Pinnacle West PESTLE Analysis

Skip the Research. Get the Strategy.

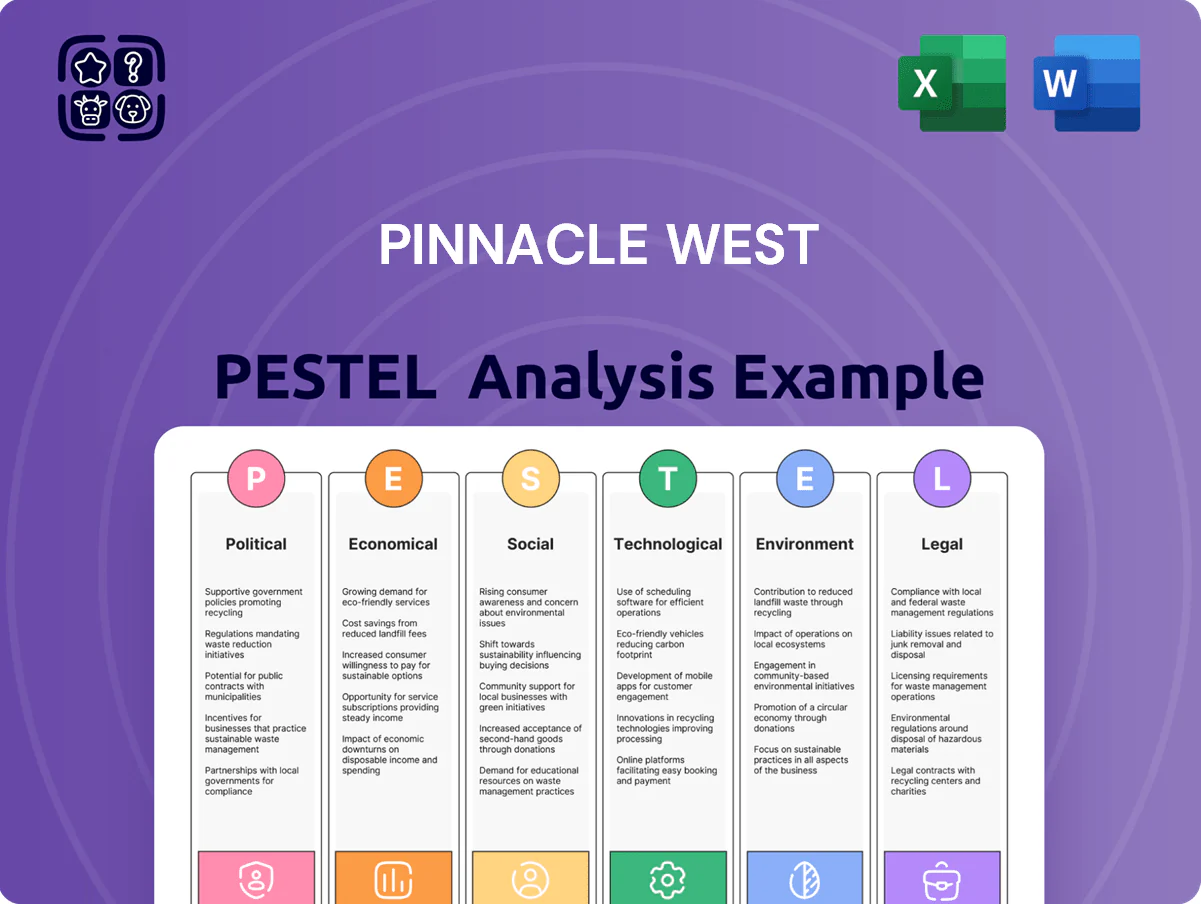

Explore how regulatory shifts, energy prices, and technological innovation are reshaping Pinnacle West’s risk and growth profile—our PESTLE distills the external forces that matter to investors and strategists. Buy the full analysis for a complete, actionable breakdown you can use in investment models, board decks, or strategy plans.

Political factors

Arizona Corporation Commission Regulatory Influence

The Arizona Corporation Commission sets APS rates and ROE; its 2024 decision approved a 9.0% return on equity benchmark for utilities, directly affecting Pinnacle West’s revenue profile and allowed rate base recovery.

By late 2025 the commission’s partisan makeup will crucially influence the speed of APS’s clean-energy transition and approvals for planned $3–4 billion transmission and generation projects.

Cost-recovery rulings hinge on commissioners’ political leanings as they weigh keeping average residential bills near the 2024 state median of $158/month against maintaining utility credit metrics and investment stability.

Federal Energy Policy and Tax Incentives

The Inflation Reduction Act’s extended tax credits, including a 30% investment tax credit and enhanced clean energy credits, lower Pinnacle West’s levelized costs for planned Arizona solar and battery projects, supporting projected capital savings of tens to hundreds of millions over the next decade.

These federal incentives reduce upfront deployment costs for utility-scale storage and PV arrays across the Arizona desert, improving project IRRs and shortening payback periods for APS renewables portfolios.

However, policy shifts in Washington can alter credit eligibility, timing, or value, introducing volatility to long-term cash flow forecasts and capital planning for Pinnacle West’s multi-year transition to clean energy.

State-Level Renewable Energy Mandates

Arizona debates over clean-energy timelines affect Pinnacle West resource planning; state-level carbon-free mandates do not exist yet, though GOP-controlled legislature has delayed sweeping rules while the Arizona Corporation Commission pushes for more renewables—utility-scale solar reached 3.1 GW in 2024. Local ordinances (e.g., Phoenix net-zero pledges) pressure Pinnacle West toward accelerated retirements of gas assets and higher CAPEX on renewables and storage.

Tribal Relations and Land Use Politics

Pinnacle West operates on and near Navajo and Hopi lands, making sovereign tribal relations central to political risk and permitting; in 2024 the company reported 2023 capital projects including $1.2bn in transmission investments that require tribal consultations.

Transmission siting and coal-plant decommissioning—notably Navajo Generating Station legacy issues—entail legal negotiations and compacts with tribes to secure easements and mitigate cultural impacts, affecting project timelines and costs.

- Essential: tribal approvals for transmission easements and right-of-way

- Financial impact: $1.2bn+ in transmission CAPEX (2023–2024)

- Operational risk: decommissioning negotiations affect grid reliability and timelines

Bipartisan Infrastructure Support for Regional Growth

Arizona's bipartisan push for industrial growth, including $25B+ in announced semiconductor investments since 2022, boosts demand for Pinnacle West's reliable power to serve high-capacity tech customers.

State and local officials coordinate with the utility to expand infrastructure across the Phoenix metro, helping align supply with projected peak load growth of ~1.5–2% annually.

Political alignment expedites permitting for substations and transmission corridors, reducing lead times for critical projects that underpin regional economic expansion.

- Semiconductor investments: $25B+ since 2022

- Projected peak load growth: ~1.5–2% annually

- Faster permitting for substations/transmission

Pinnacle West: 9% ROE, $1.2B+ transmission risk amid $25B semiconductor-driven demand

Regulatory decisions by the Arizona Corporation Commission (9.0% ROE in 2024) and federal incentives (IRA 30% ITC) materially affect Pinnacle West’s rate base recovery, capex economics and project IRRs; tribal approvals and $1.2bn+ transmission CAPEX drive permitting risk; Arizona’s $25B+ semiconductor buildouts and ~1.5–2% peak load growth increase demand and expedite permitting.

| Metric | Value |

|---|---|

| 2024 ROE | 9.0% |

| Transmission CAPEX | $1.2bn+ |

| Semiconductor investment | $25B+ |

| Peak load growth | ~1.5–2%/yr |

What is included in the product

Explores how macro-environmental factors uniquely affect Pinnacle West across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to inform executive strategy, risk management, and investor communication.

A concise, visually segmented PESTLE summary for Pinnacle West that’s easy to drop into presentations or share across teams, enabling quick alignment on external risks, regulatory impacts, and market positioning during planning sessions.

Economic factors

Industrial Expansion and Semiconductor Demand

The influx of semiconductor fabs led by TSMC and Intel in Arizona drives Pinnacle West load growth, with fabs typically adding 100–200+ MW each; TSMC's Phoenix-area investment reached $40 billion and Intel committed $20+ billion to U.S. fabs, underpinning regional demand.

These high-load industrial customers require 24/7 reliable power, shifting Pinnacle West toward heavy industrial service and increasing peak and baseload requirements by an estimated several hundred MW through 2026.

Meeting demand requires significant capital expenditure—distribution and transmission upgrades possibly totaling hundreds of millions—while providing a stable, expanding revenue base as fabs scale to full capacity by 2026.

Interest Rate Environment and Capital Costs

As a capital-intensive utility, Pinnacle West is highly sensitive to interest rates; U.S. benchmark yields rose in 2024–25 with the 10-year Treasury averaging ~4.2% in 2024 and 3.9% YTD 2025, increasing debt costs for transmission and generation projects.

Higher rates have pushed corporate borrowing spreads up; Pinnacle West’s adjusted debt servicing likely rose versus early-2020s, pressuring ROE recovery from regulator-authorized returns.

The company must protect its A- to BBB+ credit profile and optimize capital structure to prevent financing costs from eroding allowed returns and customer rates.

Inflationary Pressures on Operations and Maintenance

Ongoing inflation drove US producer prices up 2.2% year-over-year in 2024 for metals and components, pushing Pinnacle West’s O&M input costs—transformers, copper, steel—higher and contributing to reported 2024 O&M inflation of roughly 4–6% versus plan, creating potential budget variances not immediately offset by current Arizona utility rate structures.

Arizona Population Growth and Housing Market

- Population +190,000 (2023); ~7.5M (2024)

- Retail sales growth ~1–2%/yr

- Median home price ≈ $420,000 (2024)

- Housing supply +3–4% yr/yr

Energy Market Volatility and Fuel Costs

Fluctuations in natural gas and wholesale power prices drive variability in Pinnacle West’s fuel procurement; U.S. Henry Hub gas prices averaged about 3.50 USD/MMBtu in 2024 and saw monthly spikes above 6 USD/MMBtu, impacting short-term costs.

Most commodity costs are passed to customers via regulatory mechanisms, but spikes (e.g., 2024 peaks) raise affordability and political concerns in Arizona.

Pinnacle West uses hedging and a diversified fleet—nuclear, gas, renewables—to limit exposure; in 2024 hedges and fuel adjustments helped stabilize earnings despite volatile markets.

- 2024 Henry Hub avg ~3.50 USD/MMBtu; monthly highs >6 USD/MMBtu

- Regulatory cost pass-through reduces but does not eliminate rate risk

- Hedging + diverse generation mix mitigate earnings volatility

TSMC & Intel fabs spark 200–500MW Arizona load surge; $100sM capex, rising O&M

Semiconductor fabs (TSMC $40B, Intel $20B) add 100–200+ MW each, driving several-hundred-MW load growth through 2026; capex for upgrades likely in the low hundreds of millions. 2024–25 10Y Treasury ~4.2% (2024) / 3.9% YTD (2025) raised financing costs; 2024 O&M inflation ~4–6%. Arizona population ~7.5M (2024); retail sales +1–2%/yr; 2024 Henry Hub ~3.50 USD/MMBtu.

| Metric | 2024/25 |

|---|---|

| Load impact | +200–500 MW |

| Capex | $100sM |

| 10Y Treasury | 4.2% / 3.9% |

| O&M inflation | 4–6% |

| Population | ~7.5M |

| Henry Hub | $3.50/MMBtu |

Preview the Actual Deliverable

Pinnacle West PESTLE Analysis

The preview shown here is the exact Pinnacle West PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how regulatory shifts, energy prices, and technological innovation are reshaping Pinnacle West’s risk and growth profile—our PESTLE distills the external forces that matter to investors and strategists. Buy the full analysis for a complete, actionable breakdown you can use in investment models, board decks, or strategy plans.

Political factors

Arizona Corporation Commission Regulatory Influence

The Arizona Corporation Commission sets APS rates and ROE; its 2024 decision approved a 9.0% return on equity benchmark for utilities, directly affecting Pinnacle West’s revenue profile and allowed rate base recovery.

By late 2025 the commission’s partisan makeup will crucially influence the speed of APS’s clean-energy transition and approvals for planned $3–4 billion transmission and generation projects.

Cost-recovery rulings hinge on commissioners’ political leanings as they weigh keeping average residential bills near the 2024 state median of $158/month against maintaining utility credit metrics and investment stability.

Federal Energy Policy and Tax Incentives

The Inflation Reduction Act’s extended tax credits, including a 30% investment tax credit and enhanced clean energy credits, lower Pinnacle West’s levelized costs for planned Arizona solar and battery projects, supporting projected capital savings of tens to hundreds of millions over the next decade.

These federal incentives reduce upfront deployment costs for utility-scale storage and PV arrays across the Arizona desert, improving project IRRs and shortening payback periods for APS renewables portfolios.

However, policy shifts in Washington can alter credit eligibility, timing, or value, introducing volatility to long-term cash flow forecasts and capital planning for Pinnacle West’s multi-year transition to clean energy.

State-Level Renewable Energy Mandates

Arizona debates over clean-energy timelines affect Pinnacle West resource planning; state-level carbon-free mandates do not exist yet, though GOP-controlled legislature has delayed sweeping rules while the Arizona Corporation Commission pushes for more renewables—utility-scale solar reached 3.1 GW in 2024. Local ordinances (e.g., Phoenix net-zero pledges) pressure Pinnacle West toward accelerated retirements of gas assets and higher CAPEX on renewables and storage.

Tribal Relations and Land Use Politics

Pinnacle West operates on and near Navajo and Hopi lands, making sovereign tribal relations central to political risk and permitting; in 2024 the company reported 2023 capital projects including $1.2bn in transmission investments that require tribal consultations.

Transmission siting and coal-plant decommissioning—notably Navajo Generating Station legacy issues—entail legal negotiations and compacts with tribes to secure easements and mitigate cultural impacts, affecting project timelines and costs.

- Essential: tribal approvals for transmission easements and right-of-way

- Financial impact: $1.2bn+ in transmission CAPEX (2023–2024)

- Operational risk: decommissioning negotiations affect grid reliability and timelines

Bipartisan Infrastructure Support for Regional Growth

Arizona's bipartisan push for industrial growth, including $25B+ in announced semiconductor investments since 2022, boosts demand for Pinnacle West's reliable power to serve high-capacity tech customers.

State and local officials coordinate with the utility to expand infrastructure across the Phoenix metro, helping align supply with projected peak load growth of ~1.5–2% annually.

Political alignment expedites permitting for substations and transmission corridors, reducing lead times for critical projects that underpin regional economic expansion.

- Semiconductor investments: $25B+ since 2022

- Projected peak load growth: ~1.5–2% annually

- Faster permitting for substations/transmission

Pinnacle West: 9% ROE, $1.2B+ transmission risk amid $25B semiconductor-driven demand

Regulatory decisions by the Arizona Corporation Commission (9.0% ROE in 2024) and federal incentives (IRA 30% ITC) materially affect Pinnacle West’s rate base recovery, capex economics and project IRRs; tribal approvals and $1.2bn+ transmission CAPEX drive permitting risk; Arizona’s $25B+ semiconductor buildouts and ~1.5–2% peak load growth increase demand and expedite permitting.

| Metric | Value |

|---|---|

| 2024 ROE | 9.0% |

| Transmission CAPEX | $1.2bn+ |

| Semiconductor investment | $25B+ |

| Peak load growth | ~1.5–2%/yr |

What is included in the product

Explores how macro-environmental factors uniquely affect Pinnacle West across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to inform executive strategy, risk management, and investor communication.

A concise, visually segmented PESTLE summary for Pinnacle West that’s easy to drop into presentations or share across teams, enabling quick alignment on external risks, regulatory impacts, and market positioning during planning sessions.

Economic factors

Industrial Expansion and Semiconductor Demand

The influx of semiconductor fabs led by TSMC and Intel in Arizona drives Pinnacle West load growth, with fabs typically adding 100–200+ MW each; TSMC's Phoenix-area investment reached $40 billion and Intel committed $20+ billion to U.S. fabs, underpinning regional demand.

These high-load industrial customers require 24/7 reliable power, shifting Pinnacle West toward heavy industrial service and increasing peak and baseload requirements by an estimated several hundred MW through 2026.

Meeting demand requires significant capital expenditure—distribution and transmission upgrades possibly totaling hundreds of millions—while providing a stable, expanding revenue base as fabs scale to full capacity by 2026.

Interest Rate Environment and Capital Costs

As a capital-intensive utility, Pinnacle West is highly sensitive to interest rates; U.S. benchmark yields rose in 2024–25 with the 10-year Treasury averaging ~4.2% in 2024 and 3.9% YTD 2025, increasing debt costs for transmission and generation projects.

Higher rates have pushed corporate borrowing spreads up; Pinnacle West’s adjusted debt servicing likely rose versus early-2020s, pressuring ROE recovery from regulator-authorized returns.

The company must protect its A- to BBB+ credit profile and optimize capital structure to prevent financing costs from eroding allowed returns and customer rates.

Inflationary Pressures on Operations and Maintenance

Ongoing inflation drove US producer prices up 2.2% year-over-year in 2024 for metals and components, pushing Pinnacle West’s O&M input costs—transformers, copper, steel—higher and contributing to reported 2024 O&M inflation of roughly 4–6% versus plan, creating potential budget variances not immediately offset by current Arizona utility rate structures.

Arizona Population Growth and Housing Market

- Population +190,000 (2023); ~7.5M (2024)

- Retail sales growth ~1–2%/yr

- Median home price ≈ $420,000 (2024)

- Housing supply +3–4% yr/yr

Energy Market Volatility and Fuel Costs

Fluctuations in natural gas and wholesale power prices drive variability in Pinnacle West’s fuel procurement; U.S. Henry Hub gas prices averaged about 3.50 USD/MMBtu in 2024 and saw monthly spikes above 6 USD/MMBtu, impacting short-term costs.

Most commodity costs are passed to customers via regulatory mechanisms, but spikes (e.g., 2024 peaks) raise affordability and political concerns in Arizona.

Pinnacle West uses hedging and a diversified fleet—nuclear, gas, renewables—to limit exposure; in 2024 hedges and fuel adjustments helped stabilize earnings despite volatile markets.

- 2024 Henry Hub avg ~3.50 USD/MMBtu; monthly highs >6 USD/MMBtu

- Regulatory cost pass-through reduces but does not eliminate rate risk

- Hedging + diverse generation mix mitigate earnings volatility

TSMC & Intel fabs spark 200–500MW Arizona load surge; $100sM capex, rising O&M

Semiconductor fabs (TSMC $40B, Intel $20B) add 100–200+ MW each, driving several-hundred-MW load growth through 2026; capex for upgrades likely in the low hundreds of millions. 2024–25 10Y Treasury ~4.2% (2024) / 3.9% YTD (2025) raised financing costs; 2024 O&M inflation ~4–6%. Arizona population ~7.5M (2024); retail sales +1–2%/yr; 2024 Henry Hub ~3.50 USD/MMBtu.

| Metric | 2024/25 |

|---|---|

| Load impact | +200–500 MW |

| Capex | $100sM |

| 10Y Treasury | 4.2% / 3.9% |

| O&M inflation | 4–6% |

| Population | ~7.5M |

| Henry Hub | $3.50/MMBtu |

Preview the Actual Deliverable

Pinnacle West PESTLE Analysis

The preview shown here is the exact Pinnacle West PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.