Poly Property Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

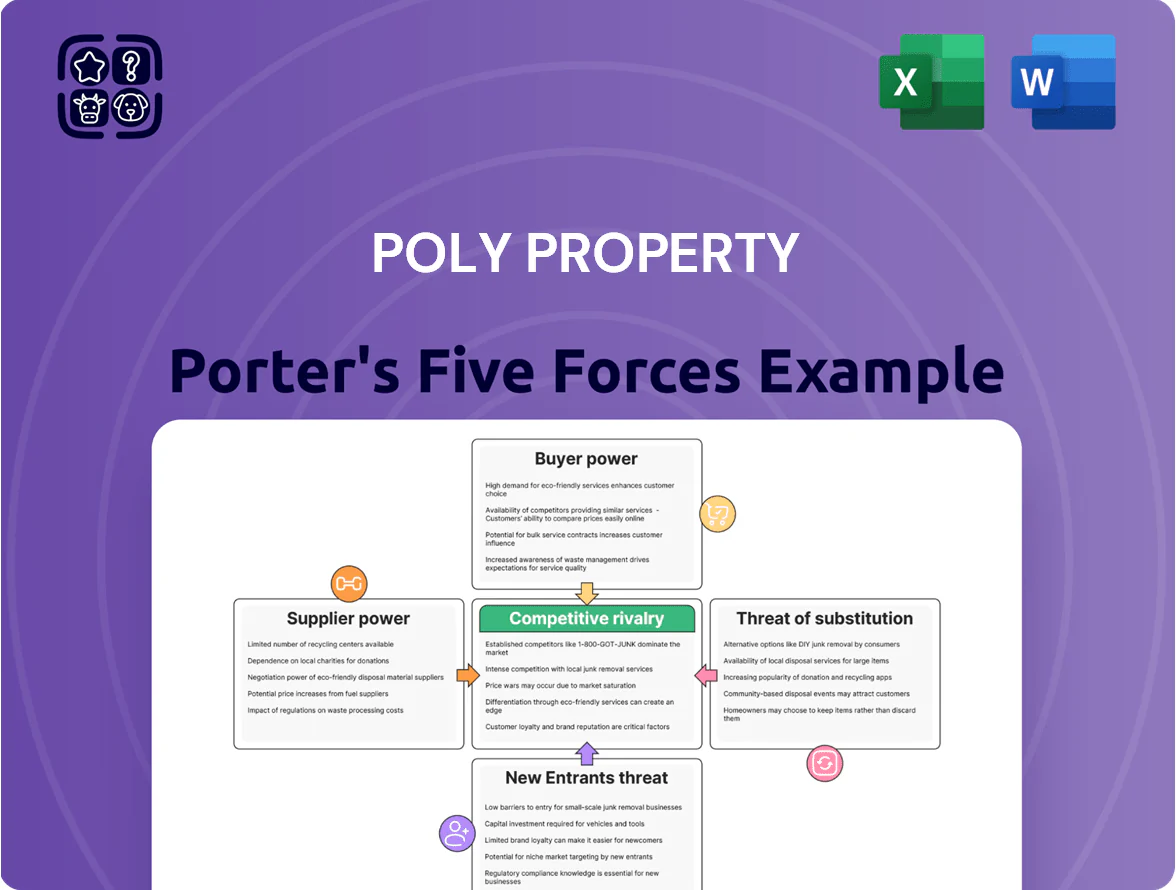

Poly Property faces moderate buyer power, cyclical demand and consolidation-driven supplier leverage, plus substantial barriers for new entrants but rising substitute risks from REITs and PropTech; competitive intensity hinges on land access and financing conditions. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy tailored to Poly Property.

Suppliers Bargaining Power

Government Control of Land Supply

The primary supplier for Poly Property is the Chinese government, which holds a monopoly on land auctions and urban planning; by Dec 2025 land quotas were tightened nationwide to curb speculation, keeping primary land transactions down ~15% y/y in 2024–25. As a state-linked developer Poly often wins priority plots, but rigid pricing floors and zoning rules limit its bargaining power and cap margin upside on new projects.

Construction Material Cost Volatility

Suppliers of steel, cement, and glass hold moderate power as global commodity volatility and China’s tighter environmental rules push prices; steel HRC rose ~12% year-on-year in 2025 while cement saw regional spikes to +8% in northern provinces.

Supply-chain resilience improved after 2023, but green materials inflation remains: low-carbon cement premiums average 10–20% higher in 2025.

Poly Property limits supplier power via multi-year procurement deals and bulk buying—group purchasing accounted for ~22% cost reduction on major projects in 2024, delivering strong economies of scale.

Access to Financial Capital

Financial institutions and bond markets are key capital suppliers; their pricing is shaped by China’s monetary policy and the Three Red Lines limits introduced in 2020. Poly Property, as a state-owned enterprise, raised onshore bonds at ~3.6% average yield in 2024 versus ~6–8% for private peers, cutting its funding cost and weakening lenders’ bargaining power. This gap lets Poly negotiate better terms and reduces lender leverage compared with smaller, non-state-backed developers.

Labor Market Shortages

The construction sector in China faces a shrinking skilled labor pool: workers aged 16–59 fell 3.5% between 2015–2020 and urban service jobs rose 7% by 2023, boosting bargaining power of labor contractors and specialist engineering firms to demand 10–15% higher rates in 2024.

Poly Property must scale prefabrication and on-site automation: prefabrication can cut labor hours by ~30% and capex for modular lines averages CNY 120–250m per plant, lowering long-term margin pressure.

- Skilled labor down 3.5% (2015–2020)

- Service jobs +7% (to 2023)

- Contractor wage premium +10–15% (2024)

- Prefab reduces labor hours ~30%

- Modular plant capex CNY 120–250m

Specialized Architectural and Tech Services

As smart-home and carbon-neutral demand rises, elite architectural and integrated-tech suppliers gain leverage over Poly Property, especially since 42% of luxury developments in 2024 advertised smart systems or net-zero targets.

These niche firms are key to differentiating Poly’s premium residential and commercial products in a crowded market, raising switching costs and margin pressure.

Top sustainable urban-design talent remains scarce — estimated vacancy-to-hire ratio 1.8x in 2024 — strengthening suppliers’ negotiating power.

- 42% of luxury projects (2024) use smart/net-zero specs

- Top-tier designer vacancy-to-hire 1.8x (2024)

- Higher switching costs and margin pressure

Poly's land power capped as costs rise: steel +12%, cement premium 10–20%, prefab saves 30%

Government controls land auctions, capping Poly’s supplier power despite priority access; land transactions down ~15% y/y (2024–25). Commodities and green materials raised costs: steel +12% y/y (2025), low‑carbon cement premium 10–20%. State backing cut funding costs (onshore bonds ~3.6% in 2024), lowering lender leverage. Skilled labor scarcity pushed contractor premiums +10–15% (2024); prefab cuts labor ~30%.

| Item | Metric |

|---|---|

| Land transactions | -15% y/y (2024–25) |

| Steel HRC | +12% (2025) |

| Low‑carbon cement premium | 10–20% (2025) |

| Onshore bond yield | 3.6% avg (Poly, 2024) |

| Contractor wage premium | +10–15% (2024) |

| Prefab labor cut | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for Poly Property that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats, with strategic commentary to inform pricing, positioning, and defensive moves.

A concise, one-sheet Porter's Five Forces for Poly Property—quickly gauges competitive pressure and highlights relief strategies to streamline boardroom decisions.

Customers Bargaining Power

Buyer Sensitivity to Interest Rates

Individual buyers in 2025 are highly sensitive to mortgage rates and People’s Bank of China policy shifts; a 100bp rise in mortgage rates cuts buyer affordability by about 8–10%, per industry estimates, directly lowering demand. After years of speculative excess, Chinese buyers now prioritize value and quality, pushing Poly Property to offer sharper pricing and premium finishes. This buyer conservatism increases customer leverage, squeezing margins and lengthening sales cycles for Poly.

Institutional Tenant Demands

Institutional tenants in Poly Property’s office portfolio push for flexible leases and premium amenities, leveraging a 2024 Shanghai Grade-A vacancy near 18% and rising incentives averaging 15% of first-year rent; this shifts bargaining power to tenants.

With post-pandemic flight-to-quality, tenants pick from surplus Grade-A stock, so Poly must invest in superior property management and digital infrastructure—recent capex benchmarks: HKD 120–200/sqft for smart upgrades—to retain high-value occupants.

Information Transparency and Digital Platforms

The proliferation of real estate data platforms and social media has given buyers clear pricing and peer reviews, and by 2025 sites like Fangdd and Beike report 45% of Chinese homebuyers use online ratings to choose developers. Buyers can now compare Poly Property’s delivery track record against rivals in real time, with Poly’s 2024 average delivery delay rate of 8% visible versus industry 12%. This information symmetry cuts Poly’s ability to charge a brand premium without verifiable construction quality, pressuring margins and pre-sale pricing.

Alternative Residential Options

The rise of government-subsidized rental housing—China added about 5.7 million units in 2024—and a booming secondary home market, which reached RMB 7.4 trillion in transaction volume in 2024, give buyers real alternatives to new launches, capping Poly Property’s pricing power.

Buyers delay purchases, seek promotions, and wait for incentives like down-payment subsidies or tax breaks; in 2024 average discount rates on new launches climbed to ~8%, showing selective buyer behavior that pressures developer margins.

- 5.7M new subsidized units (2024)

- RMB 7.4T secondary market volume (2024)

- Average new-launch discounts ~8% (2024)

Hotel Guest Loyalty and Choice

In luxury hotels, guests face low switching costs and choose among 100s of global and domestic brands; Poly Property must outcompete on service, elite loyalty tiers, and prime locations to win share.

Online travel agencies gave customers 360-degree price transparency by 2024; average luxury booking comparison time is under 6 minutes, boosting guest bargaining power and pressuring room rates and package margins.

- Low switching costs; many rivals

- Compete via service, loyalty, location

- OTAs increase price transparency

- Avg comparison <6 minutes (2024)

Buyers wield pricing power: rates, subsidies and vacancies reshape housing & hospitality

Buyers hold high bargaining power: mortgage-rate sensitivity (100bp rise → −8–10% affordability), 2024 metrics—5.7M subsidized units, RMB7.4T secondary market, ~8% avg new-launch discounts—boost alternatives and delay purchases; tenants demand flexible leases amid ~18% Shanghai Grade-A vacancy and 15% first-year rent incentives; OTA transparency and low hotel switching costs compress room and package margins.

| Metric | 2024/25 |

|---|---|

| Subsidized units added | 5.7M (2024) |

| Secondary market volume | RMB7.4T (2024) |

| New-launch discount avg | ~8% (2024) |

| Shanghai Grade-A vacancy | ~18% (2024) |

| First-year rent incentives | ~15% avg (2024) |

Preview the Actual Deliverable

Poly Property Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Poly Property you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use analysis document delivered instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Poly Property faces moderate buyer power, cyclical demand and consolidation-driven supplier leverage, plus substantial barriers for new entrants but rising substitute risks from REITs and PropTech; competitive intensity hinges on land access and financing conditions. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy tailored to Poly Property.

Suppliers Bargaining Power

Government Control of Land Supply

The primary supplier for Poly Property is the Chinese government, which holds a monopoly on land auctions and urban planning; by Dec 2025 land quotas were tightened nationwide to curb speculation, keeping primary land transactions down ~15% y/y in 2024–25. As a state-linked developer Poly often wins priority plots, but rigid pricing floors and zoning rules limit its bargaining power and cap margin upside on new projects.

Construction Material Cost Volatility

Suppliers of steel, cement, and glass hold moderate power as global commodity volatility and China’s tighter environmental rules push prices; steel HRC rose ~12% year-on-year in 2025 while cement saw regional spikes to +8% in northern provinces.

Supply-chain resilience improved after 2023, but green materials inflation remains: low-carbon cement premiums average 10–20% higher in 2025.

Poly Property limits supplier power via multi-year procurement deals and bulk buying—group purchasing accounted for ~22% cost reduction on major projects in 2024, delivering strong economies of scale.

Access to Financial Capital

Financial institutions and bond markets are key capital suppliers; their pricing is shaped by China’s monetary policy and the Three Red Lines limits introduced in 2020. Poly Property, as a state-owned enterprise, raised onshore bonds at ~3.6% average yield in 2024 versus ~6–8% for private peers, cutting its funding cost and weakening lenders’ bargaining power. This gap lets Poly negotiate better terms and reduces lender leverage compared with smaller, non-state-backed developers.

Labor Market Shortages

The construction sector in China faces a shrinking skilled labor pool: workers aged 16–59 fell 3.5% between 2015–2020 and urban service jobs rose 7% by 2023, boosting bargaining power of labor contractors and specialist engineering firms to demand 10–15% higher rates in 2024.

Poly Property must scale prefabrication and on-site automation: prefabrication can cut labor hours by ~30% and capex for modular lines averages CNY 120–250m per plant, lowering long-term margin pressure.

- Skilled labor down 3.5% (2015–2020)

- Service jobs +7% (to 2023)

- Contractor wage premium +10–15% (2024)

- Prefab reduces labor hours ~30%

- Modular plant capex CNY 120–250m

Specialized Architectural and Tech Services

As smart-home and carbon-neutral demand rises, elite architectural and integrated-tech suppliers gain leverage over Poly Property, especially since 42% of luxury developments in 2024 advertised smart systems or net-zero targets.

These niche firms are key to differentiating Poly’s premium residential and commercial products in a crowded market, raising switching costs and margin pressure.

Top sustainable urban-design talent remains scarce — estimated vacancy-to-hire ratio 1.8x in 2024 — strengthening suppliers’ negotiating power.

- 42% of luxury projects (2024) use smart/net-zero specs

- Top-tier designer vacancy-to-hire 1.8x (2024)

- Higher switching costs and margin pressure

Poly's land power capped as costs rise: steel +12%, cement premium 10–20%, prefab saves 30%

Government controls land auctions, capping Poly’s supplier power despite priority access; land transactions down ~15% y/y (2024–25). Commodities and green materials raised costs: steel +12% y/y (2025), low‑carbon cement premium 10–20%. State backing cut funding costs (onshore bonds ~3.6% in 2024), lowering lender leverage. Skilled labor scarcity pushed contractor premiums +10–15% (2024); prefab cuts labor ~30%.

| Item | Metric |

|---|---|

| Land transactions | -15% y/y (2024–25) |

| Steel HRC | +12% (2025) |

| Low‑carbon cement premium | 10–20% (2025) |

| Onshore bond yield | 3.6% avg (Poly, 2024) |

| Contractor wage premium | +10–15% (2024) |

| Prefab labor cut | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for Poly Property that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats, with strategic commentary to inform pricing, positioning, and defensive moves.

A concise, one-sheet Porter's Five Forces for Poly Property—quickly gauges competitive pressure and highlights relief strategies to streamline boardroom decisions.

Customers Bargaining Power

Buyer Sensitivity to Interest Rates

Individual buyers in 2025 are highly sensitive to mortgage rates and People’s Bank of China policy shifts; a 100bp rise in mortgage rates cuts buyer affordability by about 8–10%, per industry estimates, directly lowering demand. After years of speculative excess, Chinese buyers now prioritize value and quality, pushing Poly Property to offer sharper pricing and premium finishes. This buyer conservatism increases customer leverage, squeezing margins and lengthening sales cycles for Poly.

Institutional Tenant Demands

Institutional tenants in Poly Property’s office portfolio push for flexible leases and premium amenities, leveraging a 2024 Shanghai Grade-A vacancy near 18% and rising incentives averaging 15% of first-year rent; this shifts bargaining power to tenants.

With post-pandemic flight-to-quality, tenants pick from surplus Grade-A stock, so Poly must invest in superior property management and digital infrastructure—recent capex benchmarks: HKD 120–200/sqft for smart upgrades—to retain high-value occupants.

Information Transparency and Digital Platforms

The proliferation of real estate data platforms and social media has given buyers clear pricing and peer reviews, and by 2025 sites like Fangdd and Beike report 45% of Chinese homebuyers use online ratings to choose developers. Buyers can now compare Poly Property’s delivery track record against rivals in real time, with Poly’s 2024 average delivery delay rate of 8% visible versus industry 12%. This information symmetry cuts Poly’s ability to charge a brand premium without verifiable construction quality, pressuring margins and pre-sale pricing.

Alternative Residential Options

The rise of government-subsidized rental housing—China added about 5.7 million units in 2024—and a booming secondary home market, which reached RMB 7.4 trillion in transaction volume in 2024, give buyers real alternatives to new launches, capping Poly Property’s pricing power.

Buyers delay purchases, seek promotions, and wait for incentives like down-payment subsidies or tax breaks; in 2024 average discount rates on new launches climbed to ~8%, showing selective buyer behavior that pressures developer margins.

- 5.7M new subsidized units (2024)

- RMB 7.4T secondary market volume (2024)

- Average new-launch discounts ~8% (2024)

Hotel Guest Loyalty and Choice

In luxury hotels, guests face low switching costs and choose among 100s of global and domestic brands; Poly Property must outcompete on service, elite loyalty tiers, and prime locations to win share.

Online travel agencies gave customers 360-degree price transparency by 2024; average luxury booking comparison time is under 6 minutes, boosting guest bargaining power and pressuring room rates and package margins.

- Low switching costs; many rivals

- Compete via service, loyalty, location

- OTAs increase price transparency

- Avg comparison <6 minutes (2024)

Buyers wield pricing power: rates, subsidies and vacancies reshape housing & hospitality

Buyers hold high bargaining power: mortgage-rate sensitivity (100bp rise → −8–10% affordability), 2024 metrics—5.7M subsidized units, RMB7.4T secondary market, ~8% avg new-launch discounts—boost alternatives and delay purchases; tenants demand flexible leases amid ~18% Shanghai Grade-A vacancy and 15% first-year rent incentives; OTA transparency and low hotel switching costs compress room and package margins.

| Metric | 2024/25 |

|---|---|

| Subsidized units added | 5.7M (2024) |

| Secondary market volume | RMB7.4T (2024) |

| New-launch discount avg | ~8% (2024) |

| Shanghai Grade-A vacancy | ~18% (2024) |

| First-year rent incentives | ~15% avg (2024) |

Preview the Actual Deliverable

Poly Property Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Poly Property you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use analysis document delivered instantly upon payment.