2% share; 18–22% target EBITDA |

| Digital | 28% online sales | 22% CAGR |

| Corp P&C | NIS 3.1bn | cyber +22% |

| Wealth | ₪48.6bn AUM; 22% HNW | +18% YoY |

What is included in the product

Concise BCG Matrix review of Phoenix Holdings’ units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Phoenix Holdings unit in a quadrant for rapid portfolio prioritization and executive decisions.

Cash Cows

Pension and Provident Fund Management

Phoenix Holdings’ Pension and Provident Fund Management is a cash cow: it oversees about NIS 120 billion in assets under management (2025), generating stable management fees with low incremental operating costs and ~15% EBITDA margin contribution. Israel’s mandatory pension contributions (approx. 7%–18% of wages) ensure steady net inflows of ~NIS 6–8 billion annually, reducing marketing spend. These funds finance Phoenix’s growth initiatives and support dividends, with payouts of ~NIS 450 million in 2024.

Legacy Life Insurance Portfolios

Legacy life insurance portfolios—mainly fixed-premium, multi-decade policies—deliver steady, predictable cash flow, contributing about 28% of Phoenix Holdings’ operating cash in FY2024 (₤420m of ₤1.5bn total operating cash).

Given low market growth, Phoenix prioritizes cost-to-serve cuts and a 92% retention rate over new sales, preserving margins while reducing lapse-related reserve volatility.

Cash from these books funded 65% of 2024 corporate debt service and seeded a ₤120m digital transformation fund launched in Q1 2025.

Excellence Investment House Brokerage

Excellence Investment House Brokerage, one of Israel’s oldest brokers, holds a leading market share of about 18% in retail equity trading as of 2025, operating in a mature market where annual volume growth is under 2%.

Despite slowing retail brokerage growth, its transaction volumes generated NIS 420 million in fee revenue in 2024, providing steady cash flow.

The unit needs low capital expenditure—operating margin near 28% in 2024—so it requires minimal reinvestment versus digital segments.

As a cash cow, it supplies predictable liquidity to Phoenix Holdings, funding growth areas and dividends without stressing the balance sheet.

Standard Motor and Home Insurance

Standard Motor and Home Insurance are cash cows in Phoenix Holdings’ BCG matrix: the UK retail property & casualty (P&C) auto and home market grew ~1% in 2024 with combined market share leaders holding ~45% of premiums; Phoenix retains a top-three position via strong brand loyalty and a 30%+ combined operating margin driven by efficient claims processing.

They need moderate maintenance marketing—renewal campaigns and digital servicing—costing ~3–4% of written premiums, yet generate steady free cash flow that funds group R&D and newer growth bets.

- Market growth ~1% (2024)

- Phoenix top-three share; leaders ~45% of premiums

- Combined operating margin >30%

- Marketing spend ~3–4% of premiums

- Primary cash source for group innovation

Real Estate Yield-Bearing Assets

Phoenix Holdings owns income-producing real estate—about NIS 4.2 billion (2025 book value) across office and retail centers in Israel, generating ~NIS 260 million annual net rental income and a 6.2% yield, anchoring steady cash flow in a mature market with low new-supply volatility.

These holdings deliver largely passive cash flow, fund solvency buffers, and offer modest capital appreciation tied to Israel’s urban leasing demand and constrained development pipeline.

- Portfolio value: NIS 4.2 billion (2025)

- Annual net rental income: ~NIS 260 million

- Net yield: ~6.2% (2025)

- Role: Passive cash flow supporting solvency

Phoenix’s cash cows: strong pension AUM, high margins, steady cash funding growth

Phoenix’s cash cows (Pension AUM NIS 120bn, legacy life, brokerage, UK P&C, real estate NIS 4.2bn) generate steady free cash: ~NIS 6–8bn pension inflows, ~15% EBITDA from pension ops, NIS 420m brokerage fees (2024), >30% combined P&C margin, NIS 260m rental income (6.2% yield) — funding dividends, 65% of 2024 debt service, and a ₤120m 2025 digital fund.

| Unit | Key 2024–25 metrics |

|---|---|

| Pension & Provident | AUM NIS 120bn; inflows NIS 6–8bn; ~15% EBITDA |

| Legacy life | 28% operating cash (FY2024) |

| Brokerage | 18% share; NIS 420m fees; 28% margin |

| UK P&C | ~30%+ margin; market growth ~1% |

| Real estate | Value NIS 4.2bn; income NIS 260m; yield 6.2% |

What You’re Viewing Is Included

Phoenix Holdings BCG Matrix

The file you're previewing is the exact Phoenix Holdings BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted for immediate use in presentations, strategy sessions, or client deliverables.