PotlatchDeltic Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

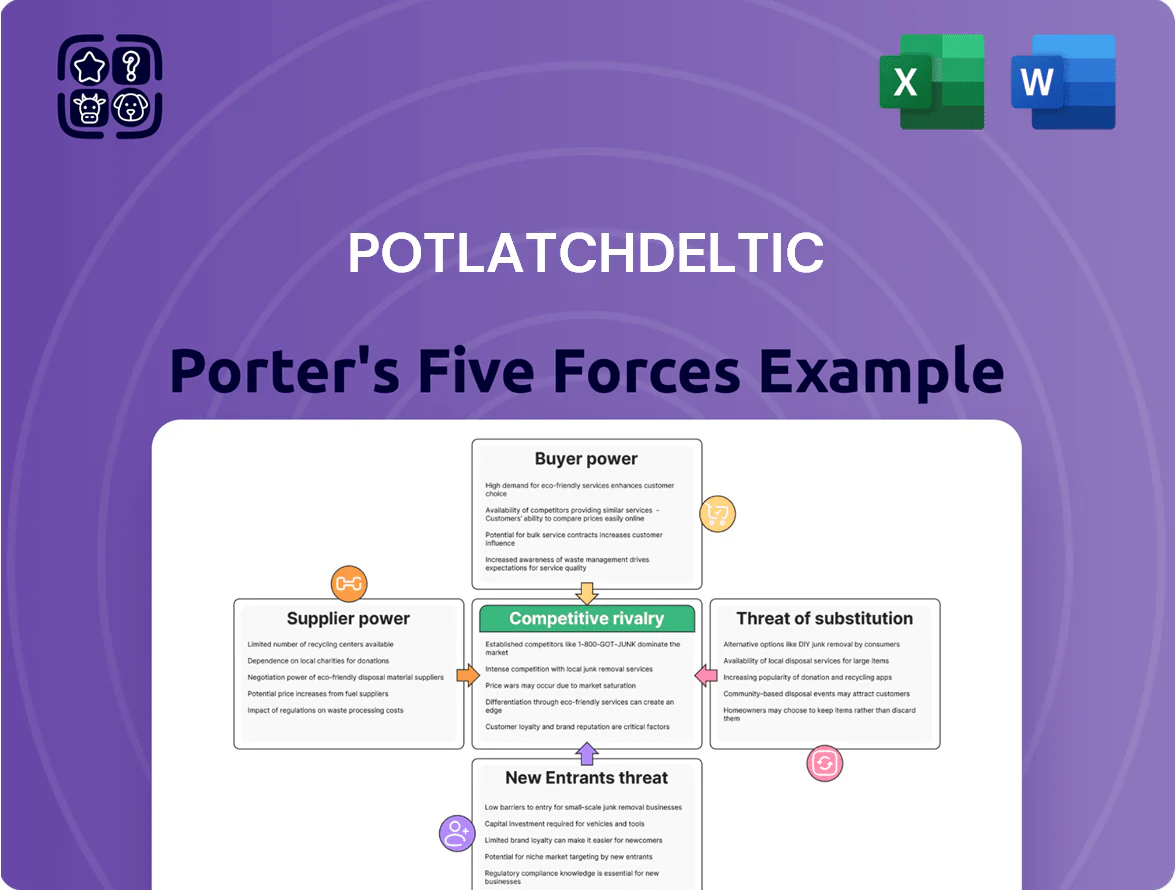

PotlatchDeltic faces moderate competitive rivalry driven by a concentrated forest products market and cyclical timber prices, while supplier power is tempered by vertical integration and long-term timber contracts.

Buyer power is moderate—large pulp, paper, and real estate buyers exert pressure, but differentiated land assets and sustainable certifications provide some pricing leverage.

Barriers to entry are significant due to capital intensity, land access, and regulatory hurdles, though niche entrants and biomass substitutes pose limited threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PotlatchDeltic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Timber Resources

PotlatchDeltic owns about 2.2 million acres of timberland, cutting supplier power by internally sourcing an estimated 60–70% of its harvestable logs (2024 harvest data).

Owning land reduces exposure to market log-price swings; average sawlog prices rose ~12% in 2023, but PotlatchDeltic’s cost volatility stayed lower, supporting a steadier gross margin.

This vertical integration gives PotlatchDeltic a cost and supply advantage versus non-integrated competitors who must bid against third-party landowners.

Reliance on Contract Logging and Hauling

PotlatchDeltic owns the timber but depends on independent contractors for harvesting and hauling, giving those suppliers leverage when crews are scarce or diesel spikes; diesel futures rose ~40% in 2024–25, raising hauling costs. If skilled logging crews fall below 2023 levels (estimated 15–20% decline in some U.S. regions in 2025), PotlatchDeltic may face 10–25% higher contractor rates to secure capacity. This reliance raises input-cost volatility and operational risk.

Energy and Chemical Input Costs

Suppliers of electricity, natural gas, and resins hold moderate bargaining power for PotlatchDeltic because prices track global energy markets; in 2024 US industrial natural gas spot prices averaged about 3.50 USD/MMBtu and crude-derived resin feedstock costs rose ~12% year-over-year, constraining plywood margins.

PotlatchDeltic hedges energy exposure and targets ~3–5% annual manufacturing efficiency gains to offset volatility; if hedges cover <50% of usage, a 20% input spike could cut segment EBITDA by roughly 4–6%.

Heavy Equipment and Technology Providers

PotlatchDeltic relies on a few global manufacturers—notably John Deere and Caterpillar—for specialized forestry harvesters and sawmill equipment; these capital purchases can cost $500k–$5m per unit and represent a meaningful share of annual capital expenditure (2024 capex ~ $120m).

Because equipment needs ongoing OEM support, software updates, and OEM-certified parts, suppliers keep long-term bargaining leverage that limits PotlatchDeltic’s ability to switch quickly or cut costs.

- Few suppliers: raises dependency risk

- Unit cost: $500k–$5m each

- 2024 capex: ~$120m

- OEM support: long-term leverage

Regulatory and Environmental Oversight

Government agencies act like suppliers by granting permits and environmental certifications that enable PotlatchDeltic’s timber harvests; as of 2025, delayed permitting added 12–18 months on average, constraining throughput and cash flow.

Mandatory Sustainable Forestry Initiative (SFI) compliance affects market access and limits harvestable acres; 2024 SFI audits showed 98% certification on company lands, but recertification costs rose ~15% YoY.

Federal/state land-use changes can cut available supply or raise costs to keep REIT status—estimated regulatory compliance and land-use costs were $28–34 million in 2024, a 9% increase vs. 2023.

- Permitting delays: +12–18 months

- SFI certified acres: 98% (2024)

- Recertification cost rise: ~15% YoY

- Regulatory costs: $28–34M (2024), +9% YoY

Vertical integration shields margins but contractor, fuel and permitting risks rise

Vertical integration—2.2M acres, 60–70% self-sourced (2024)—cuts supplier power, lowering log-price exposure; sawlog volatility reduced gross-margin swings. Contractor dependence for harvesting/hauling and OEM equipment ($500k–$5m/unit; 2024 capex ~$120m) gives suppliers leverage, especially with crew shortages and 40% diesel futures rise (2024–25). Permitting delays (12–18 months) and SFI costs (+15% YoY) add regulatory supplier risk.

| Metric | 2024–25 |

|---|---|

| Timberland owned | 2.2M acres |

| Self-sourced logs | 60–70% |

| 2024 capex | $120M |

| Diesel futures change | +40% |

| Permitting delay | 12–18 months |

What is included in the product

Tailored exclusively for PotlatchDeltic, this Porter’s Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise PotlatchDeltic Porter's Five Forces one-sheet that highlights timberland-specific competitive pressures—ready for rapid board decisions and slide decks.

Customers Bargaining Power

Concentration of Big Box Retailers

About 30% of U.S. manufactured wood products flow through big-box chains like Home Depot and Lowe’s, so these buyers push hard on prices and delivery—PotlatchDeltic reported $1.8B net sales in 2024, making retention of large wholesale contracts critical; losing favorable terms could cut margins several percentage points. PotlatchDeltic must match service levels, same-week shipments, and competitive mill-gate pricing to keep these high-volume accounts.

Sensitivity to Housing Market Cycles

Primary customers—residential homebuilders and land developers—are highly rate-sensitive; US mortgage-rate hikes to ~7% in Oct 2025 cut single-family starts 18% y/y by Q4 2025, weakening lumber demand and boosting buyer leverage to push prices down.

Commodity Nature of Wood Products

Standardized lumber and plywood grades are traded as commodities, so buyers switch suppliers mainly on price; this keeps PotlatchDeltic’s bargaining power low. In 2024 the US softwood lumber benchmark averaged about $420/MBF, reinforcing price sensitivity in industrial demand. With limited brand differentiation in structural wood, PotlatchDeltic cannot sustain wide price premiums and must target low-cost production and scale to protect margins.

Rural Land Buyer Selectivity

Buyers of rural timberland and recreational parcels can shop nationwide; USDA data show private forestland transfers varied 10–15% year-over-year in 2023, so price misalignment pushes buyers to delay or pick cheaper regions.

Because recreational land is discretionary, purchasers often treat it as optional investment: PotlatchDeltic faces high buyer leverage when inventory exceeds demand—average lot sales times rose 22% in 2024 in secondary markets.

- Wide geographic substitutes increase price sensitivity

- Purchases are postponable—raises bargaining power

- Discretionary demand makes sales elastic—higher markdown risk

Wholesale and Industrial Distribution Channels

Large industrial buyers and wood wholesalers buy in bulk and pit suppliers against each other, squeezing PotlatchDeltic’s margins; in 2024 pulpwood and lumber spot prices fell ~12% YoY, boosting buyer leverage.

These buyers track global timber indices (e.g., Random Lengths) and demand transparent, contract-level pricing; PotlatchDeltic faces substitution risk from imports—US softwood lumber imports rose ~8% in 2024.

Their international sourcing and regional alternatives keep price pressure on PotlatchDeltic’s sales mix; net sales per ton declined modestly in 2024, reflecting this pressure.

- Buyers buy bulk, play suppliers

- Track Random Lengths indices

- US softwood imports +8% (2024)

- Spot prices -12% YoY (2024)

- Net sales/ton fell in 2024

PotlatchDeltic faces margin squeeze as lumber prices fall and land sales slow

Large retail chains and builders control volumes—PotlatchDeltic’s $1.8B 2024 sales hinge on retaining big accounts; commodity lumber (avg $420/MBF in 2024) and US softwood imports +8% (2024) keep buyers price-sensitive, squeezing margins as spot prices fell ~12% YoY. Recreational land sales slowed (lot sale times +22% in 2024), increasing postponement risk and buyer leverage.

| Metric | 2024/2025 |

|---|---|

| Net sales | $1.8B (2024) |

| Avg softwood price | $420/MBF (2024) |

| Spot price change | -12% YoY (2024) |

| US softwood imports | +8% (2024) |

| Lot sale times | +22% (2024) |

Preview the Actual Deliverable

PotlatchDeltic Porter's Five Forces Analysis

This preview shows the exact PortlatchDeltic Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you can download and use the moment you buy.

You’re previewing the final deliverable: the ready-to-use analysis document available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

PotlatchDeltic faces moderate competitive rivalry driven by a concentrated forest products market and cyclical timber prices, while supplier power is tempered by vertical integration and long-term timber contracts.

Buyer power is moderate—large pulp, paper, and real estate buyers exert pressure, but differentiated land assets and sustainable certifications provide some pricing leverage.

Barriers to entry are significant due to capital intensity, land access, and regulatory hurdles, though niche entrants and biomass substitutes pose limited threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PotlatchDeltic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Timber Resources

PotlatchDeltic owns about 2.2 million acres of timberland, cutting supplier power by internally sourcing an estimated 60–70% of its harvestable logs (2024 harvest data).

Owning land reduces exposure to market log-price swings; average sawlog prices rose ~12% in 2023, but PotlatchDeltic’s cost volatility stayed lower, supporting a steadier gross margin.

This vertical integration gives PotlatchDeltic a cost and supply advantage versus non-integrated competitors who must bid against third-party landowners.

Reliance on Contract Logging and Hauling

PotlatchDeltic owns the timber but depends on independent contractors for harvesting and hauling, giving those suppliers leverage when crews are scarce or diesel spikes; diesel futures rose ~40% in 2024–25, raising hauling costs. If skilled logging crews fall below 2023 levels (estimated 15–20% decline in some U.S. regions in 2025), PotlatchDeltic may face 10–25% higher contractor rates to secure capacity. This reliance raises input-cost volatility and operational risk.

Energy and Chemical Input Costs

Suppliers of electricity, natural gas, and resins hold moderate bargaining power for PotlatchDeltic because prices track global energy markets; in 2024 US industrial natural gas spot prices averaged about 3.50 USD/MMBtu and crude-derived resin feedstock costs rose ~12% year-over-year, constraining plywood margins.

PotlatchDeltic hedges energy exposure and targets ~3–5% annual manufacturing efficiency gains to offset volatility; if hedges cover <50% of usage, a 20% input spike could cut segment EBITDA by roughly 4–6%.

Heavy Equipment and Technology Providers

PotlatchDeltic relies on a few global manufacturers—notably John Deere and Caterpillar—for specialized forestry harvesters and sawmill equipment; these capital purchases can cost $500k–$5m per unit and represent a meaningful share of annual capital expenditure (2024 capex ~ $120m).

Because equipment needs ongoing OEM support, software updates, and OEM-certified parts, suppliers keep long-term bargaining leverage that limits PotlatchDeltic’s ability to switch quickly or cut costs.

- Few suppliers: raises dependency risk

- Unit cost: $500k–$5m each

- 2024 capex: ~$120m

- OEM support: long-term leverage

Regulatory and Environmental Oversight

Government agencies act like suppliers by granting permits and environmental certifications that enable PotlatchDeltic’s timber harvests; as of 2025, delayed permitting added 12–18 months on average, constraining throughput and cash flow.

Mandatory Sustainable Forestry Initiative (SFI) compliance affects market access and limits harvestable acres; 2024 SFI audits showed 98% certification on company lands, but recertification costs rose ~15% YoY.

Federal/state land-use changes can cut available supply or raise costs to keep REIT status—estimated regulatory compliance and land-use costs were $28–34 million in 2024, a 9% increase vs. 2023.

- Permitting delays: +12–18 months

- SFI certified acres: 98% (2024)

- Recertification cost rise: ~15% YoY

- Regulatory costs: $28–34M (2024), +9% YoY

Vertical integration shields margins but contractor, fuel and permitting risks rise

Vertical integration—2.2M acres, 60–70% self-sourced (2024)—cuts supplier power, lowering log-price exposure; sawlog volatility reduced gross-margin swings. Contractor dependence for harvesting/hauling and OEM equipment ($500k–$5m/unit; 2024 capex ~$120m) gives suppliers leverage, especially with crew shortages and 40% diesel futures rise (2024–25). Permitting delays (12–18 months) and SFI costs (+15% YoY) add regulatory supplier risk.

| Metric | 2024–25 |

|---|---|

| Timberland owned | 2.2M acres |

| Self-sourced logs | 60–70% |

| 2024 capex | $120M |

| Diesel futures change | +40% |

| Permitting delay | 12–18 months |

What is included in the product

Tailored exclusively for PotlatchDeltic, this Porter’s Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise PotlatchDeltic Porter's Five Forces one-sheet that highlights timberland-specific competitive pressures—ready for rapid board decisions and slide decks.

Customers Bargaining Power

Concentration of Big Box Retailers

About 30% of U.S. manufactured wood products flow through big-box chains like Home Depot and Lowe’s, so these buyers push hard on prices and delivery—PotlatchDeltic reported $1.8B net sales in 2024, making retention of large wholesale contracts critical; losing favorable terms could cut margins several percentage points. PotlatchDeltic must match service levels, same-week shipments, and competitive mill-gate pricing to keep these high-volume accounts.

Sensitivity to Housing Market Cycles

Primary customers—residential homebuilders and land developers—are highly rate-sensitive; US mortgage-rate hikes to ~7% in Oct 2025 cut single-family starts 18% y/y by Q4 2025, weakening lumber demand and boosting buyer leverage to push prices down.

Commodity Nature of Wood Products

Standardized lumber and plywood grades are traded as commodities, so buyers switch suppliers mainly on price; this keeps PotlatchDeltic’s bargaining power low. In 2024 the US softwood lumber benchmark averaged about $420/MBF, reinforcing price sensitivity in industrial demand. With limited brand differentiation in structural wood, PotlatchDeltic cannot sustain wide price premiums and must target low-cost production and scale to protect margins.

Rural Land Buyer Selectivity

Buyers of rural timberland and recreational parcels can shop nationwide; USDA data show private forestland transfers varied 10–15% year-over-year in 2023, so price misalignment pushes buyers to delay or pick cheaper regions.

Because recreational land is discretionary, purchasers often treat it as optional investment: PotlatchDeltic faces high buyer leverage when inventory exceeds demand—average lot sales times rose 22% in 2024 in secondary markets.

- Wide geographic substitutes increase price sensitivity

- Purchases are postponable—raises bargaining power

- Discretionary demand makes sales elastic—higher markdown risk

Wholesale and Industrial Distribution Channels

Large industrial buyers and wood wholesalers buy in bulk and pit suppliers against each other, squeezing PotlatchDeltic’s margins; in 2024 pulpwood and lumber spot prices fell ~12% YoY, boosting buyer leverage.

These buyers track global timber indices (e.g., Random Lengths) and demand transparent, contract-level pricing; PotlatchDeltic faces substitution risk from imports—US softwood lumber imports rose ~8% in 2024.

Their international sourcing and regional alternatives keep price pressure on PotlatchDeltic’s sales mix; net sales per ton declined modestly in 2024, reflecting this pressure.

- Buyers buy bulk, play suppliers

- Track Random Lengths indices

- US softwood imports +8% (2024)

- Spot prices -12% YoY (2024)

- Net sales/ton fell in 2024

PotlatchDeltic faces margin squeeze as lumber prices fall and land sales slow

Large retail chains and builders control volumes—PotlatchDeltic’s $1.8B 2024 sales hinge on retaining big accounts; commodity lumber (avg $420/MBF in 2024) and US softwood imports +8% (2024) keep buyers price-sensitive, squeezing margins as spot prices fell ~12% YoY. Recreational land sales slowed (lot sale times +22% in 2024), increasing postponement risk and buyer leverage.

| Metric | 2024/2025 |

|---|---|

| Net sales | $1.8B (2024) |

| Avg softwood price | $420/MBF (2024) |

| Spot price change | -12% YoY (2024) |

| US softwood imports | +8% (2024) |

| Lot sale times | +22% (2024) |

Preview the Actual Deliverable

PotlatchDeltic Porter's Five Forces Analysis

This preview shows the exact PortlatchDeltic Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you can download and use the moment you buy.

You’re previewing the final deliverable: the ready-to-use analysis document available instantly after payment.