Poly Developments & Holdings Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

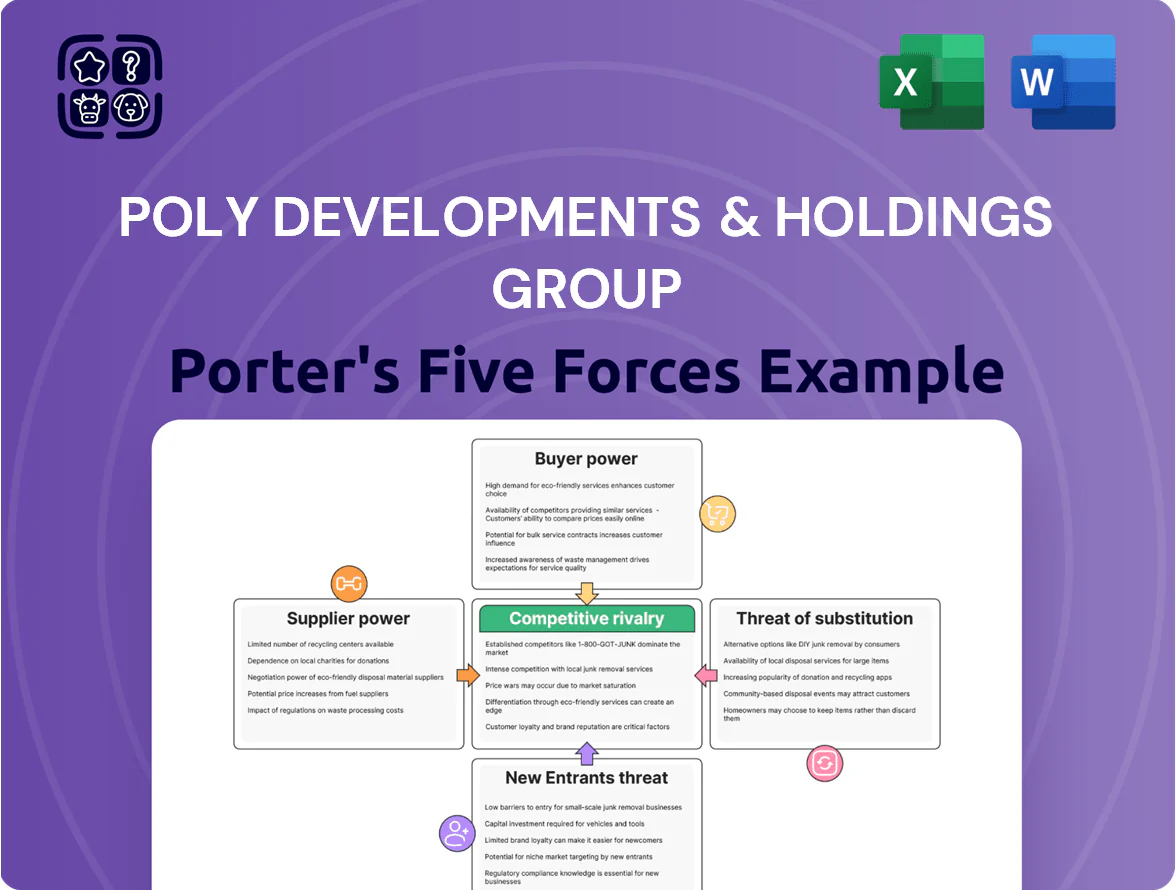

Poly Developments & Holdings faces moderate supplier and buyer power, high competitive rivalry in China's property sector, and evolving threats from new entrants and substitutes driven by policy and market shifts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Poly Developments & Holdings Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Land Reserves

As a state-owned enterprise, Poly Developments benefits from preferential land acquisition via government auctions and urban renewal, securing ~30–40% more provincial-level parcels than private peers in 2024, per China Land Market data.

The primary supplier is the Chinese government, which tightly controls land supply and pricing to cool markets; national land transfer revenues fell 12% in 2024, showing policy leverage.

Poly’s alignment with national urban plans grants it steadier access and lower bid competition in earmarked redevelopment zones, reducing site acquisition volatility versus private rivals.

Construction Material Costs

Suppliers of cement, steel and aggregates remain fragmented but exposed to global commodity swings—steel jumped ~18% in 2021–24 and cement input costs rose ~12% CAGR to 2024. Poly Developments uses scale—¥350bn+ procurement in 2024—to secure bulk contracts and hedges, lowering supplier leverage. By end‑2025 Poly reported 28% of materials from integrated subsidiaries and long‑term purchase agreements, stabilizing costs amid 3.5% inflation.

Financing and Capital Providers

State-backed banks and institutional investors are key capital suppliers for Poly Developments & Holdings Group; as of 2024 Poly’s net debt was about CNY 160 billion and SOE status helped secure cheaper funding, with average borrowing cost reported near 4.2% vs ~6% for private peers in 2023.

Labor Market Dynamics

- 8% avg wage growth 2024

- Contractors shift cost risk to Poly

- Prefab 12–15% of starts 2024

- On-site labor hours down ~20% in pilots

Technological and Design Partners

Architectural firms and smart-home tech providers are specialized suppliers that boost value in Poly Developments & Holdings premium projects; as of 2024, green-certified projects grew 18% year-on-year in China, increasing supplier leverage.

Poly counters this by signing multi-year partnerships with top-tier design institutes and tech vendors, locking in innovation and reducing cost volatility—partner contracts reportedly cover ~30% of flagship project inputs.

- Specialized suppliers: higher leverage as green/digital demand rises

- 2024: 18% YoY growth in green-certified projects in China

- Poly uses multi-year partnerships to secure 30% of flagship inputs

Poly's procurement scale and cheap debt offset supplier and wage pressures

Suppliers hold moderate power: government land control and state-bank funding give Poly advantaged access and lower financing costs (CNY160bn net debt; 4.2% avg borrowing cost, 2024), while fragmented materials suppliers and rising labor (8% wage growth, 2024) raise input risk; Poly offsets via ¥350bn+ centralized procurement, 28% internal materials, 12–15% prefab, and multi‑year vendor/design contracts.

| Metric | 2024 / 2025 |

|---|---|

| Net debt | CNY 160bn (2024) |

| Avg borrowing cost | 4.2% (2024) |

| Procurement spend | ¥350bn+ (2024) |

| Internal materials | 28% (end‑2025) |

| Prefab share | 12–15% (2024) |

| Construction wage growth | 8% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Poly Developments & Holdings Group, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Poly Developments—quickly identifies bargaining power, rivalry, and regulatory pressures to streamline strategic decisions.

Customers Bargaining Power

Market Sentiment and Buyer Confidence

Availability of Alternative Options

High inventory in Chinese cities—Beijing 2025 unsold stock ~1.2m sqm, Guangzhou ~0.9m sqm—gives buyers broad choice across developers and projects, boosting customer bargaining power.

Ample supply lets buyers quickly compare price per sqm and amenities; nationwide average new-home discount widened to 8.1% in 2025 Q1, increasing negotiation leverage.

Poly Developments & Holdings (stock 600048.SS) offsets this by prioritizing prime-site projects and rolling out upgraded property management (service fee retention rose 12% y/y in 2024) to sustain premium pricing.

Mortgage Accessibility and Interest Rates

Mortgage accessibility and interest rates drive customer bargaining power: China’s central bank cut its 5-year loan prime rate to 4.20% in Aug 2024, lowering monthly mortgage costs and expanding buyer eligibility, while tighter policy in 2023 halved mortgage approvals in some cities. When credit tightens, Poly reduces prices or adds incentives—sales incentive spend rose 18% in H1 2025—to keep turnover near its target 8–10% monthly inventory sell-through. Poly tracks PBOC policy, LPR moves, and local down-payment rules daily to tune pricing and financing offers.

Digital Transparency and Information

Digital platforms and social media give buyers access to pricing, construction updates, and reviews, cutting information asymmetry and boosting buyer bargaining power; in China, 78% of homebuyers used online listings in 2024 per China Real Estate Association.

That shifts leverage to buyers and makes Poly Developments & Holdings Group brand trust vital; Poly reported CNY 320.4 billion contracted sales in 2024, so reputation directly affects sales velocity.

Poly builds its own digital ecosystem to engage customers and control project narratives, reducing third-party review impact and shortening sales cycles.

- 78% of buyers use online listings (2024 China Real Estate Association)

- Poly contracted sales: CNY 320.4bn (2024)

- Transparency lowers info asymmetry, raises buyer leverage

- Poly’s digital ecosystems aim to manage reputation and speed sales

Demographic Shifts and Demand Quality

Buyers Leaned: Higher Bargaining Power as Discounts, Inventory & Online Listings Rise

Buyers hold high bargaining power: 64% prioritize developer solvency (late 2025), new-home sales down 12% YoY H1 2025, and nationwide discounts averaged 8.1% in 2025 Q1; Poly’s CNY 320.4bn 2024 contracted sales and state backing help, but high inventory (Beijing ~1.2m sqm unsold) and 78% online listing use raise negotiation leverage.

| Metric | Value |

|---|---|

| Poly contracted sales 2024 | CNY 320.4bn |

| New-home sales H1 2025 | −12% YoY |

| Avg new-home discount 2025 Q1 | 8.1% |

| Beijing unsold stock 2025 | ~1.2m sqm |

| Buyers using online listings 2024 | 78% |

Preview the Actual Deliverable

Poly Developments & Holdings Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Poly Developments & Holdings Group you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use. The document covers competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes with concise evidence and implications for strategy and valuation. You’ll get this exact file instantly upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Poly Developments & Holdings faces moderate supplier and buyer power, high competitive rivalry in China's property sector, and evolving threats from new entrants and substitutes driven by policy and market shifts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Poly Developments & Holdings Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Land Reserves

As a state-owned enterprise, Poly Developments benefits from preferential land acquisition via government auctions and urban renewal, securing ~30–40% more provincial-level parcels than private peers in 2024, per China Land Market data.

The primary supplier is the Chinese government, which tightly controls land supply and pricing to cool markets; national land transfer revenues fell 12% in 2024, showing policy leverage.

Poly’s alignment with national urban plans grants it steadier access and lower bid competition in earmarked redevelopment zones, reducing site acquisition volatility versus private rivals.

Construction Material Costs

Suppliers of cement, steel and aggregates remain fragmented but exposed to global commodity swings—steel jumped ~18% in 2021–24 and cement input costs rose ~12% CAGR to 2024. Poly Developments uses scale—¥350bn+ procurement in 2024—to secure bulk contracts and hedges, lowering supplier leverage. By end‑2025 Poly reported 28% of materials from integrated subsidiaries and long‑term purchase agreements, stabilizing costs amid 3.5% inflation.

Financing and Capital Providers

State-backed banks and institutional investors are key capital suppliers for Poly Developments & Holdings Group; as of 2024 Poly’s net debt was about CNY 160 billion and SOE status helped secure cheaper funding, with average borrowing cost reported near 4.2% vs ~6% for private peers in 2023.

Labor Market Dynamics

- 8% avg wage growth 2024

- Contractors shift cost risk to Poly

- Prefab 12–15% of starts 2024

- On-site labor hours down ~20% in pilots

Technological and Design Partners

Architectural firms and smart-home tech providers are specialized suppliers that boost value in Poly Developments & Holdings premium projects; as of 2024, green-certified projects grew 18% year-on-year in China, increasing supplier leverage.

Poly counters this by signing multi-year partnerships with top-tier design institutes and tech vendors, locking in innovation and reducing cost volatility—partner contracts reportedly cover ~30% of flagship project inputs.

- Specialized suppliers: higher leverage as green/digital demand rises

- 2024: 18% YoY growth in green-certified projects in China

- Poly uses multi-year partnerships to secure 30% of flagship inputs

Poly's procurement scale and cheap debt offset supplier and wage pressures

Suppliers hold moderate power: government land control and state-bank funding give Poly advantaged access and lower financing costs (CNY160bn net debt; 4.2% avg borrowing cost, 2024), while fragmented materials suppliers and rising labor (8% wage growth, 2024) raise input risk; Poly offsets via ¥350bn+ centralized procurement, 28% internal materials, 12–15% prefab, and multi‑year vendor/design contracts.

| Metric | 2024 / 2025 |

|---|---|

| Net debt | CNY 160bn (2024) |

| Avg borrowing cost | 4.2% (2024) |

| Procurement spend | ¥350bn+ (2024) |

| Internal materials | 28% (end‑2025) |

| Prefab share | 12–15% (2024) |

| Construction wage growth | 8% YoY (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Poly Developments & Holdings Group, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Poly Developments—quickly identifies bargaining power, rivalry, and regulatory pressures to streamline strategic decisions.

Customers Bargaining Power

Market Sentiment and Buyer Confidence

Availability of Alternative Options

High inventory in Chinese cities—Beijing 2025 unsold stock ~1.2m sqm, Guangzhou ~0.9m sqm—gives buyers broad choice across developers and projects, boosting customer bargaining power.

Ample supply lets buyers quickly compare price per sqm and amenities; nationwide average new-home discount widened to 8.1% in 2025 Q1, increasing negotiation leverage.

Poly Developments & Holdings (stock 600048.SS) offsets this by prioritizing prime-site projects and rolling out upgraded property management (service fee retention rose 12% y/y in 2024) to sustain premium pricing.

Mortgage Accessibility and Interest Rates

Mortgage accessibility and interest rates drive customer bargaining power: China’s central bank cut its 5-year loan prime rate to 4.20% in Aug 2024, lowering monthly mortgage costs and expanding buyer eligibility, while tighter policy in 2023 halved mortgage approvals in some cities. When credit tightens, Poly reduces prices or adds incentives—sales incentive spend rose 18% in H1 2025—to keep turnover near its target 8–10% monthly inventory sell-through. Poly tracks PBOC policy, LPR moves, and local down-payment rules daily to tune pricing and financing offers.

Digital Transparency and Information

Digital platforms and social media give buyers access to pricing, construction updates, and reviews, cutting information asymmetry and boosting buyer bargaining power; in China, 78% of homebuyers used online listings in 2024 per China Real Estate Association.

That shifts leverage to buyers and makes Poly Developments & Holdings Group brand trust vital; Poly reported CNY 320.4 billion contracted sales in 2024, so reputation directly affects sales velocity.

Poly builds its own digital ecosystem to engage customers and control project narratives, reducing third-party review impact and shortening sales cycles.

- 78% of buyers use online listings (2024 China Real Estate Association)

- Poly contracted sales: CNY 320.4bn (2024)

- Transparency lowers info asymmetry, raises buyer leverage

- Poly’s digital ecosystems aim to manage reputation and speed sales

Demographic Shifts and Demand Quality

Buyers Leaned: Higher Bargaining Power as Discounts, Inventory & Online Listings Rise

Buyers hold high bargaining power: 64% prioritize developer solvency (late 2025), new-home sales down 12% YoY H1 2025, and nationwide discounts averaged 8.1% in 2025 Q1; Poly’s CNY 320.4bn 2024 contracted sales and state backing help, but high inventory (Beijing ~1.2m sqm unsold) and 78% online listing use raise negotiation leverage.

| Metric | Value |

|---|---|

| Poly contracted sales 2024 | CNY 320.4bn |

| New-home sales H1 2025 | −12% YoY |

| Avg new-home discount 2025 Q1 | 8.1% |

| Beijing unsold stock 2025 | ~1.2m sqm |

| Buyers using online listings 2024 | 78% |

Preview the Actual Deliverable

Poly Developments & Holdings Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Poly Developments & Holdings Group you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use. The document covers competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes with concise evidence and implications for strategy and valuation. You’ll get this exact file instantly upon payment.