PNC Financial Services PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, regulatory pressures, and technological innovation are reshaping PNC Financial Services—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategies. Buy the full PESTLE Analysis to access a detailed, ready-to-use report with actionable insights, data tables, and editable slides for investors, advisors, and executives.

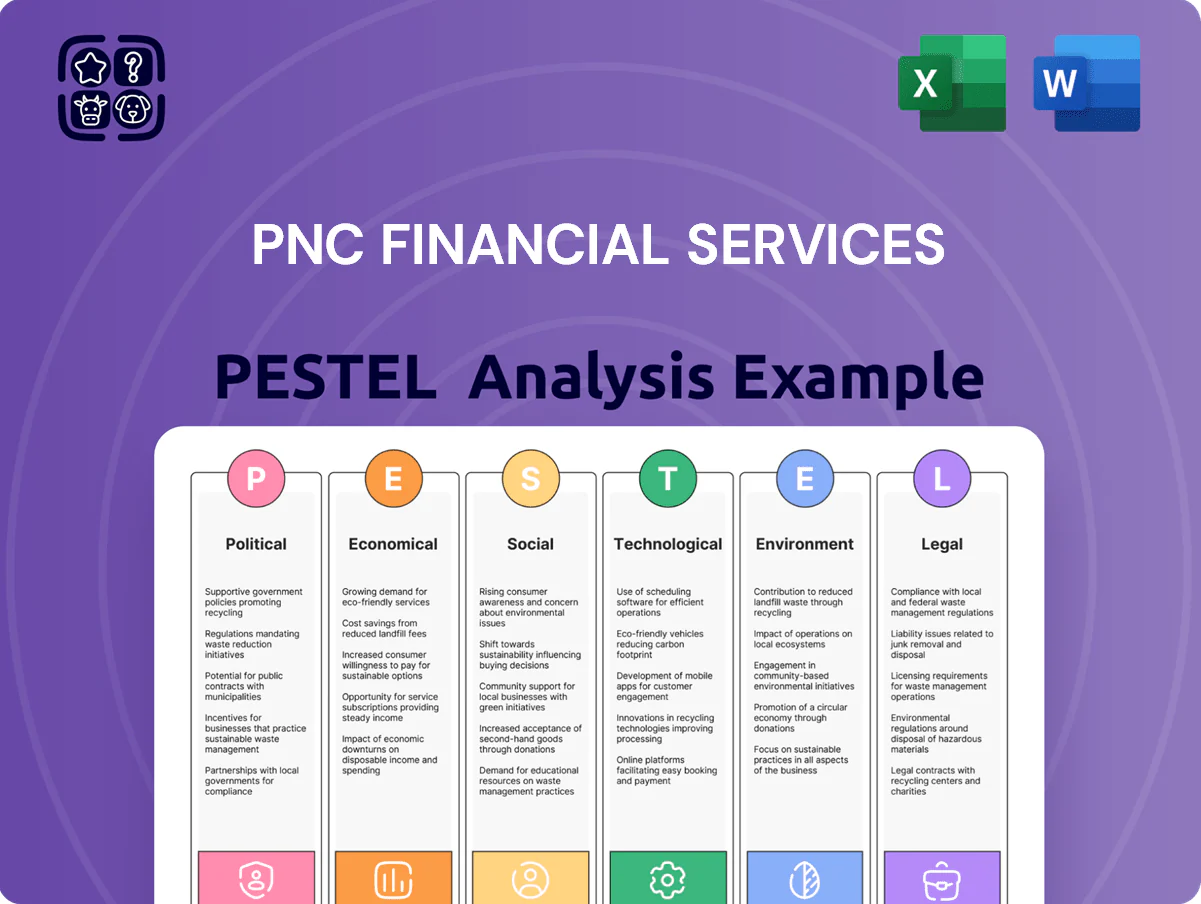

Political factors

Post-Election Regulatory Shifts

Post-2024 election shifts mean federal oversight into 2026 favors deregulation in finance-adjacent sectors while boosting consumer protection enforcement; CFPB budget rose to about $1.6bn in FY2025, increasing exam activity that affects PNC's retail operations.

Administration incentives for domestic manufacturing—$280bn CHIPS/semiconductor-style programs scale—alter corporate lending demand, while proposed corporate tax changes (rate discussions around 21–25%) influence PNC capital planning and NII forecasts.

Geopolitical Stability and Trade Policy

Ongoing international tensions and shifting trade alliances have pushed global borrowing costs higher; US corporate bond yields rose to about 4.8% in 2025, raising capital costs for PNC’s clients and potentially reducing deal activity.

PNC’s primarily domestic footprint masks exposure: 38% of its commercial loan portfolio in 2024 served firms with global supply chains, making creditworthiness sensitive to disruptions and elevating expected loss metrics.

Decisions on tariffs and sanctions—e.g., recent US tariff adjustments in 2024 affecting steel and semiconductor imports—require continuous monitoring to mitigate indirect credit risk and adjust loan loss reserves.

Government Infrastructure Spending

Federal infrastructure and green energy initiatives, including the IIJA and IRA, expand lending opportunities for PNC’s corporate and institutional banking, contributing to its $297 billion total assets (2025) and supporting project financing deals exceeding $8 billion in 2024–25; PNC uses public-private partnership frameworks to fund large-scale transportation and renewable projects across the Eastern and Midwest regions; sustained political support for regional development has helped drive mid-market commercial loan growth, reflected in a 6% annual increase in commercial lending in 2024.

Fiscal Policy and National Debt

Decisions by Congress on the 2025 federal budget and periodic debt-ceiling standoffs drive short-term market volatility and influence Treasury yields; the U.S. 10-year yield rose to ~4.2% in late 2024 amid fiscal uncertainty, affecting rate curves relevant to PNC.

As a major holder of government securities—U.S. Treasuries comprised an estimated 18–22% of large regional bank securities portfolios in 2024—PNC’s balance sheet and liquidity profile are sensitive to shifts in perceived U.S. sovereign risk.

Political gridlock can depress investor confidence and transactional activity, reducing wealth-management AUM growth and advisory fee revenue; during 2023–2024 debt-ceiling episodes, market disruptions correlated with temporary declines in advisory flows and elevated fee compression.

- Congress debt standoffs → higher Treasury yields (~4.2% 10-yr late 2024)

- PNC exposure: government securities significant (~18–22% proxy)

- Gridlock → advisory/AUM volatility and potential fee pressure

State-Level Political Dynamics

PNC faces varying state-level politics that can diverge from federal policy across markets like Pennsylvania, Ohio and Texas, where state legislation on local taxes and banking incentives directly affects branch-level margins; Pennsylvania levied $1.2bn in local tax adjustments in 2024 impacting regional operating costs.

Legislative changes in Ohio and Texas in 2023–2025 produced targeted banking tax credits and municipal incentives that altered loan origination economics and deposit pricing in those states, shifting regional ROI by an estimated 30–80 basis points.

Maintaining robust state government relations is essential for PNC to influence local economic development agendas and preserve branch profitability amid policy shifts that can affect ~40% of its retail footprint and related revenue streams.

- State tax/incentive changes in PA, OH, TX materially impact branch margins

- 2023–2025 state policies shifted regional ROI by ~30–80 bps

- ~40% of PNC retail footprint exposed to state-level policy risk

- Active state government relations required to protect profitability

Regulatory surge, higher yields and state tax shifts reshape regional bank ROI

Political shifts through 2025 raise regulatory exam activity (CFPB ~$1.6bn FY2025), sustain higher Treasury yields (~4.2% 10‑yr late‑2024) and expand infrastructure lending (PNC assets ~$297bn 2025); state tax changes (PA $1.2bn 2024) and targeted credits in OH/TX shifted regional ROI ~30–80 bps, with ~40% retail footprint state‑policy exposed.

| Metric | Value |

|---|---|

| CFPB budget FY2025 | $1.6bn |

| US 10‑yr | ~4.2% |

| PNC assets 2025 | $297bn |

| PA tax change 2024 | $1.2bn |

| Retail footprint exposure | ~40% |

What is included in the product

Explores how macro-environmental factors uniquely affect PNC Financial Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a clean, summarized PESTLE of PNC that’s visually segmented for quick interpretation, easily droppable into presentations or spreadsheets, and editable with notes to align teams and support strategic planning and risk discussions.

Economic factors

Interest Rate Environment and NIM

By end-2025, the Fed’s pivot toward neutral rates helped stabilize PNC’s net interest margin around 3.45%, after peaking near 3.9% in 2023; the shift reduces pressure from repricing but narrows excess spread. The move from a high-rate to moderate-rate environment forces PNC to manage deposit betas—which averaged about 35% in 2024—against loan yields near 5.1%. Maintaining competitive pricing while preserving ROAE targets near 12% remains a core economic challenge.

Inflationary Trends and Operating Costs

While headline U.S. inflation eased to 3.4% in 2024 from 9.1% in 2022, lingering wage growth and higher vendor rates kept PNC’s non-interest expenses elevated, contributing to a 2024 efficiency ratio near 61% (FY 2024).

Regional Economic Disparities

PNC’s heavy footprint across the Rust Belt and Sun Belt exposes it to divergent recovery rates: 2024 Q4 employment growth in the Southeast averaged 2.8% year-over-year versus 0.9% in Midwest metro areas, and population gains in Sun Belt metros exceeded 1.2% annually while Rust Belt counties contracted or stagnated.

PNC reported 2025 regional loan growth of about 5.1% in Southeast branches versus 0.8% in Midwest branches, reflecting migration-driven mortgage and small-business demand.

The bank adapts underwriting, raising stress-test loss rates by ~60–120 basis points for slower Midwest industries while loosening parameters in high-growth Sun Belt corridors to optimize portfolio risk-adjusted returns.

Consumer Credit Quality and Debt Levels

Economic pressures like high housing costs and ongoing student loan repayments have strained household budgets, contributing to elevated but manageable retail delinquency—PNC reported a consumer NCO rate of 0.45% and a 30+ day delinquency ratio near 1.2% in FY2025.

PNC closely monitors employment and spending; job gains through late 2025 (U.S. unemployment ≈ 3.7%) helped stabilize asset quality, enabling calibrated increases in provision for credit losses to $2.1B in 2025.

- Consumer NCO rate ~0.45% (FY2025)

- 30+ day delinquency ~1.2% (FY2025)

- Provision for credit losses $2.1B (2025)

- U.S. unemployment ≈ 3.7% (late 2025)

Capital Market Volatility

Fluctuations in equity and fixed-income markets directly affect PNC’s asset management and fee income; in 2025 market volatility pushed PNC’s noninterest income swing by over $1.2 billion year-over-year, highlighting sensitivity to asset flows.

Economic uncertainty reduces corporate banking deal flow, with US M&A value falling ~18% in 2024 vs 2023, pressuring PNC’s advisory revenues tied to transaction volumes.

PNC mitigates market cycles via a diversified revenue mix—retail banking, treasury services, and commercial lending together comprised ~72% of 2024 net revenue, offsetting capital markets downturns.

- 2025 noninterest-income swing ≈ $1.2B

- US M&A value down ~18% in 2024

- Diversified mix: ~72% of 2024 net revenue from retail/treasury/commercial

PNC: Fed pivot lifts NIM to 3.45% — ROAE target 12% amid cost pressures

Fed pivot to neutral stabilized NIM ~3.45% (2025) while deposit beta ~35% vs loan yields ~5.1%; ROAE target ~12%. Inflation eased to 3.4% (2024) but pushed FY2024 efficiency ratio ~61%; PNC's consumer NCO ~0.45% and 30+ delinq ~1.2% (FY2025); provision for credit losses $2.1B (2025); noninterest-income swing ~$1.2B (2025).

| Metric | Value |

|---|---|

| NIM (2025) | 3.45% |

| Deposit beta (2024) | 35% |

| Loan yields | 5.1% |

| Efficiency ratio (FY2024) | 61% |

| Consumer NCO (FY2025) | 0.45% |

| 30+ delinq (FY2025) | 1.2% |

| Provision (2025) | $2.1B |

| Noninterest-income swing (2025) | $1.2B |

Full Version Awaits

PNC Financial Services PESTLE Analysis

The preview shown here is the exact PESTLE Analysis for PNC Financial Services you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, regulatory pressures, and technological innovation are reshaping PNC Financial Services—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategies. Buy the full PESTLE Analysis to access a detailed, ready-to-use report with actionable insights, data tables, and editable slides for investors, advisors, and executives.

Political factors

Post-Election Regulatory Shifts

Post-2024 election shifts mean federal oversight into 2026 favors deregulation in finance-adjacent sectors while boosting consumer protection enforcement; CFPB budget rose to about $1.6bn in FY2025, increasing exam activity that affects PNC's retail operations.

Administration incentives for domestic manufacturing—$280bn CHIPS/semiconductor-style programs scale—alter corporate lending demand, while proposed corporate tax changes (rate discussions around 21–25%) influence PNC capital planning and NII forecasts.

Geopolitical Stability and Trade Policy

Ongoing international tensions and shifting trade alliances have pushed global borrowing costs higher; US corporate bond yields rose to about 4.8% in 2025, raising capital costs for PNC’s clients and potentially reducing deal activity.

PNC’s primarily domestic footprint masks exposure: 38% of its commercial loan portfolio in 2024 served firms with global supply chains, making creditworthiness sensitive to disruptions and elevating expected loss metrics.

Decisions on tariffs and sanctions—e.g., recent US tariff adjustments in 2024 affecting steel and semiconductor imports—require continuous monitoring to mitigate indirect credit risk and adjust loan loss reserves.

Government Infrastructure Spending

Federal infrastructure and green energy initiatives, including the IIJA and IRA, expand lending opportunities for PNC’s corporate and institutional banking, contributing to its $297 billion total assets (2025) and supporting project financing deals exceeding $8 billion in 2024–25; PNC uses public-private partnership frameworks to fund large-scale transportation and renewable projects across the Eastern and Midwest regions; sustained political support for regional development has helped drive mid-market commercial loan growth, reflected in a 6% annual increase in commercial lending in 2024.

Fiscal Policy and National Debt

Decisions by Congress on the 2025 federal budget and periodic debt-ceiling standoffs drive short-term market volatility and influence Treasury yields; the U.S. 10-year yield rose to ~4.2% in late 2024 amid fiscal uncertainty, affecting rate curves relevant to PNC.

As a major holder of government securities—U.S. Treasuries comprised an estimated 18–22% of large regional bank securities portfolios in 2024—PNC’s balance sheet and liquidity profile are sensitive to shifts in perceived U.S. sovereign risk.

Political gridlock can depress investor confidence and transactional activity, reducing wealth-management AUM growth and advisory fee revenue; during 2023–2024 debt-ceiling episodes, market disruptions correlated with temporary declines in advisory flows and elevated fee compression.

- Congress debt standoffs → higher Treasury yields (~4.2% 10-yr late 2024)

- PNC exposure: government securities significant (~18–22% proxy)

- Gridlock → advisory/AUM volatility and potential fee pressure

State-Level Political Dynamics

PNC faces varying state-level politics that can diverge from federal policy across markets like Pennsylvania, Ohio and Texas, where state legislation on local taxes and banking incentives directly affects branch-level margins; Pennsylvania levied $1.2bn in local tax adjustments in 2024 impacting regional operating costs.

Legislative changes in Ohio and Texas in 2023–2025 produced targeted banking tax credits and municipal incentives that altered loan origination economics and deposit pricing in those states, shifting regional ROI by an estimated 30–80 basis points.

Maintaining robust state government relations is essential for PNC to influence local economic development agendas and preserve branch profitability amid policy shifts that can affect ~40% of its retail footprint and related revenue streams.

- State tax/incentive changes in PA, OH, TX materially impact branch margins

- 2023–2025 state policies shifted regional ROI by ~30–80 bps

- ~40% of PNC retail footprint exposed to state-level policy risk

- Active state government relations required to protect profitability

Regulatory surge, higher yields and state tax shifts reshape regional bank ROI

Political shifts through 2025 raise regulatory exam activity (CFPB ~$1.6bn FY2025), sustain higher Treasury yields (~4.2% 10‑yr late‑2024) and expand infrastructure lending (PNC assets ~$297bn 2025); state tax changes (PA $1.2bn 2024) and targeted credits in OH/TX shifted regional ROI ~30–80 bps, with ~40% retail footprint state‑policy exposed.

| Metric | Value |

|---|---|

| CFPB budget FY2025 | $1.6bn |

| US 10‑yr | ~4.2% |

| PNC assets 2025 | $297bn |

| PA tax change 2024 | $1.2bn |

| Retail footprint exposure | ~40% |

What is included in the product

Explores how macro-environmental factors uniquely affect PNC Financial Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a clean, summarized PESTLE of PNC that’s visually segmented for quick interpretation, easily droppable into presentations or spreadsheets, and editable with notes to align teams and support strategic planning and risk discussions.

Economic factors

Interest Rate Environment and NIM

By end-2025, the Fed’s pivot toward neutral rates helped stabilize PNC’s net interest margin around 3.45%, after peaking near 3.9% in 2023; the shift reduces pressure from repricing but narrows excess spread. The move from a high-rate to moderate-rate environment forces PNC to manage deposit betas—which averaged about 35% in 2024—against loan yields near 5.1%. Maintaining competitive pricing while preserving ROAE targets near 12% remains a core economic challenge.

Inflationary Trends and Operating Costs

While headline U.S. inflation eased to 3.4% in 2024 from 9.1% in 2022, lingering wage growth and higher vendor rates kept PNC’s non-interest expenses elevated, contributing to a 2024 efficiency ratio near 61% (FY 2024).

Regional Economic Disparities

PNC’s heavy footprint across the Rust Belt and Sun Belt exposes it to divergent recovery rates: 2024 Q4 employment growth in the Southeast averaged 2.8% year-over-year versus 0.9% in Midwest metro areas, and population gains in Sun Belt metros exceeded 1.2% annually while Rust Belt counties contracted or stagnated.

PNC reported 2025 regional loan growth of about 5.1% in Southeast branches versus 0.8% in Midwest branches, reflecting migration-driven mortgage and small-business demand.

The bank adapts underwriting, raising stress-test loss rates by ~60–120 basis points for slower Midwest industries while loosening parameters in high-growth Sun Belt corridors to optimize portfolio risk-adjusted returns.

Consumer Credit Quality and Debt Levels

Economic pressures like high housing costs and ongoing student loan repayments have strained household budgets, contributing to elevated but manageable retail delinquency—PNC reported a consumer NCO rate of 0.45% and a 30+ day delinquency ratio near 1.2% in FY2025.

PNC closely monitors employment and spending; job gains through late 2025 (U.S. unemployment ≈ 3.7%) helped stabilize asset quality, enabling calibrated increases in provision for credit losses to $2.1B in 2025.

- Consumer NCO rate ~0.45% (FY2025)

- 30+ day delinquency ~1.2% (FY2025)

- Provision for credit losses $2.1B (2025)

- U.S. unemployment ≈ 3.7% (late 2025)

Capital Market Volatility

Fluctuations in equity and fixed-income markets directly affect PNC’s asset management and fee income; in 2025 market volatility pushed PNC’s noninterest income swing by over $1.2 billion year-over-year, highlighting sensitivity to asset flows.

Economic uncertainty reduces corporate banking deal flow, with US M&A value falling ~18% in 2024 vs 2023, pressuring PNC’s advisory revenues tied to transaction volumes.

PNC mitigates market cycles via a diversified revenue mix—retail banking, treasury services, and commercial lending together comprised ~72% of 2024 net revenue, offsetting capital markets downturns.

- 2025 noninterest-income swing ≈ $1.2B

- US M&A value down ~18% in 2024

- Diversified mix: ~72% of 2024 net revenue from retail/treasury/commercial

PNC: Fed pivot lifts NIM to 3.45% — ROAE target 12% amid cost pressures

Fed pivot to neutral stabilized NIM ~3.45% (2025) while deposit beta ~35% vs loan yields ~5.1%; ROAE target ~12%. Inflation eased to 3.4% (2024) but pushed FY2024 efficiency ratio ~61%; PNC's consumer NCO ~0.45% and 30+ delinq ~1.2% (FY2025); provision for credit losses $2.1B (2025); noninterest-income swing ~$1.2B (2025).

| Metric | Value |

|---|---|

| NIM (2025) | 3.45% |

| Deposit beta (2024) | 35% |

| Loan yields | 5.1% |

| Efficiency ratio (FY2024) | 61% |

| Consumer NCO (FY2025) | 0.45% |

| 30+ delinq (FY2025) | 1.2% |

| Provision (2025) | $2.1B |

| Noninterest-income swing (2025) | $1.2B |

Full Version Awaits

PNC Financial Services PESTLE Analysis

The preview shown here is the exact PESTLE Analysis for PNC Financial Services you’ll receive after purchase—fully formatted, professionally structured, and ready to use.