Post Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

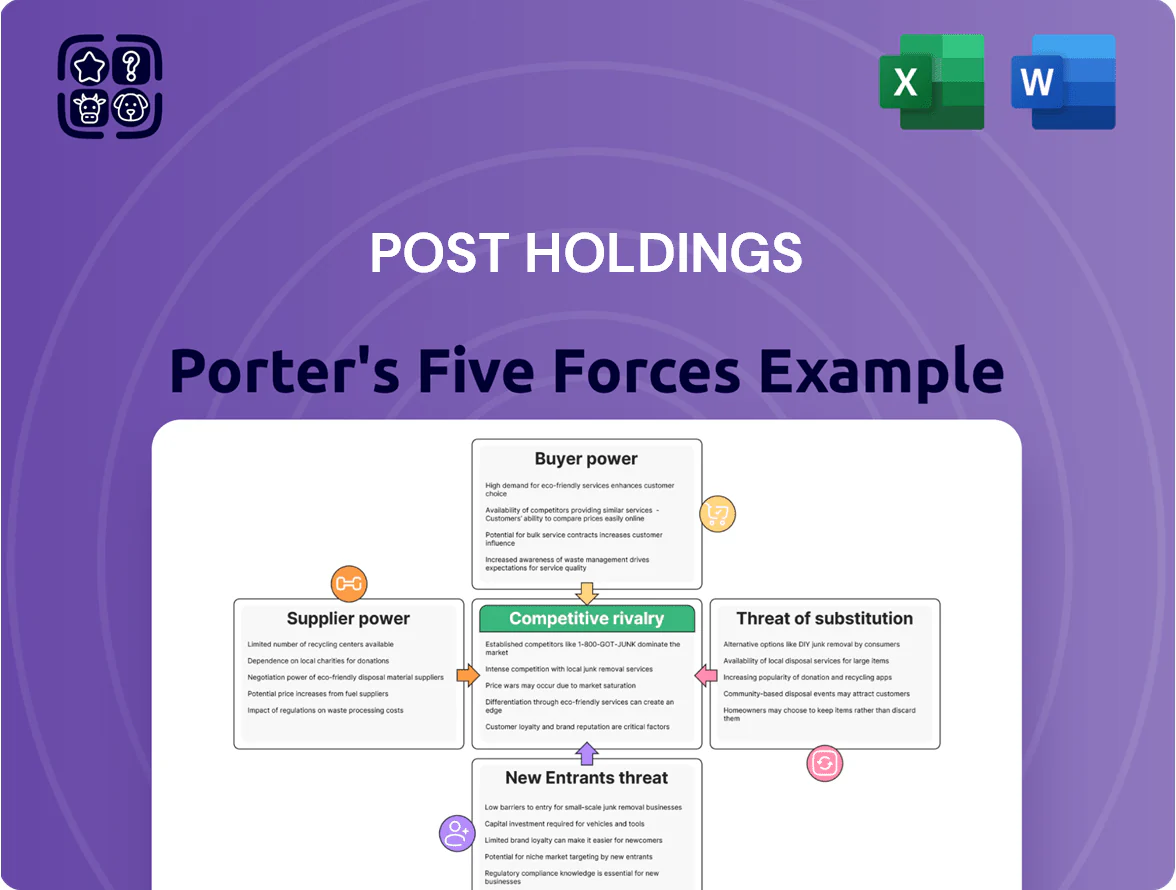

Post Holdings faces moderate supplier power, intense rivalry in branded and private-label categories, growing substitute threats from plant-based and direct-to-consumer entrants, and significant buyer influence from major retailers—while barriers to entry remain medium due to scale and distribution needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Post Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity price volatility

Post Holdings buys large volumes of corn, wheat, oats and soy; these commodities rose ~22% year-over-year in 2024 and remain volatile, pressuring COGS.

The company uses futures and swaps to hedge, but hedges covered ~60% of expected 2025 volumes as of Q3 2025, leaving exposure to spot swings.

By late 2025 climate shocks (droughts in North America) and geopolitical tensions (Black Sea grain risks) keep input-cost variability high, complicating margin management.

Concentration of specialized ingredient providers

In active nutrition, Post sources whey and plant proteins from a small number of high-grade suppliers, concentrating bargaining power; global whey protein prices rose about 18% in 2024, so suppliers can pass costs to buyers. This gives vendors leverage to demand higher prices or tighter terms, risking margin pressure for Premier Protein. Post therefore prioritizes long-term contracts and dual-sourcing to secure supply and cap input cost volatility.

Energy and packaging costs

Energy and packaging costs materially affect Post Holdings: in 2024 U.S. industrial electricity rose ~6% year-over-year and global resin (plastic) prices were up ~12%, raising input costs for cereal and snack packaging. Suppliers of plastic, cardboard and aluminum gained leverage as 2023–24 ESG rules and demand for recyclable materials pushed conversion costs up ~8–15%. Post must either absorb higher COGS—pressuring 2024 gross margins—or drive $50–150M in supply-chain efficiencies to offset impacts.

Labor market constraints

The specialized nature of food processing and foodservice gives labor supplier power; skilled operators and food-safety-trained staff are hard to replace, so Post faces wage pressure. By 2025 Post reports rising wage costs—companywide labor expense grew ~6–8% YoY in 2024–25—prompting increased automation capex and retention programs. Human-capital costs remain a top operational driver across its portfolio.

- Skilled labor = supplier power

- Labor expense +6–8% YoY (2024–25)

- More automation capex, retention spend

- Human capital = primary cost driver in 2025

Logistics and transportation availability

Post Holdings relies heavily on third-party logistics and carriers to move goods; 2024 average US truckload spot rates rose ~12% year-over-year, raising distribution costs and squeezing margins.

Supplier power grows when fuel volatility, driver shortages (shortfall ~80,000 drivers in 2024), or port congestion reduce capacity, forcing Post to accept higher rates or delayed deliveries.

Any logistics disruption quickly increases COGS and can force price hikes that harm retail competitiveness; a one‑day delay on 10% of shipments can cut weekly on‑shelf availability by ~2–4%.

- 2024 truckload spot rates +12%

- Driver shortfall ~80,000 (2024)

- Fuel price swings directly raise per-unit freight cost

Supplier power squeezes margins: commodities, proteins, packaging & logistics surge

Suppliers hold moderate-to-high power: commodity volatility (corn/wheat +22% YoY 2024), concentrated protein suppliers (whey +18% 2024), rising packaging/resin (+12% 2024) and logistics costs (US truckload spot +12% 2024) squeeze margins; hedges covered ~60% of 2025 volumes, labor up 6–8% YoY, and driver shortfall ~80,000 in 2024 heighten supplier leverage.

| Metric | 2024/2025 |

|---|---|

| Corn/wheat/oats/soy | +22% YoY (2024) |

| Whey protein | +18% (2024) |

| Resin/plastic | +12% (2024) |

| Truckload spot rates | +12% (2024) |

| Hedge coverage | ~60% expected 2025 vols (Q3 2025) |

| Labor cost | +6–8% YoY (2024–25) |

| Driver shortfall | ~80,000 (2024) |

What is included in the product

Tailored exclusively for Post Holdings, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces summary for Post Holdings—quickly gauge supplier, buyer, competitor, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Retailer consolidation

Retail concentration is high: Walmart, Kroger, and Costco together accounted for roughly 28% of US grocery sales in 2024, giving them clout to demand lower wholesale prices and deeper promotions from manufacturers like Post Holdings.

These buyers leverage scale—Walmart’s $770B US sales in 2024 and Kroger’s $155B—forcing Post to accept tighter margins or fund promotions to keep shelf space.

As consolidation continues, Post must prioritize key account negotiation, co-op spend, and exclusive SKUs to protect distribution and gross margin.

Growth of private label brands

Retailers like Walmart and Kroger raised private-label share to about 20–25% of grocery sales in 2024, intensifying price pressure on Post Holdings’ branded cereals and refrigerated foods.

Store brands often match quality at 10–30% lower price points, so retailers gain leverage in slotting fees and promotions as they rely less on national brands.

Post reported 2024 net sales of $5.3B; it must keep investing in R&D and marketing to protect brand equity and shrink price-driven churn.

Low switching costs for end consumers

Individual consumers face virtually zero cost switching from Post Holdings cereals to rivals or private labels; NielsenIQ data show U.S. cereal private-label share rose to ~15.3% in 2024, so loyalty is fragile and driven by price, taste, and health claims.

Post must invest in targeted marketing and product innovation—Post’s 2024 R&D and SG&A mix and its 2024 $6.1B net sales underscore the need to protect share in a crowded market.

Data-driven procurement by big-box retailers

Foodservice contract bidding

Foodservice contract bidding drives high customer bargaining power for Post Holdings, as Michael Foods competes for contracts with large chains and institutions that can switch suppliers over price or reliability; in 2024 foodservice accounted for roughly 27% of Post’s revenue (Post Holdings 2024 10-K), raising stakes on cost and service.

To keep accounts, Michael Foods must meet tight efficiency and quality KPIs—on-time fills, <1% defect rates, and competitive pricing—since lost contracts can cut multi-million-dollar annual spend per account.

- Foodservice = ~27% of Post revenue (2024 10-K)

- Large buyers can switch for better price/reliability

- Michael Foods needs <1% defect rates, on-time fills

- Lost contracts imply multi-million $ revenue swings

Retailer & private‑label leverage squeezes Post—foodservice reliability now mission‑critical

Large retailers (Walmart, Kroger, Costco) and growing private-labels (20–25% grocery share in 2024) give strong buyer leverage vs Post Holdings (2024 net sales $5.3B–$6.1B); retailers use daily POS data to demand lower prices, promos, and SKU transparency. Foodservice (≈27% of Post revenue, 2024) adds contract-driven pressure requiring <1% defects and tight fills to retain multi‑million accounts.

| Metric | 2024 |

|---|---|

| Retailer share (Walmart+Kroger+Costco) | ≈28% |

| Private‑label grocery | 20–25% |

| Post net sales | $5.3–$6.1B |

| Foodservice % of revenue | ≈27% |

Preview Before You Purchase

Post Holdings Porter's Five Forces Analysis

This preview shows the exact Post Holdings Porter’s Five Forces analysis you'll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Post Holdings faces moderate supplier power, intense rivalry in branded and private-label categories, growing substitute threats from plant-based and direct-to-consumer entrants, and significant buyer influence from major retailers—while barriers to entry remain medium due to scale and distribution needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Post Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity price volatility

Post Holdings buys large volumes of corn, wheat, oats and soy; these commodities rose ~22% year-over-year in 2024 and remain volatile, pressuring COGS.

The company uses futures and swaps to hedge, but hedges covered ~60% of expected 2025 volumes as of Q3 2025, leaving exposure to spot swings.

By late 2025 climate shocks (droughts in North America) and geopolitical tensions (Black Sea grain risks) keep input-cost variability high, complicating margin management.

Concentration of specialized ingredient providers

In active nutrition, Post sources whey and plant proteins from a small number of high-grade suppliers, concentrating bargaining power; global whey protein prices rose about 18% in 2024, so suppliers can pass costs to buyers. This gives vendors leverage to demand higher prices or tighter terms, risking margin pressure for Premier Protein. Post therefore prioritizes long-term contracts and dual-sourcing to secure supply and cap input cost volatility.

Energy and packaging costs

Energy and packaging costs materially affect Post Holdings: in 2024 U.S. industrial electricity rose ~6% year-over-year and global resin (plastic) prices were up ~12%, raising input costs for cereal and snack packaging. Suppliers of plastic, cardboard and aluminum gained leverage as 2023–24 ESG rules and demand for recyclable materials pushed conversion costs up ~8–15%. Post must either absorb higher COGS—pressuring 2024 gross margins—or drive $50–150M in supply-chain efficiencies to offset impacts.

Labor market constraints

The specialized nature of food processing and foodservice gives labor supplier power; skilled operators and food-safety-trained staff are hard to replace, so Post faces wage pressure. By 2025 Post reports rising wage costs—companywide labor expense grew ~6–8% YoY in 2024–25—prompting increased automation capex and retention programs. Human-capital costs remain a top operational driver across its portfolio.

- Skilled labor = supplier power

- Labor expense +6–8% YoY (2024–25)

- More automation capex, retention spend

- Human capital = primary cost driver in 2025

Logistics and transportation availability

Post Holdings relies heavily on third-party logistics and carriers to move goods; 2024 average US truckload spot rates rose ~12% year-over-year, raising distribution costs and squeezing margins.

Supplier power grows when fuel volatility, driver shortages (shortfall ~80,000 drivers in 2024), or port congestion reduce capacity, forcing Post to accept higher rates or delayed deliveries.

Any logistics disruption quickly increases COGS and can force price hikes that harm retail competitiveness; a one‑day delay on 10% of shipments can cut weekly on‑shelf availability by ~2–4%.

- 2024 truckload spot rates +12%

- Driver shortfall ~80,000 (2024)

- Fuel price swings directly raise per-unit freight cost

Supplier power squeezes margins: commodities, proteins, packaging & logistics surge

Suppliers hold moderate-to-high power: commodity volatility (corn/wheat +22% YoY 2024), concentrated protein suppliers (whey +18% 2024), rising packaging/resin (+12% 2024) and logistics costs (US truckload spot +12% 2024) squeeze margins; hedges covered ~60% of 2025 volumes, labor up 6–8% YoY, and driver shortfall ~80,000 in 2024 heighten supplier leverage.

| Metric | 2024/2025 |

|---|---|

| Corn/wheat/oats/soy | +22% YoY (2024) |

| Whey protein | +18% (2024) |

| Resin/plastic | +12% (2024) |

| Truckload spot rates | +12% (2024) |

| Hedge coverage | ~60% expected 2025 vols (Q3 2025) |

| Labor cost | +6–8% YoY (2024–25) |

| Driver shortfall | ~80,000 (2024) |

What is included in the product

Tailored exclusively for Post Holdings, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces summary for Post Holdings—quickly gauge supplier, buyer, competitor, entrant, and substitute pressures to guide strategic decisions.

Customers Bargaining Power

Retailer consolidation

Retail concentration is high: Walmart, Kroger, and Costco together accounted for roughly 28% of US grocery sales in 2024, giving them clout to demand lower wholesale prices and deeper promotions from manufacturers like Post Holdings.

These buyers leverage scale—Walmart’s $770B US sales in 2024 and Kroger’s $155B—forcing Post to accept tighter margins or fund promotions to keep shelf space.

As consolidation continues, Post must prioritize key account negotiation, co-op spend, and exclusive SKUs to protect distribution and gross margin.

Growth of private label brands

Retailers like Walmart and Kroger raised private-label share to about 20–25% of grocery sales in 2024, intensifying price pressure on Post Holdings’ branded cereals and refrigerated foods.

Store brands often match quality at 10–30% lower price points, so retailers gain leverage in slotting fees and promotions as they rely less on national brands.

Post reported 2024 net sales of $5.3B; it must keep investing in R&D and marketing to protect brand equity and shrink price-driven churn.

Low switching costs for end consumers

Individual consumers face virtually zero cost switching from Post Holdings cereals to rivals or private labels; NielsenIQ data show U.S. cereal private-label share rose to ~15.3% in 2024, so loyalty is fragile and driven by price, taste, and health claims.

Post must invest in targeted marketing and product innovation—Post’s 2024 R&D and SG&A mix and its 2024 $6.1B net sales underscore the need to protect share in a crowded market.

Data-driven procurement by big-box retailers

Foodservice contract bidding

Foodservice contract bidding drives high customer bargaining power for Post Holdings, as Michael Foods competes for contracts with large chains and institutions that can switch suppliers over price or reliability; in 2024 foodservice accounted for roughly 27% of Post’s revenue (Post Holdings 2024 10-K), raising stakes on cost and service.

To keep accounts, Michael Foods must meet tight efficiency and quality KPIs—on-time fills, <1% defect rates, and competitive pricing—since lost contracts can cut multi-million-dollar annual spend per account.

- Foodservice = ~27% of Post revenue (2024 10-K)

- Large buyers can switch for better price/reliability

- Michael Foods needs <1% defect rates, on-time fills

- Lost contracts imply multi-million $ revenue swings

Retailer & private‑label leverage squeezes Post—foodservice reliability now mission‑critical

Large retailers (Walmart, Kroger, Costco) and growing private-labels (20–25% grocery share in 2024) give strong buyer leverage vs Post Holdings (2024 net sales $5.3B–$6.1B); retailers use daily POS data to demand lower prices, promos, and SKU transparency. Foodservice (≈27% of Post revenue, 2024) adds contract-driven pressure requiring <1% defects and tight fills to retain multi‑million accounts.

| Metric | 2024 |

|---|---|

| Retailer share (Walmart+Kroger+Costco) | ≈28% |

| Private‑label grocery | 20–25% |

| Post net sales | $5.3–$6.1B |

| Foodservice % of revenue | ≈27% |

Preview Before You Purchase

Post Holdings Porter's Five Forces Analysis

This preview shows the exact Post Holdings Porter’s Five Forces analysis you'll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.