Phoenix Contact GmbH & Co. KG PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate regulatory shifts, supply-chain pressures, and rapid tech innovation with our targeted PESTLE Analysis of Phoenix Contact GmbH & Co. KG—concise, actionable insights reveal risks and growth levers to sharpen your strategy. Purchase the full report for a complete breakdown, editable templates, and data-driven recommendations to inform investment or strategic decisions immediately.

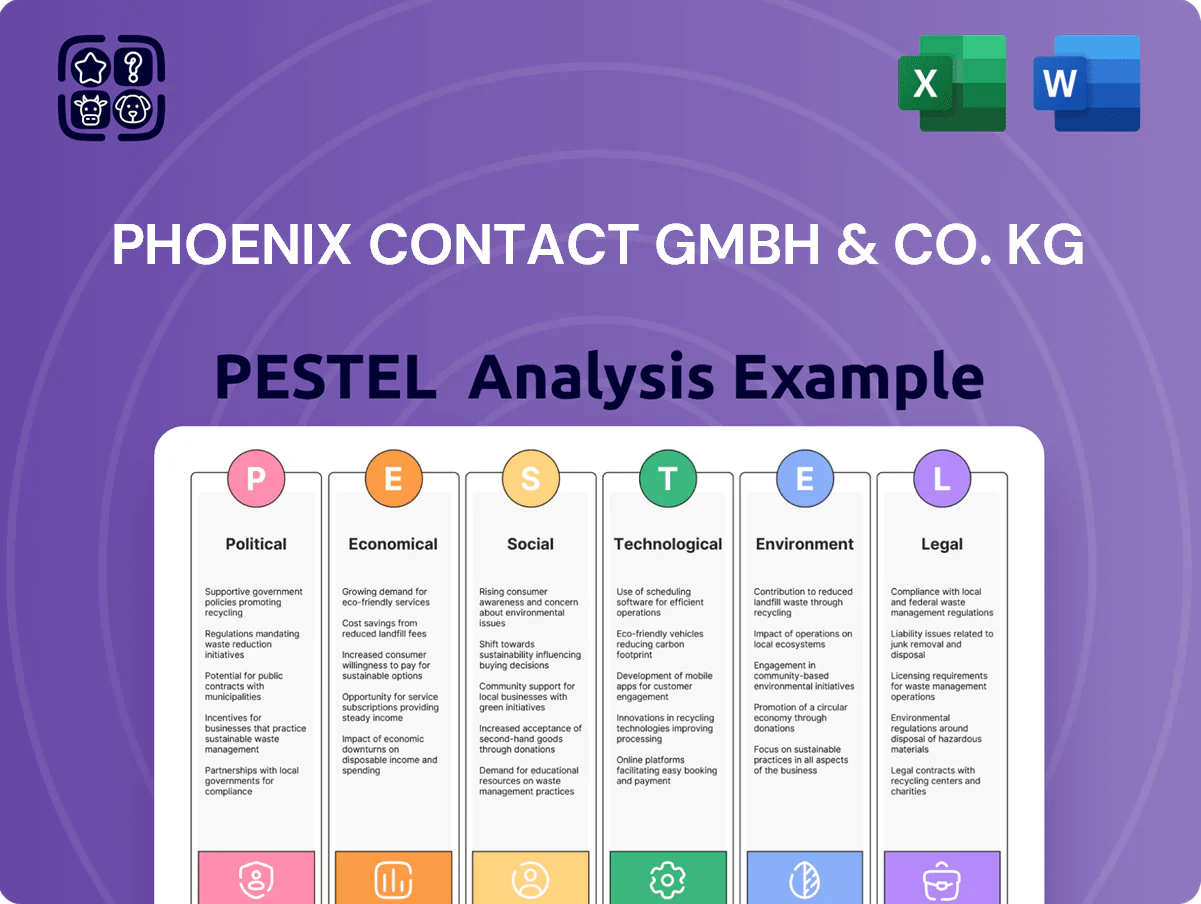

Political factors

Geopolitical instability and trade regionalization

Phoenix Contact must navigate rising geopolitical tensions that drive trade regionalization and localized production mandates; by late 2025 the company reported reallocating roughly 18% of manufacturing capacity to regional hubs, balancing a €2.7bn global revenue base with increased local investments to reduce tariff exposure. This dual footprint protects market access across Western and emerging markets and mitigates sudden political shocks to supply chains.

Governmental support for the All Electric Society

Global political agendas favoring an All Electric Society boost Phoenix Contact's market: the IEA reports electrification must deliver ~40% of emissions reductions to 2050, aligning with the firm's interconnection and automation offerings.

National subsidies — e.g., EU recovery and REPowerEU €300bn+ clean energy investments through 2024–27 — drive demand for Phoenix Contact's components and systems.

Commitments to carbon neutrality by 2050 from 125+ countries create a predictable regulatory horizon, supporting long-term capital allocation into electrification technologies and steady revenue visibility for Phoenix Contact.

Supply chain resilience and sovereignty policies

European and US sovereignty initiatives, including the European Chips Act allocating €43bn and US CHIPS Act $280bn (2022–25 funding frameworks), push Phoenix Contact to reshuffle sourcing of critical semiconductors and connectors to reduce exposure to Asia-Pacific supply shocks.

These policies incentivize onshoring and nearshoring, prompting the company to diversify suppliers and invest in local resilience—evidenced by rising supplier qualification spending and regional inventory increases reported across the automation sector in 2024.

Mandates aimed at cutting reliance on volatile regions seek continuity of industrial automation services, directly impacting Phoenix Contact’s procurement strategies, capital allocation for supplier redundancy, and expected lead-time reductions trending in 2024 procurement data.

Export control and technology restrictions

Stricter export controls on high-tech dual-use goods challenge Phoenix Contact’s distribution of advanced control systems and encryption, with EU dual-use regulation updates in 2023 expanding scope and the US adding ~1,500 entities to restrictions in 2024.

The company must maintain rigorous compliance frameworks—legal, IT, and trade controls—to navigate expanding restricted-entity lists and sanctioned jurisdictions, protecting revenues (2024 group sales €2.8bn) and market access.

Non-compliance risks include substantial fines and loss of export licenses; recent EU fines for export breaches have exceeded €50m in cases across 2022–2024, underscoring financial exposure.

- Expanded 2023 EU dual-use scope + ~1,500 US restricted entities (2024)

- 2024 Phoenix Contact sales €2.8bn at stake

- Regulatory fines in similar cases >€50m (2022–2024)

Investment in public infrastructure and smart cities

- EU/national infrastructure funds >€200bn (2024–25)

- Germany climate/transform plan €86bn

- Public projects ~10–15% of Phoenix Contact 2024 revenue

Phoenix Contact: €2.8bn sales, geopolitics force 18% regionalization amid electrification boom

Phoenix Contact faces geopolitical-driven regionalization (≈18% capacity regionalized by 2025) and trade controls while benefiting from electrification/subsidy tailwinds (EU REPowerEU €300bn+, public infrastructure €200bn+ 2024–25); 2024 sales €2.8bn with ~10–15% public-project exposure; export-control risks: recent fines >€50m and ~1,500 US restricted entities (2024).

| Metric | Value |

|---|---|

| 2024 Sales | €2.8bn |

| Regionalized Capacity (2025) | ≈18% |

| Public Projects Exposure (2024) | 10–15% |

| EU REPowerEU (2024–27) | €300bn+ |

| Infrastructure Funds (2024–25) | €200bn+ |

| US Restricted Entities (2024) | ≈1,500 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Phoenix Contact GmbH & Co. KG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify strategic threats and opportunities for executives and investors.

A concise PESTLE summary tailored for Phoenix Contact GmbH & Co. KG that highlights regulatory, economic, technological, social, and environmental pressures and opportunities—ready to drop into presentations or share across teams to streamline risk discussions and strategic planning.

Economic factors

Impact of global interest rates on capital expenditure

As of late 2025, global policy rates averaging around 4.5–5.0% in major economies have tightened industrial customers' financing costs, prompting delays in CAPEX for automation and plant upgrades and weighing on Phoenix Contact's near-term order intake.

When rates stabilize—as markets projected by ECB and Fed futures for 2026—renewed corporate investment into efficiency and automation is expected to boost demand for Phoenix Contact's control and connectivity solutions.

Rising labor costs driving automation demand

Persistent labor shortages and rising wages in OECD countries—average annual compensation up 4.2% in 2024—accelerate demand for Phoenix Contact automation, as 56% of European manufacturers report skills gaps in 2024; firms invest in labor-saving systems to protect margins amid record unit labor cost growth. The shift repositions Phoenix Contact from component supplier to provider of integrated productivity solutions, reflected in a 2023–24 uptick in industrial automation orders.

Volatility in raw material and energy prices

Fluctuations in copper, plastics and energy prices materially affect Phoenix Contact's manufacturing costs across ~20,000 products; copper rose ~35% in 2021–2023 and European power prices spiked to averages >€200/MWh in 2022, squeezing margins.

Phoenix Contact uses hedging, long‑term supplier contracts and dynamic price‑adjustment clauses—procurement saved an estimated 4–6% cost volatility in 2023 per industry disclosures.

Stability in European energy markets is critical: energy intensity of electronics manufacturing means prolonged high prices could raise COGS by several percentage points and weaken competitive pricing.

Currency exchange rate fluctuations

As a Eurozone-headquartered global industrial electronics supplier, Phoenix Contact faces currency exposure to USD and CNY movements; a 10% EUR appreciation versus USD would reduce export competitiveness and trimmed 2024 reported revenues by an estimated mid-single-digit percent based on 2023 FX sensitivity disclosures.

The firm uses forward contracts and currency swaps alongside local-for-local production—about 40% of manufacturing footprint outside Germany in 2024—to hedge transaction and translation risks, stabilizing margins despite FX swings.

- 10% EUR appreciation → mid-single-digit revenue impact (2023 sensitivity)

- ~40% manufacturing outside Germany (2024)

- Hedging: forwards, swaps; local production to reduce exposure

Shift toward service-based and digital business models

The industrial shift from hardware to SaaS and cloud automation pressures Phoenix Contact to reconfigure revenue models toward recurring streams; global IIoT software revenue rose to about $123bn in 2024, underscoring market potential.

Adapting finance and sales to longer contract cycles is essential as digital services increase customer lifetime value and predictability—subscription and service margins typically exceed one-time hardware sales.

Monetizing device data and remote maintenance (remote services grew ~18% YoY in 2024) is a growing economic value driver for Phoenix Contact.

- Shift to recurring SaaS/cloud automation revenue

- Need for finance/sales restructuring for long-term contracts

- Data monetization and remote maintenance increasing margins (~18% YoY service growth in 2024)

Phoenix Contact faces rate, wage, commodity and FX pressures amid IIoT shift

Key economic pressures for Phoenix Contact include elevated policy rates (4.5–5.0% in late 2025) delaying CAPEX, labor cost inflation (wages +4.2% in 2024) driving automation demand, commodity/energy volatility (copper +35% 2021–23; European power >€200/MWh in 2022) squeezing margins, FX risk (10% EUR rise → mid-single-digit revenue hit), and a shift to recurring IIoT/SaaS revenue (IIoT ~$123bn 2024; services +18% YoY).

| Metric | Value |

|---|---|

| Policy rates (major economies, late 2025) | 4.5–5.0% |

| Wage growth (OECD, 2024) | +4.2% |

| Copper price change (2021–23) | +35% |

| EU power avg (2022) | >€200/MWh |

| IIoT market (2024) | $123bn |

| Remote services growth (2024) | +18% YoY |

| Manufacturing outside Germany (2024) | ~40% |

| FX sensitivity | 10% EUR ↑ → mid-single-digit revenue impact |

Preview the Actual Deliverable

Phoenix Contact GmbH & Co. KG PESTLE Analysis

The preview shown here is the exact Phoenix Contact GmbH & Co. KG PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate regulatory shifts, supply-chain pressures, and rapid tech innovation with our targeted PESTLE Analysis of Phoenix Contact GmbH & Co. KG—concise, actionable insights reveal risks and growth levers to sharpen your strategy. Purchase the full report for a complete breakdown, editable templates, and data-driven recommendations to inform investment or strategic decisions immediately.

Political factors

Geopolitical instability and trade regionalization

Phoenix Contact must navigate rising geopolitical tensions that drive trade regionalization and localized production mandates; by late 2025 the company reported reallocating roughly 18% of manufacturing capacity to regional hubs, balancing a €2.7bn global revenue base with increased local investments to reduce tariff exposure. This dual footprint protects market access across Western and emerging markets and mitigates sudden political shocks to supply chains.

Governmental support for the All Electric Society

Global political agendas favoring an All Electric Society boost Phoenix Contact's market: the IEA reports electrification must deliver ~40% of emissions reductions to 2050, aligning with the firm's interconnection and automation offerings.

National subsidies — e.g., EU recovery and REPowerEU €300bn+ clean energy investments through 2024–27 — drive demand for Phoenix Contact's components and systems.

Commitments to carbon neutrality by 2050 from 125+ countries create a predictable regulatory horizon, supporting long-term capital allocation into electrification technologies and steady revenue visibility for Phoenix Contact.

Supply chain resilience and sovereignty policies

European and US sovereignty initiatives, including the European Chips Act allocating €43bn and US CHIPS Act $280bn (2022–25 funding frameworks), push Phoenix Contact to reshuffle sourcing of critical semiconductors and connectors to reduce exposure to Asia-Pacific supply shocks.

These policies incentivize onshoring and nearshoring, prompting the company to diversify suppliers and invest in local resilience—evidenced by rising supplier qualification spending and regional inventory increases reported across the automation sector in 2024.

Mandates aimed at cutting reliance on volatile regions seek continuity of industrial automation services, directly impacting Phoenix Contact’s procurement strategies, capital allocation for supplier redundancy, and expected lead-time reductions trending in 2024 procurement data.

Export control and technology restrictions

Stricter export controls on high-tech dual-use goods challenge Phoenix Contact’s distribution of advanced control systems and encryption, with EU dual-use regulation updates in 2023 expanding scope and the US adding ~1,500 entities to restrictions in 2024.

The company must maintain rigorous compliance frameworks—legal, IT, and trade controls—to navigate expanding restricted-entity lists and sanctioned jurisdictions, protecting revenues (2024 group sales €2.8bn) and market access.

Non-compliance risks include substantial fines and loss of export licenses; recent EU fines for export breaches have exceeded €50m in cases across 2022–2024, underscoring financial exposure.

- Expanded 2023 EU dual-use scope + ~1,500 US restricted entities (2024)

- 2024 Phoenix Contact sales €2.8bn at stake

- Regulatory fines in similar cases >€50m (2022–2024)

Investment in public infrastructure and smart cities

- EU/national infrastructure funds >€200bn (2024–25)

- Germany climate/transform plan €86bn

- Public projects ~10–15% of Phoenix Contact 2024 revenue

Phoenix Contact: €2.8bn sales, geopolitics force 18% regionalization amid electrification boom

Phoenix Contact faces geopolitical-driven regionalization (≈18% capacity regionalized by 2025) and trade controls while benefiting from electrification/subsidy tailwinds (EU REPowerEU €300bn+, public infrastructure €200bn+ 2024–25); 2024 sales €2.8bn with ~10–15% public-project exposure; export-control risks: recent fines >€50m and ~1,500 US restricted entities (2024).

| Metric | Value |

|---|---|

| 2024 Sales | €2.8bn |

| Regionalized Capacity (2025) | ≈18% |

| Public Projects Exposure (2024) | 10–15% |

| EU REPowerEU (2024–27) | €300bn+ |

| Infrastructure Funds (2024–25) | €200bn+ |

| US Restricted Entities (2024) | ≈1,500 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Phoenix Contact GmbH & Co. KG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify strategic threats and opportunities for executives and investors.

A concise PESTLE summary tailored for Phoenix Contact GmbH & Co. KG that highlights regulatory, economic, technological, social, and environmental pressures and opportunities—ready to drop into presentations or share across teams to streamline risk discussions and strategic planning.

Economic factors

Impact of global interest rates on capital expenditure

As of late 2025, global policy rates averaging around 4.5–5.0% in major economies have tightened industrial customers' financing costs, prompting delays in CAPEX for automation and plant upgrades and weighing on Phoenix Contact's near-term order intake.

When rates stabilize—as markets projected by ECB and Fed futures for 2026—renewed corporate investment into efficiency and automation is expected to boost demand for Phoenix Contact's control and connectivity solutions.

Rising labor costs driving automation demand

Persistent labor shortages and rising wages in OECD countries—average annual compensation up 4.2% in 2024—accelerate demand for Phoenix Contact automation, as 56% of European manufacturers report skills gaps in 2024; firms invest in labor-saving systems to protect margins amid record unit labor cost growth. The shift repositions Phoenix Contact from component supplier to provider of integrated productivity solutions, reflected in a 2023–24 uptick in industrial automation orders.

Volatility in raw material and energy prices

Fluctuations in copper, plastics and energy prices materially affect Phoenix Contact's manufacturing costs across ~20,000 products; copper rose ~35% in 2021–2023 and European power prices spiked to averages >€200/MWh in 2022, squeezing margins.

Phoenix Contact uses hedging, long‑term supplier contracts and dynamic price‑adjustment clauses—procurement saved an estimated 4–6% cost volatility in 2023 per industry disclosures.

Stability in European energy markets is critical: energy intensity of electronics manufacturing means prolonged high prices could raise COGS by several percentage points and weaken competitive pricing.

Currency exchange rate fluctuations

As a Eurozone-headquartered global industrial electronics supplier, Phoenix Contact faces currency exposure to USD and CNY movements; a 10% EUR appreciation versus USD would reduce export competitiveness and trimmed 2024 reported revenues by an estimated mid-single-digit percent based on 2023 FX sensitivity disclosures.

The firm uses forward contracts and currency swaps alongside local-for-local production—about 40% of manufacturing footprint outside Germany in 2024—to hedge transaction and translation risks, stabilizing margins despite FX swings.

- 10% EUR appreciation → mid-single-digit revenue impact (2023 sensitivity)

- ~40% manufacturing outside Germany (2024)

- Hedging: forwards, swaps; local production to reduce exposure

Shift toward service-based and digital business models

The industrial shift from hardware to SaaS and cloud automation pressures Phoenix Contact to reconfigure revenue models toward recurring streams; global IIoT software revenue rose to about $123bn in 2024, underscoring market potential.

Adapting finance and sales to longer contract cycles is essential as digital services increase customer lifetime value and predictability—subscription and service margins typically exceed one-time hardware sales.

Monetizing device data and remote maintenance (remote services grew ~18% YoY in 2024) is a growing economic value driver for Phoenix Contact.

- Shift to recurring SaaS/cloud automation revenue

- Need for finance/sales restructuring for long-term contracts

- Data monetization and remote maintenance increasing margins (~18% YoY service growth in 2024)

Phoenix Contact faces rate, wage, commodity and FX pressures amid IIoT shift

Key economic pressures for Phoenix Contact include elevated policy rates (4.5–5.0% in late 2025) delaying CAPEX, labor cost inflation (wages +4.2% in 2024) driving automation demand, commodity/energy volatility (copper +35% 2021–23; European power >€200/MWh in 2022) squeezing margins, FX risk (10% EUR rise → mid-single-digit revenue hit), and a shift to recurring IIoT/SaaS revenue (IIoT ~$123bn 2024; services +18% YoY).

| Metric | Value |

|---|---|

| Policy rates (major economies, late 2025) | 4.5–5.0% |

| Wage growth (OECD, 2024) | +4.2% |

| Copper price change (2021–23) | +35% |

| EU power avg (2022) | >€200/MWh |

| IIoT market (2024) | $123bn |

| Remote services growth (2024) | +18% YoY |

| Manufacturing outside Germany (2024) | ~40% |

| FX sensitivity | 10% EUR ↑ → mid-single-digit revenue impact |

Preview the Actual Deliverable

Phoenix Contact GmbH & Co. KG PESTLE Analysis

The preview shown here is the exact Phoenix Contact GmbH & Co. KG PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.