TXNM Energy Porter's Five Forces Analysis

From Overview to Strategy Blueprint

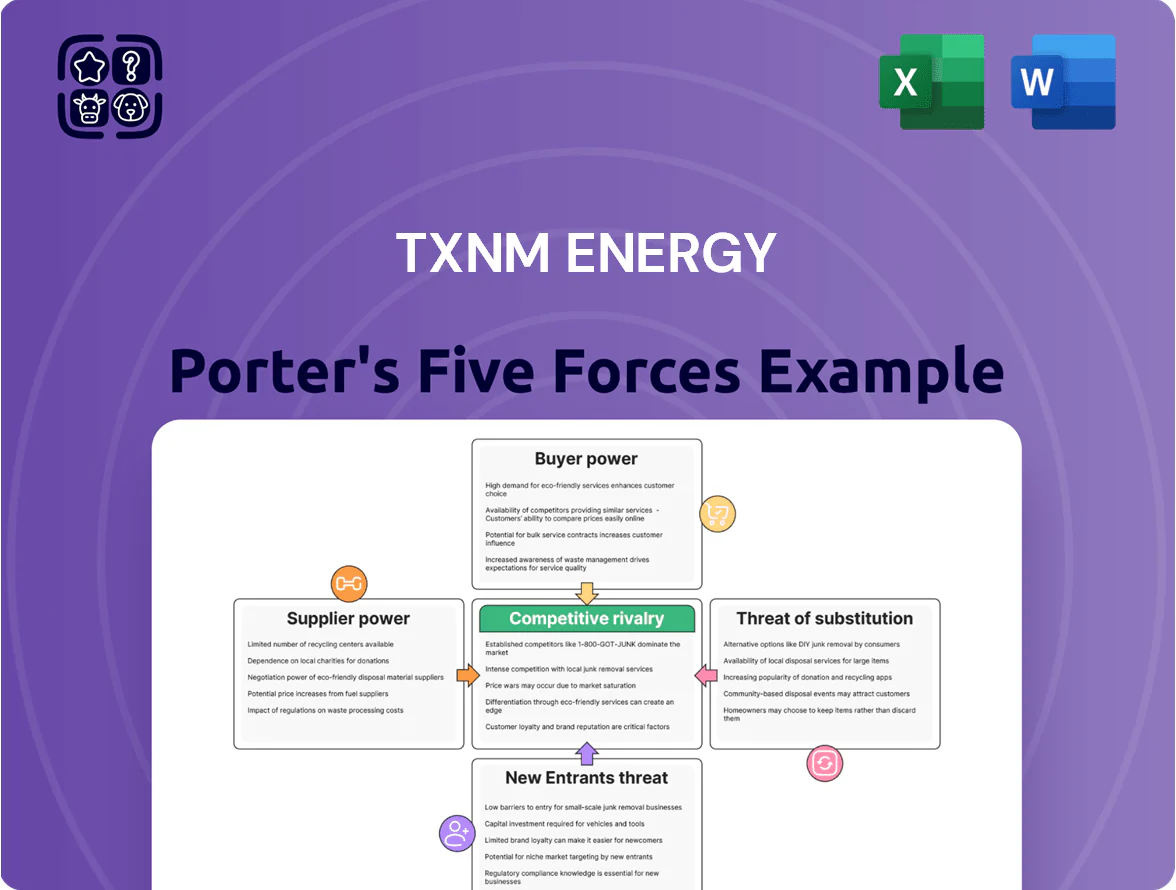

TXNM Energy faces intense competitive rivalry from integrated majors, growing buyer leverage amid commodity-sensitive pricing, and moderate supplier power tied to specialized tech and materials; regulatory shifts and clean-energy substitutes raise the threat of disruption while barriers to entry remain mixed due to capital intensity but advancing modular tech. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore TXNM Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility and Supply Chains

TXNM relies heavily on natural gas and purchased power while adding renewables; natural gas suppliers hold moderate bargaining power because prices track Henry Hub and regional indices, not single contracts.

By late 2025 PNM (Public Service Company of New Mexico) cut spot exposure via multi-year contracts and hedges covering ~60% of 2026 gas needs, lowering short-term price risk.

Still, TXNM remains exposed to supply-chain shocks for turbines, transformers, and semiconductors—global lead times hit 18–30 months in 2024–25, raising outage and capex risk.

Renewable Energy Infrastructure Vendors

As PNM pushes toward 100% carbon-free energy by 2040, it depends heavily on specialized vendors for solar panels, wind turbines, and battery storage, increasing supplier leverage.

National demand for clean-tech rose 22% in 2024, giving suppliers pricing power; utility-scale battery pack prices fell ~15% since 2020 but remain concentrated among 3–5 high-capacity manufacturers.

Limited competition lets these firms enforce firm pricing and strict delivery windows—PNM risked a 6–9 month procurement delay in 2023 when a major supplier capacity hit constraints.

Skilled Labor and Specialized Contractors

The utility sector faces a tight market for specialized electrical engineers and certified technicians needed for grid modernization; US Bureau of Labor Statistics projects 2024–34 6% growth for electrical engineers and shortages in skilled technicians. Labor unions and niche contractors hold high bargaining power since their expertise ensures regulatory compliance and safety, so TXNM (formerly PNM Resources after 2023 reorg) must offer competitive wages—industry median for senior grid engineers ~120,000–140,000 USD—and strong benefits to staff large 2024–2026 capital projects.

Transmission and Distribution Equipment Providers

Suppliers of high-voltage transformers and specialized grid software are concentrated among a few global firms (e.g., Siemens, ABB, GE), which kept lead times at 12–30 months through 2025, boosting supplier leverage in pricing and delivery terms.

PNM must plan multi-year procurement and make advance payments—often 20–40% upfront—to secure units vital for reliability, raising capex timing risk and working-capital needs.

- Few global suppliers (Siemens, ABB, GE)

- Lead times 12–30 months (through 2025)

- Advance payments 20–40% common

- Increases capex timing risk, working-capital strain

Regulatory and Environmental Compliance Services

Third-party environmental consultants and carbon-monitoring tech firms are essential for complying with New Mexico’s Energy Transition Act, creating a captive supplier market since these services are legally required for operation.

PNM faces low switching flexibility because regulators demand consistent, long-term emissions data; contracts often span 3–7 years and can cost $1–5m annually for large utilities.

Concentrated suppliers, long lead times and high upfronts squeeze project timelines and costs

Suppliers exert moderate–high power: fuel indexed to Henry Hub reduces single-supplier leverage, but concentrated vendors for turbines, transformers, batteries, and compliance services, 12–30 month lead times, 20–40% upfront payments, and labor shortages (senior grid engineer median $120k–$140k) raise price and delivery risk.

| Metric | Value |

|---|---|

| Lead times | 12–30 months (2024–25) |

| Upfront payments | 20–40% |

| Battery makers | 3–5 firms |

| Engineer median pay | $120k–$140k |

What is included in the product

Tailored Porter's Five Forces for TXNM Energy, revealing competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic barriers that shape pricing, profitability, and market positioning.

TXNM Energy Porter's Five Forces condensed into a one-sheet snapshot—rapidly assess competitive intensity and pinpoint strategic levers to relieve pricing, supply, and entry pressures.

Customers Bargaining Power

Regulatory Oversight by the NMPRC

The New Mexico Public Regulation Commission (NMPRC) sets rates for PNM, effectively standing in for residential customers who cannot individually negotiate prices; in 2024 the NMPRC approved a PNM revenue increase of about $143 million, limiting the utility’s ability to raise rates unilaterally. By reviewing cost-of-service and return-on-equity filings, the commission shifts bargaining power from TXNM Energy/PNM to a state-governed body representing public interest.

Industrial and Large Commercial Demand

Large industrial clients like data centers and manufacturers wield strong bargaining power at TXNM Energy, consuming 40–60% of site load while representing under 10% of customers; they demand bespoke SLAs and paid demand-response programs to cut costs. In 2024, corporate relocation threats rose as industrial electricity tariffs exceeded $0.10–0.12/kWh in some markets, pushing firms toward on-site cogeneration or PPAs covering 20–50% of needs.

Adoption of Distributed Energy Resources

The rise in residential rooftop solar and home batteries gave customers more control, cutting average residential consumption from utilities; U.S. residential solar capacity grew ~25% in 2024, and New Mexico installations rose ~30% year-over-year, lowering revenue per household for PNM (Public Service Company of New Mexico) by an estimated 3–6% in 2024 vs 2021. This shifts bargaining power to consumers and forces TXNM Energy to add services—grid services, DER management, time-of-use rates—to retain revenue and stay relevant.

Community Choice Aggregation Trends

Increasing interest in New Mexico for Community Choice Aggregation (CCA) means municipalities may pool demand to secure lower rates or greener mixes; New Mexico had 18 municipal energy initiatives and CCA pilots by late 2025, signaling rising threat to incumbents.

Although not yet universal, potential CCAs pressure PNM to match pricing and clean-energy offerings; PNM’s 2024 average residential rate was about 12.3 cents/kWh, so even modest CCA discounts of 5–10% could shift load.

This collective bargaining acts as a check on TXNM Energy’s long-term plans, forcing faster emissions reductions and tariff competitiveness to avoid customer migration.

- 18 municipal initiatives/CCA pilots by 2025

- PNM 2024 avg residential rate ~12.3 cents/kWh

- 5–10% CCA price gap could drive migration

Customer Sensitivity to Rate Hikes

Public sentiment and New Mexico’s weak 2024-25 economic growth (GDP +0.8% in 2024) makes customers highly sensitive to utility bill increases; median household income in 2023 was $56,000, so even $5–10 monthly hikes draw complaints.

Organized groups like the New Mexico Utility Shareholders Alliance and NMPRC intervened in >30% of PNM rate dockets in 2022–24, routinely challenging capital spend requests.

That sustained public pressure constrains PNM’s ability to pass transition costs fully to customers; recent approved rate increases averaged 3.1% vs. requested 6–8%, showing pushback effects.

- Median income $56,000 (2023)

- NM GDP growth +0.8% (2024)

- Approved rate hikes 3.1% vs requested 6–8%

- Intervention in >30% of dockets (2022–24)

Customers' Rising Leverage Cuts PNM's Raise as Solar, CCAs & Industrials Bite

Customers hold moderate-to-strong bargaining power: NMPRC rate oversight capped PNM’s 2024 approved increase (~$143M), large industrials consume 40–60% of site load and threaten relocations when tariffs exceed $0.10–0.12/kWh, residential solar grew ~30% in NM (2024) cutting utility revenue 3–6%, and 18 CCA pilots by 2025 plus public push limited approved hikes to ~3.1% vs 6–8% requested.

| Metric | Value |

|---|---|

| PNM 2024 approved increase | $143M |

| Industrial site load | 40–60% |

| NM residential solar growth 2024 | ~30% |

| Approved vs requested hikes | 3.1% vs 6–8% |

| CCA pilots (by 2025) | 18 |

What You See Is What You Get

TXNM Energy Porter's Five Forces Analysis

This preview shows the exact TXNM Energy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes. You're viewing the final deliverable you will get instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

TXNM Energy faces intense competitive rivalry from integrated majors, growing buyer leverage amid commodity-sensitive pricing, and moderate supplier power tied to specialized tech and materials; regulatory shifts and clean-energy substitutes raise the threat of disruption while barriers to entry remain mixed due to capital intensity but advancing modular tech. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore TXNM Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility and Supply Chains

TXNM relies heavily on natural gas and purchased power while adding renewables; natural gas suppliers hold moderate bargaining power because prices track Henry Hub and regional indices, not single contracts.

By late 2025 PNM (Public Service Company of New Mexico) cut spot exposure via multi-year contracts and hedges covering ~60% of 2026 gas needs, lowering short-term price risk.

Still, TXNM remains exposed to supply-chain shocks for turbines, transformers, and semiconductors—global lead times hit 18–30 months in 2024–25, raising outage and capex risk.

Renewable Energy Infrastructure Vendors

As PNM pushes toward 100% carbon-free energy by 2040, it depends heavily on specialized vendors for solar panels, wind turbines, and battery storage, increasing supplier leverage.

National demand for clean-tech rose 22% in 2024, giving suppliers pricing power; utility-scale battery pack prices fell ~15% since 2020 but remain concentrated among 3–5 high-capacity manufacturers.

Limited competition lets these firms enforce firm pricing and strict delivery windows—PNM risked a 6–9 month procurement delay in 2023 when a major supplier capacity hit constraints.

Skilled Labor and Specialized Contractors

The utility sector faces a tight market for specialized electrical engineers and certified technicians needed for grid modernization; US Bureau of Labor Statistics projects 2024–34 6% growth for electrical engineers and shortages in skilled technicians. Labor unions and niche contractors hold high bargaining power since their expertise ensures regulatory compliance and safety, so TXNM (formerly PNM Resources after 2023 reorg) must offer competitive wages—industry median for senior grid engineers ~120,000–140,000 USD—and strong benefits to staff large 2024–2026 capital projects.

Transmission and Distribution Equipment Providers

Suppliers of high-voltage transformers and specialized grid software are concentrated among a few global firms (e.g., Siemens, ABB, GE), which kept lead times at 12–30 months through 2025, boosting supplier leverage in pricing and delivery terms.

PNM must plan multi-year procurement and make advance payments—often 20–40% upfront—to secure units vital for reliability, raising capex timing risk and working-capital needs.

- Few global suppliers (Siemens, ABB, GE)

- Lead times 12–30 months (through 2025)

- Advance payments 20–40% common

- Increases capex timing risk, working-capital strain

Regulatory and Environmental Compliance Services

Third-party environmental consultants and carbon-monitoring tech firms are essential for complying with New Mexico’s Energy Transition Act, creating a captive supplier market since these services are legally required for operation.

PNM faces low switching flexibility because regulators demand consistent, long-term emissions data; contracts often span 3–7 years and can cost $1–5m annually for large utilities.

Concentrated suppliers, long lead times and high upfronts squeeze project timelines and costs

Suppliers exert moderate–high power: fuel indexed to Henry Hub reduces single-supplier leverage, but concentrated vendors for turbines, transformers, batteries, and compliance services, 12–30 month lead times, 20–40% upfront payments, and labor shortages (senior grid engineer median $120k–$140k) raise price and delivery risk.

| Metric | Value |

|---|---|

| Lead times | 12–30 months (2024–25) |

| Upfront payments | 20–40% |

| Battery makers | 3–5 firms |

| Engineer median pay | $120k–$140k |

What is included in the product

Tailored Porter's Five Forces for TXNM Energy, revealing competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic barriers that shape pricing, profitability, and market positioning.

TXNM Energy Porter's Five Forces condensed into a one-sheet snapshot—rapidly assess competitive intensity and pinpoint strategic levers to relieve pricing, supply, and entry pressures.

Customers Bargaining Power

Regulatory Oversight by the NMPRC

The New Mexico Public Regulation Commission (NMPRC) sets rates for PNM, effectively standing in for residential customers who cannot individually negotiate prices; in 2024 the NMPRC approved a PNM revenue increase of about $143 million, limiting the utility’s ability to raise rates unilaterally. By reviewing cost-of-service and return-on-equity filings, the commission shifts bargaining power from TXNM Energy/PNM to a state-governed body representing public interest.

Industrial and Large Commercial Demand

Large industrial clients like data centers and manufacturers wield strong bargaining power at TXNM Energy, consuming 40–60% of site load while representing under 10% of customers; they demand bespoke SLAs and paid demand-response programs to cut costs. In 2024, corporate relocation threats rose as industrial electricity tariffs exceeded $0.10–0.12/kWh in some markets, pushing firms toward on-site cogeneration or PPAs covering 20–50% of needs.

Adoption of Distributed Energy Resources

The rise in residential rooftop solar and home batteries gave customers more control, cutting average residential consumption from utilities; U.S. residential solar capacity grew ~25% in 2024, and New Mexico installations rose ~30% year-over-year, lowering revenue per household for PNM (Public Service Company of New Mexico) by an estimated 3–6% in 2024 vs 2021. This shifts bargaining power to consumers and forces TXNM Energy to add services—grid services, DER management, time-of-use rates—to retain revenue and stay relevant.

Community Choice Aggregation Trends

Increasing interest in New Mexico for Community Choice Aggregation (CCA) means municipalities may pool demand to secure lower rates or greener mixes; New Mexico had 18 municipal energy initiatives and CCA pilots by late 2025, signaling rising threat to incumbents.

Although not yet universal, potential CCAs pressure PNM to match pricing and clean-energy offerings; PNM’s 2024 average residential rate was about 12.3 cents/kWh, so even modest CCA discounts of 5–10% could shift load.

This collective bargaining acts as a check on TXNM Energy’s long-term plans, forcing faster emissions reductions and tariff competitiveness to avoid customer migration.

- 18 municipal initiatives/CCA pilots by 2025

- PNM 2024 avg residential rate ~12.3 cents/kWh

- 5–10% CCA price gap could drive migration

Customer Sensitivity to Rate Hikes

Public sentiment and New Mexico’s weak 2024-25 economic growth (GDP +0.8% in 2024) makes customers highly sensitive to utility bill increases; median household income in 2023 was $56,000, so even $5–10 monthly hikes draw complaints.

Organized groups like the New Mexico Utility Shareholders Alliance and NMPRC intervened in >30% of PNM rate dockets in 2022–24, routinely challenging capital spend requests.

That sustained public pressure constrains PNM’s ability to pass transition costs fully to customers; recent approved rate increases averaged 3.1% vs. requested 6–8%, showing pushback effects.

- Median income $56,000 (2023)

- NM GDP growth +0.8% (2024)

- Approved rate hikes 3.1% vs requested 6–8%

- Intervention in >30% of dockets (2022–24)

Customers' Rising Leverage Cuts PNM's Raise as Solar, CCAs & Industrials Bite

Customers hold moderate-to-strong bargaining power: NMPRC rate oversight capped PNM’s 2024 approved increase (~$143M), large industrials consume 40–60% of site load and threaten relocations when tariffs exceed $0.10–0.12/kWh, residential solar grew ~30% in NM (2024) cutting utility revenue 3–6%, and 18 CCA pilots by 2025 plus public push limited approved hikes to ~3.1% vs 6–8% requested.

| Metric | Value |

|---|---|

| PNM 2024 approved increase | $143M |

| Industrial site load | 40–60% |

| NM residential solar growth 2024 | ~30% |

| Approved vs requested hikes | 3.1% vs 6–8% |

| CCA pilots (by 2025) | 18 |

What You See Is What You Get

TXNM Energy Porter's Five Forces Analysis

This preview shows the exact TXNM Energy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes. You're viewing the final deliverable you will get instantly after payment.