Posco PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the forces shaping Posco’s future—political shifts, economic cycles, technological innovation, social expectations, legal changes, and environmental pressures—with our concise PESTLE snapshot; purchase the full analysis to unlock granular insights, risk forecasts, and actionable strategies you can apply immediately.

Political factors

Geopolitical Trade Tensions

Trade protectionism among the US, China and EU—tariffs rising: US Section 232 measures and EU provisional duties up to 25%—push POSCO to adjust exports, impacting 2024 export volumes (Korea steel exports fell 7% YoY to 32.4 Mt in 2024). POSCO must track shifting regional blocs and optimize overseas hubs (Vietnam, Indonesia, US investments) to preserve global share and offset localized quota/tariff risks.

South Korean Government Industrial Policy

The South Korean government’s 2025 Green New Deal and 2030 battery materials roadmap channelled 12 trillion KRW in subsidies and tax incentives to high-tech and green sectors, directly supporting POSCO’s shift into lithium and cathode materials, where POSCO aims for 200,000 tpa cathode capacity by 2026; recent labor-law reforms increasing minimum protections and a 2024 corporate governance code raise potential labor and compliance costs for POSCO, while state-backed diplomatic missions helped secure minority stakes in mineral projects in Argentina and Indonesia totaling estimated 1–2 Mt LCE equivalent reserves.

Supply Chain Resource Nationalism

Governments in South America and Southeast Asia increasingly impose export controls and local processing mandates; Chile’s 2023 proposals and Indonesia’s 2020–24 policies force downstream investment to retain access to ores.

To secure stable supplies, POSCO must pursue diplomatic engagement and JV structures; its 2024 announcements of partnerships in Argentina and Indonesia aim to lock long-term offtakes and local processing capacity to mitigate supply risk.

Energy Security and Infrastructure Policy

National moves toward hydrogen and a revival of nuclear (South Korea targets 30% hydrogen economy growth by 2030 and plans 6 new reactors by 2035) will lower POSCO energy costs and support its H2-ready decarbonisation pathway.

Government subsidies—Korea allocating KRW 1.5tn for hydrogen R&D in 2024—are critical to scale POSCO’s hydrogen reduction steelmaking and reach its 2030 CO2 intensity targets.

Infrastructure bills (US CHIPS/Inflation Reduction Act and India’s 2024–25 capex push of ~USD 120bn) boost demand for POSCO’s premium construction steel, lifting export prospects and margins.

- South Korea: 6 reactors by 2035; hydrogen economy growth target 2030

- KRW 1.5tn hydrogen R&D funding (2024)

- US/India infrastructure spending ~USD 120bn (India 2024–25) supporting steel demand

Global Sanctions and Compliance

Operating across 55 countries, POSCO must navigate shifting international sanctions—e.g., 2024 sanctions linked to the Russia-Ukraine conflict—where breaches can trigger fines exceeding millions and restrict SWIFT banking access.

Robust compliance programs are essential; POSCO reported 2024 compliance-related costs rising ~8% year-over-year to align with evolving EU/US sanctions and AML rules.

Constant political monitoring in emerging markets is critical to safeguard ~USD 4.5 billion in foreign assets and ongoing investments.

- Presence in 55 countries; ~USD 4.5bn foreign assets at risk

- 2024 compliance costs +8% YoY

- Rapid sanction shifts can block SWIFT/banking access

- Continuous political risk monitoring required to protect investments

POSCO faces tariff, resource and sanction risks but green/H2 funding fuels strategic pivot

Political risks—trade tariffs (US/EU up to 25%), resource nationalism (Chile/Bolivia/Indonesia), and sanctions volatility—pressure POSCO’s export volumes, feedstock costs and compliance spend (2024 compliance +8% YoY). Supportive policies—KRW 12tn Green New Deal, KRW 1.5tn hydrogen R&D (2024), India/US infrastructure ~USD120bn—enable downstream and H2 steel investments; POSCO holds ~USD4.5bn in foreign assets across 55 countries.

| Metric | 2024/2025 |

|---|---|

| Compliance cost change | +8% YoY (2024) |

| Korean green funding | KRW 12tr (2025) |

| Hydrogen R&D | KRW 1.5tr (2024) |

| Foreign assets at risk | ~USD 4.5bn |

| Countries operated | 55 |

What is included in the product

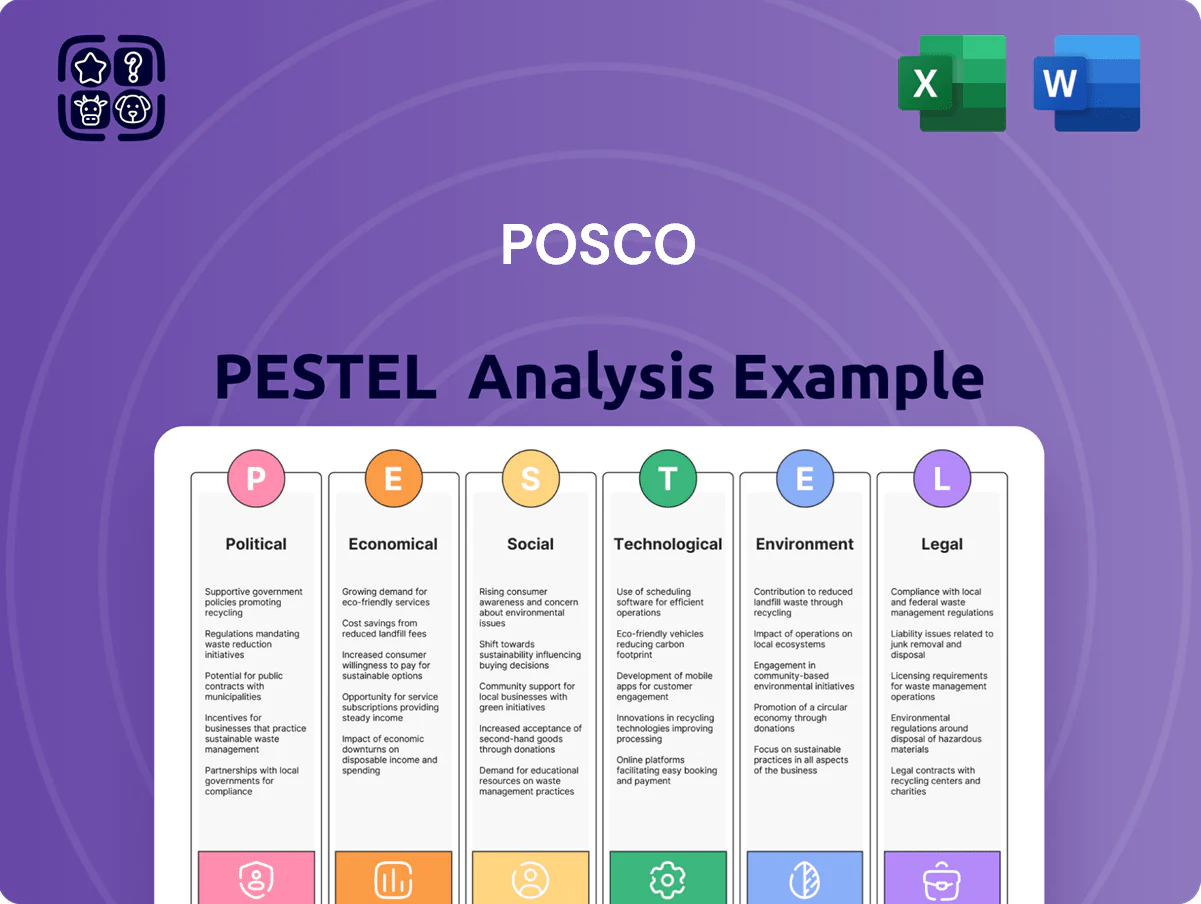

Explores how external macro-environmental factors uniquely affect Posco across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented Posco PESTLE summary that highlights key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Global Steel Demand Cyclicality

POSCO's revenue is highly cyclical, tied to auto, shipbuilding and construction demand; auto industry accounted for about 30% of global steel consumption in 2024 and South Korea's steel exports to auto makers rose 6% in 2024, underscoring exposure.

Global GDP growth slowed to an estimated 3.0% in 2024 and higher central bank rates pushed global capex down, shrinking newbuild ship orders by ~12% year-on-year and dampening steel volumes for POSCO.

By contrast, a manufacturing rebound—global industrial production up 4.2% in 2025 YTD—can lift POSCO EBITDA margins sharply, as steel price recovery historically adds several hundred basis points to core profitability.

Raw Material Price Volatility

Fluctuations in iron ore, coking coal and rising demand for battery metals like lithium and nickel materially affect POSCO margins; iron ore fell ~15% in 2024 while nickel rallied ~40%, increasing raw material cost volatility. POSCO hedges via long-term supply contracts and equity stakes—by 2025 it held minority stakes in mines supplying ~8–12% of its feedstock. Political unrest in major mining regions has triggered supply shocks, raising input cost variance and squeezing EBITDA.

Currency Exchange Rate Fluctuations

As a major exporter, POSCO is highly exposed to KRW/USD volatility; a 10% won depreciation in 2024 would have boosted export price competitiveness but raised dollar-denominated scrap/iron ore import costs by roughly 8–12%, given imports made up ~60% of COGS in 2023.

A weak won helped POSCO MEGA margins in 2024 but compressed gross margin by about 0.5–1.0 percentage point after import cost pass-through.

POSCO uses forwards, FX swaps and currency options; hedge ratios targeted ~65–75% of anticipated FX exposure in 2024, reducing reported FX translation volatility on consolidated income.

Inflationary Pressures and Interest Rates

Persistent global inflation lifted freight and wages; South Korea CPI was 2.7% in 2025 H1 while global shipping rates remained ~30% above pre‑pandemic levels, squeezing POSCO's margins and operational efficiency.

Higher policy rates—Bank of Korea at 3.5% (2025) and global benchmark yields up ~200 bps since 2021—increase debt servicing costs for POSCO's battery‑materials and green‑steel CAPEX, raising financing costs for projects exceeding billions of dollars.

Maintaining investment‑grade credit metrics (net debt/EBITDA targets) is critical to access affordable capital; POSCO reported net debt/EBITDA ~1.8x (2024), underscoring the need for balance‑sheet discipline.

- Inflation → higher labor/logistics costs; CPI 2.7% (KR, 2025 H1)

- Rates up → costlier debt; BOK 3.5% (2025)

- Net debt/EBITDA ~1.8x (2024) → focus on credit rating

EV Market Growth and Battery Material Pricing

The global EV market grew ~40% in 2023 and is projected CAGR ~22% to 2030, directly affecting returns on POSCO's investments in cathode/anode materials as battery demand drives lithium and nickel prices.

EV consumer subsidies (e.g., China/US adjustments in 2024–25) shift battery demand; lithium carbonate ranged ~$60,000/ton in 2024 while nickel metal averaged ~$24,000/ton, impacting margins.

POSCO's diversification into battery materials depends on sustained electrification to offset flat-to-declining steel demand; battery segment revenue targets aim to contribute materially by late 2020s.

- EV market CAGR ~22% to 2030

- Lithium ~60,000/ton (2024)

- Nickel ~24,000/ton (2024)

- Diversification offsets steel stagnation

POSCO: cyclical steel headwinds vs EV-linked lithium upside

POSCO faces cyclical steel demand (auto ~30% global 2024) and input volatility (iron ore -15% 2024; nickel +40% 2024), FX and rate pressure (BOK 3.5% 2025; net debt/EBITDA ~1.8x 2024), while EV-driven battery demand (EV CAGR ~22% to 2030; lithium ~$60k/t 2024) offers diversification upside.

| Metric | 2024/25 |

|---|---|

| Auto share | ~30% |

| Iron ore | -15% |

| Nickel | +40% |

| BOK rate | 3.5% |

| Net debt/EBITDA | ~1.8x |

| Lithium | ~$60k/t |

Preview Before You Purchase

Posco PESTLE Analysis

The preview shown here is the exact Posco PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. No placeholders, no teasers—this is the final, professionally structured report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the forces shaping Posco’s future—political shifts, economic cycles, technological innovation, social expectations, legal changes, and environmental pressures—with our concise PESTLE snapshot; purchase the full analysis to unlock granular insights, risk forecasts, and actionable strategies you can apply immediately.

Political factors

Geopolitical Trade Tensions

Trade protectionism among the US, China and EU—tariffs rising: US Section 232 measures and EU provisional duties up to 25%—push POSCO to adjust exports, impacting 2024 export volumes (Korea steel exports fell 7% YoY to 32.4 Mt in 2024). POSCO must track shifting regional blocs and optimize overseas hubs (Vietnam, Indonesia, US investments) to preserve global share and offset localized quota/tariff risks.

South Korean Government Industrial Policy

The South Korean government’s 2025 Green New Deal and 2030 battery materials roadmap channelled 12 trillion KRW in subsidies and tax incentives to high-tech and green sectors, directly supporting POSCO’s shift into lithium and cathode materials, where POSCO aims for 200,000 tpa cathode capacity by 2026; recent labor-law reforms increasing minimum protections and a 2024 corporate governance code raise potential labor and compliance costs for POSCO, while state-backed diplomatic missions helped secure minority stakes in mineral projects in Argentina and Indonesia totaling estimated 1–2 Mt LCE equivalent reserves.

Supply Chain Resource Nationalism

Governments in South America and Southeast Asia increasingly impose export controls and local processing mandates; Chile’s 2023 proposals and Indonesia’s 2020–24 policies force downstream investment to retain access to ores.

To secure stable supplies, POSCO must pursue diplomatic engagement and JV structures; its 2024 announcements of partnerships in Argentina and Indonesia aim to lock long-term offtakes and local processing capacity to mitigate supply risk.

Energy Security and Infrastructure Policy

National moves toward hydrogen and a revival of nuclear (South Korea targets 30% hydrogen economy growth by 2030 and plans 6 new reactors by 2035) will lower POSCO energy costs and support its H2-ready decarbonisation pathway.

Government subsidies—Korea allocating KRW 1.5tn for hydrogen R&D in 2024—are critical to scale POSCO’s hydrogen reduction steelmaking and reach its 2030 CO2 intensity targets.

Infrastructure bills (US CHIPS/Inflation Reduction Act and India’s 2024–25 capex push of ~USD 120bn) boost demand for POSCO’s premium construction steel, lifting export prospects and margins.

- South Korea: 6 reactors by 2035; hydrogen economy growth target 2030

- KRW 1.5tn hydrogen R&D funding (2024)

- US/India infrastructure spending ~USD 120bn (India 2024–25) supporting steel demand

Global Sanctions and Compliance

Operating across 55 countries, POSCO must navigate shifting international sanctions—e.g., 2024 sanctions linked to the Russia-Ukraine conflict—where breaches can trigger fines exceeding millions and restrict SWIFT banking access.

Robust compliance programs are essential; POSCO reported 2024 compliance-related costs rising ~8% year-over-year to align with evolving EU/US sanctions and AML rules.

Constant political monitoring in emerging markets is critical to safeguard ~USD 4.5 billion in foreign assets and ongoing investments.

- Presence in 55 countries; ~USD 4.5bn foreign assets at risk

- 2024 compliance costs +8% YoY

- Rapid sanction shifts can block SWIFT/banking access

- Continuous political risk monitoring required to protect investments

POSCO faces tariff, resource and sanction risks but green/H2 funding fuels strategic pivot

Political risks—trade tariffs (US/EU up to 25%), resource nationalism (Chile/Bolivia/Indonesia), and sanctions volatility—pressure POSCO’s export volumes, feedstock costs and compliance spend (2024 compliance +8% YoY). Supportive policies—KRW 12tn Green New Deal, KRW 1.5tn hydrogen R&D (2024), India/US infrastructure ~USD120bn—enable downstream and H2 steel investments; POSCO holds ~USD4.5bn in foreign assets across 55 countries.

| Metric | 2024/2025 |

|---|---|

| Compliance cost change | +8% YoY (2024) |

| Korean green funding | KRW 12tr (2025) |

| Hydrogen R&D | KRW 1.5tr (2024) |

| Foreign assets at risk | ~USD 4.5bn |

| Countries operated | 55 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Posco across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented Posco PESTLE summary that highlights key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Global Steel Demand Cyclicality

POSCO's revenue is highly cyclical, tied to auto, shipbuilding and construction demand; auto industry accounted for about 30% of global steel consumption in 2024 and South Korea's steel exports to auto makers rose 6% in 2024, underscoring exposure.

Global GDP growth slowed to an estimated 3.0% in 2024 and higher central bank rates pushed global capex down, shrinking newbuild ship orders by ~12% year-on-year and dampening steel volumes for POSCO.

By contrast, a manufacturing rebound—global industrial production up 4.2% in 2025 YTD—can lift POSCO EBITDA margins sharply, as steel price recovery historically adds several hundred basis points to core profitability.

Raw Material Price Volatility

Fluctuations in iron ore, coking coal and rising demand for battery metals like lithium and nickel materially affect POSCO margins; iron ore fell ~15% in 2024 while nickel rallied ~40%, increasing raw material cost volatility. POSCO hedges via long-term supply contracts and equity stakes—by 2025 it held minority stakes in mines supplying ~8–12% of its feedstock. Political unrest in major mining regions has triggered supply shocks, raising input cost variance and squeezing EBITDA.

Currency Exchange Rate Fluctuations

As a major exporter, POSCO is highly exposed to KRW/USD volatility; a 10% won depreciation in 2024 would have boosted export price competitiveness but raised dollar-denominated scrap/iron ore import costs by roughly 8–12%, given imports made up ~60% of COGS in 2023.

A weak won helped POSCO MEGA margins in 2024 but compressed gross margin by about 0.5–1.0 percentage point after import cost pass-through.

POSCO uses forwards, FX swaps and currency options; hedge ratios targeted ~65–75% of anticipated FX exposure in 2024, reducing reported FX translation volatility on consolidated income.

Inflationary Pressures and Interest Rates

Persistent global inflation lifted freight and wages; South Korea CPI was 2.7% in 2025 H1 while global shipping rates remained ~30% above pre‑pandemic levels, squeezing POSCO's margins and operational efficiency.

Higher policy rates—Bank of Korea at 3.5% (2025) and global benchmark yields up ~200 bps since 2021—increase debt servicing costs for POSCO's battery‑materials and green‑steel CAPEX, raising financing costs for projects exceeding billions of dollars.

Maintaining investment‑grade credit metrics (net debt/EBITDA targets) is critical to access affordable capital; POSCO reported net debt/EBITDA ~1.8x (2024), underscoring the need for balance‑sheet discipline.

- Inflation → higher labor/logistics costs; CPI 2.7% (KR, 2025 H1)

- Rates up → costlier debt; BOK 3.5% (2025)

- Net debt/EBITDA ~1.8x (2024) → focus on credit rating

EV Market Growth and Battery Material Pricing

The global EV market grew ~40% in 2023 and is projected CAGR ~22% to 2030, directly affecting returns on POSCO's investments in cathode/anode materials as battery demand drives lithium and nickel prices.

EV consumer subsidies (e.g., China/US adjustments in 2024–25) shift battery demand; lithium carbonate ranged ~$60,000/ton in 2024 while nickel metal averaged ~$24,000/ton, impacting margins.

POSCO's diversification into battery materials depends on sustained electrification to offset flat-to-declining steel demand; battery segment revenue targets aim to contribute materially by late 2020s.

- EV market CAGR ~22% to 2030

- Lithium ~60,000/ton (2024)

- Nickel ~24,000/ton (2024)

- Diversification offsets steel stagnation

POSCO: cyclical steel headwinds vs EV-linked lithium upside

POSCO faces cyclical steel demand (auto ~30% global 2024) and input volatility (iron ore -15% 2024; nickel +40% 2024), FX and rate pressure (BOK 3.5% 2025; net debt/EBITDA ~1.8x 2024), while EV-driven battery demand (EV CAGR ~22% to 2030; lithium ~$60k/t 2024) offers diversification upside.

| Metric | 2024/25 |

|---|---|

| Auto share | ~30% |

| Iron ore | -15% |

| Nickel | +40% |

| BOK rate | 3.5% |

| Net debt/EBITDA | ~1.8x |

| Lithium | ~$60k/t |

Preview Before You Purchase

Posco PESTLE Analysis

The preview shown here is the exact Posco PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. No placeholders, no teasers—this is the final, professionally structured report.