Plug Power PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

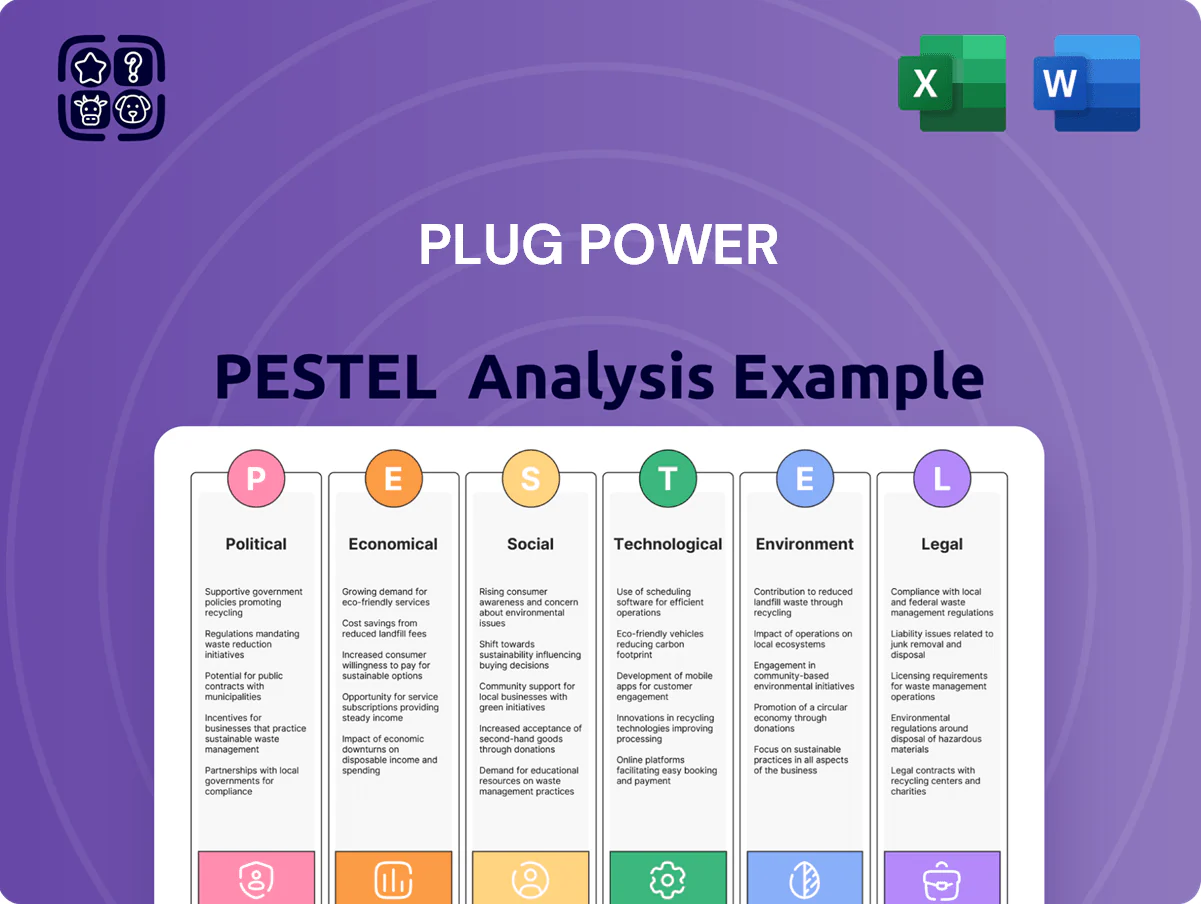

Unlock strategic clarity with our PESTLE Analysis of Plug Power—mapping political, economic, social, technological, legal, and environmental forces that will shape its hydrogen and fuel-cell ambitions; ideal for investors and strategists seeking actionable foresight. Purchase the full, editable report to access deep-dive insights, risk forecasts, and opportunity maps ready for immediate use.

Political factors

Implementation of Clean Hydrogen Production Tax Credits

The finalization of 45V guidance under the Inflation Reduction Act remains Plug Power’s key political driver through 2025, as rules on additionality, deliverability and hourly matching determine eligibility for tax credits that can cover up to 30–40% of green hydrogen production costs; DOE and IRS updates in 2024 clarified hourly matching thresholds critical for project economics. Plug Power has aligned U.S. production sites to meet federal standards, targeting 500+ MW electrolyzer capacity by 2025 to maximize incentives. These policies are central to narrowing the green premium versus gray hydrogen, where renewable-based levellized costs aim to fall below $4/kg with credits versus current market ranges of $6–8/kg.

Geopolitical Energy Security Initiatives

The global shift toward energy independence in Europe and North America has placed Plug Power at the center of strategic political planning by late 2025, with EU and US policies targeting a 50% reduction in gas import reliance by 2030 boosting demand for hydrogen solutions.

Governments view hydrogen as critical to reduce reliance on imported natural gas and volatile markets, citing EU Hydrogen Strategy targets of up to 10 million tonnes domestic production by 2030 and US IRA incentives expanding clean hydrogen tax credits to $3/kg for qualified projects.

Plug Power benefits from state-sponsored grants and bilateral agreements—receiving over $1.2 billion in public funding and commitments through 2025—which de-risk projects and attract private capital.

This political support accelerates hydrogen infrastructure build-out across regions, enabling Plug Power to scale electrolyzer and green hydrogen capacity toward planned multi-GW projects and projected revenue growth tied to infrastructure deployments.

European Union Green Deal and Hydrogen Bank

Plug Power expanded in Europe after winning supply contracts tied to the EU Green Deal and Hydrogen Bank auctions, targeting markets where EU funding aims to deploy 10 Mt H2/year by 2030; Plug Power reported €170m of European backlog in 2025. These schemes create price floors/subsidies that narrow the LCOH gap, with Hydrogen Bank rounds providing up to €3–5/kg equivalent support in early auctions. Participation in cross-border projects positions Plug Power as a core technology provider for industrial decarbonization, diversifying revenue beyond the US and contributing to 25–30% of projected 2026 international revenue.

Federal Loan Guarantee Programs

DOE Loan Programs Office support has underpinned Plug Power’s 2025 capital plan, including a conditional $1.2 billion loan facility announced in Q1 2025 to finance electrolyzer and green hydrogen projects.

Access to low-cost federal financing—estimated interest savings of ~$150–200 million vs. private markets—enables faster scale-up without diluting equity or taking high-interest debt.

This political backing reduces investment risk, catalyzing additional private commitments (>$700 million in co-investment reported in 2025) and signaling long-term government commitment to the US hydrogen supply chain.

- DOE loan: ~$1.2B (2025)

- Estimated interest savings: $150–200M

- Private co-investment attracted: >$700M

- Supports electrolyzer and green H2 plant scale-up

State-Level Decarbonization Mandates

State mandates in California, New York and Georgia drive immediate demand for Plug Power’s fuel cells—California’s Advanced Clean Fleets and New York’s Climate Leadership targets plus Georgia’s port electrification commitments underpin refueling and production growth.

Plug Power sites green hydrogen hubs in these states to access incentives and faster permits; as of 2025 the company reported hub pipeline capacity ~400 MW and regional offtake agreements representing >$1.2B revenue backlog.

- Localized mandates = near-term commercial demand

- Zero-emission heavy-duty rules create fleet refueling needs

- Hub placement maximizes incentives, lowers permitting time

- State action often outpaces federal policy, offering steady regional growth

Plug Power scales 500+MW U.S. electrolyzers, $1.2B DOE loan and $1.9B total funding

Federal IRA/45V rules and DOE/IRS clarifications (2024) drive Plug Power’s U.S. buildout—targeting 500+ MW electrolyzers by 2025 and a $1.2B DOE loan (2025); public funding >$1.2B and private co-investment >$700M de-risk projects. EU Hydrogen Bank and Green Deal boost European backlog (€170M, 2025). State mandates (CA, NY, GA) underpin ~400 MW hub pipeline and >$1.2B regional revenue backlog.

| Metric | Value |

|---|---|

| US electrolyzer target (2025) | 500+ MW |

| DOE loan (2025) | $1.2B |

| Public funding to 2025 | $1.2B+ |

| Private co-investment (2025) | $700M+ |

| EU backlog (2025) | €170M |

| Hub pipeline (2025) | ~400 MW |

| Regional revenue backlog | $1.2B+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Plug Power across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, funding, and risk management for executives, investors, and consultants.

A concise, visually segmented PESTLE snapshot for Plug Power that eases meeting prep and supports quick decision-making by highlighting regulatory, market, and technological risks and opportunities.

Economic factors

Impact of Interest Rate Volatility

As a capital-intensive business, Plug Power remained highly sensitive to global interest rate volatility at the end of 2025; the US Fed funds rate plateaued near 5.25%–5.50%, raising weighted average cost of capital for large electrolyzer and hydrogen facility projects. High rates increased financing costs, squeezing margins—Plug Power reported net cash used in operations of $1.1bn in FY2025 and continued to prioritize debt restructuring and strategic partnerships. Management secured asset sales and JV agreements reducing near-term debt by roughly $300m and extended maturities to lower refinancing risk. A stabilizing rate environment is crucial for Plug Power to achieve targets of positive cash flow and sustainable profitability.

Hydrogen Price Parity with Diesel

In 2025, hydrogen reaching price parity with diesel—target ~$2.50–$3.00/kg versus diesel-equivalent ~$3.00–$3.50/gal—remains a critical economic benchmark for Plug Power’s logistics market penetration.

Vertical integration and scaled production cut Plug Power’s levelized cost of hydrogen; company guidance and industry estimates show electrolyzer CAPEX down ~30–40% since 2021, improving unit economics.

As electrolyzer costs fall and Plug’s end-to-end offering lowers total cost of ownership for fleets by an estimated 10–25%, price convergence becomes the main driver of mass adoption.

Economies of Scale in Gigafactory Production

By end-2025 the Rochester Gigafactory reached full operational maturity, enabling Plug Power to cut PEM stack unit costs by roughly 35% versus 2023 levels, boosting gross margins on hardware to ~28% in 2025. Mass production supports competitive pricing in the global electrolyzer market while supplying Plug Power’s own hydrogen projects, reducing per-unit capex and opex. Manufacturing scale is the firm’s primary defense against lower-cost international rivals.

Corporate Capital Allocation and Liquidity

Managing liquidity and capital expenditures was central for Plug Power in 2025 as the company shifted from high-burn growth to disciplined spending, targeting positive adjusted EBITDA by late 2025 while trimming capex; FY 2025 guidance reduced capex to roughly $200–300m versus prior peaks.

Investors tracked funding via revenue, strategic JV deals (e.g., SK On/partners) and selective equity raises; Plug ended 3Q 2025 with cash and equivalents near $450m and total debt around $1.2bn, highlighting balance-sheet focus to support multi-year hydrogen infrastructure projects.

- Capex guidance 2025: ~$200–300m

- Cash & equivalents ~ $450m (3Q 2025)

- Total debt ~ $1.2bn (3Q 2025)

- Target: positive adjusted EBITDA by late 2025

Supply Chain Cost Management

Fluctuations in iridium and platinum prices—iridium rose ~15% in 2024 while platinum traded near $1,000/oz—raise input cost risk for Plug Power’s PEM electrolyzers, directly affecting margins on green hydrogen projects.

Plug Power reported investments in thrifting and recycling R&D (capex allocation increased in 2024) to cut precious-metal use; such measures lower exposure to spot-price volatility.

Rising global logistics costs (container rates up vs. 2023) and constrained availability of specialized components lengthen timelines and inflate budgets for large-scale plants.

Proactive supply-chain management—local sourcing, inventory hedging, recycling—remains critical to preserve project economics and target competitive $3–5/kg green hydrogen pathways.

- Iridium/platinum price volatility: +15% iridium (2024); platinum ≈ $1,000/oz

- Capex shift to thrifting/recycling in 2024

- Higher logistics/component constraints delaying timelines

- Supply-chain strategies key to $3–5/kg hydrogen targets

Plug trims capex, burns $1.1B as rates lift WACC; H2 parity target $2.50–3/kg

High rates in 2025 lifted WACC, pressuring margins; Plug used $1.1bn cash in FY2025, cut capex to $200–300m and held ~$450m cash (3Q25) vs $1.2bn debt. Electrolyzer CAPEX down ~30–40% since 2021; Rochester cuts PEM costs ~35% vs 2023. Target hydrogen parity ~$2.50–3.00/kg; iridium +15% (2024), platinum ≈ $1,000/oz, supply-chain strains raise timelines and costs.

| Metric | Value |

|---|---|

| Cash (3Q25) | $450m |

| Total debt (3Q25) | $1.2bn |

| Capex FY2025 | $200–300m |

| Electrolyzer CAPEX drop | 30–40% |

| PEM cost reduction | ~35% |

| H2 parity target | $2.50–3.00/kg |

Preview the Actual Deliverable

Plug Power PESTLE Analysis

The preview shown here is the exact Plug Power PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Plug Power—mapping political, economic, social, technological, legal, and environmental forces that will shape its hydrogen and fuel-cell ambitions; ideal for investors and strategists seeking actionable foresight. Purchase the full, editable report to access deep-dive insights, risk forecasts, and opportunity maps ready for immediate use.

Political factors

Implementation of Clean Hydrogen Production Tax Credits

The finalization of 45V guidance under the Inflation Reduction Act remains Plug Power’s key political driver through 2025, as rules on additionality, deliverability and hourly matching determine eligibility for tax credits that can cover up to 30–40% of green hydrogen production costs; DOE and IRS updates in 2024 clarified hourly matching thresholds critical for project economics. Plug Power has aligned U.S. production sites to meet federal standards, targeting 500+ MW electrolyzer capacity by 2025 to maximize incentives. These policies are central to narrowing the green premium versus gray hydrogen, where renewable-based levellized costs aim to fall below $4/kg with credits versus current market ranges of $6–8/kg.

Geopolitical Energy Security Initiatives

The global shift toward energy independence in Europe and North America has placed Plug Power at the center of strategic political planning by late 2025, with EU and US policies targeting a 50% reduction in gas import reliance by 2030 boosting demand for hydrogen solutions.

Governments view hydrogen as critical to reduce reliance on imported natural gas and volatile markets, citing EU Hydrogen Strategy targets of up to 10 million tonnes domestic production by 2030 and US IRA incentives expanding clean hydrogen tax credits to $3/kg for qualified projects.

Plug Power benefits from state-sponsored grants and bilateral agreements—receiving over $1.2 billion in public funding and commitments through 2025—which de-risk projects and attract private capital.

This political support accelerates hydrogen infrastructure build-out across regions, enabling Plug Power to scale electrolyzer and green hydrogen capacity toward planned multi-GW projects and projected revenue growth tied to infrastructure deployments.

European Union Green Deal and Hydrogen Bank

Plug Power expanded in Europe after winning supply contracts tied to the EU Green Deal and Hydrogen Bank auctions, targeting markets where EU funding aims to deploy 10 Mt H2/year by 2030; Plug Power reported €170m of European backlog in 2025. These schemes create price floors/subsidies that narrow the LCOH gap, with Hydrogen Bank rounds providing up to €3–5/kg equivalent support in early auctions. Participation in cross-border projects positions Plug Power as a core technology provider for industrial decarbonization, diversifying revenue beyond the US and contributing to 25–30% of projected 2026 international revenue.

Federal Loan Guarantee Programs

DOE Loan Programs Office support has underpinned Plug Power’s 2025 capital plan, including a conditional $1.2 billion loan facility announced in Q1 2025 to finance electrolyzer and green hydrogen projects.

Access to low-cost federal financing—estimated interest savings of ~$150–200 million vs. private markets—enables faster scale-up without diluting equity or taking high-interest debt.

This political backing reduces investment risk, catalyzing additional private commitments (>$700 million in co-investment reported in 2025) and signaling long-term government commitment to the US hydrogen supply chain.

- DOE loan: ~$1.2B (2025)

- Estimated interest savings: $150–200M

- Private co-investment attracted: >$700M

- Supports electrolyzer and green H2 plant scale-up

State-Level Decarbonization Mandates

State mandates in California, New York and Georgia drive immediate demand for Plug Power’s fuel cells—California’s Advanced Clean Fleets and New York’s Climate Leadership targets plus Georgia’s port electrification commitments underpin refueling and production growth.

Plug Power sites green hydrogen hubs in these states to access incentives and faster permits; as of 2025 the company reported hub pipeline capacity ~400 MW and regional offtake agreements representing >$1.2B revenue backlog.

- Localized mandates = near-term commercial demand

- Zero-emission heavy-duty rules create fleet refueling needs

- Hub placement maximizes incentives, lowers permitting time

- State action often outpaces federal policy, offering steady regional growth

Plug Power scales 500+MW U.S. electrolyzers, $1.2B DOE loan and $1.9B total funding

Federal IRA/45V rules and DOE/IRS clarifications (2024) drive Plug Power’s U.S. buildout—targeting 500+ MW electrolyzers by 2025 and a $1.2B DOE loan (2025); public funding >$1.2B and private co-investment >$700M de-risk projects. EU Hydrogen Bank and Green Deal boost European backlog (€170M, 2025). State mandates (CA, NY, GA) underpin ~400 MW hub pipeline and >$1.2B regional revenue backlog.

| Metric | Value |

|---|---|

| US electrolyzer target (2025) | 500+ MW |

| DOE loan (2025) | $1.2B |

| Public funding to 2025 | $1.2B+ |

| Private co-investment (2025) | $700M+ |

| EU backlog (2025) | €170M |

| Hub pipeline (2025) | ~400 MW |

| Regional revenue backlog | $1.2B+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Plug Power across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, funding, and risk management for executives, investors, and consultants.

A concise, visually segmented PESTLE snapshot for Plug Power that eases meeting prep and supports quick decision-making by highlighting regulatory, market, and technological risks and opportunities.

Economic factors

Impact of Interest Rate Volatility

As a capital-intensive business, Plug Power remained highly sensitive to global interest rate volatility at the end of 2025; the US Fed funds rate plateaued near 5.25%–5.50%, raising weighted average cost of capital for large electrolyzer and hydrogen facility projects. High rates increased financing costs, squeezing margins—Plug Power reported net cash used in operations of $1.1bn in FY2025 and continued to prioritize debt restructuring and strategic partnerships. Management secured asset sales and JV agreements reducing near-term debt by roughly $300m and extended maturities to lower refinancing risk. A stabilizing rate environment is crucial for Plug Power to achieve targets of positive cash flow and sustainable profitability.

Hydrogen Price Parity with Diesel

In 2025, hydrogen reaching price parity with diesel—target ~$2.50–$3.00/kg versus diesel-equivalent ~$3.00–$3.50/gal—remains a critical economic benchmark for Plug Power’s logistics market penetration.

Vertical integration and scaled production cut Plug Power’s levelized cost of hydrogen; company guidance and industry estimates show electrolyzer CAPEX down ~30–40% since 2021, improving unit economics.

As electrolyzer costs fall and Plug’s end-to-end offering lowers total cost of ownership for fleets by an estimated 10–25%, price convergence becomes the main driver of mass adoption.

Economies of Scale in Gigafactory Production

By end-2025 the Rochester Gigafactory reached full operational maturity, enabling Plug Power to cut PEM stack unit costs by roughly 35% versus 2023 levels, boosting gross margins on hardware to ~28% in 2025. Mass production supports competitive pricing in the global electrolyzer market while supplying Plug Power’s own hydrogen projects, reducing per-unit capex and opex. Manufacturing scale is the firm’s primary defense against lower-cost international rivals.

Corporate Capital Allocation and Liquidity

Managing liquidity and capital expenditures was central for Plug Power in 2025 as the company shifted from high-burn growth to disciplined spending, targeting positive adjusted EBITDA by late 2025 while trimming capex; FY 2025 guidance reduced capex to roughly $200–300m versus prior peaks.

Investors tracked funding via revenue, strategic JV deals (e.g., SK On/partners) and selective equity raises; Plug ended 3Q 2025 with cash and equivalents near $450m and total debt around $1.2bn, highlighting balance-sheet focus to support multi-year hydrogen infrastructure projects.

- Capex guidance 2025: ~$200–300m

- Cash & equivalents ~ $450m (3Q 2025)

- Total debt ~ $1.2bn (3Q 2025)

- Target: positive adjusted EBITDA by late 2025

Supply Chain Cost Management

Fluctuations in iridium and platinum prices—iridium rose ~15% in 2024 while platinum traded near $1,000/oz—raise input cost risk for Plug Power’s PEM electrolyzers, directly affecting margins on green hydrogen projects.

Plug Power reported investments in thrifting and recycling R&D (capex allocation increased in 2024) to cut precious-metal use; such measures lower exposure to spot-price volatility.

Rising global logistics costs (container rates up vs. 2023) and constrained availability of specialized components lengthen timelines and inflate budgets for large-scale plants.

Proactive supply-chain management—local sourcing, inventory hedging, recycling—remains critical to preserve project economics and target competitive $3–5/kg green hydrogen pathways.

- Iridium/platinum price volatility: +15% iridium (2024); platinum ≈ $1,000/oz

- Capex shift to thrifting/recycling in 2024

- Higher logistics/component constraints delaying timelines

- Supply-chain strategies key to $3–5/kg hydrogen targets

Plug trims capex, burns $1.1B as rates lift WACC; H2 parity target $2.50–3/kg

High rates in 2025 lifted WACC, pressuring margins; Plug used $1.1bn cash in FY2025, cut capex to $200–300m and held ~$450m cash (3Q25) vs $1.2bn debt. Electrolyzer CAPEX down ~30–40% since 2021; Rochester cuts PEM costs ~35% vs 2023. Target hydrogen parity ~$2.50–3.00/kg; iridium +15% (2024), platinum ≈ $1,000/oz, supply-chain strains raise timelines and costs.

| Metric | Value |

|---|---|

| Cash (3Q25) | $450m |

| Total debt (3Q25) | $1.2bn |

| Capex FY2025 | $200–300m |

| Electrolyzer CAPEX drop | 30–40% |

| PEM cost reduction | ~35% |

| H2 parity target | $2.50–3.00/kg |

Preview the Actual Deliverable

Plug Power PESTLE Analysis

The preview shown here is the exact Plug Power PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review or presentation.