Shanghai Prime Machinery PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and tech innovation are shaping Shanghai Prime Machinery's strategic outlook—our concise PESTLE highlights key external drivers and risks to inform smarter decisions. Ready-made for investors and strategists, the full analysis delivers actionable insights, editable formats, and data-driven recommendations. Purchase the complete PESTLE now to unlock the detailed intelligence you need.

Political factors

State-led industrial modernization policy

As of late 2025 the Made in China 2025 roadmap and follow-up industrial upgrade policies continue to prioritize high-end equipment, directing roughly CNY 420 billion in targeted industrial funds in 2024–25; Shanghai Prime Machinery gains from state backing for domestic core-component self-sufficiency and advanced manufacturing capability upgrades.

Geopolitical trade tensions and export barriers

Ongoing China-West trade friction reduced Chinese machinery exports by 9.7% y/y in 2024, pressuring Shanghai Prime Machinery’s fastener shipments; EU and US tariffs plus anti-dumping probes (over 30 ongoing cases in 2023–24) push the firm to reorient toward China’s domestic market and Belt and Road partners, where exports to Southeast Asia rose 14% in 2024; navigating sanctions and bilateral diplomacy is critical to preserve global distribution and ~$120m export revenue streams.

State-owned enterprise reform mandates

As a subsidiary of Shanghai Electric Group, SPMC faces SOE reform mandates that in 2024 targeted RMB 1.5–2.0 trillion in mixed-ownership reforms across central and local SOEs, pushing SPMC toward clearer corporate governance and minority investor protections.

Regulators demand improved board independence and performance metrics; Shanghai Electric reported a 2024 ROE of ~6.8%, prompting internal restructuring to meet state targets for higher market competitiveness.

Political pressure ties efficiency gains to national goals—energy transition and manufacturing upgrades—aligning SPMC’s strategic shifts with China’s 2025 industrial policy and state-directed investment priorities.

Regional stability in manufacturing hubs

Political stability in Shanghai supports SPMC’s manufacturing base; Shanghai reported zero major civil disruptions in 2024 and ranks top 5 in China for business environment, sustaining operations for 90% of local MNCs.

Municipal policies—including a 2025 tax incentive package reducing manufacturing VAT by up to 3 percentage points for advanced equipment—create a predictable regulatory framework that aids investment decisions.

This environment underpins long-term capital deployment and supply-chain reliability: Shanghai’s port handled 43.7 million TEUs in 2024, ensuring resilient inbound/outbound logistics for SPMC.

- Stable local governance: low disruption, high business confidence

- Policy support: VAT cuts and targeted incentives through 2025

- Logistics strength: 43.7M TEUs at Shanghai port (2024)

Belt and Road Initiative integration

The Belt and Road Initiative expansion gives Shanghai Prime Machinery political access to Southeast and Central Asian markets, where BRI commitments total over $1.0 trillion in projects since 2013 and $150–200 billion annually in recent years, supporting demand for industrial tools and fasteners.

Government-backed infrastructure spending in 2023–2025 in BRI corridors rose ~8–12% year-on-year, creating a predictable order pipeline SPMC can target to offset revenue risks from restrictive Western trade regimes.

- BRI projects cumulative financing >$1.0T since 2013

- Annual BRI-related spend ~ $150–200B recently

- Infrastructure spend growth in corridors +8–12% (2023–25)

- Strategic diplomatic ties mitigate Western market losses

Policy Push, Trade Headwinds and BRI Scale Shape SPMC’s 2024–25 Risk-Return Pivot

State support for high-end equipment (CNY 420bn funds 2024–25), trade friction cutting exports 9.7% y/y (2024) and ~30 anti-dumping probes, SOE mixed-ownership reforms (RMB 1.5–2.0tn target 2024), Shanghai port 43.7M TEU (2024), BRI pipeline >$1.0T since 2013 with $150–200B p.a., and municipal VAT cuts (~3ppt) shape SPMC’s political risk and market pivot.

| Metric | Value |

|---|---|

| Targeted industrial funds | CNY 420bn (2024–25) |

| Machinery export change | -9.7% (2024) |

| Port throughput | 43.7M TEU (2024) |

| BRI financing | >$1.0T since 2013; $150–200B p.a. |

| SOE reform target | RMB 1.5–2.0tn (2024) |

What is included in the product

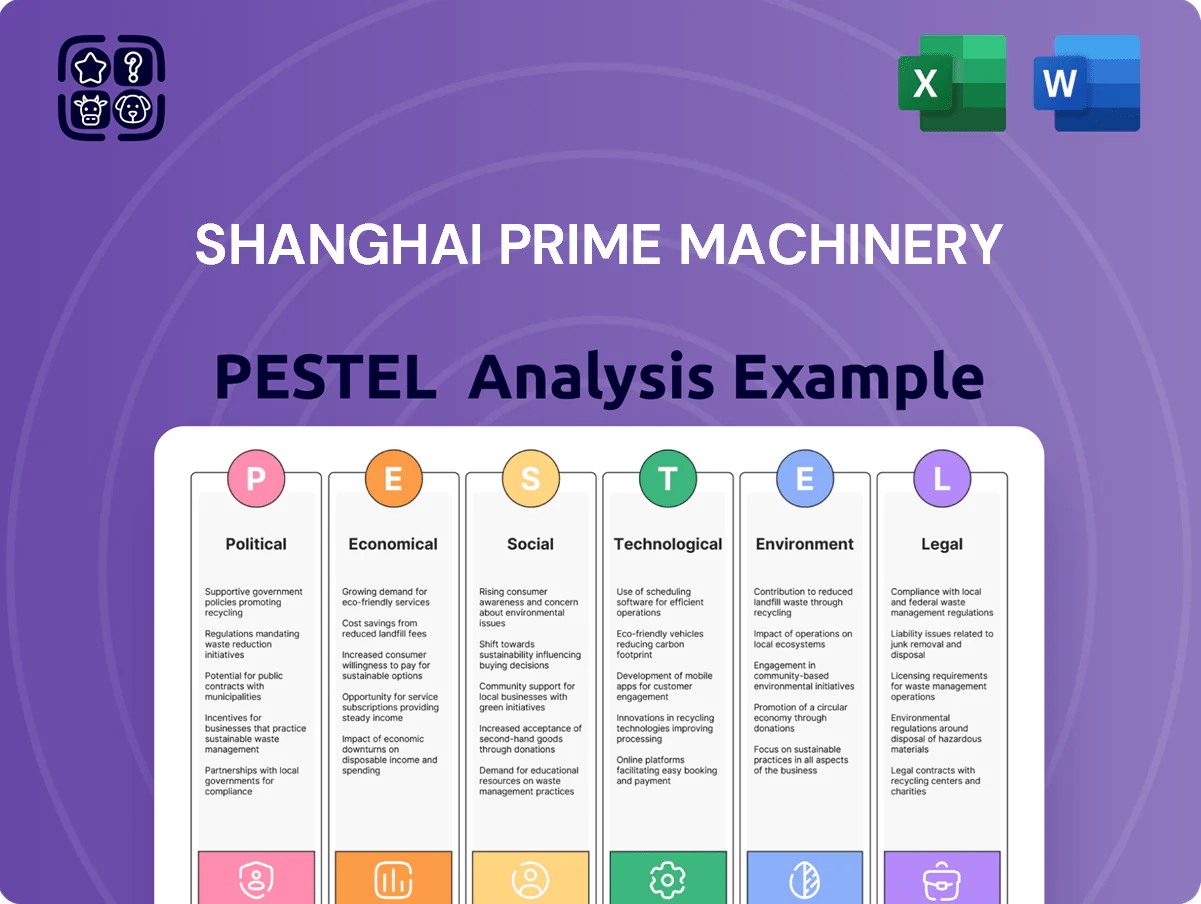

Explores how macro-environmental factors uniquely affect Shanghai Prime Machinery across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and entrepreneurs in identifying threats, opportunities, and actionable scenarios for strategy, funding, and operational planning.

A concise, visually segmented PESTLE summary of Shanghai Prime Machinery that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and strategic positioning during planning sessions.

Economic factors

Fluctuations in global raw material costs

Fluctuations in global raw material costs — notably a 22% year‑over‑year rise in steel prices through Q3 2025 — sharply pressure Shanghai Prime Machinery’s gross margin, since metals account for roughly 48% of COGS. Commodity-market volatility in 2025 increased input-cost variance by 15% vs 2023, directly eroding operating margins. Effective hedging reduced exposure: SPMC’s futures/forward cover mitigated about 60% of anticipated price swings in 2025, while supplier consolidation and JIT adjustments cut procurement inflation impact by an estimated 8–10%.

Interest rate environment and capital expenditure

Monetary policy shifts in China and major markets like the US raise borrowing costs for industrial expansion; China's 1-year LPR rose to 3.95% in 2025 vs 3.65% in 2023, tightening capital for buyers of heavy machinery. Higher global rates have dampened demand for forging equipment, with China heavy machinery sales down ~6% YoY in 2024. Conversely, targeted low-rate loans and a 2024 government R&D subsidy package (RMB 120bn) support SPMC’s internal R&D and facility upgrades.

Currency exchange rate volatility

As SPMC conducts significant international trade, Renminbi volatility versus the USD and euro—which saw a roughly 6% depreciation vs USD in 2023–2024 and swings of ±3% in 2025—directly affects price competitiveness. RMB weakness can boost exports but raised imported-tech and raw-material costs; China imported $2.8 trillion goods in 2024. SPMC must hedge forex exposure (forwards, options, natural hedges) to protect margins.

Industrial automation and labor cost trends

Rising labor costs in coastal hubs—average manufacturing wages up about 6–8% y/y in 2024 to roughly CNY 95,000 per worker—push Shanghai Prime Machinery to accelerate automation to protect margins.

SPMC must balance higher pay for skilled technicians (premium ~20–30% vs general staff) with CAPEX for robotics; China industrial robot installations rose 12% in 2024, signaling heavier capital intensity.

Shift to capital-intensive methods increases upfront CAPEX but cuts labor share of costs; firms report 5–15% unit cost reductions after automation rollouts within 18–24 months.

- Wages +6–8% (2024); avg CNY 95k

- Technician wage premium 20–30%

- Industrial robot installs +12% (2024)

- Post-automation unit cost cut 5–15%

Domestic infrastructure and construction cycles

The demand for fasteners and bearings is cyclical and tracks China’s real estate and infrastructure investment; fixed-asset investment in property fell 5.9% y/y in 2024 H1, pressuring volumes for Shanghai Prime Machinery (SPMC).

Economic cooling or targeted stimulus in 2024—RMB 800bn local government bond issuance for infrastructure—correlates with SPMC’s sales swings, with construction-related revenue representing ~45% of FY2023 sales.

Diversification into aerospace and automotive, sectors growing 7% and 4.5% respectively in 2024, helps SPMC offset construction volatility and stabilise margins.

- Construction exposure ~45% of revenue

- 2024 H1 property FAI -5.9% y/y

- RMB 800bn 2024 infrastructure bond stimulus

- Aerospace +7% and auto +4.5% growth in 2024

Steel +22% YoY, metals 48% COGS; wages up, RMB volatile, LPR 3.95%

Global steel +22% YoY to Q3 2025; metals = 48% COGS; hedging covered ~60% of 2025 exposure. China 1‑yr LPR 3.95% (2025) vs 3.65% (2023); heavy‑machinery sales -6% YoY (2024). RMB -6% vs USD (2023–24); forex swings ±3% (2025). Wages +6–8% (2024), avg CNY95k; technician premium 20–30%; robot installs +12% (2024); construction revenue ~45%.

| Metric | Value |

|---|---|

| Steel change | +22% Y/Y |

| Metals %COGS | 48% |

| 1‑yr LPR (2025) | 3.95% |

| Wages (avg) | CNY95k (+6–8%) |

Preview Before You Purchase

Shanghai Prime Machinery PESTLE Analysis

The preview shown here is the exact Shanghai Prime Machinery PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real snapshot of the product you’re buying, delivered exactly as shown with no placeholders or surprises. The content, layout, and structure visible here match the file you’ll download immediately after payment. What you see is the finished file you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and tech innovation are shaping Shanghai Prime Machinery's strategic outlook—our concise PESTLE highlights key external drivers and risks to inform smarter decisions. Ready-made for investors and strategists, the full analysis delivers actionable insights, editable formats, and data-driven recommendations. Purchase the complete PESTLE now to unlock the detailed intelligence you need.

Political factors

State-led industrial modernization policy

As of late 2025 the Made in China 2025 roadmap and follow-up industrial upgrade policies continue to prioritize high-end equipment, directing roughly CNY 420 billion in targeted industrial funds in 2024–25; Shanghai Prime Machinery gains from state backing for domestic core-component self-sufficiency and advanced manufacturing capability upgrades.

Geopolitical trade tensions and export barriers

Ongoing China-West trade friction reduced Chinese machinery exports by 9.7% y/y in 2024, pressuring Shanghai Prime Machinery’s fastener shipments; EU and US tariffs plus anti-dumping probes (over 30 ongoing cases in 2023–24) push the firm to reorient toward China’s domestic market and Belt and Road partners, where exports to Southeast Asia rose 14% in 2024; navigating sanctions and bilateral diplomacy is critical to preserve global distribution and ~$120m export revenue streams.

State-owned enterprise reform mandates

As a subsidiary of Shanghai Electric Group, SPMC faces SOE reform mandates that in 2024 targeted RMB 1.5–2.0 trillion in mixed-ownership reforms across central and local SOEs, pushing SPMC toward clearer corporate governance and minority investor protections.

Regulators demand improved board independence and performance metrics; Shanghai Electric reported a 2024 ROE of ~6.8%, prompting internal restructuring to meet state targets for higher market competitiveness.

Political pressure ties efficiency gains to national goals—energy transition and manufacturing upgrades—aligning SPMC’s strategic shifts with China’s 2025 industrial policy and state-directed investment priorities.

Regional stability in manufacturing hubs

Political stability in Shanghai supports SPMC’s manufacturing base; Shanghai reported zero major civil disruptions in 2024 and ranks top 5 in China for business environment, sustaining operations for 90% of local MNCs.

Municipal policies—including a 2025 tax incentive package reducing manufacturing VAT by up to 3 percentage points for advanced equipment—create a predictable regulatory framework that aids investment decisions.

This environment underpins long-term capital deployment and supply-chain reliability: Shanghai’s port handled 43.7 million TEUs in 2024, ensuring resilient inbound/outbound logistics for SPMC.

- Stable local governance: low disruption, high business confidence

- Policy support: VAT cuts and targeted incentives through 2025

- Logistics strength: 43.7M TEUs at Shanghai port (2024)

Belt and Road Initiative integration

The Belt and Road Initiative expansion gives Shanghai Prime Machinery political access to Southeast and Central Asian markets, where BRI commitments total over $1.0 trillion in projects since 2013 and $150–200 billion annually in recent years, supporting demand for industrial tools and fasteners.

Government-backed infrastructure spending in 2023–2025 in BRI corridors rose ~8–12% year-on-year, creating a predictable order pipeline SPMC can target to offset revenue risks from restrictive Western trade regimes.

- BRI projects cumulative financing >$1.0T since 2013

- Annual BRI-related spend ~ $150–200B recently

- Infrastructure spend growth in corridors +8–12% (2023–25)

- Strategic diplomatic ties mitigate Western market losses

Policy Push, Trade Headwinds and BRI Scale Shape SPMC’s 2024–25 Risk-Return Pivot

State support for high-end equipment (CNY 420bn funds 2024–25), trade friction cutting exports 9.7% y/y (2024) and ~30 anti-dumping probes, SOE mixed-ownership reforms (RMB 1.5–2.0tn target 2024), Shanghai port 43.7M TEU (2024), BRI pipeline >$1.0T since 2013 with $150–200B p.a., and municipal VAT cuts (~3ppt) shape SPMC’s political risk and market pivot.

| Metric | Value |

|---|---|

| Targeted industrial funds | CNY 420bn (2024–25) |

| Machinery export change | -9.7% (2024) |

| Port throughput | 43.7M TEU (2024) |

| BRI financing | >$1.0T since 2013; $150–200B p.a. |

| SOE reform target | RMB 1.5–2.0tn (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Shanghai Prime Machinery across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and entrepreneurs in identifying threats, opportunities, and actionable scenarios for strategy, funding, and operational planning.

A concise, visually segmented PESTLE summary of Shanghai Prime Machinery that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and strategic positioning during planning sessions.

Economic factors

Fluctuations in global raw material costs

Fluctuations in global raw material costs — notably a 22% year‑over‑year rise in steel prices through Q3 2025 — sharply pressure Shanghai Prime Machinery’s gross margin, since metals account for roughly 48% of COGS. Commodity-market volatility in 2025 increased input-cost variance by 15% vs 2023, directly eroding operating margins. Effective hedging reduced exposure: SPMC’s futures/forward cover mitigated about 60% of anticipated price swings in 2025, while supplier consolidation and JIT adjustments cut procurement inflation impact by an estimated 8–10%.

Interest rate environment and capital expenditure

Monetary policy shifts in China and major markets like the US raise borrowing costs for industrial expansion; China's 1-year LPR rose to 3.95% in 2025 vs 3.65% in 2023, tightening capital for buyers of heavy machinery. Higher global rates have dampened demand for forging equipment, with China heavy machinery sales down ~6% YoY in 2024. Conversely, targeted low-rate loans and a 2024 government R&D subsidy package (RMB 120bn) support SPMC’s internal R&D and facility upgrades.

Currency exchange rate volatility

As SPMC conducts significant international trade, Renminbi volatility versus the USD and euro—which saw a roughly 6% depreciation vs USD in 2023–2024 and swings of ±3% in 2025—directly affects price competitiveness. RMB weakness can boost exports but raised imported-tech and raw-material costs; China imported $2.8 trillion goods in 2024. SPMC must hedge forex exposure (forwards, options, natural hedges) to protect margins.

Industrial automation and labor cost trends

Rising labor costs in coastal hubs—average manufacturing wages up about 6–8% y/y in 2024 to roughly CNY 95,000 per worker—push Shanghai Prime Machinery to accelerate automation to protect margins.

SPMC must balance higher pay for skilled technicians (premium ~20–30% vs general staff) with CAPEX for robotics; China industrial robot installations rose 12% in 2024, signaling heavier capital intensity.

Shift to capital-intensive methods increases upfront CAPEX but cuts labor share of costs; firms report 5–15% unit cost reductions after automation rollouts within 18–24 months.

- Wages +6–8% (2024); avg CNY 95k

- Technician wage premium 20–30%

- Industrial robot installs +12% (2024)

- Post-automation unit cost cut 5–15%

Domestic infrastructure and construction cycles

The demand for fasteners and bearings is cyclical and tracks China’s real estate and infrastructure investment; fixed-asset investment in property fell 5.9% y/y in 2024 H1, pressuring volumes for Shanghai Prime Machinery (SPMC).

Economic cooling or targeted stimulus in 2024—RMB 800bn local government bond issuance for infrastructure—correlates with SPMC’s sales swings, with construction-related revenue representing ~45% of FY2023 sales.

Diversification into aerospace and automotive, sectors growing 7% and 4.5% respectively in 2024, helps SPMC offset construction volatility and stabilise margins.

- Construction exposure ~45% of revenue

- 2024 H1 property FAI -5.9% y/y

- RMB 800bn 2024 infrastructure bond stimulus

- Aerospace +7% and auto +4.5% growth in 2024

Steel +22% YoY, metals 48% COGS; wages up, RMB volatile, LPR 3.95%

Global steel +22% YoY to Q3 2025; metals = 48% COGS; hedging covered ~60% of 2025 exposure. China 1‑yr LPR 3.95% (2025) vs 3.65% (2023); heavy‑machinery sales -6% YoY (2024). RMB -6% vs USD (2023–24); forex swings ±3% (2025). Wages +6–8% (2024), avg CNY95k; technician premium 20–30%; robot installs +12% (2024); construction revenue ~45%.

| Metric | Value |

|---|---|

| Steel change | +22% Y/Y |

| Metals %COGS | 48% |

| 1‑yr LPR (2025) | 3.95% |

| Wages (avg) | CNY95k (+6–8%) |

Preview Before You Purchase

Shanghai Prime Machinery PESTLE Analysis

The preview shown here is the exact Shanghai Prime Machinery PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real snapshot of the product you’re buying, delivered exactly as shown with no placeholders or surprises. The content, layout, and structure visible here match the file you’ll download immediately after payment. What you see is the finished file you’ll own upon checkout.