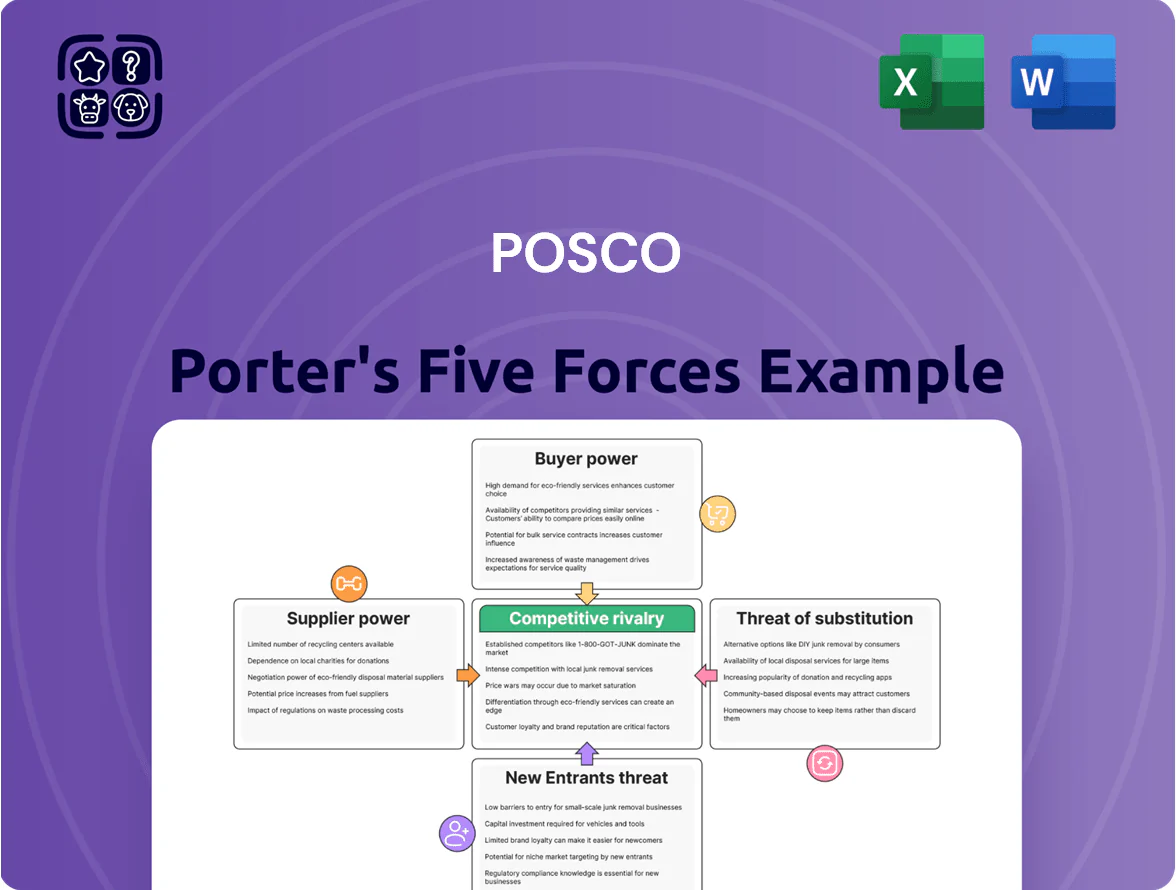

Posco Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Posco operates in a capital-intensive, global steel market where supplier relationships, large-scale rivals, and cyclical demand shape profitability; technological scale and downstream integration are key competitive levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Posco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The global iron ore and coking coal markets are oligopolistic, led by Vale, Rio Tinto and BHP, which together controlled roughly 45% of seaborne iron ore exports and 40% of metallurgical coal exports in 2024; that concentration gives suppliers pricing power over POSCO, especially in demand spikes.

During 2021–2025 price shocks, iron ore fines surged to peaks near $180/t in 2021 and coking coal hit $330/t in late 2021; similar volatility or supply disruptions by end‑2025 raise POSCO’s input-cost risk and margins exposure.

Strategic Importance of Lithium and Nickel Suppliers

Impact of Energy Transition and Green Hydrogen

POSCO’s HyREX steelmaking needs large volumes of renewable power and green hydrogen; suppliers of electrolyzers and renewables wield strong leverage as global green hydrogen capacity was only ~0.3 GW in 2023 vs. needed multi-GW scale, creating a squeeze on price and delivery.

This dependency raises contract and CAPEX risk: POSCO must secure long-term PPAs and hydrogen offtake deals, increasing supplier bargaining power compared with coal-era fuel markets.

Logistics and Maritime Transport Constraints

Shipping firms and logistics providers control sea transport of iron ore and coal to POSCO’s South Korea plants, raising supplier power when specialized capesize and panamax bulk carriers are scarce.

Freight rate volatility—Baltic Capesize Index rose ~45% in 2023 and average tanker/day rates jumped in 2024—shifts costs to POSCO; fuel spikes (IFO380 up ~30% in 2022–24) amplify transport spend and unit steel costs.

- Limited capesize supply concentrates power

- BDI swings alter COGS volatility

- Fuel price hikes raise per-ton transport cost

Supplier Forward Integration Threats

Some large miners like BHP Group and Rio Tinto have invested in processing and alloy projects—BHP’s 2024 nickel downstream JV targeted 50–100 ktpa of refined output—showing limited forward integration into value-added metals; full steelmaking remains capital- and scale-intensive, so threat is partial not total.

Even partial moves erode POSCO’s flexibility by capturing margins in preliminary processing; POSCO reported raw material costs at ~48% of COGS in 2024, so supplier capture of value-added segments could raise input costs and squeeze margins.

To mitigate risk POSCO keeps long-term offtakes and equity ties with key suppliers; in 2023 POSCO held strategic partnerships covering ~30% of iron ore needs, reducing disruption risk while preserving access to upgraded feedstocks.

- Partial forward integration observed (BHP, Rio Tinto projects)

- POSCO raw-materials ≈48% of COGS (2024)

- POSCO strategic supplier ties cover ≈30% of ore (2023)

- Threat limits POSCO’s pricing and product flexibility

Suppliers dominate costs: offtakes, stakes & PPAs crucial as raw materials squeeze margins

Suppliers hold high bargaining power: three majors (Vale, Rio Tinto, BHP) supplied ~45% seaborne iron ore and ~40% coking coal in 2024, and battery metals tightened (lithium ~$70,000/t 2024); POSCO raw materials ≈48% of COGS (2024) and ~30% of ore covered by strategic ties (2023), so long-term offtakes, equity stakes, PPAs and logistics constraints are critical to limit cost and supply risk.

| Metric | Value |

|---|---|

| Seaborne iron ore share (top 3) | ~45% (2024) |

| Lithium price | ~$70,000/t (2024) |

| Raw materials / COGS | ≈48% (2024) |

| Ore covered by ties | ~30% (2023) |

What is included in the product

Tailored exclusively for Posco, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping Posco’s strategic position and profitability.

One-sheet Porter's Five Forces for POSCO—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Major Industrial Buyers

POSCO supplies heavy buyers in automotive, shipbuilding and construction, where a few firms like Hyundai Motor Group and major shipyards account for >30% of segmental steel demand; their bulk orders give them strong price leverage over POSCO.

By end-2025 these customers push for premium, customized steels—advanced high-strength steel for autos and corrosion-resistant plates for ships—forcing POSCO to accept tighter ASPs (average selling prices) to retain volumes.

Demand for Low-Carbon and Green Steel

Institutional and consumer pressure for sustainable supply chains has empowered buyers to demand certified green steel, with global procurement policies rising—EU Green Deal and Japan’s 2050 net-zero targets push demand; 2024 corporate commitments cover >30% of global steel demand. Customers can switch suppliers over carbon intensity, forcing POSCO to speed decarbonization—POSCO targets 2030 GHG cuts of 40% vs 2017 and 2050 neutrality; buyers now set environmental standards and reporting as contract prerequisites.

Availability of Global Sourcing Options

Availability of multiple high-quality steel producers in Asia and Europe lets buyers dual-source or switch if POSCO’s pricing lags; Asian suppliers like China Baowu and Japan’s JFE offer spot prices often 5–10% below POSCO on commoditized grades in 2025, driving negotiation pressure.

POSCO’s higher-quality products help retain contracts for advanced grades, but roughly 60% of global flat-steel trade remains price-sensitive, so customers routinely use Chinese and Japanese quotes to extract better terms from POSCO.

Price Sensitivity in the Construction Sector

The construction sector, which accounted for roughly 28% of POSCO’s domestic steel demand in 2024, is highly rate- and cycle-sensitive; a 1 percentage-point rise in global real interest rates in 2024 cut global construction starts by about 3%, making buyers sharply price-sensitive and pressuring POSCO’s margins.

To retain clients POSCO offered flexible financing and bundled services via POSCO E&C and trading arms, discounting volumes up to 5–8% in Q3 2024 to defend market share.

Impact of Digital Procurement Platforms

The rise of transparent B2B marketplaces lets smaller buyers compare prices and lead times instantly, cutting information asymmetry that once favored large steelmakers and boosting customer bargaining power.

POSCO responded by upgrading its digital sales channels—integrating order data and analytics into its POSCO eMarketplace—raising customer retention; digital sales accounted for about 18% of export volumes in 2024, up from 11% in 2021.

This shift pressures margins: spot-price sensitivity increased, and contract lengths shortened, so POSCO focuses on value-added services (just-in-time delivery, steel-grade matching) to lock customers.

- Smaller buyers can price-check in minutes

- Information asymmetry down; bargaining power up

- POSCO digital sales share: 18% (2024)

- Value services used to secure loyalty

Buyers, green rules and digital sales squeeze POSCO margins — Asian commods down 5–10%

Buyers (Hyundai, major shipyards) account for >30% segment demand, granting strong price leverage; commoditized grades saw 5–10% lower Asian offers in 2025. Sustainability rules (EU Green Deal, Japan net-zero) and corporate green procurement covering >30% steel demand force POSCO to cut ASPs and speed decarbonization (2030 −40% vs 2017). Digital sales rose to 18% (2024), shortening contracts and increasing spot sensitivity; Q3 2024 discounts reached 5–8%.

| Metric | Value |

|---|---|

| Major buyers share | >30% |

| Asian price gap (commod.) | 5–10% |

| Green procurement coverage | >30% |

| POSCO digital exports | 18% (2024) |

| Q3 2024 discounts | 5–8% |

Preview the Actual Deliverable

Posco Porter's Five Forces Analysis

This preview shows the exact POSCO Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

The document displayed here is the full, professionally written analysis of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, available for instant download once you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Posco operates in a capital-intensive, global steel market where supplier relationships, large-scale rivals, and cyclical demand shape profitability; technological scale and downstream integration are key competitive levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Posco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The global iron ore and coking coal markets are oligopolistic, led by Vale, Rio Tinto and BHP, which together controlled roughly 45% of seaborne iron ore exports and 40% of metallurgical coal exports in 2024; that concentration gives suppliers pricing power over POSCO, especially in demand spikes.

During 2021–2025 price shocks, iron ore fines surged to peaks near $180/t in 2021 and coking coal hit $330/t in late 2021; similar volatility or supply disruptions by end‑2025 raise POSCO’s input-cost risk and margins exposure.

Strategic Importance of Lithium and Nickel Suppliers

Impact of Energy Transition and Green Hydrogen

POSCO’s HyREX steelmaking needs large volumes of renewable power and green hydrogen; suppliers of electrolyzers and renewables wield strong leverage as global green hydrogen capacity was only ~0.3 GW in 2023 vs. needed multi-GW scale, creating a squeeze on price and delivery.

This dependency raises contract and CAPEX risk: POSCO must secure long-term PPAs and hydrogen offtake deals, increasing supplier bargaining power compared with coal-era fuel markets.

Logistics and Maritime Transport Constraints

Shipping firms and logistics providers control sea transport of iron ore and coal to POSCO’s South Korea plants, raising supplier power when specialized capesize and panamax bulk carriers are scarce.

Freight rate volatility—Baltic Capesize Index rose ~45% in 2023 and average tanker/day rates jumped in 2024—shifts costs to POSCO; fuel spikes (IFO380 up ~30% in 2022–24) amplify transport spend and unit steel costs.

- Limited capesize supply concentrates power

- BDI swings alter COGS volatility

- Fuel price hikes raise per-ton transport cost

Supplier Forward Integration Threats

Some large miners like BHP Group and Rio Tinto have invested in processing and alloy projects—BHP’s 2024 nickel downstream JV targeted 50–100 ktpa of refined output—showing limited forward integration into value-added metals; full steelmaking remains capital- and scale-intensive, so threat is partial not total.

Even partial moves erode POSCO’s flexibility by capturing margins in preliminary processing; POSCO reported raw material costs at ~48% of COGS in 2024, so supplier capture of value-added segments could raise input costs and squeeze margins.

To mitigate risk POSCO keeps long-term offtakes and equity ties with key suppliers; in 2023 POSCO held strategic partnerships covering ~30% of iron ore needs, reducing disruption risk while preserving access to upgraded feedstocks.

- Partial forward integration observed (BHP, Rio Tinto projects)

- POSCO raw-materials ≈48% of COGS (2024)

- POSCO strategic supplier ties cover ≈30% of ore (2023)

- Threat limits POSCO’s pricing and product flexibility

Suppliers dominate costs: offtakes, stakes & PPAs crucial as raw materials squeeze margins

Suppliers hold high bargaining power: three majors (Vale, Rio Tinto, BHP) supplied ~45% seaborne iron ore and ~40% coking coal in 2024, and battery metals tightened (lithium ~$70,000/t 2024); POSCO raw materials ≈48% of COGS (2024) and ~30% of ore covered by strategic ties (2023), so long-term offtakes, equity stakes, PPAs and logistics constraints are critical to limit cost and supply risk.

| Metric | Value |

|---|---|

| Seaborne iron ore share (top 3) | ~45% (2024) |

| Lithium price | ~$70,000/t (2024) |

| Raw materials / COGS | ≈48% (2024) |

| Ore covered by ties | ~30% (2023) |

What is included in the product

Tailored exclusively for Posco, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping Posco’s strategic position and profitability.

One-sheet Porter's Five Forces for POSCO—quickly gauge supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of Major Industrial Buyers

POSCO supplies heavy buyers in automotive, shipbuilding and construction, where a few firms like Hyundai Motor Group and major shipyards account for >30% of segmental steel demand; their bulk orders give them strong price leverage over POSCO.

By end-2025 these customers push for premium, customized steels—advanced high-strength steel for autos and corrosion-resistant plates for ships—forcing POSCO to accept tighter ASPs (average selling prices) to retain volumes.

Demand for Low-Carbon and Green Steel

Institutional and consumer pressure for sustainable supply chains has empowered buyers to demand certified green steel, with global procurement policies rising—EU Green Deal and Japan’s 2050 net-zero targets push demand; 2024 corporate commitments cover >30% of global steel demand. Customers can switch suppliers over carbon intensity, forcing POSCO to speed decarbonization—POSCO targets 2030 GHG cuts of 40% vs 2017 and 2050 neutrality; buyers now set environmental standards and reporting as contract prerequisites.

Availability of Global Sourcing Options

Availability of multiple high-quality steel producers in Asia and Europe lets buyers dual-source or switch if POSCO’s pricing lags; Asian suppliers like China Baowu and Japan’s JFE offer spot prices often 5–10% below POSCO on commoditized grades in 2025, driving negotiation pressure.

POSCO’s higher-quality products help retain contracts for advanced grades, but roughly 60% of global flat-steel trade remains price-sensitive, so customers routinely use Chinese and Japanese quotes to extract better terms from POSCO.

Price Sensitivity in the Construction Sector

The construction sector, which accounted for roughly 28% of POSCO’s domestic steel demand in 2024, is highly rate- and cycle-sensitive; a 1 percentage-point rise in global real interest rates in 2024 cut global construction starts by about 3%, making buyers sharply price-sensitive and pressuring POSCO’s margins.

To retain clients POSCO offered flexible financing and bundled services via POSCO E&C and trading arms, discounting volumes up to 5–8% in Q3 2024 to defend market share.

Impact of Digital Procurement Platforms

The rise of transparent B2B marketplaces lets smaller buyers compare prices and lead times instantly, cutting information asymmetry that once favored large steelmakers and boosting customer bargaining power.

POSCO responded by upgrading its digital sales channels—integrating order data and analytics into its POSCO eMarketplace—raising customer retention; digital sales accounted for about 18% of export volumes in 2024, up from 11% in 2021.

This shift pressures margins: spot-price sensitivity increased, and contract lengths shortened, so POSCO focuses on value-added services (just-in-time delivery, steel-grade matching) to lock customers.

- Smaller buyers can price-check in minutes

- Information asymmetry down; bargaining power up

- POSCO digital sales share: 18% (2024)

- Value services used to secure loyalty

Buyers, green rules and digital sales squeeze POSCO margins — Asian commods down 5–10%

Buyers (Hyundai, major shipyards) account for >30% segment demand, granting strong price leverage; commoditized grades saw 5–10% lower Asian offers in 2025. Sustainability rules (EU Green Deal, Japan net-zero) and corporate green procurement covering >30% steel demand force POSCO to cut ASPs and speed decarbonization (2030 −40% vs 2017). Digital sales rose to 18% (2024), shortening contracts and increasing spot sensitivity; Q3 2024 discounts reached 5–8%.

| Metric | Value |

|---|---|

| Major buyers share | >30% |

| Asian price gap (commod.) | 5–10% |

| Green procurement coverage | >30% |

| POSCO digital exports | 18% (2024) |

| Q3 2024 discounts | 5–8% |

Preview the Actual Deliverable

Posco Porter's Five Forces Analysis

This preview shows the exact POSCO Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

The document displayed here is the full, professionally written analysis of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry, available for instant download once you buy.