PORR PESTLE Analysis

Your Shortcut to Market Insight Starts Here

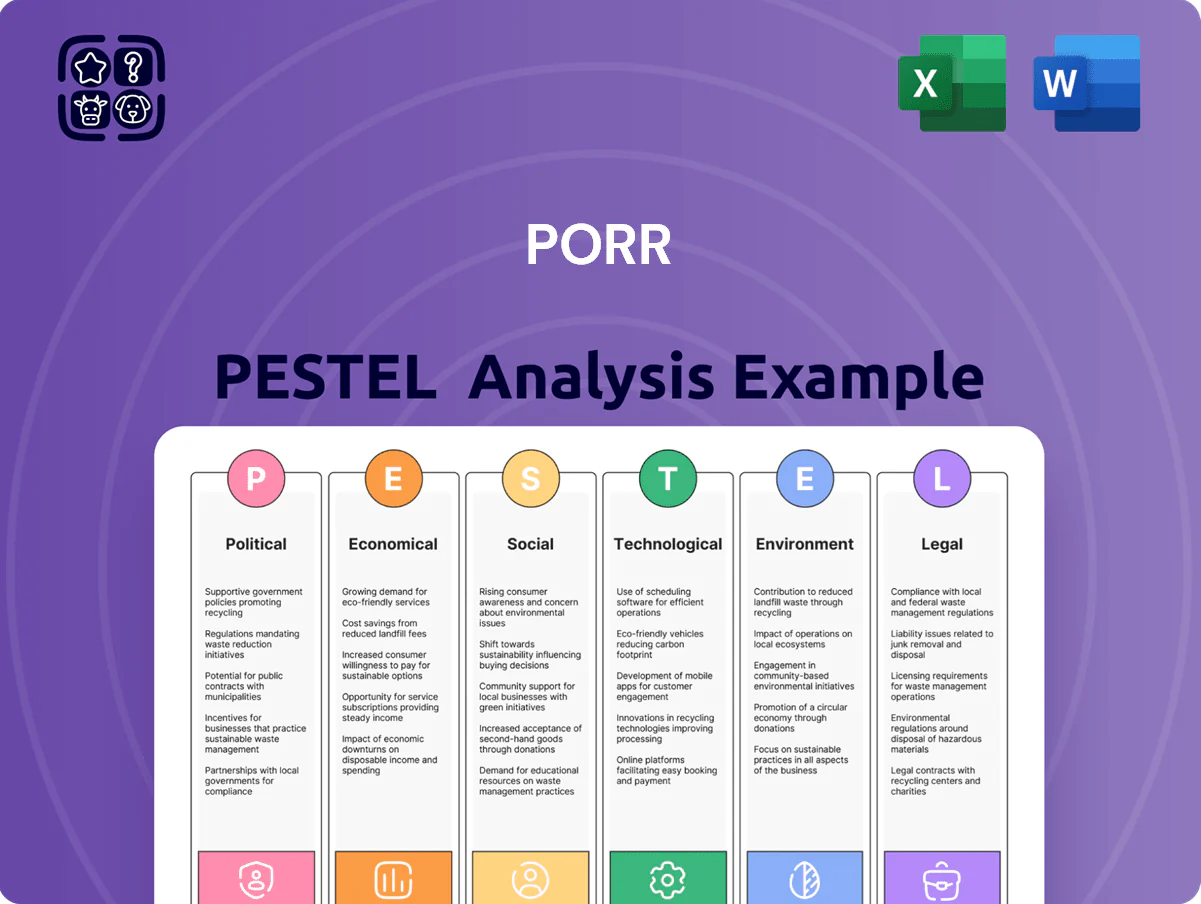

Gain a competitive edge with our PESTLE Analysis of PORR—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report now to access the complete breakdown and actionable recommendations for investors and strategists.

Political factors

EU Infrastructure Funding and Green Deal

The EU’s Connecting Europe Facility and Green Deal continue to channel multi-billion euro funding—the 2024-27 CEF+ and Green Deal investments total over €80bn—supporting rail and energy projects; PORR depends on these allocations for major contracts across Austria, Germany and CEE, where public procurement for low-emission transport rose c.18% y/y in 2024; ongoing political commitment to decarbonizing transport secures a steady pipeline of public contracts for PORR.

Geopolitical Stability in Central and Eastern Europe

The political climate in Poland, Romania and the Czech Republic remains pivotal for PORR’s regional operations and supply chain security; Poland’s 2024 infrastructure budget rose to €16.5bn, Romania committed €9.2bn for transport projects in 2025, and the Czech Republic allocated CZK 150bn (≈€6.3bn) for roads and rail through 2025–26. Regional tensions persist, but EU and NATO integration—Poland and Romania NATO members, Czech Republic a strong EU fund recipient (€24.7bn in 2021–27 cohesion funds)—provide baseline stability for long-term infrastructure investment. Political shifts can materially affect public tender timelines and budget allocations, as seen in 2023–24 when changes in government delayed major tenders by 6–12 months in select projects.

Public Procurement and Transparency Regulations

Governmental pushes for procurement transparency reshape PORR’s competitive field; EU public procurement reforms and the 2024 EU Anti-Corruption Report highlight increased scrutiny with member-state digital procurement adoption rates exceeding 70% in the DACH and CEE regions, reducing opaque contracting. Stricter anti-corruption measures and e-procurement mandates aim to equalize access among large firms; PORR must ensure full political compliance and transparent bidding to retain preferred contractor status on state projects, which accounted for roughly 38% of its 2024 revenue.

Government Housing Initiatives

Government housing subsidies and social residential programs across Europe expanded sharply by 2025, with EU member states allocating an estimated EUR 45–60 billion annually to affordable housing, boosting PORR’s building construction demand in metros such as Vienna and Berlin where public residential projects rose ~18% YoY.

Policy shifts or electoral changes can rapidly alter pipelines: a 10–25% variance in municipal housing budgets has historically translated into equivalent swings in project awards affecting PORR’s order book.

- EUR 45–60bn/year EU housing allocations (2025 est.)

- ~18% YoY increase in public residential projects in Vienna/Berlin

- 10–25% pipeline volatility tied to political/fiscal shifts

Trade Relations and Material Sovereignty

- Steel ~930 USD/tonne (2024); timber imports -12% YoY

- EU domestic steel capacity +8% (2024 incentives)

- Supply-chain disruptions +18% (2023–24)

EU Green Deal & national budgets fuel PORR pipelines amid cost and political volatility

EU Green Deal/CEF+ funding (>€80bn for 2024–27) and rising national infrastructure budgets (Poland €16.5bn; Romania €9.2bn; Czech CZK150bn) secure pipelines for PORR, while procurement reforms and anti-corruption measures (e‑procurement >70% regionally) increase bidding transparency; housing subsidies (€45–60bn/yr EU est. 2025) lift public residential demand (~18% YoY in Vienna/Berlin). Political shifts drive 10–25% pipeline volatility; input cost pressures: steel $930/t (2024), timber imports -12% YoY; supply disruptions +18% (2023–24).

| Indicator | Value |

|---|---|

| CEF+/Green Deal (2024–27) | >€80bn |

| Poland infra budget | €16.5bn |

| Romania transport | €9.2bn |

| Czech roads/rail | CZK150bn (~€6.3bn) |

| EU housing alloc. (2025 est.) | €45–60bn/yr |

| Public residential growth (Vienna/Berlin) | ~18% YoY |

| Procurement digital adoption | >70% |

| Steel price (2024) | $930/t |

| Timber imports | -12% YoY |

| Supply disruptions (2023–24) | +18% |

What is included in the product

Explores how macro-environmental factors uniquely affect PORR across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condenses PORR's full PESTLE into a shareable, slide-ready summary that highlights regulatory and market risks for quick alignment in meetings.

Economic factors

Interest Rate Environment and Financing Costs

Raw Material Price Volatility

Raw material costs for cement, bitumen and steel remain volatile—steel prices swung ~18% in 2024 and oil-linked bitumen rose 22% in H2 2023—exposing PORR to input-price risk.

PORR mitigates shocks through strategic hedging and multi-year supplier contracts covering ~60–70% of major inputs as of 2025.

Indexation clauses in PORR contracts have allowed pass-through of ~80% of material cost increases, supporting margins during recent price spikes.

Skilled Labor Shortages and Wage Inflation

A persistent shortage of qualified engineers and specialized construction workers across Europe has driven wage inflation—EU construction wages rose about 6–8% YoY in 2024, pressuring PORR to increase pay rates. PORR faces economic pressure to offer competitive compensation while scaling internal training; the company reported training investments of roughly EUR 25–30m in 2024. Labor tightness is delaying projects and compressing margins, contributing to elevated subcontractor costs that trimmed PORR’s construction EBIT margin by ~0.5–1.0 percentage point in 2024.

GDP Growth and Infrastructure Demand

The economic health of PORR’s core markets—Austria (2025 GDP 1.6%), Germany (2025 GDP 0.7%), Poland (2025 GDP 3.8%)—directly affects commercial and industrial construction volumes, with stronger Polish growth supporting industrial demand while slower German GDP dampens private investment.

Moderate GDP growth forecasts for 2026 (EU Commission: Austria ~1.2%, Germany ~0.5%, Poland ~3.4%) imply a stable but cautious investment climate for private developers, favoring phased or selective projects.

PORR actively monitors these macro indicators and rebalances portfolios between public infrastructure (where EU Recovery and national budgets boost spending) and private commercial sectors as market signals change.

- Austria 2025 GDP 1.6% — cautious private demand

- Germany 2025 GDP 0.7% — subdued commercial investment

- Poland 2025 GDP 3.8% — stronger industrial pipeline

- 2026 forecasts: Austria ~1.2%, Germany ~0.5%, Poland ~3.4%

Currency Fluctuations in Non-Euro Markets

While roughly 75% of PORR Group revenue is Euro-denominated, sizable operations in Poland and the Czech Republic expose the company to Zloty and Koruna volatility; a 10% depreciation of PLN or CZK versus EUR would lower translated EBITDA by an estimated 3–5% given 2024 regional revenue shares.

Fluctuations affect both reported earnings and cross-border procurement: Poland accounts for ~20% of group revenue and rising construction-material imports mean a 1–2% currency move can change input costs materially.

Stable macro conditions in Poland and Czechia—2024 GDP growth ~3.5% and ~2.7% respectively and inflation moderating to low single digits—support balance-sheet resilience but renewed FX swings could pressure margins and net debt ratios.

- ~75% revenue in EUR; ~20% from Poland, ~8% from Czechia

- 10% PLN/CZK move → ~3–5% EBITDA translation impact

- 1–2% FX shift materially affects cross-border material costs

- 2024 GDP: Poland ~3.5%, Czechia ~2.7%; inflation trending lower

PORR weathers higher ECB rates, input volatility and wage inflation via hedges & debt focus

End-2025 ECB rate ~3.25% keeps financing predictable but 300–350bp above pre-2021, compressing project IRRs; PORR focuses on debt maturity and hedging. Input-price volatility persists—steel ±18% in 2024, bitumen +22% H2 2023—mitigated by hedges and supplier contracts covering ~65% of inputs. Labor-driven wage inflation (EU construction +6–8% YoY 2024) and regional GDP mix (AT 1.6%, DE 0.7%, PL 3.8% 2025) shape demand and margins.

| Metric | Value |

|---|---|

| ECB rate (end‑2025) | 3.25% |

| Steel price swing 2024 | ~18% |

| Bitumen H2 2023 | +22% |

| Inputs hedged | ~65% |

| EU construction wages 2024 | +6–8% YoY |

| 2025 GDP (AT/DE/PL) | 1.6% / 0.7% / 3.8% |

What You See Is What You Get

PORR PESTLE Analysis

The preview shown here is the exact PORR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis of PORR—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report now to access the complete breakdown and actionable recommendations for investors and strategists.

Political factors

EU Infrastructure Funding and Green Deal

The EU’s Connecting Europe Facility and Green Deal continue to channel multi-billion euro funding—the 2024-27 CEF+ and Green Deal investments total over €80bn—supporting rail and energy projects; PORR depends on these allocations for major contracts across Austria, Germany and CEE, where public procurement for low-emission transport rose c.18% y/y in 2024; ongoing political commitment to decarbonizing transport secures a steady pipeline of public contracts for PORR.

Geopolitical Stability in Central and Eastern Europe

The political climate in Poland, Romania and the Czech Republic remains pivotal for PORR’s regional operations and supply chain security; Poland’s 2024 infrastructure budget rose to €16.5bn, Romania committed €9.2bn for transport projects in 2025, and the Czech Republic allocated CZK 150bn (≈€6.3bn) for roads and rail through 2025–26. Regional tensions persist, but EU and NATO integration—Poland and Romania NATO members, Czech Republic a strong EU fund recipient (€24.7bn in 2021–27 cohesion funds)—provide baseline stability for long-term infrastructure investment. Political shifts can materially affect public tender timelines and budget allocations, as seen in 2023–24 when changes in government delayed major tenders by 6–12 months in select projects.

Public Procurement and Transparency Regulations

Governmental pushes for procurement transparency reshape PORR’s competitive field; EU public procurement reforms and the 2024 EU Anti-Corruption Report highlight increased scrutiny with member-state digital procurement adoption rates exceeding 70% in the DACH and CEE regions, reducing opaque contracting. Stricter anti-corruption measures and e-procurement mandates aim to equalize access among large firms; PORR must ensure full political compliance and transparent bidding to retain preferred contractor status on state projects, which accounted for roughly 38% of its 2024 revenue.

Government Housing Initiatives

Government housing subsidies and social residential programs across Europe expanded sharply by 2025, with EU member states allocating an estimated EUR 45–60 billion annually to affordable housing, boosting PORR’s building construction demand in metros such as Vienna and Berlin where public residential projects rose ~18% YoY.

Policy shifts or electoral changes can rapidly alter pipelines: a 10–25% variance in municipal housing budgets has historically translated into equivalent swings in project awards affecting PORR’s order book.

- EUR 45–60bn/year EU housing allocations (2025 est.)

- ~18% YoY increase in public residential projects in Vienna/Berlin

- 10–25% pipeline volatility tied to political/fiscal shifts

Trade Relations and Material Sovereignty

- Steel ~930 USD/tonne (2024); timber imports -12% YoY

- EU domestic steel capacity +8% (2024 incentives)

- Supply-chain disruptions +18% (2023–24)

EU Green Deal & national budgets fuel PORR pipelines amid cost and political volatility

EU Green Deal/CEF+ funding (>€80bn for 2024–27) and rising national infrastructure budgets (Poland €16.5bn; Romania €9.2bn; Czech CZK150bn) secure pipelines for PORR, while procurement reforms and anti-corruption measures (e‑procurement >70% regionally) increase bidding transparency; housing subsidies (€45–60bn/yr EU est. 2025) lift public residential demand (~18% YoY in Vienna/Berlin). Political shifts drive 10–25% pipeline volatility; input cost pressures: steel $930/t (2024), timber imports -12% YoY; supply disruptions +18% (2023–24).

| Indicator | Value |

|---|---|

| CEF+/Green Deal (2024–27) | >€80bn |

| Poland infra budget | €16.5bn |

| Romania transport | €9.2bn |

| Czech roads/rail | CZK150bn (~€6.3bn) |

| EU housing alloc. (2025 est.) | €45–60bn/yr |

| Public residential growth (Vienna/Berlin) | ~18% YoY |

| Procurement digital adoption | >70% |

| Steel price (2024) | $930/t |

| Timber imports | -12% YoY |

| Supply disruptions (2023–24) | +18% |

What is included in the product

Explores how macro-environmental factors uniquely affect PORR across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condenses PORR's full PESTLE into a shareable, slide-ready summary that highlights regulatory and market risks for quick alignment in meetings.

Economic factors

Interest Rate Environment and Financing Costs

Raw Material Price Volatility

Raw material costs for cement, bitumen and steel remain volatile—steel prices swung ~18% in 2024 and oil-linked bitumen rose 22% in H2 2023—exposing PORR to input-price risk.

PORR mitigates shocks through strategic hedging and multi-year supplier contracts covering ~60–70% of major inputs as of 2025.

Indexation clauses in PORR contracts have allowed pass-through of ~80% of material cost increases, supporting margins during recent price spikes.

Skilled Labor Shortages and Wage Inflation

A persistent shortage of qualified engineers and specialized construction workers across Europe has driven wage inflation—EU construction wages rose about 6–8% YoY in 2024, pressuring PORR to increase pay rates. PORR faces economic pressure to offer competitive compensation while scaling internal training; the company reported training investments of roughly EUR 25–30m in 2024. Labor tightness is delaying projects and compressing margins, contributing to elevated subcontractor costs that trimmed PORR’s construction EBIT margin by ~0.5–1.0 percentage point in 2024.

GDP Growth and Infrastructure Demand

The economic health of PORR’s core markets—Austria (2025 GDP 1.6%), Germany (2025 GDP 0.7%), Poland (2025 GDP 3.8%)—directly affects commercial and industrial construction volumes, with stronger Polish growth supporting industrial demand while slower German GDP dampens private investment.

Moderate GDP growth forecasts for 2026 (EU Commission: Austria ~1.2%, Germany ~0.5%, Poland ~3.4%) imply a stable but cautious investment climate for private developers, favoring phased or selective projects.

PORR actively monitors these macro indicators and rebalances portfolios between public infrastructure (where EU Recovery and national budgets boost spending) and private commercial sectors as market signals change.

- Austria 2025 GDP 1.6% — cautious private demand

- Germany 2025 GDP 0.7% — subdued commercial investment

- Poland 2025 GDP 3.8% — stronger industrial pipeline

- 2026 forecasts: Austria ~1.2%, Germany ~0.5%, Poland ~3.4%

Currency Fluctuations in Non-Euro Markets

While roughly 75% of PORR Group revenue is Euro-denominated, sizable operations in Poland and the Czech Republic expose the company to Zloty and Koruna volatility; a 10% depreciation of PLN or CZK versus EUR would lower translated EBITDA by an estimated 3–5% given 2024 regional revenue shares.

Fluctuations affect both reported earnings and cross-border procurement: Poland accounts for ~20% of group revenue and rising construction-material imports mean a 1–2% currency move can change input costs materially.

Stable macro conditions in Poland and Czechia—2024 GDP growth ~3.5% and ~2.7% respectively and inflation moderating to low single digits—support balance-sheet resilience but renewed FX swings could pressure margins and net debt ratios.

- ~75% revenue in EUR; ~20% from Poland, ~8% from Czechia

- 10% PLN/CZK move → ~3–5% EBITDA translation impact

- 1–2% FX shift materially affects cross-border material costs

- 2024 GDP: Poland ~3.5%, Czechia ~2.7%; inflation trending lower

PORR weathers higher ECB rates, input volatility and wage inflation via hedges & debt focus

End-2025 ECB rate ~3.25% keeps financing predictable but 300–350bp above pre-2021, compressing project IRRs; PORR focuses on debt maturity and hedging. Input-price volatility persists—steel ±18% in 2024, bitumen +22% H2 2023—mitigated by hedges and supplier contracts covering ~65% of inputs. Labor-driven wage inflation (EU construction +6–8% YoY 2024) and regional GDP mix (AT 1.6%, DE 0.7%, PL 3.8% 2025) shape demand and margins.

| Metric | Value |

|---|---|

| ECB rate (end‑2025) | 3.25% |

| Steel price swing 2024 | ~18% |

| Bitumen H2 2023 | +22% |

| Inputs hedged | ~65% |

| EU construction wages 2024 | +6–8% YoY |

| 2025 GDP (AT/DE/PL) | 1.6% / 0.7% / 3.8% |

What You See Is What You Get

PORR PESTLE Analysis

The preview shown here is the exact PORR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.