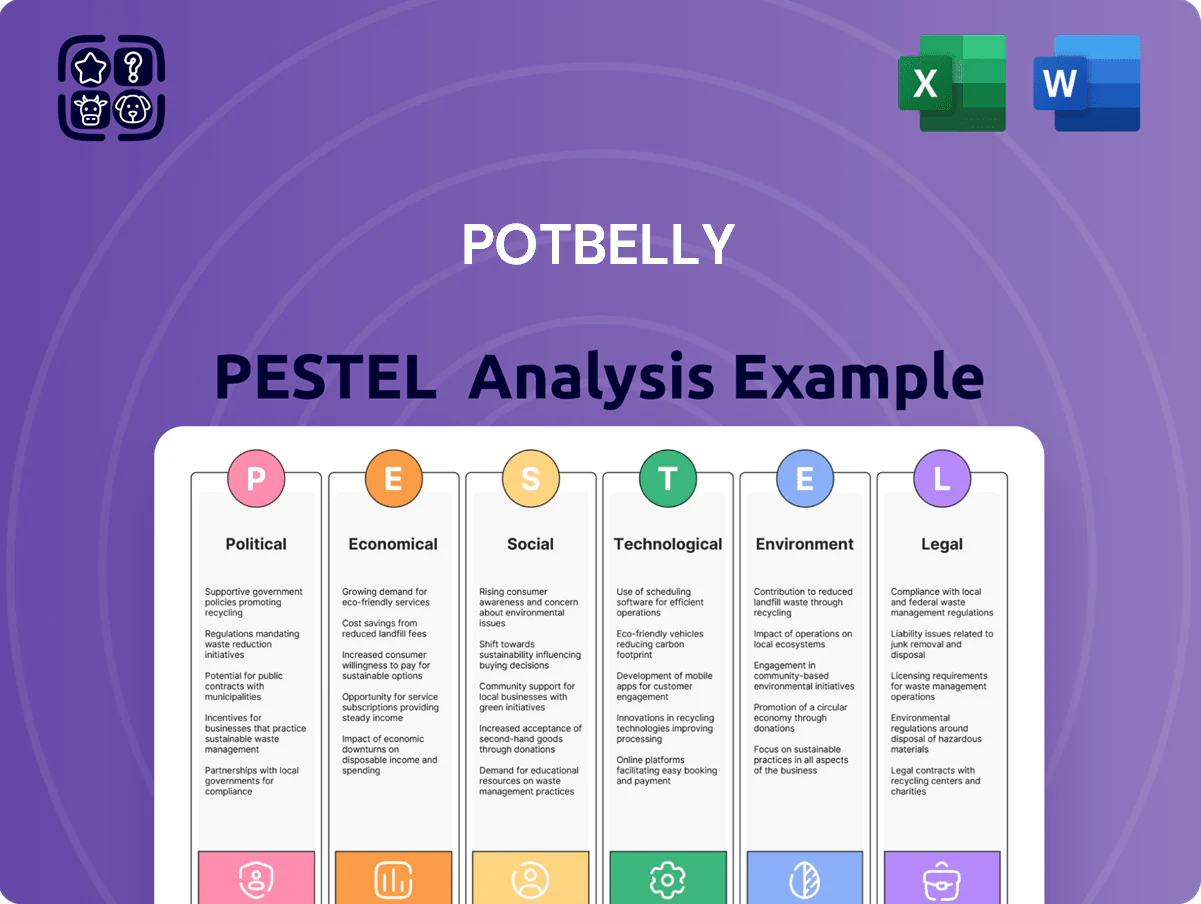

Potbelly PESTLE Analysis

Skip the Research. Get the Strategy.

Uncover how political shifts, economic pressures, and tech trends are reshaping Potbelly’s growth prospects—our concise PESTLE snapshot highlights risks and opportunities you need to know; purchase the full analysis for a detailed, ready-to-use report to inform investment or strategic decisions.

Political factors

Federal and State Minimum Wage Policies

As of late 2025, Potbelly faces rising labor costs as 22 states and numerous cities have minimum wages at or above $15 — with California at $16 and New York City at $15.50 — pushing company-wide hourly payroll up an estimated 6–9% year-over-year for corporate stores.

Varying state hikes force Potbelly to consider menu price increases; a 3–5% price adjustment could be required to protect EBITDA margins, given labor is ~28% of store-level operating costs.

Management must manage a regulatory patchwork affecting both corporate and franchised units, where franchisees in high-wage jurisdictions report compressed margins and increased requests for royalty relief or localized pricing flexibility.

Trade Policies and Import Tariffs

Changes in international trade agreements and recent US tariff actions — tariffs rose on select appliances and food imports by up to 10–25% in 2024 in some categories — can increase costs for Potbelly’s kitchen equipment and specialty ingredients, squeezing margins given company gross margin of about 20.5% in FY2024.

Corporate Tax Regulation

The 2025 US corporate tax environment, with an effective federal rate around 21% and combined state rates averaging ~6%, directly reduces Potbelly’s net margins and limits cash available for its ~ $50k–$150k per-store renovation investments.

Proposed 2024–25 federal small business tax credits and enhanced franchise expensing debated in Congress could raise franchisee ROI by several percentage points, affecting expansion interest.

Potbelly’s financial planning is sensitive to federal fiscal shifts—hospitality tax burden changes of 1–2 percentage points could move annual taxable income by millions relative to 2024 revenue levels (~$600M).

Healthcare Mandates and Employee Benefits

- 2024 employer premium avg: 12,000 USD per FT employee

- Franchise labor cost growth: ~4% YoY

- Operating margin 2024: ~6%

Geopolitical Stability and Supply Chain Security

Global political instability raises risk of supply disruptions for Potbelly, which sources specialty ingredients and energy-sensitive supplies; 2024 logistics cost pressures rose 12% YoY in US foodservice, heightening vulnerability to fuel price shocks.

Potbelly’s dependence on stable domestic and international routes exposes margins to unrest-driven delays and higher freight costs—fuel surcharges contributed up to 2–3% operating expense swings in comparable chains in 2023–24.

Maintaining a diversified supplier base across regions and contracting strategies is a key mitigation: Potbelly’s procurement team reported expanding supplier count by 18% in 2024 to reduce single-source risk.

- 2024 logistics costs +12% YoY

- Fuel-related opex volatility 2–3%

- Supplier base +18% in 2024

Rising wages, tariffs and logistics squeeze Potbelly margins—labor & costs up, profits tight

Political factors pressuring Potbelly include state/local minimum wages ≥$15 (22 states), rising labor costs (+6–9% corporate payroll), fragmented regulation increasing franchisee relief requests, tariffs up to 10–25% on some imports, FY2024 gross margin ~20.5% and operating margin ~6%, employer health premiums ~$12,000/FT employee, and 2024 logistics costs +12% YoY.

| Metric | 2024/25 Value |

|---|---|

| Min wage ≥$15 states | 22 |

| Labor cost impact | +6–9% |

| Gross margin | ~20.5% |

| Operating margin | ~6% |

| Employer health premium | $12,000 |

| Logistics cost change | +12% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Potbelly across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends for reliable insights.

Condenses Potbelly's PESTLE into a clean, shareable snapshot that highlights key external risks and opportunities for rapid inclusion in presentations or strategy sessions.

Economic factors

Inflationary Pressures on Food Commodities

Rising 2024–25 input costs—beef and poultry up roughly 12–18% year-over-year, dairy +10% and U.S. wheat futures ~20% above 2021 averages—have materially pressured Potbelly’s COGS, contributing to margin compression in 2024 (operating margin down ~150–200 bps). Persistent food inflation forces careful menu pricing to avoid losing price-sensitive core customers while protecting AUVs. Potbelly increasingly relies on strategic sourcing and multi-year supplier contracts to hedge agricultural volatility and cap input exposure.

Consumer Disposable Income Trends

The fast-casual segment is highly sensitive to middle-class discretionary income; US real disposable personal income fell 1.2% year-on-year in Q4 2025, putting pressure on dining-out spend. Economic slowdowns and lower consumer confidence—Gallup consumer confidence averaging 82 in 2025 vs 90 in 2023—drive frequency down and shift patrons to value quick-service options. Potbelly’s expansion relies on stable incomes as average ticket premiums (~20% above QSR) hinge on customers willing to pay for premium sandwiches.

Interest Rate Environment and Capital Costs

Current US benchmark rates (Fed funds 5.25–5.50% as of Dec 2024) raise borrowing costs for Potbelly and franchisees, increasing franchise loan payments and franchise development hurdles.

Higher rates can slow new shop openings and make financing digital/physical upgrades pricier; commercial loan spreads rose in 2024, pushing SME borrowing costs above historical averages.

Potbelly’s multi-year growth plan depends on affordable credit availability—elevated rates constrain capex and franchise expansion cadence in 2025.

Labor Market Tightness and Wage Inflation

Competitive labor markets in the service industry have driven US average hourly earnings up 4.2% year-over-year in 2025, forcing Potbelly to raise wages to attract staff.

Potbelly now competes with fast-casual chains, retail and gig roles—sectors reporting 3–6% pay growth—raising turnover and hiring costs.

This reality requires investments in retention programs and efficiency gains to offset higher payrolls, which comprised ~24% of operating expenses for similar chains in 2024.

- Wage pressure: +4.2% avg hourly earnings (2025)

- Competes with retail/gig sectors (3–6% pay growth)

- Payroll ≈24% of ops costs for peers (2024)

Urbanization and Return-to-Office Dynamics

The economic health of Potbelly is tied to office-worker density in urban centers; pre-2025 data show downtown foot traffic remains ~20–35% below 2019 levels in major U.S. markets, pressuring sales at city stores.

With hybrid work models largely permanent in 2025, Potbelly must realign store formats and hours to capture shifted midday demand and delivery volume.

Rising commercial rents—urban Class A vacancy averaging ~14% in 2024 but with uneven recovery—means higher costs for high-rent locations, impacting margins.

- Urban foot traffic 20–35% below 2019 (major markets, 2024)

- Hybrid work entrenched by 2025—midday demand shifts to delivery/pickup

- Class A vacancy ~14% (2024) → rent pressure on metropolitan sites

Inflation, higher rates and weak traffic squeeze dining margins, pressuring operators

Input inflation (beef +12–18% YoY, dairy +10%, wheat futures +20% vs 2021) squeezed 2024 margins ~150–200bps; Fed funds 5.25–5.50% (Dec 2024) raised borrowing costs; real disposable income down 1.2% YoY (Q4 2025) hit dining spend; avg hourly earnings +4.2% (2025) raised payrolls ~24% of ops for peers; downtown foot traffic 20–35% below 2019.

| Metric | Value |

|---|---|

| Beef/poultry | +12–18% YoY |

| Fed funds | 5.25–5.50% |

| Real DPI | -1.2% Q4 2025 |

| Avg hourly | +4.2% (2025) |

| Downtown traffic | -20–35% vs 2019 |

Preview Before You Purchase

Potbelly PESTLE Analysis

The preview shown here is the exact Potbelly PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Uncover how political shifts, economic pressures, and tech trends are reshaping Potbelly’s growth prospects—our concise PESTLE snapshot highlights risks and opportunities you need to know; purchase the full analysis for a detailed, ready-to-use report to inform investment or strategic decisions.

Political factors

Federal and State Minimum Wage Policies

As of late 2025, Potbelly faces rising labor costs as 22 states and numerous cities have minimum wages at or above $15 — with California at $16 and New York City at $15.50 — pushing company-wide hourly payroll up an estimated 6–9% year-over-year for corporate stores.

Varying state hikes force Potbelly to consider menu price increases; a 3–5% price adjustment could be required to protect EBITDA margins, given labor is ~28% of store-level operating costs.

Management must manage a regulatory patchwork affecting both corporate and franchised units, where franchisees in high-wage jurisdictions report compressed margins and increased requests for royalty relief or localized pricing flexibility.

Trade Policies and Import Tariffs

Changes in international trade agreements and recent US tariff actions — tariffs rose on select appliances and food imports by up to 10–25% in 2024 in some categories — can increase costs for Potbelly’s kitchen equipment and specialty ingredients, squeezing margins given company gross margin of about 20.5% in FY2024.

Corporate Tax Regulation

The 2025 US corporate tax environment, with an effective federal rate around 21% and combined state rates averaging ~6%, directly reduces Potbelly’s net margins and limits cash available for its ~ $50k–$150k per-store renovation investments.

Proposed 2024–25 federal small business tax credits and enhanced franchise expensing debated in Congress could raise franchisee ROI by several percentage points, affecting expansion interest.

Potbelly’s financial planning is sensitive to federal fiscal shifts—hospitality tax burden changes of 1–2 percentage points could move annual taxable income by millions relative to 2024 revenue levels (~$600M).

Healthcare Mandates and Employee Benefits

- 2024 employer premium avg: 12,000 USD per FT employee

- Franchise labor cost growth: ~4% YoY

- Operating margin 2024: ~6%

Geopolitical Stability and Supply Chain Security

Global political instability raises risk of supply disruptions for Potbelly, which sources specialty ingredients and energy-sensitive supplies; 2024 logistics cost pressures rose 12% YoY in US foodservice, heightening vulnerability to fuel price shocks.

Potbelly’s dependence on stable domestic and international routes exposes margins to unrest-driven delays and higher freight costs—fuel surcharges contributed up to 2–3% operating expense swings in comparable chains in 2023–24.

Maintaining a diversified supplier base across regions and contracting strategies is a key mitigation: Potbelly’s procurement team reported expanding supplier count by 18% in 2024 to reduce single-source risk.

- 2024 logistics costs +12% YoY

- Fuel-related opex volatility 2–3%

- Supplier base +18% in 2024

Rising wages, tariffs and logistics squeeze Potbelly margins—labor & costs up, profits tight

Political factors pressuring Potbelly include state/local minimum wages ≥$15 (22 states), rising labor costs (+6–9% corporate payroll), fragmented regulation increasing franchisee relief requests, tariffs up to 10–25% on some imports, FY2024 gross margin ~20.5% and operating margin ~6%, employer health premiums ~$12,000/FT employee, and 2024 logistics costs +12% YoY.

| Metric | 2024/25 Value |

|---|---|

| Min wage ≥$15 states | 22 |

| Labor cost impact | +6–9% |

| Gross margin | ~20.5% |

| Operating margin | ~6% |

| Employer health premium | $12,000 |

| Logistics cost change | +12% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Potbelly across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends for reliable insights.

Condenses Potbelly's PESTLE into a clean, shareable snapshot that highlights key external risks and opportunities for rapid inclusion in presentations or strategy sessions.

Economic factors

Inflationary Pressures on Food Commodities

Rising 2024–25 input costs—beef and poultry up roughly 12–18% year-over-year, dairy +10% and U.S. wheat futures ~20% above 2021 averages—have materially pressured Potbelly’s COGS, contributing to margin compression in 2024 (operating margin down ~150–200 bps). Persistent food inflation forces careful menu pricing to avoid losing price-sensitive core customers while protecting AUVs. Potbelly increasingly relies on strategic sourcing and multi-year supplier contracts to hedge agricultural volatility and cap input exposure.

Consumer Disposable Income Trends

The fast-casual segment is highly sensitive to middle-class discretionary income; US real disposable personal income fell 1.2% year-on-year in Q4 2025, putting pressure on dining-out spend. Economic slowdowns and lower consumer confidence—Gallup consumer confidence averaging 82 in 2025 vs 90 in 2023—drive frequency down and shift patrons to value quick-service options. Potbelly’s expansion relies on stable incomes as average ticket premiums (~20% above QSR) hinge on customers willing to pay for premium sandwiches.

Interest Rate Environment and Capital Costs

Current US benchmark rates (Fed funds 5.25–5.50% as of Dec 2024) raise borrowing costs for Potbelly and franchisees, increasing franchise loan payments and franchise development hurdles.

Higher rates can slow new shop openings and make financing digital/physical upgrades pricier; commercial loan spreads rose in 2024, pushing SME borrowing costs above historical averages.

Potbelly’s multi-year growth plan depends on affordable credit availability—elevated rates constrain capex and franchise expansion cadence in 2025.

Labor Market Tightness and Wage Inflation

Competitive labor markets in the service industry have driven US average hourly earnings up 4.2% year-over-year in 2025, forcing Potbelly to raise wages to attract staff.

Potbelly now competes with fast-casual chains, retail and gig roles—sectors reporting 3–6% pay growth—raising turnover and hiring costs.

This reality requires investments in retention programs and efficiency gains to offset higher payrolls, which comprised ~24% of operating expenses for similar chains in 2024.

- Wage pressure: +4.2% avg hourly earnings (2025)

- Competes with retail/gig sectors (3–6% pay growth)

- Payroll ≈24% of ops costs for peers (2024)

Urbanization and Return-to-Office Dynamics

The economic health of Potbelly is tied to office-worker density in urban centers; pre-2025 data show downtown foot traffic remains ~20–35% below 2019 levels in major U.S. markets, pressuring sales at city stores.

With hybrid work models largely permanent in 2025, Potbelly must realign store formats and hours to capture shifted midday demand and delivery volume.

Rising commercial rents—urban Class A vacancy averaging ~14% in 2024 but with uneven recovery—means higher costs for high-rent locations, impacting margins.

- Urban foot traffic 20–35% below 2019 (major markets, 2024)

- Hybrid work entrenched by 2025—midday demand shifts to delivery/pickup

- Class A vacancy ~14% (2024) → rent pressure on metropolitan sites

Inflation, higher rates and weak traffic squeeze dining margins, pressuring operators

Input inflation (beef +12–18% YoY, dairy +10%, wheat futures +20% vs 2021) squeezed 2024 margins ~150–200bps; Fed funds 5.25–5.50% (Dec 2024) raised borrowing costs; real disposable income down 1.2% YoY (Q4 2025) hit dining spend; avg hourly earnings +4.2% (2025) raised payrolls ~24% of ops for peers; downtown foot traffic 20–35% below 2019.

| Metric | Value |

|---|---|

| Beef/poultry | +12–18% YoY |

| Fed funds | 5.25–5.50% |

| Real DPI | -1.2% Q4 2025 |

| Avg hourly | +4.2% (2025) |

| Downtown traffic | -20–35% vs 2019 |

Preview Before You Purchase

Potbelly PESTLE Analysis

The preview shown here is the exact Potbelly PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investor review.