PostNL Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

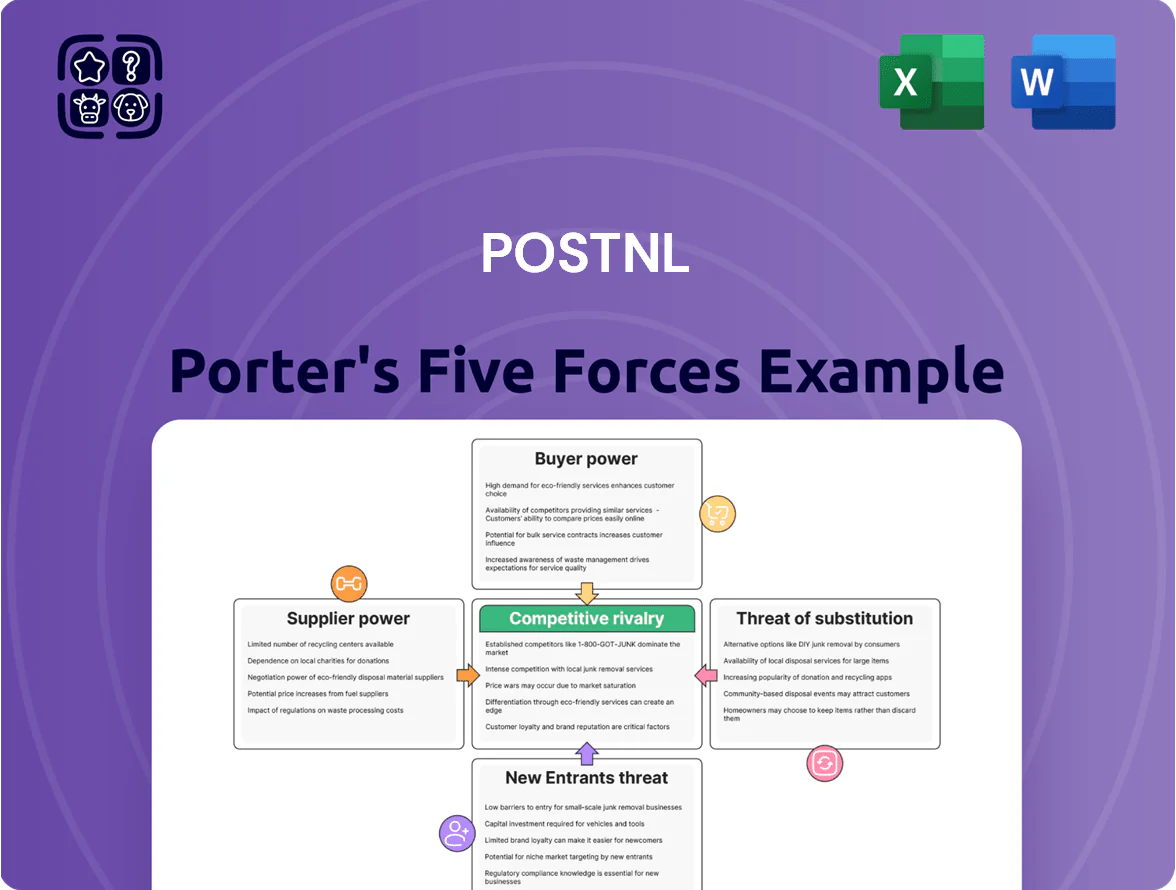

PostNL faces moderate buyer power and intense competition from parcel specialists and global carriers, while regulatory shifts and digital disruption raise substitute and entrant threats; supplier influence remains limited but operational costs are a key pressure point. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PostNL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Labor Unions and Collective Labor Agreements

PostNL depends on ~40,000 employees in the Benelux for sorting and delivery (2024 headcount), so Dutch unions like FNV and CNV wield strong bargaining power over wages, benefits, and hours.

Collective labor agreements covering roughly 70% of the workforce limit unilateral cost cuts and drove a 2024 labor-cost increase of ~5–7%, squeezing operating margin (2024 EBITDA margin 5.2%).

Energy and Fuel Providers

PostNL’s fleet costs are highly sensitive: fuel and electricity accounted for about 18% of operating expenses in 2024, and global Brent oil averaged $86/barrel in 2024, pushing diesel prices up 12% year-over-year.

Though PostNL plans 100% zero-emission city deliveries by 2025 and had ~25% EVs in its fleet by end-2024, it still relies on energy suppliers for fuel and charging infrastructure.

Large energy firms show limited competition; their moderate bargaining power affects pricing and long-term contracts, constraining PostNL’s cost visibility and capex for chargers.

Subcontracted Delivery Partners

About 60% of PostNL’s last-mile volumes rely on independent subcontractors and delivery partners, giving PostNL flexible capacity during peaks like Q4 when parcel volumes rose ~25% in 2024.

Those partners face rising fuel and labor costs, so they press for higher per-delivery rates; PostNL reported subcontractor cost increases of roughly 8% in 2024.

PostNL must balance rate offers to keep margins while avoiding partner churn to rivals such as DPDgroup and DHL, which could poach capacity with better terms.

Vehicle Manufacturers and EV Infrastructure

As PostNL shifts to emission-free delivery, its reliance on electric van and specialized-equipment makers rises; in 2024 PostNL ordered 2,250 EVs and plans 10,000+ by 2030, so supplier access matters.

Battery shortages and long global manufacturing cycles—EV battery capacity growth slowed to 18% in 2023 vs 40% in 2021—tighten supply, giving major OEMs leverage on price and delivery.

Large suppliers can demand multi-year contracts and upfront deposits, raising procurement costs and scheduling risk for PostNL.

- 2024 order: 2,250 EVs; target 10,000+ by 2030

- Battery capacity growth: 18% in 2023

- Supplier leverage: favors OEMs on long-term contracts

Specialized IT and Automation Vendors

Specialized IT and automation vendors wield strong supplier power at PostNL because modernizing sorting centers and implementing tracking rely on software/hardware from a few global providers; switching costs are high and integration is deep.

These suppliers influence maintenance and licensing costs—PostNL spent ~€180m on IT & telecom in 2024, so vendor pricing materially affects margins and uptime.

- Few suppliers: concentrated vendor base

- High switching cost: deep system integration

- Essential services: €180m IT spend in 2024

- Ongoing leverage: control over maintenance/licensing

Suppliers tighten grip: rising labor, energy, subcontractor costs and EV capex risk

Suppliers (labor unions, energy firms, OEMs, IT vendors, subcontractors) exert moderate-to-strong bargaining power, driving 2024 cost pressure: labor +5–7% (70% under collective agreements), fuel/electricity ~18% of Opex (Brent $86/bbl), subcontractor costs +8%, IT/telecom spend €180m; EV procurement (2,250 in 2024; target 10,000+ by 2030) raises OEM leverage and capex timing risk.

| Metric | 2024 | Note |

|---|---|---|

| Headcount | ~40,000 | Benelux |

| Labor cost change | +5–7% | Collective agreements ~70% |

| Fuel/electricity | ~18% Opex | Brent $86/bbl |

| Subcontractor cost | +8% | Last-mile partners ~60% volumes |

| IT & telecom | €180m | 2024 spend |

| EV orders / target | 2,250 / 10,000+ | 2024 / by 2030 |

What is included in the product

Tailored exclusively for PostNL, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and strategic levers that influence pricing, profitability, and market position.

A concise PostNL Porter's Five Forces one-sheet that highlights shipment industry pressures—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Large E-commerce Platforms and Retailers

Major online retailers like Bol.com, Amazon, and Coolblue ship millions of parcels yearly—Bol.com handled ~50m shipments in 2024—giving them strong leverage to demand lower per-parcel rates from PostNL.

The scale lets them consider alternatives or build in-house logistics; Amazon already runs extensive EU networks, and Coolblue and Bol.com have tested carrier diversification in 2023–25.

This volume-shifting power forces PostNL to keep prices competitive and service levels high; loss of a single major client could cut millions in annual revenue—Bol.com alone accounts for an estimated 5–10% of Dutch parcel volumes in 2024.

Price Sensitivity of Small and Medium Enterprises

SMEs make up about 60% of PostNL’s B2B parcel volume in 2024 but buy too little each to secure bulk discounts, so they remain highly price-sensitive and quick to switch to DHL or DPD if rates rise.

Retention hinges on easy digital tools and 99%+ delivery reliability targets; PostNL’s 2024 SME churn rose 4% after a 6% tariff hike, showing sensitivity.

Individual Consumer Service Expectations

Private consumers demand flexible delivery: 45% in the Netherlands (2024 PostNL survey) prefer evening slots and 60% use pick‑up points; this raises service expectations beyond price sensitivity.

Individually they have low price bargaining power, but their collective choices pushed e‑commerce returns and same‑day options, influencing retailers’ carrier selection.

If PostNL misses these needs, it risks share loss—online retailers shifted 12% of parcel volume to rivals in 2023 for faster, more flexible options.

Corporate and Institutional Mail Clients

Corporate and institutional clients like banks and government agencies have become scarce and thus more valuable as Dutch letter volumes fell 9.3% in 2024; they frequently consolidate mail and run tenders to secure lowest-cost, reliable delivery, raising PostNL’s bargaining pressure.

PostNL’s unit cost per item rises as volumes decline—letter volumes down to ~1.2 billion in 2024—forcing discounts on large contracts while squeezing margins on transactional mail.

- Clients: banks, government—high value

- Tenders drive price pressure

- 2024 letter volumes ~1.2bn (-9.3%)

- Unit cost up as volumes fall, margin squeeze

Switching Costs for Business Integration

- High current stickiness from direct API integrations

- Switch cost = IT resources + operational disruption

- Standardized platforms (28% adoption in NL, 2024) lower costs

- Net effect: modest rise in customer power

Delivery power shifts: big e‑tailers & SMEs force discounts, flexible pick‑up rises

Large e‑tailers (Bol.com ~50m parcels 2024; Bol.com = ~5–10% Dutch volume) and SMEs (60% B2B volume) drive price sensitivity; major clients can switch or insource, forcing discounts. Consumer demand for flexible delivery (45% evening, 60% pick‑up points, 2024) raises service expectations. API integrations create stickiness, but 28% multi‑carrier middleware adoption (2024) nudges switching up.

| Metric | 2024 |

|---|---|

| Bol.com parcels | ~50m |

| Bol.com share | 5–10% |

| SME B2B share | 60% |

| Pick‑up preference | 60% |

| Multi‑carrier middleware | 28% |

Preview Before You Purchase

PostNL Porter's Five Forces Analysis

This preview shows the exact PostNL Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

PostNL faces moderate buyer power and intense competition from parcel specialists and global carriers, while regulatory shifts and digital disruption raise substitute and entrant threats; supplier influence remains limited but operational costs are a key pressure point. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PostNL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Labor Unions and Collective Labor Agreements

PostNL depends on ~40,000 employees in the Benelux for sorting and delivery (2024 headcount), so Dutch unions like FNV and CNV wield strong bargaining power over wages, benefits, and hours.

Collective labor agreements covering roughly 70% of the workforce limit unilateral cost cuts and drove a 2024 labor-cost increase of ~5–7%, squeezing operating margin (2024 EBITDA margin 5.2%).

Energy and Fuel Providers

PostNL’s fleet costs are highly sensitive: fuel and electricity accounted for about 18% of operating expenses in 2024, and global Brent oil averaged $86/barrel in 2024, pushing diesel prices up 12% year-over-year.

Though PostNL plans 100% zero-emission city deliveries by 2025 and had ~25% EVs in its fleet by end-2024, it still relies on energy suppliers for fuel and charging infrastructure.

Large energy firms show limited competition; their moderate bargaining power affects pricing and long-term contracts, constraining PostNL’s cost visibility and capex for chargers.

Subcontracted Delivery Partners

About 60% of PostNL’s last-mile volumes rely on independent subcontractors and delivery partners, giving PostNL flexible capacity during peaks like Q4 when parcel volumes rose ~25% in 2024.

Those partners face rising fuel and labor costs, so they press for higher per-delivery rates; PostNL reported subcontractor cost increases of roughly 8% in 2024.

PostNL must balance rate offers to keep margins while avoiding partner churn to rivals such as DPDgroup and DHL, which could poach capacity with better terms.

Vehicle Manufacturers and EV Infrastructure

As PostNL shifts to emission-free delivery, its reliance on electric van and specialized-equipment makers rises; in 2024 PostNL ordered 2,250 EVs and plans 10,000+ by 2030, so supplier access matters.

Battery shortages and long global manufacturing cycles—EV battery capacity growth slowed to 18% in 2023 vs 40% in 2021—tighten supply, giving major OEMs leverage on price and delivery.

Large suppliers can demand multi-year contracts and upfront deposits, raising procurement costs and scheduling risk for PostNL.

- 2024 order: 2,250 EVs; target 10,000+ by 2030

- Battery capacity growth: 18% in 2023

- Supplier leverage: favors OEMs on long-term contracts

Specialized IT and Automation Vendors

Specialized IT and automation vendors wield strong supplier power at PostNL because modernizing sorting centers and implementing tracking rely on software/hardware from a few global providers; switching costs are high and integration is deep.

These suppliers influence maintenance and licensing costs—PostNL spent ~€180m on IT & telecom in 2024, so vendor pricing materially affects margins and uptime.

- Few suppliers: concentrated vendor base

- High switching cost: deep system integration

- Essential services: €180m IT spend in 2024

- Ongoing leverage: control over maintenance/licensing

Suppliers tighten grip: rising labor, energy, subcontractor costs and EV capex risk

Suppliers (labor unions, energy firms, OEMs, IT vendors, subcontractors) exert moderate-to-strong bargaining power, driving 2024 cost pressure: labor +5–7% (70% under collective agreements), fuel/electricity ~18% of Opex (Brent $86/bbl), subcontractor costs +8%, IT/telecom spend €180m; EV procurement (2,250 in 2024; target 10,000+ by 2030) raises OEM leverage and capex timing risk.

| Metric | 2024 | Note |

|---|---|---|

| Headcount | ~40,000 | Benelux |

| Labor cost change | +5–7% | Collective agreements ~70% |

| Fuel/electricity | ~18% Opex | Brent $86/bbl |

| Subcontractor cost | +8% | Last-mile partners ~60% volumes |

| IT & telecom | €180m | 2024 spend |

| EV orders / target | 2,250 / 10,000+ | 2024 / by 2030 |

What is included in the product

Tailored exclusively for PostNL, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and strategic levers that influence pricing, profitability, and market position.

A concise PostNL Porter's Five Forces one-sheet that highlights shipment industry pressures—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Large E-commerce Platforms and Retailers

Major online retailers like Bol.com, Amazon, and Coolblue ship millions of parcels yearly—Bol.com handled ~50m shipments in 2024—giving them strong leverage to demand lower per-parcel rates from PostNL.

The scale lets them consider alternatives or build in-house logistics; Amazon already runs extensive EU networks, and Coolblue and Bol.com have tested carrier diversification in 2023–25.

This volume-shifting power forces PostNL to keep prices competitive and service levels high; loss of a single major client could cut millions in annual revenue—Bol.com alone accounts for an estimated 5–10% of Dutch parcel volumes in 2024.

Price Sensitivity of Small and Medium Enterprises

SMEs make up about 60% of PostNL’s B2B parcel volume in 2024 but buy too little each to secure bulk discounts, so they remain highly price-sensitive and quick to switch to DHL or DPD if rates rise.

Retention hinges on easy digital tools and 99%+ delivery reliability targets; PostNL’s 2024 SME churn rose 4% after a 6% tariff hike, showing sensitivity.

Individual Consumer Service Expectations

Private consumers demand flexible delivery: 45% in the Netherlands (2024 PostNL survey) prefer evening slots and 60% use pick‑up points; this raises service expectations beyond price sensitivity.

Individually they have low price bargaining power, but their collective choices pushed e‑commerce returns and same‑day options, influencing retailers’ carrier selection.

If PostNL misses these needs, it risks share loss—online retailers shifted 12% of parcel volume to rivals in 2023 for faster, more flexible options.

Corporate and Institutional Mail Clients

Corporate and institutional clients like banks and government agencies have become scarce and thus more valuable as Dutch letter volumes fell 9.3% in 2024; they frequently consolidate mail and run tenders to secure lowest-cost, reliable delivery, raising PostNL’s bargaining pressure.

PostNL’s unit cost per item rises as volumes decline—letter volumes down to ~1.2 billion in 2024—forcing discounts on large contracts while squeezing margins on transactional mail.

- Clients: banks, government—high value

- Tenders drive price pressure

- 2024 letter volumes ~1.2bn (-9.3%)

- Unit cost up as volumes fall, margin squeeze

Switching Costs for Business Integration

- High current stickiness from direct API integrations

- Switch cost = IT resources + operational disruption

- Standardized platforms (28% adoption in NL, 2024) lower costs

- Net effect: modest rise in customer power

Delivery power shifts: big e‑tailers & SMEs force discounts, flexible pick‑up rises

Large e‑tailers (Bol.com ~50m parcels 2024; Bol.com = ~5–10% Dutch volume) and SMEs (60% B2B volume) drive price sensitivity; major clients can switch or insource, forcing discounts. Consumer demand for flexible delivery (45% evening, 60% pick‑up points, 2024) raises service expectations. API integrations create stickiness, but 28% multi‑carrier middleware adoption (2024) nudges switching up.

| Metric | 2024 |

|---|---|

| Bol.com parcels | ~50m |

| Bol.com share | 5–10% |

| SME B2B share | 60% |

| Pick‑up preference | 60% |

| Multi‑carrier middleware | 28% |

Preview Before You Purchase

PostNL Porter's Five Forces Analysis

This preview shows the exact PostNL Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or mockups.