Pool PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our tailored PESTLE Analysis for Pool—revealing how political, economic, social, technological, legal, and environmental forces will shape its trajectory and your decisions; buy the full report for actionable insights, ready-to-use charts, and a downloadable, editable format to accelerate your research and strategy.

Political factors

Trade Tariffs and Global Sourcing

Trade tariffs on imported pool chemicals and equipment raised Pool Corporation's input costs by an estimated 4–6% in 2024–2025, pressuring gross margins as overseas sourcing accounts for roughly 30% of product purchases.

Geopolitical tensions and renegotiated trade deals altered prices for PVC, motors and chemical precursors, contributing to a reported 5.2% year-over-year increase in supply chain costs in FY2025.

Management is adjusting procurement, reallocating inventory and passing selective price increases to support 16,000+ retailer and builder customers while targeting margin recovery toward historical levels.

Local Zoning and Permitting Regulations

Municipal decisions on residential land use and pool permits directly affect installation volumes; for example, U.S. single-family permit trends—up 3.2% in 2024 to 1.2M units—signal regional pool demand shifts. Local political changes can tighten zoning or speed approvals for outdoor living spaces, affecting sales cycles and margins. Pool Corporation tracks permitting and zoning across states to forecast demand for construction products and adjust inventory and capex planning accordingly.

Labor Policy and Workforce Availability

Federal and state labor regulations — including 2024 minimum wage increases in 27 states (e.g., CA $16.00, NY $15.00–$15.00+) and evolving independent contractor rules after state-level gig reforms — raise labor costs and tighten skilled technician supply for the pool industry.

For Pool Corporation customers, higher wages and reclassification risks increase installation and service payroll expenses; Bureau of Labor Statistics 2024 shows construction employment up ~2.5% year-over-year, tightening labor markets and raising hourly wage pressure.

These political shifts compress margins in service and installation segments, raising operating costs that can reduce profit margins for dealers and installers who drive Pool Corporation’s parts and equipment revenue.

Infrastructure and Urban Planning

Government investment in community recreation and public health infrastructure bolstered demand for commercial-grade pool equipment; US public recreation capital outlays rose to $40.6B in 2023, supporting municipal pool projects that favor wholesale suppliers.

Urban planning emphasizing green spaces and community pools—over 1,200 new municipal aquatic projects funded via 2022–2024 grants—creates growth channels for distributors.

Pool Corporation aligns inventory to private development and public works specifications, with commercial segment revenues contributing roughly 18% of 2024 net sales.

- Public recreation spending $40.6B (2023)

- ~1,200 municipal aquatic projects funded (2022–2024)

- PoolCorp commercial revenues ~18% of 2024 net sales

International Trade Stability

As a global distributor, Pool Corporation is highly sensitive to stability of international shipping routes and diplomatic relations; in 2024, global container rates rose 18% year-over-year during regional disruptions, increasing logistics spend for distributors.

Political unrest in manufacturing or transit hubs—evidenced by 2023–24 factory shutdowns in Southeast Asia that delayed shipments by an average of 12–20 days—can disrupt Pool’s supply chain and raise costs.

Maintaining a diversified supplier base across North America, Europe, and Asia reduces single-source exposure and is a strategic necessity to mitigate risks from geopolitical volatility.

- 2024 container rate +18% YoY

- 2023–24 shipment delays 12–20 days

- Diversified suppliers across NA, EU, ASIA

Rising costs and robust municipal spending boost commercial pool demand

Trade tariffs and supply-chain disruptions raised input costs ~4–6% in 2024–25 while container rates rose 18% YoY; labor and wage hikes in 27 states increased installation payrolls amid construction employment +2.5% (2024). Municipal recreation outlays $40.6B (2023) and ~1,200 aquatic projects (2022–24) support commercial demand (~18% of 2024 sales).

| Metric | Value |

|---|---|

| Tariff impact | 4–6% input cost increase |

| Container rates | +18% YoY (2024) |

| Construction employment | +2.5% (2024) |

| Public recreation spend | $40.6B (2023) |

| Municipal pool projects | ~1,200 (2022–24) |

| Commercial revenue share | ~18% (2024) |

What is included in the product

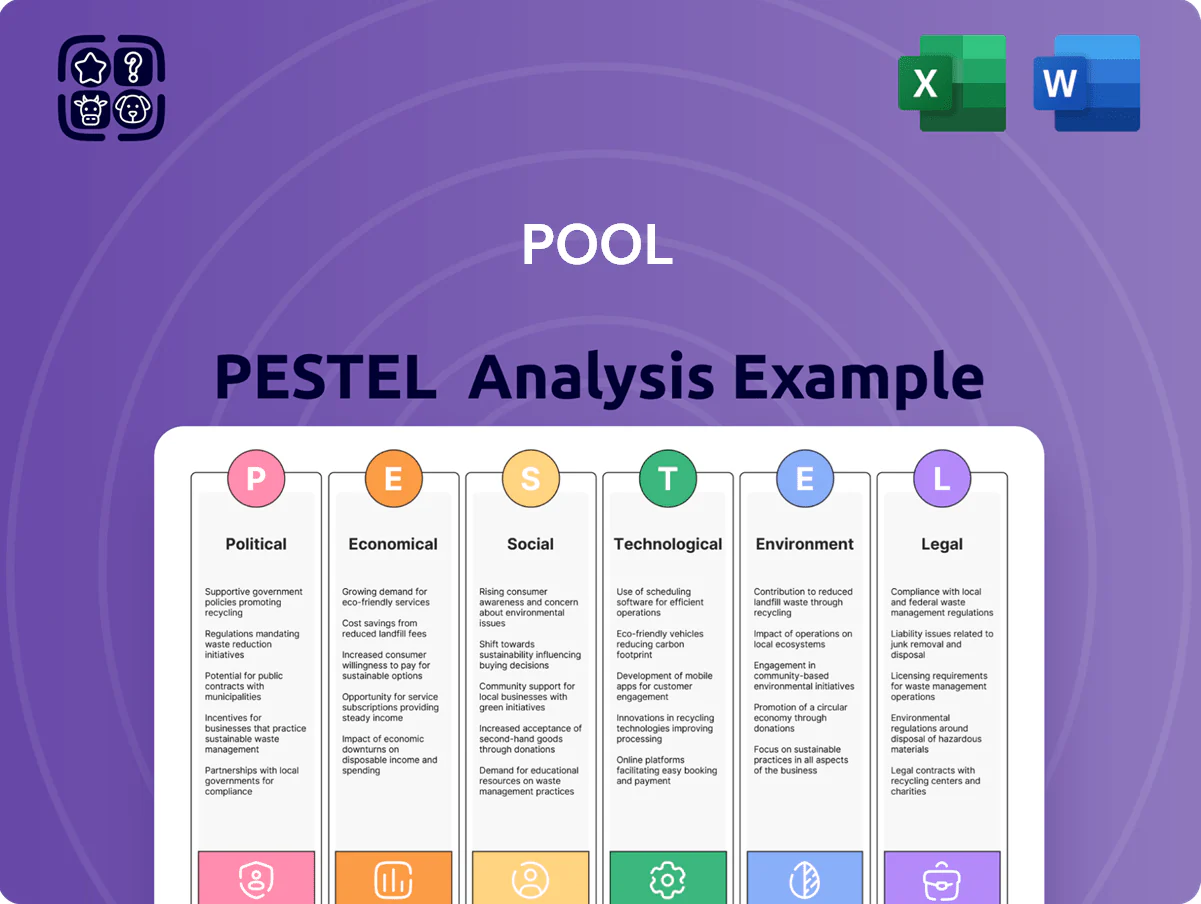

Explores how external macro-environmental factors uniquely affect the Pool across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trend analysis to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, visually segmented PESTLE summary that’s easy to drop into presentations or share across teams for quick alignment on external risks and market positioning.

Economic factors

Interest Rate Fluctuations

The trajectory of interest rates through 2025 is a primary driver for new pool construction and large-scale remodels; the Fed's 2024 terminal rate near 5.25–5.50% and markets pricing a 2025 easing to ~4.5% will shape buyer behavior. High borrowing costs—average 30-year fixed mortgage ~7.1% in 2024—can deter homeowners from financing major backyard projects, reducing demand for concrete, liners, and equipment. Conversely, a stable or declining rate environment encourages long-term investment in residential leisure infrastructure, boosting multi-year planning and supplier order books.

Housing Market Dynamics

Housing market strength directly affects Pool Corporation: US existing-home sales rose 3.0% in 2024 vs 2023 and median existing-home price hit $388,300 in 2024, boosting homeowner equity and discretionary spend on pool upgrades. Higher turnover rates increase replacement demand for pumps, liners and heaters; NA pool equipment sales grew ~6% in 2024 as remodeling activity rose. Robust real estate supports both retrofit and new-install revenues, correlating with PoolCorp’s FY2024 revenue growth of 9.4%.

Consumer Discretionary Income

Spending on pool supplies and outdoor living closely tracks disposable income; US real disposable personal income fell 0.9% annually in 2024 Q3, pressuring non-essential purchases.

During downturns consumers delay maintenance and luxury items—home improvement spending dropped 4.2% YoY in 2024, signaling risk to pool accessory demand.

Pool Corporation depends on middle/upper-class stability: top 40% households account for roughly 70% of discretionary spend, making their employment and wage trends critical.

Inflationary Pressure on Raw Materials

Persistent inflation raised global chemical and resin prices by ~12% in 2023–2024, increasing costs for pool equipment makers; metals rose ~8% in 2024, squeezing margins.

Pool Corporation must weigh passing costs to dealers while keeping wholesale pricing competitive—its 2024 gross margin of ~27% reflects this pressure.

Improved inventory turns, hedging and bulk purchasing reduced cost volatility exposure; strategic sourcing saved peers an estimated 3–5% on COGS in 2024.

- Raw material inflation: chemicals +12% (2023–24), metals +8% (2024)

- Pool Corp 2024 gross margin ~27% under pressure

- Inventory/hedging can cut COGS volatility ~3–5%

Energy Costs and Operational Expenses

Fluctuating energy prices raise operating costs for distribution centers and long-haul transport of heavy pool equipment; U.S. diesel averaged about 4.00 USD/gal in 2025 Q4 versus 3.70 USD/gal in 2024, increasing per-trip fuel spend by ~8–10% for typical routes.

Higher fuel costs drive shipping surcharges that can suppress demand for frequent deliveries, with surveys showing 22% of commercial buyers delay nonurgent shipments when surcharges rise.

Efficient logistics, route optimization, and fuel-management programs—often cutting fuel use 10–15%—are essential to preserve the company’s industry-leading distribution network.

- Diesel ≈ 4.00 USD/gal (2025 Q4); +8–10% per-trip fuel cost vs 2024

- 22% of buyers delay nonurgent shipments when surcharges rise

- Logistics/fuel programs can reduce fuel use 10–15%

PoolCorp margins buoyed by high rates, resilient housing and fuel/raw material swings

Interest rates, housing strength, inflation and fuel costs drove PoolCorp demand and margins in 2024–25: mortgage ~7.1% (2024), existing‑home median $388,300 (2024), raw materials +12% (chemicals) / +8% (metals), gross margin ~27% (2024), diesel ~4.00 USD/gal (2025 Q4), inventory/hedge savings 3–5%, logistics fuel reduction 10–15%.

| Metric | Value |

|---|---|

| Mortgage (2024) | ~7.1% |

| Median home price (2024) | $388,300 |

| Chemicals (2023–24) | +12% |

| Metals (2024) | +8% |

| PoolCorp gross margin (2024) | ~27% |

| Diesel (2025 Q4) | $4.00/gal |

| Inventory hedge savings | 3–5% |

| Fuel programs | 10–15% |

Full Version Awaits

Pool PESTLE Analysis

The preview shown here is the exact Pool PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our tailored PESTLE Analysis for Pool—revealing how political, economic, social, technological, legal, and environmental forces will shape its trajectory and your decisions; buy the full report for actionable insights, ready-to-use charts, and a downloadable, editable format to accelerate your research and strategy.

Political factors

Trade Tariffs and Global Sourcing

Trade tariffs on imported pool chemicals and equipment raised Pool Corporation's input costs by an estimated 4–6% in 2024–2025, pressuring gross margins as overseas sourcing accounts for roughly 30% of product purchases.

Geopolitical tensions and renegotiated trade deals altered prices for PVC, motors and chemical precursors, contributing to a reported 5.2% year-over-year increase in supply chain costs in FY2025.

Management is adjusting procurement, reallocating inventory and passing selective price increases to support 16,000+ retailer and builder customers while targeting margin recovery toward historical levels.

Local Zoning and Permitting Regulations

Municipal decisions on residential land use and pool permits directly affect installation volumes; for example, U.S. single-family permit trends—up 3.2% in 2024 to 1.2M units—signal regional pool demand shifts. Local political changes can tighten zoning or speed approvals for outdoor living spaces, affecting sales cycles and margins. Pool Corporation tracks permitting and zoning across states to forecast demand for construction products and adjust inventory and capex planning accordingly.

Labor Policy and Workforce Availability

Federal and state labor regulations — including 2024 minimum wage increases in 27 states (e.g., CA $16.00, NY $15.00–$15.00+) and evolving independent contractor rules after state-level gig reforms — raise labor costs and tighten skilled technician supply for the pool industry.

For Pool Corporation customers, higher wages and reclassification risks increase installation and service payroll expenses; Bureau of Labor Statistics 2024 shows construction employment up ~2.5% year-over-year, tightening labor markets and raising hourly wage pressure.

These political shifts compress margins in service and installation segments, raising operating costs that can reduce profit margins for dealers and installers who drive Pool Corporation’s parts and equipment revenue.

Infrastructure and Urban Planning

Government investment in community recreation and public health infrastructure bolstered demand for commercial-grade pool equipment; US public recreation capital outlays rose to $40.6B in 2023, supporting municipal pool projects that favor wholesale suppliers.

Urban planning emphasizing green spaces and community pools—over 1,200 new municipal aquatic projects funded via 2022–2024 grants—creates growth channels for distributors.

Pool Corporation aligns inventory to private development and public works specifications, with commercial segment revenues contributing roughly 18% of 2024 net sales.

- Public recreation spending $40.6B (2023)

- ~1,200 municipal aquatic projects funded (2022–2024)

- PoolCorp commercial revenues ~18% of 2024 net sales

International Trade Stability

As a global distributor, Pool Corporation is highly sensitive to stability of international shipping routes and diplomatic relations; in 2024, global container rates rose 18% year-over-year during regional disruptions, increasing logistics spend for distributors.

Political unrest in manufacturing or transit hubs—evidenced by 2023–24 factory shutdowns in Southeast Asia that delayed shipments by an average of 12–20 days—can disrupt Pool’s supply chain and raise costs.

Maintaining a diversified supplier base across North America, Europe, and Asia reduces single-source exposure and is a strategic necessity to mitigate risks from geopolitical volatility.

- 2024 container rate +18% YoY

- 2023–24 shipment delays 12–20 days

- Diversified suppliers across NA, EU, ASIA

Rising costs and robust municipal spending boost commercial pool demand

Trade tariffs and supply-chain disruptions raised input costs ~4–6% in 2024–25 while container rates rose 18% YoY; labor and wage hikes in 27 states increased installation payrolls amid construction employment +2.5% (2024). Municipal recreation outlays $40.6B (2023) and ~1,200 aquatic projects (2022–24) support commercial demand (~18% of 2024 sales).

| Metric | Value |

|---|---|

| Tariff impact | 4–6% input cost increase |

| Container rates | +18% YoY (2024) |

| Construction employment | +2.5% (2024) |

| Public recreation spend | $40.6B (2023) |

| Municipal pool projects | ~1,200 (2022–24) |

| Commercial revenue share | ~18% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Pool across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trend analysis to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, visually segmented PESTLE summary that’s easy to drop into presentations or share across teams for quick alignment on external risks and market positioning.

Economic factors

Interest Rate Fluctuations

The trajectory of interest rates through 2025 is a primary driver for new pool construction and large-scale remodels; the Fed's 2024 terminal rate near 5.25–5.50% and markets pricing a 2025 easing to ~4.5% will shape buyer behavior. High borrowing costs—average 30-year fixed mortgage ~7.1% in 2024—can deter homeowners from financing major backyard projects, reducing demand for concrete, liners, and equipment. Conversely, a stable or declining rate environment encourages long-term investment in residential leisure infrastructure, boosting multi-year planning and supplier order books.

Housing Market Dynamics

Housing market strength directly affects Pool Corporation: US existing-home sales rose 3.0% in 2024 vs 2023 and median existing-home price hit $388,300 in 2024, boosting homeowner equity and discretionary spend on pool upgrades. Higher turnover rates increase replacement demand for pumps, liners and heaters; NA pool equipment sales grew ~6% in 2024 as remodeling activity rose. Robust real estate supports both retrofit and new-install revenues, correlating with PoolCorp’s FY2024 revenue growth of 9.4%.

Consumer Discretionary Income

Spending on pool supplies and outdoor living closely tracks disposable income; US real disposable personal income fell 0.9% annually in 2024 Q3, pressuring non-essential purchases.

During downturns consumers delay maintenance and luxury items—home improvement spending dropped 4.2% YoY in 2024, signaling risk to pool accessory demand.

Pool Corporation depends on middle/upper-class stability: top 40% households account for roughly 70% of discretionary spend, making their employment and wage trends critical.

Inflationary Pressure on Raw Materials

Persistent inflation raised global chemical and resin prices by ~12% in 2023–2024, increasing costs for pool equipment makers; metals rose ~8% in 2024, squeezing margins.

Pool Corporation must weigh passing costs to dealers while keeping wholesale pricing competitive—its 2024 gross margin of ~27% reflects this pressure.

Improved inventory turns, hedging and bulk purchasing reduced cost volatility exposure; strategic sourcing saved peers an estimated 3–5% on COGS in 2024.

- Raw material inflation: chemicals +12% (2023–24), metals +8% (2024)

- Pool Corp 2024 gross margin ~27% under pressure

- Inventory/hedging can cut COGS volatility ~3–5%

Energy Costs and Operational Expenses

Fluctuating energy prices raise operating costs for distribution centers and long-haul transport of heavy pool equipment; U.S. diesel averaged about 4.00 USD/gal in 2025 Q4 versus 3.70 USD/gal in 2024, increasing per-trip fuel spend by ~8–10% for typical routes.

Higher fuel costs drive shipping surcharges that can suppress demand for frequent deliveries, with surveys showing 22% of commercial buyers delay nonurgent shipments when surcharges rise.

Efficient logistics, route optimization, and fuel-management programs—often cutting fuel use 10–15%—are essential to preserve the company’s industry-leading distribution network.

- Diesel ≈ 4.00 USD/gal (2025 Q4); +8–10% per-trip fuel cost vs 2024

- 22% of buyers delay nonurgent shipments when surcharges rise

- Logistics/fuel programs can reduce fuel use 10–15%

PoolCorp margins buoyed by high rates, resilient housing and fuel/raw material swings

Interest rates, housing strength, inflation and fuel costs drove PoolCorp demand and margins in 2024–25: mortgage ~7.1% (2024), existing‑home median $388,300 (2024), raw materials +12% (chemicals) / +8% (metals), gross margin ~27% (2024), diesel ~4.00 USD/gal (2025 Q4), inventory/hedge savings 3–5%, logistics fuel reduction 10–15%.

| Metric | Value |

|---|---|

| Mortgage (2024) | ~7.1% |

| Median home price (2024) | $388,300 |

| Chemicals (2023–24) | +12% |

| Metals (2024) | +8% |

| PoolCorp gross margin (2024) | ~27% |

| Diesel (2025 Q4) | $4.00/gal |

| Inventory hedge savings | 3–5% |

| Fuel programs | 10–15% |

Full Version Awaits

Pool PESTLE Analysis

The preview shown here is the exact Pool PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.