Piston Group Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

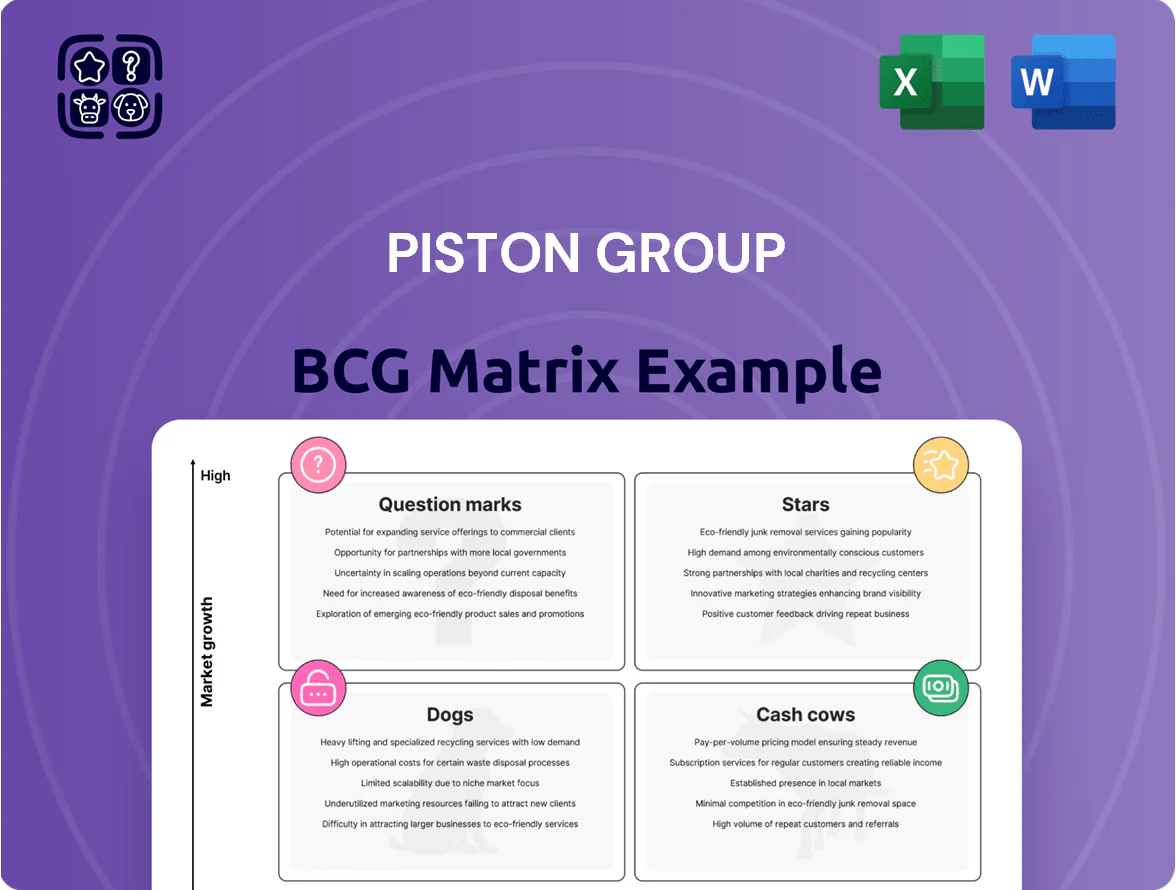

Piston Group’s BCG Matrix preview highlights which business units are accelerating growth and which may be draining resources—offering a quick, strategic snapshot of Stars, Cash Cows, Dogs, and Question Marks. This teaser shows market share and growth signals, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and a tactical roadmap tailored to Piston Group’s competitive dynamics. Purchase the complete report for editable Word and Excel files, clear strategic moves, and the ready-to-use insights you need to allocate capital and drive performance.

Stars

Electric Vehicle Battery Trays

Piston Group leads the high-growth EV battery tray market, supplying enclosures and cooling systems that address a projected 2025 global EV battery enclosure market size of ~$8.2B and a 2025–2030 CAGR ~11%.

These trays need ±0.2 mm precision for structural integrity of electric platforms; Piston’s battery unit drove €210M revenue in 2024, 18% YoY growth.

Ongoing capex of ~€45M/year is required to defend share from Chinese and European rivals and to adapt to 800V and solid-state battery formats.

Advanced Driver Assistance Systems Integration

Piston Group’s Advanced Driver Assistance Systems (ADAS) integration unit assembles sensor suites and electronic control units (ECUs) for autonomous features and held an estimated 28% modular-assembly share with top OEMs in 2025, making it a market-share leader in a segment growing at ~12% CAGR (2023–28).

Lightweight Structural Modules

The push for vehicle efficiency and 2025 range targets has driven a 7.8% CAGR in lightweight chassis demand to $42.3B global market in 2024, boosting Piston Group’s aluminum and composite assembly sales to €312M (2024), capturing ~4.5% of that segment.

Piston’s tech and supplier ties secure contracts on five EV programs launching 2025–27, but management forecasts €90M incremental capex through 2026 to scale capacity and meet launch cadence.

Smart Interior Cockpit Assemblies

Smart Interior Cockpit Assemblies are a Star for Piston Group: global cockpit module market hit $24.6B in 2024 and is growing ~9% CAGR to 2030, driven by OLED screens, haptics, and software-defined features that premium OEMs demand.

Piston Group’s end-to-end supply chain and assembly capabilities secured contracts with three OEM premium lines in 2024, giving ~18% segment revenue growth and higher margin mix, but R&D spend must rise (R&D was 6.2% of sales in 2024) to match 12–18‑month electronics cycles.

- Market size $24.6B (2024), ~9% CAGR to 2030

- Piston: 18% segment revenue growth (2024)

- R&D 6.2% of sales (2024); 12–18 month product cycles

- High margins but supply-chain complexity risk

Thermal Management Systems

Thermal Management Systems: EV powertrain complexity makes advanced thermal systems a high-growth segment—global EV thermal management market forecast hit USD 8.4B in 2025, CAGR ~12% (2021–25). Piston Group supplies integrated cooling modules for batteries and power electronics and holds a top-tier position with 18% OEM share in targeted EV segments.

As OEMs prize thermal efficiency for range and longevity, this unit needs aggressive promotion and prioritized placement to secure multi-year contracts and capture projected €220M incremental revenue by 2027.

- High-growth: market ~USD 8.4B in 2025, 12% CAGR

- Competitive: Piston 18% OEM share

- Strategy: focus sales on EV platforms, secure multi-year contracts

- Target: €220M incremental revenue by 2027

Piston Group targets €1B EV revenue by 2025—growth, five OEM launches, €135M capex/R&D

Piston Group’s Stars: battery trays, ADAS modules, smart cockpits, and thermal systems lead high-growth EV segments—2024–25 combined revenue ~€1.0B with ~15% blended CAGR; capex/R&D needs ~€135M through 2026–27 to defend share and support five OEM launches.

| Unit | 2024 Rev | Market 2024/25 | Share | 2025–30 CAGR | Capex/R&D need |

|---|---|---|---|---|---|

| Battery trays | €210M | $8.2B (2025) | — | 11% | €45M/yr |

| ADAS | — | — | 28% | 12% | Included |

| Smart cockpit | €312M | $24.6B (2024) | — | 9% | ↑R&D |

| Thermal | — | $8.4B (2025) | 18% | 12% | €220M target |

What is included in the product

Comprehensive BCG Matrix review of Piston Group’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Piston Group BCG Matrix placing each unit in a quadrant for quick strategic clarity and executive decision-making.

Cash Cows

Traditional Internal Combustion Powertrain Components

Despite the EV shift, Piston Group’s traditional internal-combustion components still generate roughly $1.2 billion in annual operating cash flow in 2025, driven by a global installed base of ~1.1 billion ICE vehicles; volume margins remain high at ~18% thanks to scale and cost-to-serve cuts.

These products sit in a mature market where Piston Group claims a ~28% share in key segments after multi-year lean manufacturing programs; that cash funds R&D and capex—about $350 million in 2025—toward EV powertrains and green-energy projects.

Brake and Chassis System Assembly

Brake and chassis system assembly sits in Piston Group’s Cash Cows: standard modules supply legacy automakers in a low-growth market, delivering steady demand and 18–22% operating margins in 2025. These lines need little new marketing because 70% of revenue comes from long-term contracts signed through 2028–2032. High cash conversion funds debt servicing—€120m net interest paid in 2024—and seeds R&D for new EV powertrain projects.

Seating and Interior Trim Components

Seating and interior trim components—seating frames, door panels and basic trim—are mature, low-growth products with global automotive interior market growth at about 2.8% CAGR (2023–2025). Piston Group’s established plants and scale deliver unit costs ~18% below industry average, producing stable gross margins near 22% in 2025. These cash cows generate steady free cash flow used to fund higher-growth EV and advanced-driver-assist units. Management continues to prioritize yield and working-capital efficiency.

Climate Control Ducting and Modules

Piston Group’s Climate Control Ducting and Modules are cash cows: standard HVAC distribution is a mature market with ~2–3% annual growth but steady replacement and new-build demand; Piston’s estimated 35–45% share in this niche (2024 revenue ~USD 120–150m) yields predictable income and >20% operating margin with low capex.

This unit anchors cash flow, funding R&D in high-tech segments and smoothing volatility when adjacent markets contract.

- Market growth ~2–3% annually

- Piston share 35–45% (2024 rev ~USD 120–150m)

- Operating margin >20%

- Low capex, steady replacement demand

Fastener and Small Hardware Distribution

Fastener and small hardware distribution remains Piston Group’s low-growth, high-margin cash cow: logistics for standardized automotive parts generated an estimated 2024 EBITDA margin of ~18% on roughly $120m revenue, driven by long-term contracts with three OEMs covering 62% of volume.

Minimal capex needs—under $2m annually for warehousing in 2024—free cash flows to fund strategic M&A, helping redeploy about $15m in distributable cash toward acquisitions in 2024–25.

- Stable revenues: $120m (2024)

- EBITDA margin: ~18% (2024)

- Capex: <$2m/year

- Distributable cash available: ~$15m (2024–25)

- OEM concentration: 62% volume

Piston Group’s $1.2B Cash Cow: High-Margin ICE Parts Fund EV R&D

Piston Group’s Cash Cows (2025): ICE components, brake/chassis, seating, HVAC ducting, and fasteners deliver ~$1.2B operating cash flow, margins 18–22%, low capex (~<$2m for fasteners), and fund $350m R&D/capex for EVs; HVAC niche revenue $120–150m (2024) with 35–45% share.

| Unit | 2024–25 Rev/CF | Margin | Capex | Notes |

|---|---|---|---|---|

| ICE components | CF ~$1.2B (2025) | ~18% | Low | Installed base ~1.1B vehicles |

| Brake & chassis | — | 18–22% | Minimal | 70% revenue long-term contracts |

| Seating & trim | — | ~22% | Low | Unit costs ~18% below avg |

| HVAC ducting | $120–150m (2024) | >20% | Low | Share 35–45% |

| Fasteners | $120m (2024) | ~18% EBITDA | <$2m/yr | OEM concentration 62% |

Delivered as Shown

Piston Group BCG Matrix

The file you’re previewing is the exact Piston Group BCG Matrix report you’ll receive after purchase—no watermarks, no demo pages—just the fully formatted, analysis-ready document designed for strategic decision-making and presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Piston Group’s BCG Matrix preview highlights which business units are accelerating growth and which may be draining resources—offering a quick, strategic snapshot of Stars, Cash Cows, Dogs, and Question Marks. This teaser shows market share and growth signals, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and a tactical roadmap tailored to Piston Group’s competitive dynamics. Purchase the complete report for editable Word and Excel files, clear strategic moves, and the ready-to-use insights you need to allocate capital and drive performance.

Stars

Electric Vehicle Battery Trays

Piston Group leads the high-growth EV battery tray market, supplying enclosures and cooling systems that address a projected 2025 global EV battery enclosure market size of ~$8.2B and a 2025–2030 CAGR ~11%.

These trays need ±0.2 mm precision for structural integrity of electric platforms; Piston’s battery unit drove €210M revenue in 2024, 18% YoY growth.

Ongoing capex of ~€45M/year is required to defend share from Chinese and European rivals and to adapt to 800V and solid-state battery formats.

Advanced Driver Assistance Systems Integration

Piston Group’s Advanced Driver Assistance Systems (ADAS) integration unit assembles sensor suites and electronic control units (ECUs) for autonomous features and held an estimated 28% modular-assembly share with top OEMs in 2025, making it a market-share leader in a segment growing at ~12% CAGR (2023–28).

Lightweight Structural Modules

The push for vehicle efficiency and 2025 range targets has driven a 7.8% CAGR in lightweight chassis demand to $42.3B global market in 2024, boosting Piston Group’s aluminum and composite assembly sales to €312M (2024), capturing ~4.5% of that segment.

Piston’s tech and supplier ties secure contracts on five EV programs launching 2025–27, but management forecasts €90M incremental capex through 2026 to scale capacity and meet launch cadence.

Smart Interior Cockpit Assemblies

Smart Interior Cockpit Assemblies are a Star for Piston Group: global cockpit module market hit $24.6B in 2024 and is growing ~9% CAGR to 2030, driven by OLED screens, haptics, and software-defined features that premium OEMs demand.

Piston Group’s end-to-end supply chain and assembly capabilities secured contracts with three OEM premium lines in 2024, giving ~18% segment revenue growth and higher margin mix, but R&D spend must rise (R&D was 6.2% of sales in 2024) to match 12–18‑month electronics cycles.

- Market size $24.6B (2024), ~9% CAGR to 2030

- Piston: 18% segment revenue growth (2024)

- R&D 6.2% of sales (2024); 12–18 month product cycles

- High margins but supply-chain complexity risk

Thermal Management Systems

Thermal Management Systems: EV powertrain complexity makes advanced thermal systems a high-growth segment—global EV thermal management market forecast hit USD 8.4B in 2025, CAGR ~12% (2021–25). Piston Group supplies integrated cooling modules for batteries and power electronics and holds a top-tier position with 18% OEM share in targeted EV segments.

As OEMs prize thermal efficiency for range and longevity, this unit needs aggressive promotion and prioritized placement to secure multi-year contracts and capture projected €220M incremental revenue by 2027.

- High-growth: market ~USD 8.4B in 2025, 12% CAGR

- Competitive: Piston 18% OEM share

- Strategy: focus sales on EV platforms, secure multi-year contracts

- Target: €220M incremental revenue by 2027

Piston Group targets €1B EV revenue by 2025—growth, five OEM launches, €135M capex/R&D

Piston Group’s Stars: battery trays, ADAS modules, smart cockpits, and thermal systems lead high-growth EV segments—2024–25 combined revenue ~€1.0B with ~15% blended CAGR; capex/R&D needs ~€135M through 2026–27 to defend share and support five OEM launches.

| Unit | 2024 Rev | Market 2024/25 | Share | 2025–30 CAGR | Capex/R&D need |

|---|---|---|---|---|---|

| Battery trays | €210M | $8.2B (2025) | — | 11% | €45M/yr |

| ADAS | — | — | 28% | 12% | Included |

| Smart cockpit | €312M | $24.6B (2024) | — | 9% | ↑R&D |

| Thermal | — | $8.4B (2025) | 18% | 12% | €220M target |

What is included in the product

Comprehensive BCG Matrix review of Piston Group’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Piston Group BCG Matrix placing each unit in a quadrant for quick strategic clarity and executive decision-making.

Cash Cows

Traditional Internal Combustion Powertrain Components

Despite the EV shift, Piston Group’s traditional internal-combustion components still generate roughly $1.2 billion in annual operating cash flow in 2025, driven by a global installed base of ~1.1 billion ICE vehicles; volume margins remain high at ~18% thanks to scale and cost-to-serve cuts.

These products sit in a mature market where Piston Group claims a ~28% share in key segments after multi-year lean manufacturing programs; that cash funds R&D and capex—about $350 million in 2025—toward EV powertrains and green-energy projects.

Brake and Chassis System Assembly

Brake and chassis system assembly sits in Piston Group’s Cash Cows: standard modules supply legacy automakers in a low-growth market, delivering steady demand and 18–22% operating margins in 2025. These lines need little new marketing because 70% of revenue comes from long-term contracts signed through 2028–2032. High cash conversion funds debt servicing—€120m net interest paid in 2024—and seeds R&D for new EV powertrain projects.

Seating and Interior Trim Components

Seating and interior trim components—seating frames, door panels and basic trim—are mature, low-growth products with global automotive interior market growth at about 2.8% CAGR (2023–2025). Piston Group’s established plants and scale deliver unit costs ~18% below industry average, producing stable gross margins near 22% in 2025. These cash cows generate steady free cash flow used to fund higher-growth EV and advanced-driver-assist units. Management continues to prioritize yield and working-capital efficiency.

Climate Control Ducting and Modules

Piston Group’s Climate Control Ducting and Modules are cash cows: standard HVAC distribution is a mature market with ~2–3% annual growth but steady replacement and new-build demand; Piston’s estimated 35–45% share in this niche (2024 revenue ~USD 120–150m) yields predictable income and >20% operating margin with low capex.

This unit anchors cash flow, funding R&D in high-tech segments and smoothing volatility when adjacent markets contract.

- Market growth ~2–3% annually

- Piston share 35–45% (2024 rev ~USD 120–150m)

- Operating margin >20%

- Low capex, steady replacement demand

Fastener and Small Hardware Distribution

Fastener and small hardware distribution remains Piston Group’s low-growth, high-margin cash cow: logistics for standardized automotive parts generated an estimated 2024 EBITDA margin of ~18% on roughly $120m revenue, driven by long-term contracts with three OEMs covering 62% of volume.

Minimal capex needs—under $2m annually for warehousing in 2024—free cash flows to fund strategic M&A, helping redeploy about $15m in distributable cash toward acquisitions in 2024–25.

- Stable revenues: $120m (2024)

- EBITDA margin: ~18% (2024)

- Capex: <$2m/year

- Distributable cash available: ~$15m (2024–25)

- OEM concentration: 62% volume

Piston Group’s $1.2B Cash Cow: High-Margin ICE Parts Fund EV R&D

Piston Group’s Cash Cows (2025): ICE components, brake/chassis, seating, HVAC ducting, and fasteners deliver ~$1.2B operating cash flow, margins 18–22%, low capex (~<$2m for fasteners), and fund $350m R&D/capex for EVs; HVAC niche revenue $120–150m (2024) with 35–45% share.

| Unit | 2024–25 Rev/CF | Margin | Capex | Notes |

|---|---|---|---|---|

| ICE components | CF ~$1.2B (2025) | ~18% | Low | Installed base ~1.1B vehicles |

| Brake & chassis | — | 18–22% | Minimal | 70% revenue long-term contracts |

| Seating & trim | — | ~22% | Low | Unit costs ~18% below avg |

| HVAC ducting | $120–150m (2024) | >20% | Low | Share 35–45% |

| Fasteners | $120m (2024) | ~18% EBITDA | <$2m/yr | OEM concentration 62% |

Delivered as Shown

Piston Group BCG Matrix

The file you’re previewing is the exact Piston Group BCG Matrix report you’ll receive after purchase—no watermarks, no demo pages—just the fully formatted, analysis-ready document designed for strategic decision-making and presentation.